World Oil Outlook 2040

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Petroleum Extension-The University of Texas at Austin ROTARY DRILLING SERIES

Petroleum Extension-The University of Texas at Austin ROTARY DRILLING SERIES Unit I: The Rig and Its Maintenance Lesson 1: The Rotary Rig and Its Components Lesson 2: The Bit Lesson 3: Drill String and Drill Collars Lesson 4: Rotary, Kelly, Swivel, Tongs, and Top Drive Lesson 5: The Blocks and Drilling Line Lesson 6: The Drawworks and the Compound Lesson 7: Drilling Fluids, Mud Pumps, and Conditioning Equipment Lesson 8: Diesel Engines and Electric Power Lesson 9: The Auxiliaries Lesson 10: Safety on the Rig Unit II: Normal Drilling Operations Lesson 1: Making Hole Lesson 2: Drilling Fluids Lesson 3: Drilling a Straight Hole Lesson 4: Casing and Cementing Lesson 5: Testing and Completing Unit III: Nonroutine Operations Lesson 1: Controlled Directional Drilling Lesson 2: Open-Hole Fishing Lesson 3: Blowout Prevention Unit IV: Man Management and Rig Management Unit V: Offshore Technology Lesson 1: Wind, Waves, and Weather Lesson 2: Spread Mooring Systems Lesson 3: Buoyancy, Stability, and Trim Lesson 4: Jacking Systems and Rig Moving Procedures Lesson 5: Diving and Equipment Lesson 6: Vessel Inspection and Maintenance Lesson 7: Helicopter Safety Lesson 8: Orientation for Offshore Crane Operations Lesson 9: Life Offshore Lesson 10: Marine Riser Systems and Subsea Blowout Preventers Petroleum Extension-The University of Texas at Austin Library of Congress Cataloging-in-Publication Data Vieira, João Luiz, 1958– Controlled directional drilling / by João Luiz Vieira. — 4th ed. p. cm. — (Rotary drilling series ; unit 3, lesson 1) Rev. ed. of: Controlled directional drilling. 1984 Includes index. ISBN-10 0-88698-254-5 (alk. paper) ISBN-13 978-0-88698-254-6 (alk. -

Unconventional Gas and Oil in North America Page 1 of 24

Unconventional gas and oil in North America This publication aims to provide insight into the impacts of the North American 'shale revolution' on US energy markets and global energy flows. The main economic, environmental and climate impacts are highlighted. Although the North American experience can serve as a model for shale gas and tight oil development elsewhere, the document does not explicitly address the potential of other regions. Manuscript completed in June 2014. Disclaimer and copyright This publication does not necessarily represent the views of the author or the European Parliament. Reproduction and translation of this document for non-commercial purposes are authorised, provided the source is acknowledged and the publisher is given prior notice and sent a copy. © European Union, 2014. Photo credits: © Trueffelpix / Fotolia (cover page), © bilderzwerg / Fotolia (figure 2) [email protected] http://www.eprs.ep.parl.union.eu (intranet) http://www.europarl.europa.eu/thinktank (internet) http://epthinktank.eu (blog) Unconventional gas and oil in North America Page 1 of 24 EXECUTIVE SUMMARY The 'shale revolution' Over the past decade, the United States and Canada have experienced spectacular growth in the production of unconventional fossil fuels, notably shale gas and tight oil, thanks to technological innovations such as horizontal drilling and hydraulic fracturing (fracking). Economic impacts This new supply of energy has led to falling gas prices and a reduction of energy imports. Low gas prices have benefitted households and industry, especially steel production, fertilisers, plastics and basic petrochemicals. The production of tight oil is costly, so that a high oil price is required to make it economically viable. -

Monthly Report on Petroleum Developments in the World Markets February 2020

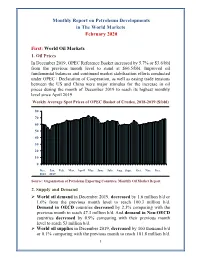

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Carbon Dioxide Enhanced Oil Recovery (CO2 EOR)

