A Structural Growth Story We're Very Bullish On

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

25February 2020 India Daily

INDIA DAILY February 25, 2020 India 24-Feb 1-day 1-mo 3-mo Sensex 40,363 (2.0) (3.0) (1.3) Nifty 11,829 (2.1) (3.4) (2.0) Contents Global/Regional indices Dow Jones 27,961 (3.6) (3.5) (0.4) Special Reports Nasdaq Composite 9,221 (3.7) (1.0) 6.8 FTSE 7,157 (3.3) (5.7) (3.2) Initiating Coverage Nikkei 22,684 (3.0) (4.8) (1.9) GMR Infrastructure: Poised for flight Hang Seng 26,849 0.1 (3.9) (0.5) Initiate coverage on GMRI with a BUY rating and fair value of Rs30/share KOSPI 2,097 0.9 (6.6) (1.2) Mar-21 SoTP Value traded – India Cash (NSE+BSE) 411 412 244 GMRI: Banking on increasing relevance of airports and of non-aero Derivatives (NSE) 12,813 9,719 7,715 revenues Deri. open interest 3,875 3,756 3,409 Financials: Expect 4-year CAGR of 12% in EBITDA, FCF generation beyond FY2022 Forex/money market Key risks: Changes in the shape or timeline of airport monetization deal Change, basis points Daily Alerts 24-Feb 1-day 1-mo 3-mo Rs/US$ 71.9 (17) 43 20 Sector alerts 10yr govt bond, % 6.7 (4) (33) (30) Insurance: Fire and motor TP recover Net investment (US$ mn) 20-Feb MTD CYTD Motor TP picks up in January 2020; motor OD growth steady FIIs 117 2,239 3,612 Retail health steady, but group health moderates MFs 98 235 (140) Top movers Crop business flat yoy in January 2020; up 28% yoy in YTD FY2020 Change, % Best performers 24-Feb 1-day 1-mo 3-mo DMART IN Equity 2,390 (3.0) 22.6 30.0 IHFL IN Equity 331 (2.2) 2.6 27.5 APHS IN Equity 1,797 (0.2) 7.7 23.9 DIVI IN Equity 2,160 (0.4) 13.1 22.5 TGBL IN Equity 369 (3.0) (4.0) 22.2 Worst performers YES IN Equity 35 (1.4) (18.3) (45.2) BHEL IN Equity 34 (3.4) (24.7) (39.6) EDEL IN Equity 93 3.5 0.5 (27.7) HPCL IN Equity 216 (2.8) (11.7) (26.9) ONGC IN Equity 98 (4.6) (17.2) (25.1) [email protected] Contact: +91 22 6218 6427 For Private Circulation Only. -

Inner 49 Retirement Savings Fund

Modera erate tely Mod High to e H w at ig o er h L d o M V e r y w H Tata Retirement Savings Fund - Moderate Plan o i L g (An open ended retirement solution oriented scheme having a lock-in of 5 years or till retirement age (whichever is earlier)) h Riskometer Investors understand that their principal As on 30th June 2021 PORTFOLIO will be at Very High Risk INVESTMENT STYLE Company name No. of Market Value % of Company name No. of Market Value % of A Fund that aims to provide an investment tool for retirement Shares Rs. Lakhs Assets Shares Rs. Lakhs Assets planning to suit the risk profile of the investor. Equity & Equity Related Total 119762.82 81.89 Software INVESTMENT OBJECTIVE Auto Tata Consultancy Services Ltd. 165000 5520.49 3.77 To provide a financial planning tool for long term financial Eicher Motors Ltd. 64000 1709.54 1.17 Infosys Ltd. 345000 5453.76 3.73 security for investors based on their retirement planning goals. Bajaj Auto Ltd. 38500 1591.53 1.09 HCL Technologies Ltd. 345000 3393.08 2.32 However, there can be no assurance that the investment Banks Oracle Financials Services Soft Ltd. 60050 2192.73 1.50 objective of the fund will be realized, as actual market ICICI Bank Ltd. 1503000 9482.43 6.48 Birlasoft Ltd. 400000 1598.40 1.09 movements may be at variance with anticipated trends. HDFC Bank Ltd. 580000 8687.82 5.94 Other Equities^ 16009.86 10.95 DATE OF ALLOTMENT Kotak Mahindra Bank Ltd. -

