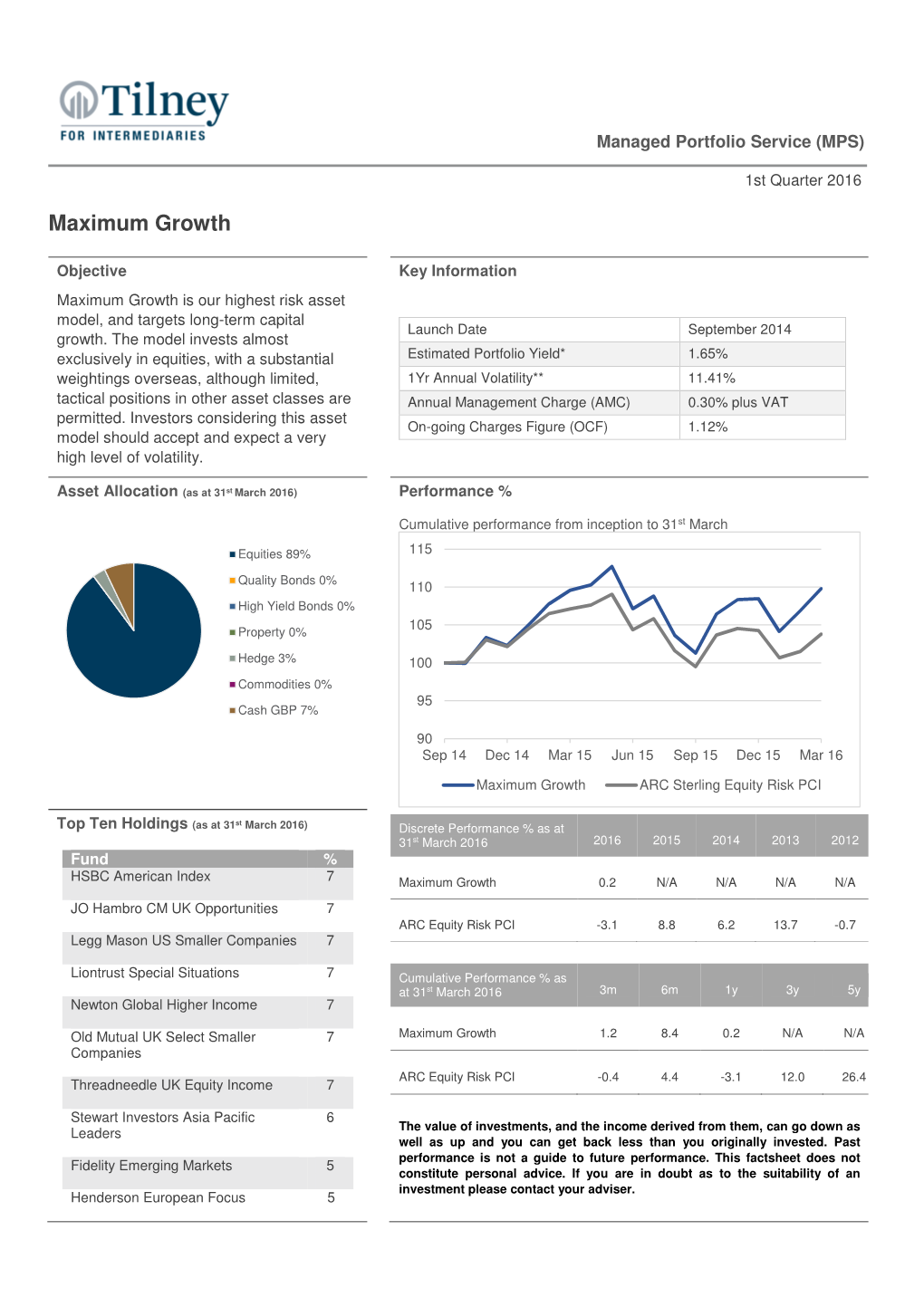

Maximum Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

The London School of Economics and Political Science

The London School of Economics and Political Science Thesis Foreign Government Loan Issues on the London Capital Market, 1870 - 1913, with Special Reference to Japan by Toshio SUZUKI A Thesis submitted to the University of London for the Degree of Doctor of Philosophy, 1991 February UMI Number: U050B50 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. Dissertation Publishing UMI U050B50 Published by ProQuest LLC 2014. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 F 6&'F- x6( I o 7<>c Abstract This thesis examines foreign government loan issues on the London capital market in the period from 1870 to 1913, with special reference to Japan. Chapter One provides an overview of foreign government loan issues in London. Chapter Two deals with a number of more specific topics: the development of the loan issue organisations on the market, and the role and involvement of various types of financial institutions in loan issue business. Later Chapters mainly take up the detailed history of Japanese government loan issues, referring to domestic Japanese financial conditions. Chapters Three to Seven examine the development of Japanese government loan issues on the international capital markets. -

Societe Generale Private Banking Hambros

SOCIETE GENERALE PRIVATE BANKING HAMBROS SPRING/SUMMER 2016 – N°9 James Welling – Choreograph, 2014-2015, Ink jet print, 160x107cm. New acquisition 02 02 04 04 06 06 08 ECONOMICECONOMIC OUTLOOK OUTLOOK EXPERTISE EXPERTISE PORTRAIT PORTRAITPRIVATE BANKING OIL, AOIL, DIFFERENT A DIFFERENT HEDGE FUNDSHEDGE FUNDS IGNACE IGNACEOUR REGIONAL ENVIRONMENTENVIRONMENTA TIME OF RENEWALA TIME OF RENEWALVAN DOORSELAEREVAN DOORSELAEREEXPANSION CEO, VAN DE VELDE CEO, VAN DE VELDE WE ARE PROUD SPONSOR OF THE V&A’S MAJOR EXHIBITION BOTTICELLI REIMAGINED MARCH 5 – JULY 3, 2016 VICTORIA AND ALBERT MUSEUM, LONDON SOCIETEGENERALE.CO.UK Societe Generale is a French credit institution (Bank) authorised and supervised by the European Central Bank (ECB) and the Autorité de Contrôle Prudentiel et de Résolution (ACPR) (the French Prudential Control and Resolution Authority) and regulated by the Autorité des marchés financiers (the French financial markets regulator) (AMF). Societe Generale, London Branch is authorised by the ECB, the ACPR and the Prudential Regulation Authority (PRA) and subject to limited regulation by the Financial Conduct Authority (FCA) and the PRA. Details about the extent of our authorisation, supervision and regulation by the above mentioned authorities are available from us on request. FFGROUP © MICHEL LABELLE ANDY PARADISE ‘PARADISE T/AS PHOTO’ WelcomeA RENOVATED to the EUROPEAN Spring issue ORGANISATION of La Lettre. The transformation of private banks is gaining pace under the impulse of regulatory changes,The transformation the revolution of private in information banks istechnologies gaining pace and under changes the impulsein behaviour. These upheavalsof regulatory changes, are often the presented revolution as in constraints, information but technologies we see them and as changes an excellent inopportunity behaviour. -

Special Operations Executive - Wikipedia

12/23/2018 Special Operations Executive - Wikipedia Special Operations Executive The Special Operations Executive (SOE) was a British World War II Special Operations Executive organisation. It was officially formed on 22 July 1940 under Minister of Economic Warfare Hugh Dalton, from the amalgamation of three existing Active 22 July 1940 – 15 secret organisations. Its purpose was to conduct espionage, sabotage and January 1946 reconnaissance in occupied Europe (and later, also in occupied Southeast Asia) Country United against the Axis powers, and to aid local resistance movements. Kingdom Allegiance Allies One of the organisations from which SOE was created was also involved in the formation of the Auxiliary Units, a top secret "stay-behind" resistance Role Espionage; organisation, which would have been activated in the event of a German irregular warfare invasion of Britain. (especially sabotage and Few people were aware of SOE's existence. Those who were part of it or liaised raiding operations); with it are sometimes referred to as the "Baker Street Irregulars", after the special location of its London headquarters. It was also known as "Churchill's Secret reconnaissance. Army" or the "Ministry of Ungentlemanly Warfare". Its various branches, and Size Approximately sometimes the organisation as a whole, were concealed for security purposes 13,000 behind names such as the "Joint Technical Board" or the "Inter-Service Nickname(s) The Baker Street Research Bureau", or fictitious branches of the Air Ministry, Admiralty or War Irregulars Office. Churchill's Secret SOE operated in all territories occupied or attacked by the Axis forces, except Army where demarcation lines were agreed with Britain's principal Allies (the United Ministry of States and the Soviet Union). -

