The Business of Judging Directors' Business Judgments in Singapore

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SOL LLM Brochure 2021 Copy

SMU – Right in the Heart of Asia’s Hub, Singapore Masters of Laws In the dynamic, cosmopolitan hub that is Singapore, you will find a vibrant city-state that pulses with the diversity of both East and West. LL.M. in Judicial Studies Situated at the cross-roads of the world, Singapore is home to multinational companies and thousands of small and medium-sized LL.M. in Cross-border Business and Finance Law in Asia enterprises flourishing in a smart city renowned for its business excellence and connectivity. With its strong infrastructure, political Dual LL.M. in Commercial Law (Singapore & London) stability and respect for intellectual property rights, this City in a Garden offers you unique opportunities to develop as a global citizen. Thorough. Transnational. Transformative. Tapping into the energy of the city is a university with a difference — the Singapore Management University. Our six schools: the School of Accountancy, Lee Kong Chian School of Business, School of Computing and Information Systems, School of Economics, Yong Pung How School of Law, and School of Social Sciences form the country’s only city campus, perfectly sited to foster strategic links with businesses and the community. Modelled after the University of Pennsylvania’s Wharton School, SMU generates leading-edge research with global impact and produces broad-based, creative and entrepreneurial leaders for a knowledge-based economy. Discover a multi-faceted lifestyle right here at SMU, in the heart of Singapore. The SMU Masters Advantage GLOBAL RECOGNITION SMU is globally recognised as one of the best specialised universities in Asia and the world. -

Lee Kuan Yew Continue to flow As Life Returns to Normal at a Market at Toa Payoh Lorong 8 on Wednesday, Three Days After the State Funeral Service

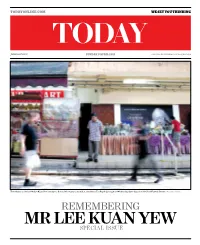

TODAYONLINE.COM WE SET YOU THINKING SUNDAY, 5 APRIL 2015 SPECIAL EDITION MCI (P) 088/09/2014 The tributes to the late Mr Lee Kuan Yew continue to flow as life returns to normal at a market at Toa Payoh Lorong 8 on Wednesday, three days after the State Funeral Service. PHOTO: WEE TECK HIAN REMEMBERING MR LEE KUAN YEW SPECIAL ISSUE 2 REMEMBERING LEE KUAN YEW Tribute cards for the late Mr Lee Kuan Yew by the PCF Sparkletots Preschool (Bukit Gombak Branch) teachers and students displayed at the Chua Chu Kang tribute centre. PHOTO: KOH MUI FONG COMMENTARY Where does Singapore go from here? died a few hours earlier, he said: “I am for some, more bearable. Servicemen the funeral of a loved one can tell you, CARL SKADIAN grieved beyond words at the passing of and other volunteers went about their the hardest part comes next, when the DEPUTY EDITOR Mr Lee Kuan Yew. I know that we all duties quietly, eiciently, even as oi- frenzy of activity that has kept the mind feel the same way.” cials worked to revise plans that had busy is over. I think the Prime Minister expected to be adjusted after their irst contact Alone, without the necessary and his past week, things have been, many Singaporeans to mourn the loss, with a grieving nation. fortifying distractions of a period of T how shall we say … diferent but even he must have been surprised Last Sunday, about 100,000 people mourning in the company of others, in Singapore. by just how many did. -

