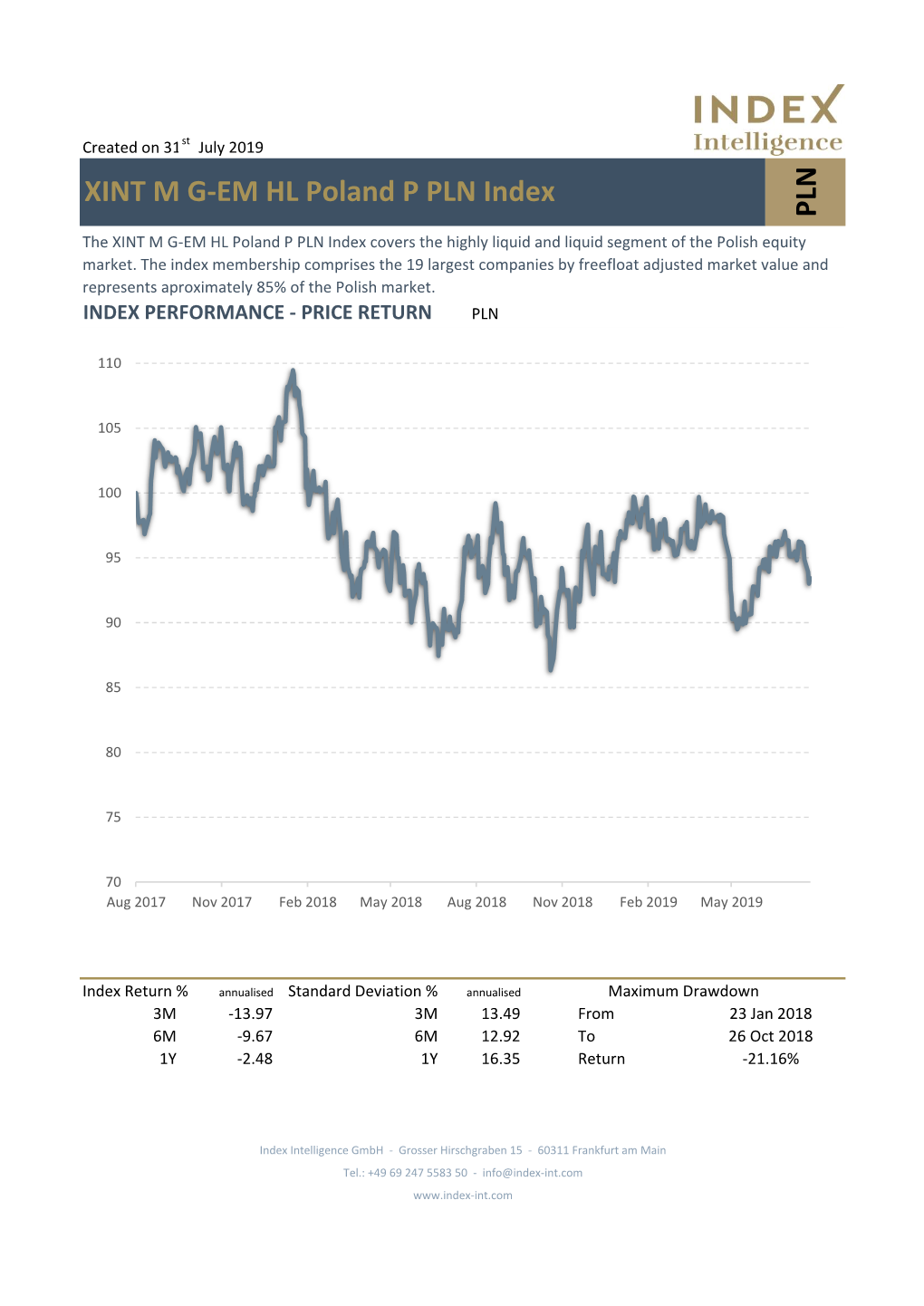

PLN XINT M G-EM HL Poland P PLN Index

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TGE and Pgnig Embark on Cooperation with a View to Developing a Biomethane Market in Poland