The Perfin Foreign Bill Stamps of Great Britain

THE PERFIN FOREIGN BILL STAMPS OF GREAT BRITAIN THE PERFIN FOREIGN BILL STAMPS OF GREAT BRITAIN By Jeff Turnbull THE PERFIN FOREIGN BILL STAMPS OF GREAT BRITAIN PART ONE FOREIGN BILL STAMPS © COPYRIGHT 2021 THE PERFIN FOREIGN BILL STAMPS OF GREAT BRITAIN DEDICATION This opening page is dedicated to the Late Mr. Kevin Parkhill of Rochdale, a keen Perfin Society member, who initiated this study of the perfined revenue stamps of Great Britain. I would not have been able to produce this catalogue without Kevin's notes, papers and correspondence from perfin collectors around the world. You all know who you are, so many thanks indeed for your information which has culminated in this first specialised edition of a GB Foreign Bill Perfin Revenue Catalogue. THE PERFIN FOREIGN BILL STAMPS INTRODUCTIONOF GREAT BRITAIN The following pages have been put together with the intention of helping the collector of perfinned revenue stamps, it is by no means complete, hopefully collectors who have additional information will let me know the details, and more pages will be made up as and when. As there is no present perfinned Revenue cataloguing system I am adopting a new system, using the letter followed by two numbers and two decimal places. A single letter "M" after the catalogue number indicates a Multi headed die. I.E. A 23.01. Where the perfin is already catalogued in the New Gault Illustrated perfin catalogue on postage stamps, then this catalogue number will also be alongside. At this moment in time only different Reigns will be used, with an accompanying list of stamps on which the perfin has been seen. -

Intelligence and the War Against Japan Britain, America and the Politics of Secret Service

Intelligence and the War against Japan Britain, America and the Politics of Secret Service Richard J. Aldrich PUBLISHED BY THE PRESS SYNDICATE OF THE UNIVERSITY OF CAMBRIDGE The Pitt Building, Trumpington Street, Cambridge, United Kingdom CAMBRIDGE UNIVERSITY PRESS The Edinburgh Building, Cambridge CB2 2RU, UK http: // www.cup.cam.ac.uk 40 West 20th Street, New York NY 1011–4211, USA http: // www.cup.org 10 Stamford Road, Oakleigh, Melbourne 3166, Australia Richard Aldrich 2000 This book is in copyright. Subject to statutory exception and to the provisions of relevant collective licensing agreements, no reproduction of any part may take place without the written permission of Cambridge University Press. First published 2000 Printed in the United Kingdom at the University Press, Cambridge Typeset in Times 10/12pt [WV] A catalogue record for this book is available from the British Library Library of Congress cataloguing in publication data Aldrich, Richard J. (Richard James), 1961– Intelligence and the War against Japan: Britain, America and the politics of secret service / Richard J. Aldrich. p. cm. Includes bibliographical references and index. ISBN C 521 64186 1 (hardbound) 1. World War, 1939–1945 – Secret service – Great Britain. 2. World War, 1939– 1945 – Secret service – United States. 3. World War, 1939–1945 – Asia. I. Title. D810.S7A482 2000 940.54′ 8641 – dc21 99–29697 CIP ISBN 0 521 64186 1 (hardback) Contents List of plates page xi List of maps xiii Preface xiv Acknowledgements xvii List of abbreviations xix 1 Introduction: intelligence -