View Brochure

th ANNIVERSARY Artist Impression of the School of Law. CONTENTS e First Decade e Founding Years e Future 2 LAW OF SCHOOL 3 LAW OF SCHOOL e idea of the “We were audacious aer “Aer sending in the proposal, I told SMU Law School receiving encouragement – we my colleagues in the Law Department was in the minds were cautioned to take it slowly we had a 50-50 chance of getting a law of the SMU and open the school a few years school. e arguments for it – diversity, later than when we actually did. competition and SMU’s development – leadership from We took a risk but being young were compelling enough, but whether the university’s and impatient, we discarded the proposal would be accepted inception. caution and brought forward depended on the powers that be. When our vision by a few years. In the the good news came, we were elated! end, we pulled it o and the Law It was a great privilege to have been School has been acknowledged involved in the start-up of the SMU Law as one of the nest in Asia since School - a memory I will always cherish.” then. e moral? Carpe diem … seize the day!” Associate Professor Low Kee Yang, School of Law Mr Ho Kwon Ping, Chairman, Board of Trustees, SMU “A Law School was in the original plan of SMU. It’s a natural discipline that ts in well with the original concept of a management university.” Professor Tan Chin Tiong, Senior Advisor to President, SMU 5 LAW OF SCHOOL “I remember receiving a call, as president, in early 2007 saying that the opening of a new “It was vital for the School to law school at SMU had been oer a distinct law education approved. -

Smubrochure.Pdf

SMU LAW SCHOOL The Singapore Government, in a major review of the domestic supply of lawyers, confirmed a shortage of lawyers in Singapore. 2007 hence marked a major milestone in the development of legal education in Singapore – the setting up of the nation’s second law school. SMU is honoured to be entrusted with this important responsibility. As Singapore’s first private university and the only university here with a city campus purpose-built to its pedagogy of small class size and interactive learning, SMU will be extending its unique approach to its School of Law. SMU’s undergraduate law programme aims to mould students into excellent lawyers who will contribute significantly to society. The objective is to produce law graduates who have contextualised legal expertise and the ability to think across disciplines and geographical borders. In terms of pedagogy, SMU’s seminar-style learning will be put to good effect to nurture students who are confident, articulate and analytically agile. CONTENTS 03 Dean’s Message 04 Investing In The Fundamentals // Rigorous and Challenging Curriculum // Holistic Pedagogy & Course Assessment // Optional Second Major // Wide Range of Double Degree Options // Beneficial Internship & Community Service // Internship Partners 09 Commitment To Excellence // Scholarships & Awards // National & International Competitions // International Exchange 12 Career Prospects // Raising The Bar 13 Visionary Campus // City Campus // Facilities 15 Strengthening Our Relevance // Centre for Dispute Resolution // International Islamic Law and Finance Centre // Pro Bono Centre // Asian Peace-building and Rule of Law Programme 18 Heeding The Best // Advisory Board Members 19 Top Notch Faculty // Deanery // Faculty 24 The Fun Stuff // Beyond The Classroom Dean’s Message The School of Law was started in 2007 after a major review of legal education in Singapore concluded that it was timely to have a second law school in Singapore. -

The Singapore Management University School of Law Groundbreaking Event

THE SINGAPORE MANAGEMENT UNIVERSITY SCHOOL OF LAW GROUNDBREAKING EVENT ADDRESS BY THE HONOURABLE ATTORNEY-GENERAL STEVEN CHONG 20 JANUARY 2014 Mr Yong Pung How, Chancellor of Singapore Management University Mr Ho Kwon Ping, Chairman of the Board of Trustees of Singapore Management University Professor Arnoud De Meyer, President of SMU Professor Yeo Tiong Min, Dean of SMU School of Law Distinguished guests Staff, past and present students of SMU School of Law The ground-breaking of the SMU School of Law building is a very historic occasion and I am extremely honoured to be here. As I participate in this event, I am conscious that I follow in the footsteps of the Attorneys-General before me. At every stage of its brief history, SMU School of Law has enjoyed a close affiliation with the office of the Attorney-General. AG Chan Sek Keong chaired the Third Committee on the Supply of Lawyers. This committee recommended the establishment of a second law school in Singapore. Judge of Appeal Chao Hick Tin, as the then AG, was on the governmental panel that reviewed the report of the Steering Committee for the establishment of the School of Law. The current Chief Justice, Mr Sundaresh Menon, and the current dean of the Singapore Institute of Legal Education, Professor Walter Woon, my two 1 immediate predecessors, were founding members of the School of Law’s Advisory Board. The Past At this landmark occasion, it is appropriate, even as we contemplate the future, to gaze into the past. Many of you here today are current students of the law school. -