Carbon Dioxide Enhanced Oil Recovery (CO2 EOR): Factors Involved in Adding Carbon Capture, Utilization and Storage (CCUS) to Enhanced Oil Recovery L. Stephen Melzer CO2 Consultant and Annual CO2 Flooding Conference Director Midland, TX February 2012 Carbon Dioxide Enhanced Oil Recovery (CO2 EOR): Factors Involved in Adding Carbon Capture, Utilization and Storage (CCUS) to Enhanced Oil Recovery Table of Contents I. Introduction II. The Background and Fundamentals of Oil Production and CO2 EOR a. Primary Production Phase b. Secondary Production Phase c. Tertiary Phase III. Current and Projected Flooding CO2 EOR Activity In the U.S. & Permian Basin a. Long-Term Nature of The Industry b. U.S. Project Planning Underway IV. The Effectiveness of CO2 Storage in an EOR Project V. Monitoring CO2 Within The Reservoir: Existing Practices VI. CCUS: Incremental Requirements VII. CO2 Recycle, Reservoir Retention, and CO2 ‘Losses’ During EOR: The Metrics and Experience Base a. Purchases and Recycle Volumes b. CO2 Retention c. CO2 Losses During EOR: Causes and the Experience Base VIII. How to Move Forward? The Urgency and Areas for Caution a. Storage Frameworks b. Recommended Action References FIGURES AND TABLES Figure 1: Number of CO2 EOR Projects (Worldwide, U.S. and Permian Basin) Figure 2: U.S. CO2 EOR Projects, Supply Sources and Pipelines Figure 3: CO2 EOR Production (U.S. and Permian Basin, 1992-2010) Table 1: Basin Scale Criteria for Storage Figure 4: Crossectional Representation of the Various Types of Geologic Basins Table 2: Reservoir Surveillance Tools Commonly Used in CO2 EOR Figure 5: CO2 Flood Surveillance vs. CCUS Monitoring, Measurement and Verification Figure 6: Example CO2 Purchase vs. -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

UCS TIGHT OIL.Indd

The Truth about Tight Oil Don Anair Amine Mahmassani Methane from Unconventional Oil Extraction Poses Significant Climate Risks July 2013 Since 2010, “tight oil”—oil extracted from hard- to-access deposits using horizontal drilling and hydraulic fracturing (fracking)—has dramatically changed the US oil industry, reversing decades of declining domestic oil production and reducing US oil imports (EIA 2015a). In 2015, tight oil comprised more than half of US oil produc- 10,000 feet to reach sedimentary rock and then sideways or tion, bringing total production close to 10 million barrels per horizontally for a mile or more. Next, a mixture of water, day—a peak not seen since the 1970s (see Figure 1). But this sand, and chemicals is pumped at high pressure into the wells sudden expansion has also led to an increase of global warm- to create fractures in the rocks, which frees the oil and gas ing emissions due, in large part, to methane—an extremely potent heat-trapping gas that is found in larger concentra- tions in tight oil regions. Although most of the emissions associated with the con- sumption of oil are a result of burning the finished fuel (for example, in a car or truck), the emissions from extracting, transporting, and refining oil add, on average, 35 percent to a fuel’s life cycle emissions. These “upstream” emissions can- not be overlooked when seeking to mitigate emissions from oil use overall. Recent scientific evidence highlights major gaps in our knowledge of these large and rising sources of global warming pollution (Caulton et al. -