Market Outlook

November 4, 2019 Derivatives Thematic Report – • PRODUCT 1 Stocks likely to be included in F&O… • PRODUCT 2 Retail Equity Research Equity Retail – Research Analysts Dipesh Dedhia Amit Gupta Securities ICICI [email protected] [email protected] Raj Deepak Singh Nandish Patel [email protected] [email protected] Eligibility criteria of stocks for inclusion in F&O segment The eligibility of a stock for inclusion in the derivatives segment is based on the criteria laid down by Sebi through various circulars issued from time to time. Based on Sebi guidelines, the following criteria has been adopted by the exchange for selecting stocks on which futures & options (F&O) contracts would be introduced. Futures & options contracts may be introduced on new securities, which meet the below mentioned eligibility criteria, subject to approval by Sebi. Thematic Report Thematic 1) The stock shall be chosen from among the top 500 stocks in terms of average daily market capitalisation and average daily traded value in the previous six months on a rolling basis 2) The stock's median quarter-sigma order size over the last six months shall not be less than | 25 lakh. For this purpose, a stock's quarter-sigma order size shall mean the order size (in value terms) required to cause a change in the stock price equal to one-quarter of a standard deviation 3) The market wide position limit in the stock shall not be less than | 500 crore on a rolling basis. The market wide position limit (number of shares) shall be valued taking the closing price of stocks in the underlying cash market on the date of expiry of contract in the month. -

Axis-Max Life Strategic Partnership: Will It Be a Win-Win Game for Both Players?

Amity Journal of Commerce and Financial Review Jasuja, D. Axis-Max Life Strategic Partnership: Will it be a Win-Win Game for Both Players? 1 Deepmala Jasuja Abstract Max Life, one of the prominent life insurer in Indian Insurance space was always considered as an outcast in the league of hallowed names but was never allowed to dictate its terms. Now, the fortunes seem to have changed. After failed merger attempt with HDFC LIFE in 2017, Max Life finally rolled its dice well. Recently, Axis Bank signed a pact with Max Life to strengthen their decade old relationship by acquiring 29% stake in its shareholding. This exclusive agreement is set to enter into a long time strategic relationship. The mentioned stake costs for a consideration of about 1600 crores, priced at the book value of Max Life. The boards of both the companies have given a green signal. Experts wondered if this alliance would succeed. Will this strategic move of Bancassurance partnership make Max life an impregnable lead in the Indian life insurance market space? Will it be a win-win game for both the players? Keywords: Max Life, HDFC Life, strategic partnership A Case Study: The Indian insurance sector seems to be in a state of transition. While there has been a significant change in the operations after opening up of FDI in insurance sector, still India largely remains an under-explored market. The competitive edge of life insurers is largely dependent on their distribution network system, adoption of modern technology like block chain, IOT and Artificial Intelligence to foster sustainable growth in future. -

Motilal Oswal Nifty Smallcap 250 Index Fund (MOFSMALLCAP) (An Open Ended Scheme Replicating / Tracking Nifty Smallcap 250 Index)

FACT SHEETth As on 30 April 2021 BUY RIGHT : SIT TIGHT Buying quality companies and riding their growth cycle Motilal Oswal Focused 25 Fund (MOF25) (An open ended equity scheme investing in maximum 25 stocks intending to focus on Large Cap stocks) Investment Objective Performance (As on 30-April-2021) The investment objective of the Scheme is to achieve long term capital appreciation by 1 Year 3 Year 5 Year Since Inception investing in up to 25 companies with long term Current Value Current Value Current Value Current Value sustainable competitive advantage and CAGR of Investment CAGR of Investment CAGR of Investment CAGR of Investment growth potential. However, there can be no (%) of ` 10,000 (%) of ` 10,000 (%) of ` 10,000 (%) of ` 10,000 assurance or guarantee that the investment 38.7 13,865 10.4 13,465 13.9 19,225 14.5 29,354 objective of the Scheme would be achieved. Scheme Nifty 50 TRI (Benchmark) Benchmark 49.9 14,989 12.2 14,135 14.7 19,869 13.3 27,015 Nifty 50 TRI S&P BSE Sensex TRI (Additional Benchmark) 46.3 14,626 12.9 14,377 15.1 20,260 13.6 27,579 Continuous Offer NAV (`) Per Unit 21.1712 21.8001 15.2688 10.0000 Minimum Application Amount : ` 500/- and in (29.3541 : as on 30-Apr-2021) multiples of `1 /- thereafter. Date of inception: 13-May-13. = Incase, the start/end date of the concerned period is non business date (NBD), the NAV of the previous date is considered for Additional Application Amount : ` 500/- and in computation of returns. -

