12. Final Official Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Marginable OTC Stocks

List of Marginable OTC Stocks @ENTERTAINMENT, INC. ABACAN RESOURCE CORPORATION ACE CASH EXPRESS, INC. $.01 par common No par common $.01 par common 1ST BANCORP (Indiana) ABACUS DIRECT CORPORATION ACE*COMM CORPORATION $1.00 par common $.001 par common $.01 par common 1ST BERGEN BANCORP ABAXIS, INC. ACETO CORPORATION No par common No par common $.01 par common 1ST SOURCE CORPORATION ABC BANCORP (Georgia) ACMAT CORPORATION $1.00 par common $1.00 par common Class A, no par common Fixed rate cumulative trust preferred securities of 1st Source Capital ABC DISPENSING TECHNOLOGIES, INC. ACORN PRODUCTS, INC. Floating rate cumulative trust preferred $.01 par common $.001 par common securities of 1st Source ABC RAIL PRODUCTS CORPORATION ACRES GAMING INCORPORATED 3-D GEOPHYSICAL, INC. $.01 par common $.01 par common $.01 par common ABER RESOURCES LTD. ACRODYNE COMMUNICATIONS, INC. 3-D SYSTEMS CORPORATION No par common $.01 par common $.001 par common ABIGAIL ADAMS NATIONAL BANCORP, INC. †ACSYS, INC. 3COM CORPORATION $.01 par common No par common No par common ABINGTON BANCORP, INC. (Massachusetts) ACT MANUFACTURING, INC. 3D LABS INC. LIMITED $.10 par common $.01 par common $.01 par common ABIOMED, INC. ACT NETWORKS, INC. 3DFX INTERACTIVE, INC. $.01 par common $.01 par common No par common ABLE TELCOM HOLDING CORPORATION ACT TELECONFERENCING, INC. 3DO COMPANY, THE $.001 par common No par common $.01 par common ABR INFORMATION SERVICES INC. ACTEL CORPORATION 3DX TECHNOLOGIES, INC. $.01 par common $.001 par common $.01 par common ABRAMS INDUSTRIES, INC. ACTION PERFORMANCE COMPANIES, INC. 4 KIDS ENTERTAINMENT, INC. $1.00 par common $.01 par common $.01 par common 4FRONT TECHNOLOGIES, INC. -