Warsaw, 12 January 2021 TGE and PGNiG embark on cooperation with a view to developing a biomethane market in Poland Press Release On 12 January Towarowa Giełda Energii (TGE) and Polish Oil and Gas Company (PGNiG) signed a cooperation agreement aimed at leveraging their mutual expertise and capabilities in creating a biomethane market in Poland. TGE and PGNiG intend to jointly prepare modern solutions supporting the creation and development of a biomethane market in Poland. The expertise of both PGNiG, as a key player on the gas market, and of TGE as a trading platform where the trading in gas and certificates promoting the use of RES are concentrated, should contribute to the transformation of the energy market leading not only to increased significance of green technologies but also the emerging market for alternative fuels, such as biomethane or hydrogen. ‘For over 20 years, TGE has been supporting all transformation processes on the energy market and actively contributing to its development by offering its participants comprehensive solutions and products. The cooperation with PGNiG in creating a biomethane market is an opportunity for the Exchange to further develop the RES segment. Certainly, our registers have a key role to play in this project’ said Piotr Zawistowski, President of the Management Board of TGE. ‘PGNiG has been an active member of the gas exchange market since its inception and continues to contribute to its development, as evidenced, among other things, by the record-high volume of natural gas trading on TGE in 2020. Now we are about to a new chapter of cooperation, which will allow us to create modern market solutions in the field of biomethane trading. -

CD PROJEKT RED and NVIDIA Partner to Bring Ray Tracing to ‘Cyberpunk 2077’

CD PROJEKT RED and NVIDIA Partner to Bring Ray Tracing to ‘Cyberpunk 2077’ Highly Acclaimed, Highly Anticipated Game Uses Real-Time Ray Tracing E3--NVIDIA and CD PROJEKT RED today announced that NVIDIA® GeForce RTX™ is an official technology partner for Cyberpunk 2077 and that the companies are working together to bring real-time ray tracing to the game. Cyberpunk 2077 won over 100 awards at E3 2018 and Gamespot calls it “one of the most anticipated games of the decade.'' The game is the next project from CD PROJEKT RED, makers of the highly acclaimed The Witcher 3: Wild Hunt, which has won numerous “Game of the Year'' awards. NVIDIA and CD PROJEKT RED have a long history of technology collaboration that spans more than a decade. “Cyberpunk 2077 is an incredibly ambitious game, mixing first-person perspective and deep role-playing, while also creating an intricate and immersive world in which to tell its story,'' said Matt Wuebbling, head of GeForce marketing at NVIDIA. “We think the world of Cyberpunk will greatly benefit from the realistic lighting that ray tracing delivers.'' Ray tracing is the advanced graphics technique used to give movies their ultra-realistic visual effects. NVIDIA GeForce RTX GPUs contain specialized processor cores designed specifically to accelerate ray tracing so the visual effects in games can be rendered in real time. “Ray tracing allows us to realistically portray how light behaves in a crowded urban environment,'' says Adam Badowski, head of Studio at CD PROJEKT RED. “Thanks to this technology, we can add another layer of depth and verticality to the already impressive megacity the game takes place in.'' Cyberpunk 2077 is an open-world, action-adventure story set in Night City, a megalopolis obsessed with power, glamour and body modification. -