ICICI LOMBARD Lemonade from Lemons

RESULT UPDATE ICICI LOMBARD Lemonade from lemons India Equity Research| Banking and Financial Services ICICI Lombard’s Q1FY21 PAT jumped 28.5% YoY to INR3.98bn. However, EDELWEISS 4D RATINGS gross direct premium income (GDPI) fell 5.3% YoY, marginally Absolute Rating BUY underperforming the industry (-4.2% YoY). Net earned premium (NEP) Rating Relative to Sector Outperformer grew 3.5% YoY. Investment leverage remained unchanged at 4.2x net Risk Rating Relative to Sector Low worth. The company continues to grow in the preferred areas of SME fire Sector Relative to Market Overweight and agency-driven health indemnity, accompanying added momentum in commercial lines. We estimate NEP would increase by only 3% in FY21 as 15% shrinkage in motor OD business is offset by growth in retail health MARKET DATA (R:ICIL.BO, B:ICICIGI IN) CMP : INR 1,289 and fire. Underwriting performance should improve greatly as more Target Price : INR 1,600 profitable areas of fire and health account for a higher share in business mix along with better economics in motor OD. These drive upward 52-week range (INR) : 1,440 / 806 revisions of 16% in FY21E and 8% in FY22E earnings. We maintain ‘BUY’ Share in issue (mn) : 454.5 with a revised TP of INR1,600 (INR1,490 earlier, multiple unchanged). We M cap (INR bn/USD mn) : 586/ 7,817 single out ICICI Lombard as a long-term beneficiary of the current Avg. Daily Vol.BSE/NSE(‘000) : 656.0 disruption with higher pricing freedom accompanying market share gain. Key risks remain growth/scale-agnostic focus on earning too high an RoE SHARE HOLDING PATTERN (%) and under-investment in distribution and technology. -

Reappointment of Shri Amitabh Chaudhry As the Managing Director and CEO of the Bank

AXIS/CO/CS/32/2021-22 29th April 2021 Chief Manager, The Deputy General Manager, Listing & Compliance Department Listing Department National Stock Exchange of India Limited BSE Limited Exchange Plaza, 5th Floor 1st Floor, New Trading Ring, Plot No. C/1, “G” Block Rotunda Building Bandra-Kurla Complex P. J. Towers, Dalal Street Fort, Bandra (E), Mumbai – 400 051 Mumbai – 400 001 NSE Symbol: AXISBANK BSE Scrip Code : 532215 Dear Sir(s), SUB: RE-APPOINTMENT OF SHRI AMITABH CHAUDHRY AS THE MANAGING DIRECTOR & CEO OF THE BANK REF: REGULATION 30 OF THE SEBI (LISTING OBLIGATIONS AND DISCLOSURE REQUIREMENTS) REGULATIONS, 2015 (‘SEBI LISTING REGULATIONS’) This is to inform you that at the 214th meeting of the Board of Directors (the “Board”) of the Bank held on 27th April 2021 which continued on 28th April 2021, as recommended by the Nomination & Remuneration Committee of Directors, the Board has on 28th April 2021, considered and approved the proposal relating to re-appointment of Shri Amitabh Chaudhry as the Managing Director & CEO of the Bank, for a further period of 3 years, w.e.f. 1st January 2022 up to 31st December 2024 (both days inclusive) subject to the approval of the Reserve Bank of India(RBI) and the Shareholders of the Bank, in terms of the relevant provisions of the Companies Act, 2013, the relevant Rules made thereunder, the SEBI Listing Regulations, the Banking Regulation Act, 1949, the Guidelines issued by the RBI in this regard and the Articles of Association of the Bank. The brief profile of Shri Amitabh Chaudhry is attached herewith as Annexure A. -

HDFC Life Enters Into a Corporate Agency Arrangement with YES BANK to Offer Life Insurance Solutions to Its Customers