Official Statement

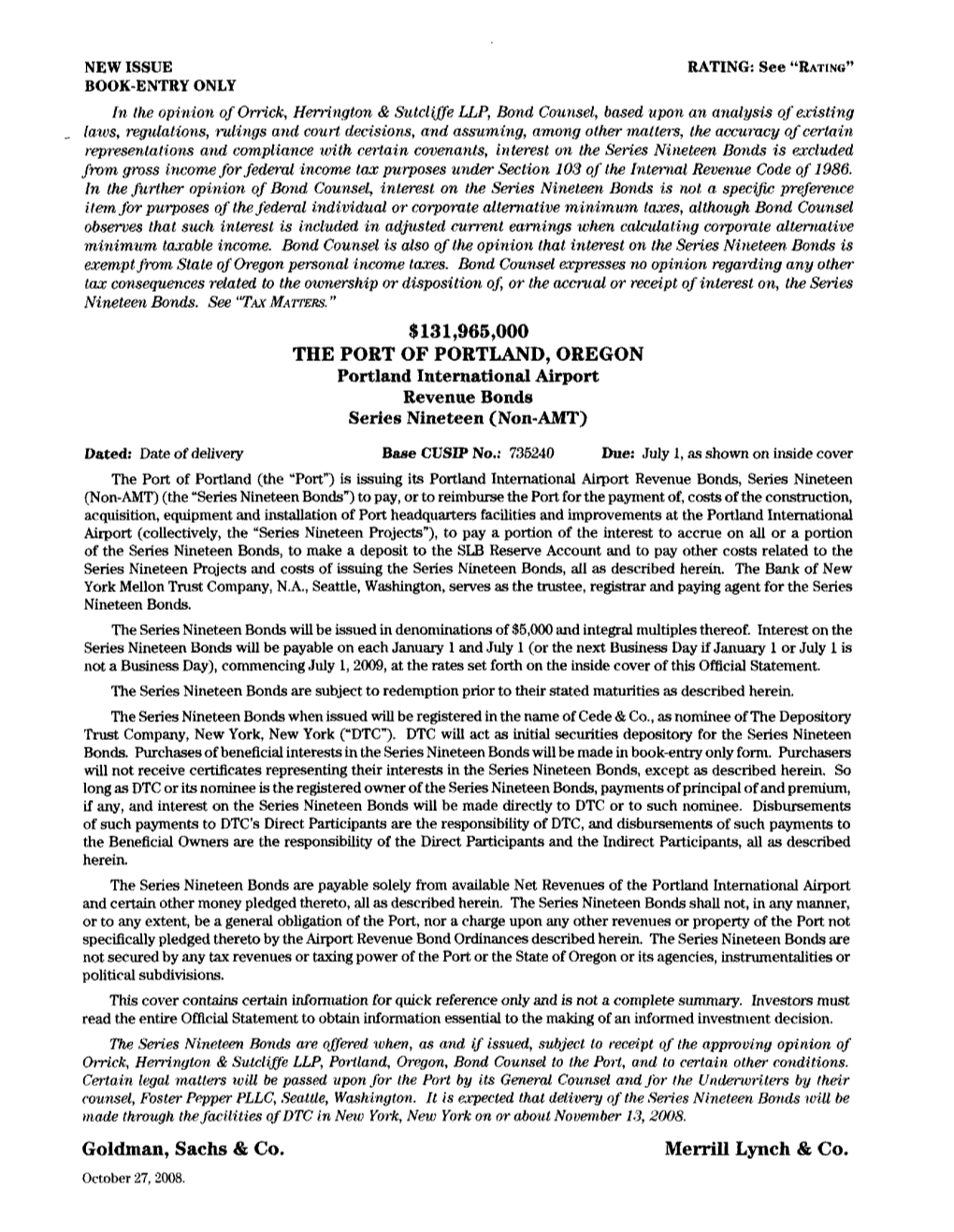

NEW ISSUE—BOOK ENTRY ONLY RATING: See “Rating” In the opinion of Orrick, Herrington & Sutcliffe LLP, Bond Counsel, based upon an analysis of existing laws, regulations, rulings and court decisions and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Series Twenty-One C Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, except that no opinion is expressed as to the status of interest on any Series Twenty-One C Bond for any period that such Series Twenty-One C Bond is held by a “substantial user” of the facilities refinanced by the Series Twenty- One C Bonds or by a “related person” within the meaning of Section 147(a) of the Internal Revenue Code of 1986. Bond Counsel observes, however, that interest on the Series Twenty-One C Bonds is a specific preference item for purposes of the federal individual and corporate alternative minimum taxes. In the further opinion of Bond Counsel, interest on the Series Twenty-One C Bonds is exempt from personal income taxation by the State of Oregon. Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of, or the accrual or receipt of interest on, the Series Twenty-One C Bonds. See “Tax MaTTers.” $27,685,000 THE PORT OF PORTLAND, OREGON Portland International Airport Refunding Revenue Bonds Series Twenty-One C (AMT) Dated: Date of initial delivery Base CUSIP No.: 735240 Due: July 1, as shown on inside cover The Port of Portland (the “Port”) is issuing its Portland International Airport Refunding Revenue Bonds, Series Twenty-One C (AMT) (the “Series Twenty-One C Bonds”) to refund the Port’s outstanding Portland International Airport Refunding Revenue Bonds, Series Fifteen D, to make a deposit to the SLB Reserve Account and to pay costs of issuing the Series Twenty-One C Bonds, all as described herein. -

Tigard Chamber Business Directory

TIGARD AREA 2011-2012 Tigard Chamber CHAMBER OF Business Directory COMMERCE Where Business Soars! • Building a Strong Local Economy • Providing Business Networking • Promoting the Community • Advocating for Business with Government Community and Visitor Guide Included! Wills, Trusts, Probates Guardianships & Conservatorships Medicaid Planning 503-639-8800 15405 SW 116th Ave • Ste. 112, King City Affordable legal solutions for Oregon Families Call for your complimentary consultation today TIG2012 Health care for that crazy thing called life When life gets busy, scheduling medical appointments can feel like just one more thing you have to do. At Providence Bridgeport Health Center, we make it easy to get the care you need. With even more services now in place, you’ll fi nd that checkups, immediate care, medical imaging, lab testing, prescriptions, day surgery, rehabilitation and more are all available close to home. Providence combines the care you deserve with the convenience your schedule demands. No matter what life brings, we’ll be right here with you. To schedule an appointment, call 503-216-0696. www.providence.org/healthcenters Providence Bridgeport Health Center 18040 SW Lower Boones Ferry Road, Tigard, OR 97224 Contents 4 Your local chamber of commerce: 300 members and growing 6 Choosing the right tool to build your business 7 It pays to be a chamber member 8 Support your neighbors — buy local Life in Tigard DEBI MOLLAHAN 9 2011-2012 Tigard Community & Visitors Guide 10 Discover the hidden gems of Tigard 11 Local cuisine 12 Tigard -