Lee Kuan Yew Our Founding Prime Minister 1923 – 2015

A commemorative publication by Challenge magazine Remembering Lee Kuan Yew Our Founding Prime Minister 1923 – 2015 His ideas and impact on the Singapore Public Service P • 1 FOREWORD FOUNDING OurPRIME MINISTER... of his legendary attention to detail, his exacting performance standards and the clarity of purpose he applied to every problem. They also found the side of him that was a caring boss. But underpinning all these was Mr Lee’s unwavering dedication to keeping Singapore successful. For Mr Lee, if something was worth doing for Singapore and Singaporeans, it was worth doing it very well. We saw this, for example, in his dedication to the cause of the trade unions, so that Mr Lee Kuan Yew at the 2014 National Day Parade. Source: Suhaimi Abdullah/Getty Images workers can have a share in the fruits of the nation’s progress; his promotion of home ownership so that every Singaporean has a stake in the country; his Our founding Prime Minister, Mr Lee Kuan Yew, personal attention to the greening of Singapore died on March 23, 2015, at the age of 91. which he saw as a means of gifting to every Singaporean, no matter his station in life, a very To say that Mr Lee served Singapore and Singaporeans conducive urban environment. The list is endless. for almost all of his adult life would be understating his extraordinary contributions. Mr Lee and his Mr Lee’s passing is a poignant moment in Singapore’s Old Guard colleagues played indispensable roles in history, a moment for all of us to pause and reflect transforming Singapore from a Third World country on his contributions to Singapore. -

PM Lee Hsien Loong's Speech at the Official Opening of Singapore Management University Law School Building and the Kwa Geok

Singapore Management University Institutional Knowledge at Singapore Management University SMU Press Releases University Heritage 3-2017 PM Lee Hsien Loong's speech at the official opening of Singapore Management University law school building and the Kwa Geok Choo Law Library on 15 March 2017 Hsien Loong LEE Follow this and additional works at: https://ink.library.smu.edu.sg/oh_pressrelease Part of the Asian Studies Commons, Higher Education Commons, and the Law Commons Citation LEE, Hsien Loong. PM Lee Hsien Loong's speech at the official opening of Singapore Management University law school building and the Kwa Geok Choo Law Library on 15 March 2017. (2017). SMU Press Releases. Available at: https://ink.library.smu.edu.sg/oh_pressrelease/154 This Transcript is brought to you for free and open access by the University Heritage at Institutional Knowledge at Singapore Management University. It has been accepted for inclusion in SMU Press Releases by an authorized administrator of Institutional Knowledge at Singapore Management University. For more information, please email [email protected]. PM Lee Hsien Loong officially opened the Singapore Management University law school building and the Kwa Geok Choo Law Library on 15 March 2017 15 March 2017 Speech by PM Lee Hsien Loong http://www.pmo.gov.sg/newsroom/pm-lee-hsien-loong-opening-smu-school-law-building Mr Ho Kwon Ping, Chairman of the Singapore Management University (SMU); Professor Arnoud De Meyer, President of SMU; Professor Yeo Tiong Min, Dean of the School of Law; Chief Justice, ladies and gentlemen. A very good morning to all of you. -