Kleinwort Hambros Elite PCC Limited Scheme Particulars

28 August 2020 Kleinwort Hambros Elite PCC Limited Scheme Particulars Scheme Particulars Kleinwort Hambros Elite PCC Limited (A protected cell company registered with limited liability in Guernsey with registration number 42365.) Important Information This document is not available for general distribution in, from or into the United Kingdom because the Company is an unregulated collective investment scheme whose promotion is restricted by sections 238 and 240 of the Financial Services and Markets Act 2000 (“FSMA”). SG Kleinwort Hambros Bank (CI) Limited (formerly Kleinwort Benson (Channel Islands) Investment Management Limited) has given written notification to the FCA for the purposes of regulation 59 of the Alternative Investment Fund Management Regulations 2013 (the “AIFMR”). When distributed in, from or into the United Kingdom, this document is only intended for professional investors within the meaning of regulation 2(1) of the AIFMR, investment professionals within article 14 of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 (as amended) (“SPO”)); sophisticated investors within article 23 of the SPO, being individuals who have signed within a period of 12 months a statement complying with article 23 of the FPO; high net worth companies, unincorporated associations and others within article 22 of the SPO; (together “eligible persons”), persons outside the European Economic Area receiving it electronically, persons outside the United Kingdom receiving it non-electronically and any other persons to whom it may be communicated lawfully. No other person should act or rely on this document. Other persons distributing this document in, from or into the United Kingdom must satisfy themselves that it is lawful to do so. -

1 the Napoleon of Finance1 and the End of Finance Capitalism. Emil

The Napoleon of Finance1 and the end of Finance Capitalism. Emil Glückstadt and the collapse of Landmandsbanken in 1922. Per H. Hansen, Copenhagen Business School, [email protected] [This is a draft only. Please do not quote. Comments are welcome] Introduction Over the last few decades of deregulation a new narrative has been constructed that have made the business leader, the entrepreneur, the financier and private equity capitalists into our new heroes.2 The authors of this narrative have to a large degree been the heroes themselves well assisted by the media, academics and others. The “business and finance leader as hero”-narrative means that emphasis has shifted from distribution and redistribution of the “cake” (GDP) to what size the cake has. The more or less implicit assumption is that if the cake is large enough everyone will get their fair share, a rather doubtful assumption. It could be argued that this construction of a new hero of the deregulated, globalized Western economies had led to financialization of the economy and, ultimately, to the financial crisis of 2007 to 2009. If this thesis is sustainable, it could perhaps be further argued that the reason that the financial crisis was so deep and so serious was related to the degree of deregulation and financialization of the economy.3 I am not going to analyze the current crisis, however. Rather, my aim in this paper is to contribute to an understanding of one the bank manager, Emil Glückstadt, and his bank, Landmandsbanken’s role in the Danish financial system and the financial crisis in Denmark in the interwar period. -

Weekly Update

Investment Strategy 5 February 2021 C0 | EXTERNAL PUBLICATION WEEKLY UPDATE Of stimulus and prices Recent discussions in Washington have strengthened hope that President Biden’s $1.9 tn fiscal plan could make progress in Congress, while the rapid ramp-up in vaccinations – 10.2% of the US population, 15.8% in the UK (see the left-hand chart below) – has lent weight to the prospect of cyclical economic recovery later this year. With recent inflation figures in the euro zone and the US surprising on the upside, investors have continued to position themselves for reflation. What does all this mean for the economic outlook and for markets? This week, Biden began talks with a group of moderate Republican senators who had proposed a $618 bn alternative plan. Although the Democrats’ majority in Congress means bipartisan support for his package may not be necessary, the President is looking to the longer term. By seeking to build bridges and engage with the Republicans, he may slow approval of the current plan but he may also garner support for his separate $2 tn stimulus plan which is due later this year. The two plans are very different in nature. The current proposal seeks to provide support for households (via $1,400 cheques), schoolchildren ($130 bn to accelerate school reopenings), the unemployed (an additional $400 per week in benefits) and state and local governments ($350 bn cash injection to prevent lay-offs of public sector employees). The second plan aims to focus on investment in green energy technologies and infrastructure, for example in transportation, electricity and construction. -