CMTC-485111-MS Feasibility of CO2-EOR in Shale-Oil

CMTC-485111-MS Feasibility of CO2-EOR in Shale-Oil Reservoirs: Numerical Simulation Study and Pilot Tests Dheiaa Alfarge, Iraqi Ministry of Oil, Missouri University of Science and Technology; Mingzhen Wei and Baojun Bai, Missouri University of Science and Technology Copyright 2017, Carbon Management Technology Conference This paper was prepared for presentation at the Carbon Management Technology Conference held in Houston, Texas, USA, 17-20 July 2017. This paper was selected for presentation by a CMTC program committee following review of information contained in an abstract submitted by the author(s). Contents of the paper have not been reviewed and are subject to correction by the author(s). The material does not necessarily reflect any position of the Carbon Management Technology Conference, its officers, or members. Electronic reproduction, distribution, or storage of any part of this paper without the written consent of the Carbon Management Technology Conference is prohibited. Permission to reproduce in print is restricted to an abstract of not more than 300 words; illustrations may not be copied. The abstract must contain conspicuous acknowledgment of CMTC copyright. Abstract Shale oil reservoirs such as Bakken, Niobrara, and Eagle Ford have become the main target for oil and gas investors as conventional formations started to be depleted and diminished in number. These unconventional plays have a huge oil potential; however, the predicted primary oil recovery is still low as an average of 7.5 %. Injecting carbon dioxide (CO2) to enhance oil recovery in these poor-quality formations is still a debatable issue among investigators. In this study, three steps of research have been integrated to investigate the parameters which control the success of CO2 huff-n-puff process in the field scale of shale oil reservoirs. -

Welcome to the 11Th Edition of Energy Perspectives! This Is An

Welcome to the 11th edition of Energy Perspectives! This is an independent report that informs Equinor’s strategy and offers a fact-based contribution to the energy transition debate. This year’s edition is an update of the edition from November last year, and with a lot happening on the global arena the last 6 months, there is a lot to consider when looking 30 years ahead. As always, this report and its data and conclusions would be impossible without the excellent work of many of my colleagues, to whom I extend my appreciation and gratitude. You are the best! 1 Covid19 is not over. In a global perspective, we are still dealing with its impact and the enormous effects it has on people, societies, economies, and markets. We are not through it yet. And we might have to live with recurring infection spikes, especially in parts of the world that do not get sufficient access to vaccines. Recurring lockdowns entailed that energy demand, and in particular oil demand due to its use as a transport fuel, was hit hard. Recovery is in the making, and faster than many feared, but oil demand, as an example, is still not back to pre-Covid19-levels. The map shows how the pandemic has affected economies across the globe, with almost all countries pink or red, that is, with negative economic development. Industrialised countries are on their way out of recession while disabling the virus, but the uncertainty is still high in many emerging economies. 2 We are seeing signs of recovery. Thanks to the development and rollout of vaccines and massive public spending to stimulate demand, there are signs that the situation is being brought under control so that we can live with the virus more like we do with normal flus. -

Bitumen Partial Upgrading 2018 Whitepaper

Bitumen Partial Upgrading 2018 Whitepaper AM0401A Alberta Innovates Prepared By Bill Keesom, Jacobs Consultancy – Technical Lead John Gieseman, Jacobs Consultancy – Project Manager March 2018 Document Title Bitumen Partial Upgrading 2018 Whitepaper - AM0401A Study No: JC158400 Document Title: Bitumen Partial Upgrading 2018 Whitepaper - AM0401A Client Name: Alberta Innovates Date: March 2018 Study Manager: John Gieseman Approved by: Robert S. Brasier Jacobs Consultancy Inc. 525 W. Monroe, Suite 1600 Chicago, IL 60661 United States www.jacobsconsultancy.com [email protected] This study or report was prepared by Jacobs Consultancy Canada Inc., (“Jacobs”) for the sole benefit of ALBERTA INNOVATES. There are no third party beneficiaries intended, and none of Jacobs and its affiliates, Alberta Innovates or any of their respective officers, directors, partners, employees, agents shall have any liability whatsoever to third parties for any defect, deficiency, error, or omission in any statement contained in or any way related to the study or report or any related documents. Neither Jacobs nor any person acting on Jacobs’ behalf make any warranty, express or implies, or assumes any liability with respect to use or reliance on any information, technology, engineering or methods disclosed or discussed in the study or report. Any forecasts, estimates, projections, opinions or conclusions reached in the study or report are dependent upon numerous technical and economic conditions over which Jacobs has no control, and which are or may not occur. Reliance upon such opinions or conclusions by any person or entity is at the sole risk of the person relying thereon. The data, information and assumptions used to develop the report or study were obtained or derived from documents or information furnished by others. -