Class and Politics in Malaysian and Singaporean Nation Building

CLASS AND POLITICS IN MALAYSIAN AND SINGAPOREAN NATION BUILDING Muhamad Nadzri Mohamed Noor, M.A. Political Science College of Business, Government and Law Flinders University Submitted in fulfillment of the requirements for the degree of Doctor of Philosophy August 2017 Page Left Deliberately Blank. Abstract This study endeavours to deliver an alternative account of the study of nation-building by examining the subject matter eclectically from diverse standpoints, predominantly that of class in Southeast Asia which is profoundly dominated by ‘cultural’ perspectives. Two states in the region, Malaysia and Singapore, have been selected to comprehend and appreciate the nature of nation-building in these territories. The nation-building processes in both of the countries have not only revolved around the national question pertaining to the dynamic relations between the states and the cultural contents of the racial or ethnic communities in Malaysia and Singapore; it is also surrounded, as this thesis contends, by the question of class - particularly the relations between the new capitalist states’ elites (the rulers) and their masses (the ruled). More distinctively this thesis perceives nation-building as a project by political elites for a variety of purposes, including elite entrenchment, class (re)production and regime perpetuation. The project has more to do with ‘class-(re)building’ and ‘subject- building’ rather than ‘nation-building’. Although this thesis does not eliminate the significance of culture in the nation-building process in both countries; it is explicated that cultures were and are heavily employed to suit the ruling class’s purpose. Hence, the cultural dimension shall be used eclectically with other perspectives. -

Lee Kuan Yew Lee Kuan Yew Blazing the Freedom Trail Blazing the Freedom Trail Lee Kuanyew

Anthony Oei Anthony For Review onlyLEE KUAN YEW LEE KUAN YEW BLAZING THE FREEDOM TRAIL BLAZING THE FREEDOM TRAIL YEW LEE KUAN It was the 1950s, a tumultuous time for post-war Singapore. Disgruntled with the British ruling power, anti-colonial forces were calling for independence. The main contenders were the People’s Action Party led by nationalist Lee Kuan Yew and the Communist Party of Malaya headed by Chin Peng. Displaying their political acumen, Lee and his team overcame all adversities to win the people’s mandate. Lee, who became Singapore’s first Prime Minister in 1959, orchestrated the movement to build a prosperous FREEDOM TRAI Singapore. When he stepped down in 1990, he left behind B L an efficient government, world-class infrastructure and a AZING THE thriving economy. When he died in 2015, he left behind a shining Singapore as his legacy. This book is an updated and revised edition of Days of Thunder: How Lee Kuan Yew Blazed the Freedom Trail (2005). It explores Lee’s leadership during Singapore’s early years and the question: Could Singapore have L achieved as much without Lee Kuan Yew, the founding father of modern Singapore? Marshall Cavendish Editions SINGAPORE/POLITICS ISBN 978-981-4677-77-6 Exploring the leadership of Singapore’s ,!7IJ8B4-ghhhhg! first Prime Minister from 1959 to 1990 Anthony Oei For Review only LEE KUAN YEW BLAZING THE FREEDOM TRAIL QUOTES BY LEE KUAN YEW For Review only The verdict of the people is a terrifying thing. To build a country, you need passion. You will trample over us, over our dead bodies. -

Chan Sek Keong the Accidental Lawyer

December 2012 ISSN: 0219-6441 Chan Sek Keong The Accidental Lawyer Against All Odds Interview with Nicholas Aw Be The Change Sustainable Development from Scraps THE ALUMNI MAGAZINE OF THE NATIONAL UNIVERSITY OF SINGAPORE FACULTY OF LAW Contents DEAN’S MESSAGE A law school, more so than most professional schools at a university, is people. We have no laboratories; our research does not depend on expensive equipment. In our classes we use our share of information technology, but the primary means of instruction is the interaction between individuals. This includes teacher and student interaction, of course, but as we expand our project- based and clinical education programmes, it also includes student-student and student-client interactions. 03 Message From The Dean MESSAGE FROM The reputation of a law school depends, almost entirely, on the reputation of its people — its faculty LAW SCHOOL HIGHLIGHTS THE DEAN and staff, its students, and its alumni — and their 05 Benefactors impact on the world. 06 Class Action As a result of the efforts of all these people, NUS 07 NUS Law in the World’s Top Ten Schools Law has risen through the ranks of our peer law 08 NUS Law Establishes Centre for Asian Legal Studies schools to consolidate our reputation as Asia’s leading law school, ranked by London’s QS Rankings as the 10 th p12 09 Asian Law Institute Conference 10 NUS Law Alumni Mentor Programme best in the world. 11 Scholarships in Honour of Singapore’s First CJ Let me share with you just a few examples of some of the achievements this year by our faculty, our a LAWMNUS FEATURES students, and our alumni. -