Enea, Energa, LPP, Pekao, PGE, Pgnig, Tauron, Asseco Poland

Dziennik 21 listopada 2018 r. Najważniejsze informacje: Indeksy GPW zmiana WIG otw. 55 635,5 0,1% Enea, Energa - Udział banków w finansowaniu bloku w Elektrowni Ostrołęka wyniesie 30-35% - WIG zam. 55 205,5 -1,3% Tchórzewski obrót (mln PLN) 880,0 -2,3% Energa - Energa rozpoczyna budowę hybrydowego magazynu energii WIG 20 otw. 2 181,1 0,4% LPP - LPP spodziewa się w przyszłości raczej jednocyfrowych wzrostów sprzedaży LFL WIG 20 zam. 2 160,6 -1,3% FW20 otw. 2 177,0 0,7% LPP - LPP uważa, że utrzymanie w ‘19 podobnych marż rdr jest ambitne, ale możliwe FW20 zam. 2 163,0 -1,1% LPP - LPP chce w '19 zwiększyć sprzedaż dwucyfrowo mWIG40 otw. 3 813,3 -0,2% Pekao - Pekao podtrzymuje cele strategii do '20; koszty ryzyka mogą wzrosnąć do ok. 50 pb mWIG40 zam. 3 772,3 -1,2% PGE - PGE podpisało umowę na dostawę węgla z PGG o szacowanej wartości 5,25 mld PLN Największe wzrosty kurs zmiana PGNiG - Zysk netto grupy PGNiG w III kw '18 wyniósł 554 mln PLN, zgodnie z szacunkami Grupa Azoty 28,00 6,1% Tauron - Tauron szacuje, że przychody grupy z rynku mocy w '21 wyniosą 642,25 mln PLN LiveChat Software 27,40 3,8% Sektor energetyczny - Cena w aukcji rynku mocy na rok 2021 wynosi 240,32 PLN/kW/rok PZU 40,40 2,3% ING BSK 182,00 1,7% Asseco Poland - Wyniki Asseco Poland w III kw. 2018 roku vs. konsensus PAP 11 bit studios 235,00 1,1% Asseco Poland - Portfel zamówień grupy Asseco na '18 ma wartość 8,786 mld PLN Atal - Wyniki Atalu w III kw. -

CD Projekt Bloomberg: CDR PW Equity, Reuters: CDR.WA

CD Projekt Bloomberg: CDR PW Equity, Reuters: CDR.WA Kupuj, 106,00 PLN 11 września 2017 r., 07:30 Podtrzymana Kampania dla inwestorów Wyniki 1H 17 udowodniły dobrą monetyzację Gwinta. Co najważniejsze, bardzo podoba Informacje nam się naszkicowana przez firmę ścieżka rozwoju gry. Tak jak przewidywaliśmy w Kurs akcji (PLN) 94,65 poprzedniej rekomendacji CD Projekt zaczął już działać na dwóch silnikach. Starszy silnik Upside 12% – Wiedźmin 3 ciągle sprzedają się fenomenalnie (powyżej oczekiwań). Jednocześnie Liczba akcji (mn) 96,12 najlepsze, konkurencyjne firmy na rynku gier przeżywają boom. W związku z tym Kapitalizacja (mln PLN) 9 097,76 podnosimy naszą wycenę CD Projekt do PLN 106, utrzymując rekomendację Kupuj. Free float 67% Free float (mln PLN) 6 060,02 Choć Gwint przeżywa lepsze i gorsze momenty na swojej ścieżce wzrostu, trzeba przyznać, Free float (mln USD) 1 714,58 że całościowy obraz i monetyzacja projektu wygląda bardzo dobrze. Największe wrażenie EV (mln PLN) 8 411,15 robi na nas projekt dodatku do gry (kampania dla jednego gracza), który naszym zdaniem Dług netto (mln PLN) -686,61 będzie mocno przypominał samodzielną grę dla jednego gracza. To może bardzo poszerzyć jego sprzedaż i później zwiększyć bazę graczy internetowych. Dywidenda Stopa dywidendy (%) 1,1% Wydaje nam się również, że niedługo pojawi się na horyzoncie mobilna wersja gry Gwinta – Odcięcie dywidendy 29.05.2017 będzie to bardzo mocnym impulsem dla projektu. Taki ruch w przeszłości więcej niż podwoił lidera tej niższy (grę Hearthstone). W przypadku Gwinta wydawał się dość trudny Akcjonariusze % Akcji technicznie i obarczony pewnym ryzykiem, ale sądzimy, że jego prawdopodobieństwo Marcin Iwiński 12,64 wyraźnie się zwiększa. -