PRESS RELEASE HDFC Life enters into a Corporate Agency arrangement with YES BANK to offer life insurance solutions to its customers Mumbai, September 22, 2020: HDFC Life, one of India’s leading life insurers and YES BANK Limited entered into a Corporate Agency (CA) arrangement. This CA arrangement will enable customers of YES BANK to avail HDFC Life’s wide range of life insurance products which include solutions for protection, savings and investment, retirement and critical illness. Life insurance is an important financial tool for covering the risk of mortality, morbidity and longevity. Every individual with responsibilities needs adequate life insurance to ensure that their family is financially protected in their absence. Thanks to a robust multi-channel distribution set up and strong diversified network, HDFC Life is able to offer life insurance solutions at scale. Speaking on the arrangement Suresh Badami, Executive Director, HDFC Life said, "We are delighted to partner with YES BANK. There is a huge potential for insurance coverage across life & health protection, savings and annuity products in our country. With our bancassurance experience we aim to offer a comprehensive suite of product solutions and best in class servicing, leveraging our investments in technology. We look forward to working closely with the YES BANK team for the benefit of their customers". Rajan Pental, Global Head - Retail Banking, YES BANK said, “We are extremely excited to partner HDFC Life to offer our growing customer base access to HDFC Life’s comprehensive and innovative product suite – through a shared commitment to make a difference in their lives by addressing their unique insurance needs. -

ICICI Lombard General Insurance Company Limited Ref

Ref. No.: MUM/SEC/14-04/2022 April 17, 2021 To, To, General Manager Vice-President Listing Department Listing Department BSE Limited National Stock Exchange of India Ltd. Phiroze Jeejeebhoy Tower, Exchange Plaza, 5th Floor, Plot C/1, 14th Floor, Dalal Street, G Block, Bandra-Kurla Complex, Mumbai - 400 001 Bandra (East), Mumbai - 400 051 Equity (BSE: 540716/ NSE: ICICIGI); Debt (BSE: 954492/ NSE: ILGl26) Dear Sir/Madam, Sub: Outcome of the Board Meeting held on April 17, 2021 Pursuant to Regulation 30 and 33 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 ("Listing Regulations"), we wish to inform you that the Board of Directors of the Company, at their Meeting held today i.e. Saturday, April 17, 2021 in Mumbai, have inter-alia: Approved the Audited Financial Results of the Company for the quarter and financial year ended March 31, 2021. A copy of the Audited Financial Results for the quarter and financial year ended March 31, 2021 together with the Statutory Auditors’ Report in the prescribed format is enclosed herewith. A copy of the press release being issued in this connection is also attached. Please note that Chaturvedi & Co. and PKF Sridhar & Santhanam LLP, the Joint Statutory Auditors of the Company, have issued audit reports with unmodified opinion. Recommendation of final dividend of ₹ 4.0 per equity share i.e. at the rate of 40.0% of face value of ₹ 10 each for the financial year ended March 31, 2021, subject to approval of the Members at the ensuing Annual General Meeting (“AGM”) of the Company. -

Home Insurance Policy Wordings

Buy / Renew / Service / Claim related queries Log on to www.icicilombard.com or call 1800 2666 HOME INSURANCE POLICY WORDINGS Part II of the Schedule “Schedule” means the schedule, and any annexure to it, attached to and forming part of this Policy. 1. Definitions “Short Period Rates” means rates of premium for periods shorter than one year, as per details below- “Accident and Accidental” means a sudden, unforeseen, and unexpected physical event beyond the control of the Insured caused by external, visible and violent means. For a period not exceeding 15 days 10% of the annual rate “Actual Cash Value” means the cost of replacement less any depreciation, which would be For a period not exceeding 1 month 15% of the annual rate determined by considering the condition immediately before the loss or damage, the resale For a period not exceeding 2 months 30% of the annual rate value and the normal life expectancy. For a period not exceeding 3 months 40% of the annual rate “Bodily Injury” means any accidental physical bodily harm but does not include any For a period not exceeding 4 months 50% of the annual rate sickness or disease. For a period not exceeding 5 months 60% of the annual rate “Business or Business Purposes” means any full or part time, permanent or temporary, For a period not exceeding 6 months 70% of the annual rate activity undertaken in the dwelling with a view to profit or gain. For a period not exceeding 7 months 75% of the annual rate “Burglary” means an act involving the unauthorised entry to or exit from the Insured's Home For a period not exceeding 8 months 80 % of the annual rate or attempt threat by unexpected, forcible, visible and violent means, with the intent to For a period not exceeding 9 months 85% of the annual rate commit an act of Theft. -