Girton150 Asia Celebrations Booklet

ASIA PACIFIC GIRTON 150 ANNIVERSARY CELEBRATIONS Singapore 12-14 April 2019 Girton: the College for Women A BRIEF HISTORY Girton College was founded on 16 October 1869 in Hitchin, thirty miles outside Cambridge. It was known as The College for Women. That it was founded for women was radical; that it was a College - with its own ethos, aims and autonomy - was key to its success. At the time, it was the only residential institution that dared offer degree level education to women. Only five students enrolled in the first year! It was, however, part of a wider, unstoppable movement seeking inclusion for women into all aspects of professional and public life; and it supported women to secure the education they required to win admission to degrees. It was a long journey, even after the move to Cambridge in 1873; but it was propelled by a strong sense of purpose among a self-governing community of scholars who knew they would succeed. DEGREES BY DEGREE Girton’s principal founders, Emily Davies and Barbara Bodichon, knew in their bones that that women could attain the same educational standards as men. Early in 1873 the first Girtonians passed the relevant exams and proved - year in, year out - that they too were capable of academic excellence. However it took years of campaigning and some notable defeats before, in 1948, Cambridge University finally yielded to the inevitable and allowed Her Majesty Queen Elizabeth (Queen consort to George VI) to receive the first degree granted by that University to a woman. Others followed and with that, Girton had fulfilled its foundational aim. -

Lawlink 2017 Contents 03 Contents

December 2017 ISSN: 0219 - 6441 Honouring EW Barker PLUS NUS Law Celebrates Moot Victories Diamond Jubilee New Centre for Pro Bono Efforts Faculty Features Book Launches Pioneer Graduates Welcome New Generation New Masters in International Arbitration REUNIONS! & Dispute Resolution Classes of 1982, 1987, 1992, 1997 & 2007 THE ALUMNI MAGAZINE OF From left: Ambassador-at-Large Professor Tommy Koh ‘61, Dean of NUS Law Professor Simon Chesterman, THE NATIONAL UNIVERSITY OF SINGAPORE former Chief Justice Mr Chan Sek Keong ‘61, Emeritus Professor Koh Kheng Lian ‘61, FACULTY OF LAW Ms Tan Leng Fong ‘61 and Mr Amarjeet Singh SC ‘61 PIONEER GRADUATES WELCOME NEXT GENERATION The Class of 1961 joined the Class of 2017 at this year’s Commencement on 8 July at the University Cultural Centre Members of the Class of 1961 at Commencement 2017. Front row (from left): Ms Aileen Lim, Ms Tan Leng Fong, and Emeritus Professor Koh Kheng Lian Back row (from left): Ambassador-at-Large Professor Tommy Koh, Mr Foo Yew Heng, Mr Amarjeet Singh SC, former Chief Justice Mr Chan Sek Keong, and former Solicitor- General Mr Koh Eng Tian This year marked the 60th Anniversary of firms thought that those who qualified As over 300 of this year’s graduates sat the first intake of law students at NUS in England had a superior hallmark. among the faculty’s pioneer batch and and the Faculty was particularly delighted But the Class of 1961 quickly put that renowned members of our alumni, it was to welcome eight members from this misconception right. I would like to a timely reminder of how the Class of 1961 first cohort (the Class of 1961) who were recognise three of them whom as a law set the bar high for all the generations present to share the celebrations! student I looked up to.