Management Board's Report on Operations Of

Asseco Group Annual Report for the year ended December 31, 2019 Present in Sales revenues 56 countries 10 667 mPLN 26 843 Net profit attributable highly commited to the parent employees company's shareholders 322.4 mPLN Order backlog for 2020 5.3 bPLN 7 601 mPLN market capitalization 1) 1) As at December 30, 2019 Asseco Group in 2019 non-IFRS measures (unaudited data) Non-IFRS figures presented below have not been audited or reviewed by an independent auditor. Non-IFRS figures are not financial data in accordance with EU IFRS. Non-IFRS data are not uniformly defined or calculated by other entities, and consequently they may not be comparable to data presented by other entities, including those operating in the same sector as the Asseco Group. Such financial information should be analyzed only as additional information and not as a replacement for financial information prepared in accordance with EU IFRS. Non-IFRS data should not be assigned a higher level of significance than measures directly resulting from the Consolidated Financial Statements. Financial and operational summary: • Dynamic organic growth and through acquisitions – increase in revenues by 14.4% to 10 667.4 mPLN and in operating profit by 22.5% to 976.2 mPLN (1 204.4 mPLN EBIT non-IFRS – increase by 14.9%) • International markets are the Group’s growth engine – 89% of revenues generated on these markets • Double-digit increase in sales in the Formula Systems and Asseco International segments • 81% of revenues from the sales of proprietary software and services • Strong business diversification (geographical, sectoral, product) Selected consolidated financial data for 2019 on a non-IFRS basis For the assessment of the financial position and business development of the Asseco Group, the basic data published on a non-IFRS basis constitute an important piece of information. -

Asseco Poland, CCC, CD Projekt, Dino Polska, JSW

Dziennik 20 sierpnia 2019 r. Komentarz dnia: Indeksy GPW zmiana WIG otw. 55 756,5 -0,1% Trwa sezon publikacji wyników finansowych. Ostateczne dane Lotosu za drugi kwartał 2019 są WIG zam. 56 035,2 1,5% zgodne ze wstępnymi wynikami i oceniamy je neutralnie. Neutralnie podchodzimy także do wyników Dino i Alumetalu. W przypadku Dino dane są nieco lepsze niż oczekiwania rynkowe, obrót (mln PLN) 632,3 -24,4% ale nieco poniżej naszych szacunków. Podoba nam się silny wzrost przychodów (+38% r/r) oraz WIG 20 otw. 2 078,8 -0,3% utrzymanie wysokiej marży brutto. Uważamy, że wysoka inflacja żywności jest czynnikiem WIG 20 zam. 2 102,2 1,8% sprzyjającym wynikom spółki. W odniesieniu do Alumetalu wyniki są zbieżne z naszymi FW20 otw. 2 085,0 -0,1% oczekiwaniami. Dostrzegamy spadek wolumenów, ale jednocześnie wyższe marże. FW20 zam. 2 103,0 1,5% mWIG40 otw. 3 775,5 -0,1% Z pozytywnych danych warto wskazać na wyniki Netii. Są one powyżej oczekiwań, zwłaszcza na mWIG40 zam. 3 778,5 0,6% poziomie zysku netto. W wynikach spółki widać wyraźnie pozytywny efekt oszczędności kosztowych (przede wszystkim na kosztach wynagrodzeń). Największe wzrosty kurs zmiana Mieszane wstępne wyniki podało CCC. Z jednej strony są one wyraźnie słabsze r/r, ale z drugiej Cyfrowy Polsat 28,00 4,6% wyższe niż nasze prognozy. Sumarycznie oceniamy je zatem lekko pozytywnie. Na plus należy mBank 317,00 4,6% wskazać spadek kosztów w sklepach CCC oraz dobre wyniki sprzedażowe segmentu e- commerce. Na minus natomiast zwracają uwagę wysokie koszty w nowo przejętych markach GTC 9,58 4,0% (Gino Rossi, Vogele). -