1914 and 1939

APPENDIX PROFILES OF THE BRITISH MERCHANT BANKS OPERATING BETWEEN 1914 AND 1939 An attempt has been made to identify as many merchant banks as possible operating in the period from 1914 to 1939, and to provide a brief profle of the origins and main developments of each frm, includ- ing failures and amalgamations. While information has been gathered from a variety of sources, the Bankers’ Return to the Inland Revenue published in the London Gazette between 1914 and 1939 has been an excellent source. Some of these frms are well-known, whereas many have been long-forgotten. It has been important to this work that a comprehensive picture of the merchant banking sector in the period 1914–1939 has been obtained. Therefore, signifcant efforts have been made to recover as much information as possible about lost frms. This listing shows that the merchant banking sector was far from being a homogeneous group. While there were many frms that failed during this period, there were also a number of new entrants. The nature of mer- chant banking also evolved as stockbroking frms and issuing houses became known as merchant banks. The period from 1914 to the late 1930s was one of signifcant change for the sector. © The Editor(s) (if applicable) and The Author(s), 361 under exclusive licence to Springer Nature Switzerland AG 2018 B. O’Sullivan, From Crisis to Crisis, Palgrave Studies in the History of Finance, https://doi.org/10.1007/978-3-319-96698-4 362 Firm Profle T. H. Allan & Co. 1874 to 1932 A 17 Gracechurch St., East India Agent. -

Hambros Bank - Wikipedia

1/9/2019 Hambros Bank - Wikipedia Hambros Bank Hambros Bank was a British bank based in London. The Hambros bank was Hambros Bank a specialist in Anglo-Scandinavian business with expertise in trade finance and investment banking, and was the sole banker to the Scandinavian kingdoms for many years. The Bank was sold in 1998, and today survives only in the name of the private banking division of the French group Société Générale. Contents History Early history Pre-war and Second World War Post-war development Shipping crises and Hilmar Reksten Hambro family break up Sale to Société Générale Formation of boutiques and spin-offs SG Hambros References Former type Public Sources Industry Banking Fate Acquired History Successor Société Générale Founded 1839 Defunct 2016 Early history Headquarters London, UK Hambros was founded by the Danish merchant and banker Carl Joachim Key people Chips Keswick Hambro in London in 1839 as C. J. Hambro & Son. During the 1850s he was (Chairman) responsible for arranging various British Government loan stock issues enabling the bank to prosper.[1] Pre-war and Second World War After merging with the British Bank of Northern Commerce (owned by Enskilda Banken and a number of Scandinavian savings banks) in 1921 the name was changed to Hambros Bank, and the firm expanded. As a result, in 1926 a bigger head office was constructed at 41 Bishopsgate, where the bank remained until 1988. The 1930 depression affected the bank's international business and it concentrated on domestic lending and Scandinavia. During World War II, Sir Charles Hambro raised finance for the Norwegian exiled government and was also the head of the Special Operations Executive.[2] Post-war development https://en.wikipedia.org/wiki/Hambros_Bank 1/4 1/9/2019 Hambros Bank - Wikipedia After the Second World War, Hambros became also known as the 'diamond bank' with its thriving activity in financing the diamond industry and its trade.[3] Hambros was one of the top three banks in the Euromarket by the mid-1960s. -

Ws Kleinwort Hambros Growth Fund

30 JUNE 2021 WS KLEINWORT HAMBROS GROWTH FUND Market commentary Fund details Despite positive economic data and company commentary, bond yields fell before and after the Benchmark Federal Reserve meeting. That meeting signalled a slightly earlier increase in interest rates than Morningstar EAA Fund GBP had previously been communicated. This is an entirely reasonable position for the Fed to take Moderately Adventurous Allocation given the evidence of economic recovery and inflationary pressures. Fund classes available Company commentary suggests vibrant trading conditions – many businesses reporting sales A Class materially above 2019 levels, product shortages and difficulties getting labour. We currently see this as transitory but are watching the data closely for indicators that would prompt a change of Fund size as at 30 June 2021 view. £76.9 million In line with lower bond yields and a more defensive market, most commodity prices continued to retreat from their mid-May highs, albeit it was noticeable that iron ore recovered markedly from its Base currency prior month’s weakness. Sterling The fund’s equities were the largest positive contributors, though its bond allocation added Price listing modestly: alternatives were a detractor. Within equities all regions expect the UK added value, Bloomberg led by the US and supported by the emerging markets, European and Japanese positions. While many of the portfolio’s funds delivered positive returns, the following were worthy of mention, Bloomberg ticker Loomis Sayles US Growth Equity, Pictet Global Environmental Opportunities, BlackRock Income units – CFKBCAI LN Continental European Flexible and Baillie Gifford Japanese. Accumulation units – CFKBCAA LN The fixed income positioning saw small gains from both its government and credit exposure.