Southwest Airlines Corporation: a Domestic Industry Analysis & Recommendation for Expansion

University of Tennessee, Knoxville TRACE: Tennessee Research and Creative Exchange Supervised Undergraduate Student Research Chancellor’s Honors Program Projects and Creative Work 5-2006 Southwest Airlines Corporation: A Domestic Industry Analysis & Recommendation for Expansion Joel LaSharon Thomas University of Tennessee-Knoxville Follow this and additional works at: https://trace.tennessee.edu/utk_chanhonoproj Part of the Marketing Commons Recommended Citation Thomas, Joel LaSharon, "Southwest Airlines Corporation: A Domestic Industry Analysis & Recommendation for Expansion" (2006). Chancellor’s Honors Program Projects. https://trace.tennessee.edu/utk_chanhonoproj/1019 This is brought to you for free and open access by the Supervised Undergraduate Student Research and Creative Work at TRACE: Tennessee Research and Creative Exchange. It has been accepted for inclusion in Chancellor’s Honors Program Projects by an authorized administrator of TRACE: Tennessee Research and Creative Exchange. For more information, please contact [email protected]. Southwest Airlines Corporation: A Domestic Industry Analysis & Recommendation for Expansion Joel L. Thomas Chancellor's Honors Program University of Tennessee Senior Project May 2,2006 Joel L. Thomas Senior Honors Project Southwest Airlines May 2, 2006 2 Executive Summary After almost thirty years of service, Southwest Airlines has emerged as one of the world's premier airlines. The Southwest approach to business and the industry at large have enabled the company to continue to grow at profit in times of true economic downturn. Presently, the market for air carriers is saturated and highly fragmented. Overcapacity has led the major United States airlines to compete with Southwest's low fare pricing strategy. However, due to the company's brand image of efficient and effective low fare service, Southwest has been able to ward off its competitors (e.g. -

List of Section 13F Securities

List of Section 13F Securities 1st Quarter FY 2004 Copyright (c) 2004 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of March 15, 2004, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 31, 2004. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by Section 13(f)(1) and Rule 13f-1 thereunder. -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

Chapter 6 Airline Business Strategy

CHAPTER 6 AIRLINE BUSINESS STRATEGY Gui Lohmann and Bojana Spasojevic Airlines are notorious for providing lower returns on investment when compared with other corporations. As a result, airline executives implement business strategies aiming to obtain higher than normal financial returns. With the liberalisation process that airlines have enjoyed around the world, some carriers have been quite creative in fostering new approaches in terms of their business models, product differentiation and cost reduction. In addition, because of the international multiple-business related nature of airline operations (which includes aircraft manufacturers and maintenance, distribution channels, and airport logistics), these characteristics make airline strategic management a very complex exercise. A number of approaches have been used to explain strategic issues related to airlines. One of them is Shaw’s (2011) application of Porter's classic Five Forces model to the airline industry, a framework for analysing competitive forces, for instance, rivalry, substitution, new entry, power of customers, and power of suppliers. Scholars have also focused their attention on analysing airline strategic decisions relating to a number of managerial issues, with a particular emphasis on mergers and alliances (Gudmundsson and Lechner, 2011; Iatrou and Oretti, 2016). This chapter is structured into four main sections. The first one provides some generic strategies. The second section focuses on airline differentiation strategies and niche products, mainly charter and leisure carriers. The third section tackles growth strategies, examining the four distinct strategies proposed by Ansoff’s Matrix: market penetration, product development, market development and diversification. The fourth section considers different strategic growth methods, including organic growth, mergers and acquisitions, industry cooperation, franchising. -