Using the Idea of Market-Expected Return

BUSINESS, MANAGEMENT AND EDUCATION ISSN 2029-7491 print / ISSN 2029-6169 online 2012, 10(1): 11–24 doi:10.3846/bme.2012.02 USING THE IDEA OF MARKET-EXPECTED RETURN RATES ON INVESTED CAPITAL IN THE VERIFICATION OF CONFORMITY OF MARKET EVALUATION OF STOCK-LISTED COMPANIES WITH THEIR INTRINSIC VALUE Paweł Mielcarz1, Emilia Roman2 1Kozminski University, Jagiellonska 57/59, 03-301 Warsaw, Poland 2DCF Consulting Sp. z o.o., Kochanowskiego 24, 05-071 Sulejowek, Poland E-mails: [email protected] (corresponding author); [email protected] Received 02 October 2011; accepted 07 March 2012 Abstract. This article presents the concept of investor-expected rates of return on capital of listed companies and the use of these rates in the assessment of the extent to which the stock evaluation of a given entity is compatible with its intrinsic value. The article also features results of the research aimed at verification – with the use of the presented tool – of whether the market value of WSE-listed companies reflects their fundamental value. The calculations presented in the empirical part of the article show that at the beginning of 2011, market evaluation of the most of the analysed entities greatly exceeded their fundamental value. Keywords: DCF, EVA, valuation, capital markets, fundamental analysis, ROIC, intrinsic value. Reference to this paper should be made as follows: Mielcarz, P.; Roman, E. 2012. Using the idea of market-expected return rates on invested capital in the verifica- tion of conformity of market evaluation of stock-listed companies with their intrin- sic value, Business, Management and Education 10(1): 11–24. -

Inflated Hopes Or a Promising Alternative? Evaluating Impact of LNG on Polish Energy Security

University of Pennsylvania ScholarlyCommons Wharton Research Scholars Wharton Undergraduate Research 5-2019 Inflated Hopes or a Promising Alternative? Evaluating Impact of LNG on Polish Energy Security Przemyslaw Stefan Macholak University of Pennsylvania Follow this and additional works at: https://repository.upenn.edu/wharton_research_scholars Part of the Business Commons Macholak, Przemyslaw Stefan, "Inflated Hopes or a Promising Alternative? Evaluating Impact of LNG on Polish Energy Security" (2019). Wharton Research Scholars. 179. https://repository.upenn.edu/wharton_research_scholars/179 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/wharton_research_scholars/179 For more information, please contact [email protected]. Inflated Hopes or a Promising Alternative? Evaluating Impact of LNG on Polish Energy Security Keywords energy security, LNG Disciplines Business This thesis or dissertation is available at ScholarlyCommons: https://repository.upenn.edu/ wharton_research_scholars/179 INFLATED HOPES OR A PROMISING ALTERNATIVE? EVALUATING IMPACT OF LNG ON POLISH ENERGY SECURITY. By Przemyslaw Stefan Macholak An Undergraduate Thesis submitted in partial fulfillment of the requirements for the WHARTON RESEARCH SCHOLARS Faculty Advisor: Anna Mikulska Ph.D. Senior Fellow at Kleinman Center for Energy Policy THE HUNTSMAN PROGRAM IN INTERNATIONAL STUDIES AND BUSINESS THE WHARTON SCHOOL, UNIVERSITY OF PENNSYLVANIA MAY 2019 1. Introduction Over the last 10 years, global energy landscape has been significantly -