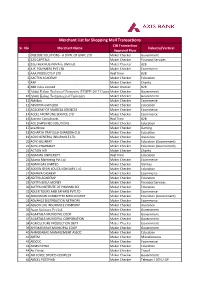

Merchant List for Shopping Mall Transactions CIB Transaction Sr

Merchant List for Shopping Mall Transactions CIB Transaction Sr. No Merchant Name Industry/Vertical Approval Flow 1 (N)CODE SOLUTIONS - A DIVN. OF GNFC LTD. Maker Checker Government 2 123 CAPITALS Maker Checker Financial Services 3 2GETHER HUB PRIVATE LIMITED Maker Checker B2B 4 A.R. POLYMERS PVT LTD Maker Checker Ecommerce 5 AAA PRODUCTS P LTD Real Time B2B 6 AACTEN ACADEMY Maker Checker Education 7 AAP Maker Checker Charity 8 ABB India Limited Maker checker B2B 9 Abdul Kalam Technical University (UPSEE-2017 Counselling)Maker Checker Government 10 Abdul Kalam Technological University Maker Checker Government 11 Abhibus Maker Checker Ecommerce 12 ABVIIITM-GWALIOR Maker Checker Education 13 ACADEMY OF MAGICAL SCIENCES Maker Checker Ecommerce 14 ACCEL FRONTLINE SERVICE LTD Maker Checker Ecommerce 15 Accrete Consultants Real Time B2B 16 ACE SIMPLIFIED SOLUTIONS Maker Checker Education 17 ace2three Maker Checker Gaming 18 ACHARYA PRAFULLA CHANDRA CLG Maker Checker Education 19 ACKO GENERAL INSURANCE LTD Maker Checker Insurance 20 ACPC-GUJARAT Maker Checker Education (Government) 21 ACPC-PHARMACY Maker Checker Education (Government) 22 ACTION AID Maker Checker Charity 23 ADAMAS UNIVERSITY Real Time Education 24 Adams Marketing Pvt Ltd Maker Checker Ecommerce 25 ADANI GAS LIMITED Maker Checker Utilities 26 ADDON GYAN EDUCATION SERV LTD Maker Checker Education 27 ADHAVA CASHEW Maker Checker Ecommerce 28 ADITYA ACADEMY Maker Checker Education 29 ADITYA BIRLA MONEY Maker Checker Financial Services 30 ADITYA INSTITUTE OF PHARMA SCI Maker Checker -

Star Health and Bank of Baroda Enter Into a Corporate Agency Agreement

Star Health and Bank of Baroda enter into a corporate agency agreement 1 Media Coverage Details Sr. No Publication Headline Date Wire 1. PTI BoB, Star Health enter into Corporate Agency May 9, 2016 agreement Print - English 2. Deccan Herald BoB inks MoU with Max Bupa and Star Health May 8, 2016 3. Free Press Journal BoB signs MoU with max Bupa and Star Heath May 9, 2016 4. Business Standard Bank of Baroda enters into an MoU May 10, 2016 5. Financial Chronicle BoB, Star Heath ties-up May 10, 2016 6. The Financial Express Star Health ties up with BoB to market insurance May 12, 2016 products 7. Lucknow News Bank of Baroda branches to offer Star Health and May 12, 2016 Allied Health Insurance products 8. The Financial Express BoB to offer Star health Insurance products May 13, 2016 9. The Economic Times BoB joins MOU with Max Bupa Health Insurance May 16, 2016 10. The Financial Express Star Health Insurance tie up with Bank of Baroda May 17, 2016 11. The Indian Express Star Health Insurance tie up with Bank of Baroda May 17, 2016 12. Daily News and Analysis BoB ties up with Star Health May 17, 2016 13. Daily News and Analysis BoB ties up with Star Health May 17, 2016 14. Mid -Day Star Health and BoB enter into an agreement May 17, 2016 Print - Regionals 15. Punjab Kesari Bank of Baroda branches to offer Star Health and May 11, 2016 Allied Health Insurance products 16. Loksatta Bank of Baroda ties up with insurance companies May 11, 2016 17.