Climate Change Challenges Portland Natural Gas Utility

QB quandary Suspect Ducks struggling at most important position Portland— SEE LIFE, B1 Tribune TUESDAY, OCTOBER 13, 2015 • TWICE CHOSEN THE NATION’S BEST NONDAILY PAPER • PORTLANDTRIBUNE.COM • PUBLISHED TUESDAY AND THURSDAY City declares housing emergency, starts to act Now what? economy for drawing new peo- Questions remain on The unanimous vote fol- ple to town and driving up next steps, paying for lowed hours of emotional testi- rents, reducing the amount of mony from people living on the affordable housing units not solutions to crisis streets and tenants who are owned by public agencies or being forced to move by no- nonprofi t organizations. How- Relocating the By JIM REDDEN fault evictions and rent in- ever, some landlords said they Right 2 Dream The Tribune creases. Advocates for low-in- were only responding to the Too homeless come people and landlords also law of supply and demand. camp in Old The City Council declared testifi ed. But the ordinance submitted Town is in the a “housing emergency” last Many of the witnesses works. week. blamed Portland’s recovering See HOUSING / Page 3 TRIBUNE FILE PHOTO CLIMATE CHANGE CHALLENGES PORTLAND NATURAL GAS UTILITY PAMPLIN MEDIA GROUP FILE PHOTO Clackamas County Chair John Ludlow says his commission is not willing to simply sign off on the Metro Council’s urban reserve decision. Showdown coming Fred Meyer fl eet manager Nick between Metro, Brocato pumps fuel into one of the retailer’s Clackamas County new LNG-fueled freight trucks in mand,” says a letter signed by Clackamas. LNG Commissioners Chairman John Ludlow. -

Sacramento International Airport Airline Passenger Statistics July 2010

Sacramento International Airport Airline Passenger Statistics July 2010 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE THIS YEAR LAST YEAR % + / ( - ) 2010/11 2009/10 % + / ( - ) 2010 2009 % + / ( - ) Enplaned Domestic Alaska Airlines 25,519 19,792 28.9% 25,519 19,792 28.9% 123,342 106,591 15.7% American Airlines 16,593 16,140 2.8% 16,593 16,140 2.8% 107,297 86,244 24.4% Continental Airlines 14,658 14,288 2.6% 14,658 14,288 2.6% 94,379 98,856 (4.5%) Delta Airlines 36,317 19,603 85.3% 36,317 19,603 85.3% 184,669 117,759 56.8% Frontier Airlines 15,931 12,687 25.6% 15,931 12,687 25.6% 84,949 73,540 15.5% Hawaiian Airlines 7,536 7,616 (1.1%) 7,536 7,616 (1.1%) 49,307 50,683 (2.7%) Horizon Air 13,753 12,058 14.1% 13,753 12,058 14.1% 81,296 71,717 13.4% Jet Blue 10,453 10,669 (2.0%) 10,453 10,669 (2.0%) 64,002 53,048 20.6% Mesa/US Airways Express/YV 753 - 753 - 2,821 - Northwest - 13,184 (100.0%) - 13,184 (100.0%) - 66,533 (100.0%) Skywest/Delta Connection 5,818 5,689 2.3% 5,818 5,689 2.3% 31,982 30,524 4.8% Skywest/United Express 15,635 13,611 14.9% 15,635 13,611 14.9% 107,786 92,425 16.6% Southwest 205,786 214,471 (4.0%) 205,786 214,471 (4.0%) 1,380,693 1,410,965 (2.1%) United Airlines 29,249 32,626 (10.4%) 29,249 32,626 (10.4%) 173,518 199,056 (12.8%) US Airways 25,755 29,462 (12.6%) 25,755 29,462 (12.6%) 129,309 166,358 (22.3%) CHARTER - - - - - - 423,756 421,896 0.4% 423,756 421,896 0.4% 2,615,350 2,624,299 (0.3%) International Mexicana 5,303 6,524 (18.7%) 5,303 6,524 (18.7%) 33,480 32,327 3.6% 5,303 6,524 (18.7%) 5,303 6,524 -