Pgnig: Accumulate (Reiterated) PGN PW; PGN.WA | Gas & Oil, Polska

Wednesday, July 27, 2016 | update PGNiG: accumulate (reiterated) PGN PW; PGN.WA | Gas & Oil, Polska High FCF Guarantees Sustained Dividends Current Price PLN 5.50 Target Price PLN 6.06 PGNiG has generated a total return of 13% since our last update in April, outperforming the WIG20 index by 19 points, and at the Market Cap PLN 32.45bn current level the first-quarter positive earnings surprise is fully Free Float PLN 9.47bn priced in. That said, we still see upside potential in the Company ADTV (3M) PLN 65.18m even despite a disappointing preliminary second-quarter report, and we maintain an accumulate rating for PGN with the price target Ownership raised to PLN 6.06 per share. We have upgraded our FY2017 outlook for the Power Generation business and the E&P business which will State Treasury 70.83% more than offset the slowdown in Trade and in Distribution. According to our calculations, PGNiG will end 2016 with a net debt Others 29.17% close to zero even after this year's acquisitions, and with the 2017- 2018 FCF projected at PLN 1.9bn this leaves a thick cash cushion to Business Profile sustain dividends. PGNiG is still at risk of becoming involved in PGNiG is Poland’s largest natural gas company with furthering the government's energy policy, but at this time there are annual sales exceeding 14 billion cubic meters. The no specific plans on the table (the potential acquisitions of EDF Company produces 4.5bcm of gas and 1.2mmt of Poland assets or Petrobaltic should not significantly hurt crude oil per year (including from international deposits, most notably the Skarv project in shareholder value, and the Norway pipeline plans are a remote Norway). -

Santander Bank Polska, Asseco Poland, Energa, Enea

Dziennik 27 grudnia 2019 r. Komentarz dnia: Indeksy GPW zmiana WIG otw. 57 176,1 0,0% KNF zaktualizowała indywidualne bufory kapitałowe wymagane w przypadku wypłaty WIG zam. 57 569,7 0,0% dywidendy dla banków Santander oraz Handlowego. To powinno pozwolić BHW wypłacić 100% zysku. Podobny mechanizm może zadziałać w przypadku Pekao. obrót (mln PLN) 464,8 0,0% WIG 20 otw. 2 128,7 0,0% WIG 20 zam. 2 142,5 0,0% WIG30: FW20 otw. 0,0 FW20 zam. 2 154,0 0,0% Santander Bank Polska - KNF ustalił parametr ST na poziomie 1,24 p.p. mWIG40 otw. 3 857,9 0,0% Asseco Poland - W ramach zaproszenia do sprzedaży złożono oferty na 18,18 mln akcji mWIG40 zam. 3 884,5 0,0% Energa, Enea - Energa pożyczy Elektrowni Ostrołęka maksymalnie 340 mln zł Największe wzrosty kurs zmiana Pozostałe informacje: 11 bit studios 396,00 0,0% AB 24,90 0,0% Sektor energetyczny - Nord Stream 2 ukończony w 93% Alior Bank 28,02 0,0% Sektor budowlany - Nakłady inwestycyjne PLK w przyszłym roku wzrosną o 30% r/r Alumetal 39,10 0,0% AmRest 43,95 0,0% Nadchodzące wydarzenia: Największe spadki kurs zmiana Novaturas – NWZ (27 grudnia) 11 bit studios 396,00 0,0% Livechat - Ostatni dzień z prawem do dywidendy (27 grudnia) AB 24,90 0,0% Alior Bank 28,02 0,0% Livechat - Ex-div (30 grudnia) Alumetal 39,10 0,0% Giełda w Pradze - Dzień bez sesji (31 grudnia) AmRest 43,95 0,0% Giełda w Wiedniu - Dzień bez sesji (31 grudnia) Giełda w Warszawie - Dzień bez sesji (31 grudnia) Najwyższe obroty kurs obrót CD Projekt 280,00 79 Nornickel 30,52 55 Erste Group 34,11 41 Pekao 101,25 36 OMV 50,50 33 Indeksy zagraniczne zmiana BUX 45 984,5 0,0% RTS 1 534,9 -0,6% PX50 1 114,7 0,0% DJIA 28 621,4 0,4% NASDAQ 9 022,4 0,8% S&P 500 3 239,9 0,5% DAX XETRA 13 301,0 0,0% FTSE 7 632,2 0,0% CAC 40 6 029,6 0,0% NIKKEI 23 924,9 0,6% HANG SENG 27 864,2 0,0% Waluty i surowce zmiana WIBOR 3m (%) 98,35 0,0% EUR/PLN 4,261 0,2% USD/PLN 3,840 0,1% EUR/USD 1,110 0,2% miedź (USD/t) 6 184,5 0,0% miedź (PLN/t) 23 745,4 0,1% ropa Brent (USD/bbl) 67,92 1,1% Document downloaded by [email protected] Dziennik 27 grudnia 2019 r. -