U.S.-Canada Cross- Border Petroleum Trade

U.S.-Canada Cross- Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits March 2021 Submitted to: American Petroleum Institute 200 Massachusetts Ave NW Suite 1100, Washington, DC 20001 Submitted by: Kevin DeCorla-Souza ICF Resources L.L.C. 9300 Lee Hwy Fairfax, VA 22031 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits This report was commissioned by the American Petroleum Institute (API) 2 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits Table of Contents I. Executive Summary ...................................................................................................... 4 II. Introduction ................................................................................................................... 6 III. Overview of U.S.-Canada Petroleum Trade ................................................................. 7 U.S.-Canada Petroleum Trade Volumes Have Surged ........................................................... 7 Petroleum Is a Major Component of Total U.S.-Canada Bilateral Trade ................................. 8 IV. North American Oil Production and Refining Markets Integration ...........................10 U.S.-Canada Oil Trade Reduces North American Dependence on Overseas Crude Oil Imports ..................................................................................................................................10 Cross-Border Pipelines Facilitate U.S.-Canada Oil Market Integration...................................14 -

Drilling and Completion Services Cost Index Q2 2015

Drilling and Completion Services Cost Index Q2 2015 Prepared by Spears and Associates, Inc. 8908 S. Yale, Suite 440 Tulsa, OK 74137 www.spearsresearch.com July 2015 Drilling and Completion Services Cost Index: Q2 2015 Introduction The Drilling and Completion Services (DCS) Cost Index tracks and forecasts price changes for products and services used in drilling and completing new wells in the US. The DCS Cost Index is a tool for oil and gas companies, oilfield equipment and service firms, and financial institutions interested in benchmarking and forecasting well costs. Methodology Spears and Associates undertakes a quarterly survey of independent well engineering and wellsite supervision firms to collect “spot market” drilling and completion services price information for a specific set of commonly drilled wells in the US. The information in the “well profile” survey is collected in the form of detailed drilling and completion services cost estimates based on current unit prices and usage rates in each location at the end of the quarter. The well profiles are equally-weighted in calculating an average price change per quarter for the drilling and completion services cost components. A “total well cost” price change is calculated for each well profile covered by the survey which reflects the weighted average price change for each component of the well’s cost. An overall “total well cost” price change is calculated, with each well profile equally weighted, to determine the “composite well cost” index shown in this report. All cost items are indexed to 100 as of Q1 2008. “Spot” prices tracked by the DCS Cost Index are those in effect at the end of each quarter and as such may differ from prices averaged across the entire quarter. -

Best Research Support and Anti-Plagiarism Services and Training

CleanScript Group – best research support and anti-plagiarism services and training List of oil field acronyms The oil and gas industry uses many jargons, acronyms and abbreviations. Obviously, this list is not anywhere near exhaustive or definitive, but this should be the most comprehensive list anywhere. Mostly coming from user contributions, it is contextual and is meant for indicative purposes only. It should not be relied upon for anything but general information. # 2D - Two dimensional (geophysics) 2P - Proved and Probable Reserves 3C - Three components seismic acquisition (x,y and z) 3D - Three dimensional (geophysics) 3DATW - 3 Dimension All The Way 3P - Proved, Probable and Possible Reserves 4D - Multiple Three dimensional's overlapping each other (geophysics) 7P - Prior Preparation and Precaution Prevents Piss Poor Performance, also Prior Proper Planning Prevents Piss Poor Performance A A&D - Acquisition & Divestment AADE - American Association of Drilling Engineers [1] AAPG - American Association of Petroleum Geologists[2] AAODC - American Association of Oilwell Drilling Contractors (obsolete; superseded by IADC) AAR - After Action Review (What went right/wrong, dif next time) AAV - Annulus Access Valve ABAN - Abandonment, (also as AB) ABCM - Activity Based Costing Model AbEx - Abandonment Expense ACHE - Air Cooled Heat Exchanger ACOU - Acoustic ACQ - Annual Contract Quantity (in reference to gas sales) ACQU - Acquisition Log ACV - Approved/Authorized Contract Value AD - Assistant Driller ADE - Asphaltene