Historia De La Aviación Comercial Desde 1909 Hasta Nuestros Días

FACULTAT DE FILOSOFIA I LETRES, DEPARTAMENT DE CIÈNCIES HISTÒRIQUES I TEORIA DE LES ARTS HISTORIA DE LA AVIACIÓN COMERCIAL DESDE 1909 HASTA NUESTROS DÍAS TESIS DOCTORAL PRESENTADA POR EL DR. MARTÍN BINTANED ARA DIRIGIDA POR EL DR. SEBASTIÁ SERRA BUSQUETS CATEDRÀTIC D'HISTÒRIA CONTEMPORÀNIA PARA OPTAR AL TÍTULO DE DOCTOR EN HISTORIA CURSO ACADÉMICO 2013/2014 Martín Bintaned Ara 2 Historia de la aviación comercial Resumen Esta tesis doctoral investiga acerca de la aportación de la aviación comercial a la historia contemporánea, en particular por su impacto en las relaciones exteriores de los países, su papel facilitador en la actividad económica internacional y por su contribución al desarrollo del turismo de masas. La base de trabajo ha sido el análisis de la prensa especializada, a partir de la cual se han identificado los casos innovadores. Gracias al análisis de su origen (tecnológico, geo- político, aero-político, corporativo, de producto y en la infraestructura) y a su contextualización, hemos podido trazar la historia de la aviación comercial desde su origen en 1919 hasta nuestros días. Palabras clave: Historia contemporánea, Aviación comercial, Política aérea, Relaciones internacionales, Turismo, Innovación, Aerolíneas, Aeropuertos Abstract This doctoral thesis analyses the contribution of commercial aviation to the contemporary history, particularly in the field of external relations, international economy and mass tourism. We have identified all innovations with a structural impact on the industry through specialised press, considering the changes on technology, geopolitics, aeropolitics, business models, product and services, and infrastructure. This methodology has allowed us to write the history of the commercial aviation since its origin in 1919. -

Jetblue Airways Contract of Carriage

JetBlue Airways Contract of Carriage (Revised, August 12, 2020) Domestic transportation and international transportation by JetBlue Airways Corporation (“Carrier” or “JetBlue”) is subject to the terms and conditions contained in this Contract of Carriage and, where applicable, also subject to treaties, government regulations, and tariffs on file with the U.S. Department of Transportation, as well as any terms, conditions, and/or restrictions applicable to your booking channel. If your itinerary involves travel on a flight operated by a JetBlue Codeshare Partner (as defined below), please see Section 35. If your itinerary involves travel on a flight operated by a JetBlue interline partner, please see Section 36. By making a reservation or accepting transportation on Carrier, each Passenger (as defined below) agrees to be bound by all of the following terms and conditions. 1. Definitions Assistive Device refers to any piece of equipment that assists an Individual with a Disability to cope with the effects of his or her disability, and may include medical devices and medications. Battery-Powered Mobility Aid refers to an assistive device used by individuals with mobility impairments such as a wheelchair, scooter or a Segway when it is used as a mobility device by a person with a mobility-related disability. Blue Fare, Blue Basic Fare, Blue Plus Fare, Blue Extra Fare, and Blue Flex Fare refer to fare options offered for purchase. Details regarding fare options are available at www.jetblue.com/fares. Carriage refers to the transportation of passengers and/or baggage by air, together with any related services of Carrier in connection with such transportation. -

2019 Expo Resource Guide

PORTLANDWORKFORCEALLIANCE #PWAExpo PWORKFORCEA 2019 RESOURCE GUIDE Tuesday, March 19, 2019 9:00 am – 1:30 pm • Oregon Convention Center PORTLANDWORKFORCEALLIANCE.ORG/EXPO Daimler Trucks North America Work locally. Make an impact globally. We’ve been shaping the future of transportation since the invention of the commercial vehicle. Our spirit of innovation fuels our passion to continually challenge perceptions and transform today’s mobility concepts. From our Portland-based headquarters, we take aim at making mobility safe, simple, and globally sustainable. Daimler-trucksnorthamerica.com Copyright © Daimler Trucks North America LLC. All rights reserved. Daimler Trucks North America LLC is a Daimler company. 2019 NW Youth Careers Expo • 1 NW YOUTH CAREERS EXPO The annual NW YOUTH CAREERS EXPO is the Northwest’s premier career-education event. The EXPO shows students the region’s amazing diversity of career opportunities, and offers information on the skills and education needed for those jobs. The EXPO connects employers to their future workforce and helps students make informed, inspired decisions about their education after high school – whether they choose a four-year university, community college or apprenticeship training center. THANK YOU to our sponsors, exhibitors and high schools for making the annual NW YOUTH CAREERS EXPO a success! CONNECT WITH PWA PORTLANDWORKFORCEALLIANCE PWORKFORCEA Share your photos! #PWAExpo #MyPWA TABLE OF CONTENTS MAP OF EXHIBIT HALL .............................................. 2 MOCK INTERVIEWS & CAREER TALKS ........................ 3 BIG DREAMS. GOOD JOBS. ALL STUDENTS. EXHIBITORS by Career Pathway ................................. 5 EXHIBITORS Alphabetically ...................................... 10 The Portland Workforce Alliance PWA EVENTS CALENDAR ......................................... 16 is an independent nonprofit that sees young people as the key to ALL SPONSORS ..........................................