Santander Bank Polska SA

The official magazine of the American Chamber of Commerce in Poland 3/2020 VOL III, No. 3 • ISSN 2545-322X COMPANY PROFILE: Santander Bank Polska S.A. AMCHAM.PL QUARTERLY IS A VOICE FOR FOREIGN INVESTORS AND THE AMERICAN BUSINESS COMMUNITY IN POLAND. IT STRIVES TO KEEP READERS UP TO DATE WITH AMCHAM NEWS AS WELL AS LEADING TRENDS IN BUSINESS AND POLICY. THE MAGAZINE ALSO PROMOTES AMCHAM MEMBER COMPANIES. IN THIS DISPATCH WE PRESENT AN INTERVIEW WITH MAGDALENA KUSA, INTERNATIONAL BUSINESS MANAGER AT SANTANDER BANK POLSKA S.A ., A NEW MEMBER COMPANY, WHO TALKS ABOUT BANK'S BUSINESS GOALS AND AMBITIONS. AMCHAM.PL QUARTERLY Vol. III, No. 3 Company Profile Santander Bank Polska S.A. STRIVING FOR PERFECTION What is driving the development of flexibility, and conducting business re - the banking and financial services sponsibly while caring for others. sector in Poland? Being a large financial institution, we In addition to technological progress, have always been prepared to re - the process of continuous changes in spond to the changing needs of cus - our industry is also driven by customer tomers and the world. This is an expectations and developments in the integral part of our approach to doing AmCham.pl Quarterly business. It is one of the reasons the Editor Tom Ćwiok talks mechanisms devel - oped so far, also with Magdalena Kusa, within the Santander Group structure, and International Business allows us to share our resources with Manager at Santander others. During these unexpected changes Bank Polska S.A. , about and transformations, how the bank positions leaders must strive to balance short- and itself on the Polish market. -

Poland Is Promoted to Developed Market Status by Ftse Russell

POLAND IS PROMOTED TO DEVELOPED MARKET STATUS BY FTSE RUSSELL As of 24 September 2018, Poland is classified as a Key issues Developed market by FTSE Russell. This promotion to the highest possible status in FTSE Russell's classifications is a • About FTSE Russell and FTSE significant achievement and a recognition of continuous Global Equity Index Series enhancements of the capital markets infrastructure and (GEIS) steady economic growth in Poland. Poland is now among the • International context eight largest economies in the European Union (EU) and 25 • For whom is Poland's promotion relevant? largest economies in the world. • Status of some Polish blue chips • Further implications ABOUT FTSE RUSSELL AND FTSE GLOBAL EQUITY INDEX SERIES (GEIS) FTSE Russell, a subsidiary of the London Stock Exchange Group, is a provider of stock market indices and associated data services, one of the largest in the world. FTSE Global Equity Index Series (GEIS) is a benchmark measuring the performance of global equity markets. According to FTSE Russell, FTSE GEIS looks at around 7,400 large-, mid- and small-cap stocks across 47 countries, with a total net market capitalization of USD 52 trillion, covering approximately 98 percent of the world’s investable market. FTSE Russell classifies markets using four categories: Developed, Advanced Emerging, Secondary Emerging and Frontier. Developed market status means that apart from market quality and size criteria being met, the country is considered as having high gross national income with developed market infrastructures. When determining a country's status, FTSE Russell measures, amongst other things, the market quality (regulatory framework, transactional landscape, derivatives market, etc.), adequateness of the market size, consistency and predictability, stability and market access (ease of investment and disinvestment).