3Q20 Baron Emerging Markets Fund Letter

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Morgan Stanley's Top-Performing Fund Buys Undervalued Stocks

January 19, 2020 | bloomberg.com Photographer: Michael Nagle/Bloomberg Markets Morgan Stanley’s Top-Performing Fund Buys Undervalued Stocks by Ishika Mookerjee January 19, 2020 ▶ Consumer stocks are a focus; more than half of assets in China ▶ Meituan, Moutai among drivers of fund’s 44% gain in past year A top-performing Morgan Stanley fund remain a key focus this year despite its invested capital and 15% revenue growth is betting on cash-rich consumption- slower growth in 2019. over the past three years, he added. The focused stocks in Asia, especially China, to Asian consumer stocks provide “high MSCI Asia ex Japan Index has gained 3.4% manage risks in market cycles this year. returns on capital, low leverage and so far this year. The Wall Street firm’s Asia Opportunity quality growth prospects,” Hong Kong- With more than 800 million people Portfolio, which focuses on equities in based Heugh said. The region offers “the emerging from poverty since market the region excluding Japan, returned 44% highest ratio” of high-quality companies reforms began in 1978, China is an in the past year, beating 99% of its peers, that have generated both 15% return on especially attractive hunting ground for according to data compiled by Bloomberg. The portfolio focuses on undervalued companies with low debt or net cash on their balance sheets, many of which are found in consumer sectors, said Kristian Heugh, who has been co-managing the fund since its inception in 2016. “We seek to protect investors’ capital by focusing on high quality companies with sustainable competitive advantages and purchasing them at a discount to our estimate of intrinsic value,” Heugh said. -

Hang Seng Indexes Announces Index Review Results

14 August 2020 Hang Seng Indexes Announces Index Review Results Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 30 June 2020. All changes will take effect on 7 September 2020 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents remains unchanged at 50. Inclusion: Code Company 1810 Xiaomi Corporation - W 2269 WuXi Biologics (Cayman) Inc. 9988 Alibaba Group Holding Ltd. - SW Removal: Code Company 83 Sino Land Co. Ltd. 151 Want Want China Holdings Ltd. 1088 China Shenhua Energy Co. Ltd. - H Shares The list of constituents is provided in Appendix 1. The Hang Seng Index Advisory Committee today reviewed the fast expanding innovation and new economy sectors in the Hong Kong capital market and agreed with the proposal from Hang Seng Indexes to conduct a comprehensive study on the composition of the Hang Seng Index. This holistic review will encompass various aspects including, but not limited to, composition and selection of constituents, number of constituents, weightings, and industry and geographical representation, etc. The underlying aim of the study is to ensure the Hang Seng Index continues to serve as the most representative and important benchmark of the Hong Kong stock market. Hang Seng Indexes will report its findings and propose recommendations to the Advisory Committee within six months. The number of constituents of the Hang Seng Index may increase during this period. Hang Seng Indexes Announces Index Review Results /2 2. -

Xiaomi Sews up Deals for Smart Homes

16 BUSINESS Thursday, November 29, 2018 CHINA DAILY HONG KONG EDITION Xiaomi sews Shenzhen firms hike investment up deals for in R&D sector By ZHOU MO in Shenzhen, Guangdong smart homes [email protected] 20 percent of Shenzhenregistered list Tech tieups with Ikea, Microsoft and Nearly 20 percent of ed companies devoted more Shenzhenregistered listed than 10 percent of their iKongjian ‘to create better life for people’ companies devoted more operating revenue to R&D than 10 percent of their oper By OUYANG SHIJIA shortly after Ikea, the world’s ating revenue to research ouyangshijia@ largest furniture retailer, said and development last year, a chinadaily.com.cn last week that it would acceler level on par with globally ate its transformation to fully leading hightech enterpris the sector that took the lead. Chinese technology giant embrace new technologies and es like Google and Apple, Of the 10 listed companies Xiaomi Corp announced on offer better user experiences. according to a report. with the biggest R&D invest Wednesday it has teamed up Bjorn Block, business leader In all, 256 companies cov ment, eight were IT compa with Sweden’s furniture titan for Ikea’s Home Smart divi Lei Jun, founder and CEO of Xiaomi Corp, delivers a speech on Wednesday during the MIDC Xiaomi ered in the Shenzhenregis nies. Ikea to offer smart home prod sion, told during the confer AIoT Developer Conference in Beijing. PROVIDED TO CHINA DAILY tered Listed Companies The R&D investment of ucts. ence that the new partnership Development Report dis Tencent Holdings Ltd, the The tieup is part of its larg marked a key step in creating a closed their R&D spending world’s largest game maker er efforts to expand into the seamless experience for cus partnership would benefit home renovation service plat in their 2017 annual reports. -

Greater China 2019

IR Magazine Awards – Greater China 2019 Winners and nominees AWARDS BY RESEARCH Best overall investor relations (large cap) ANTA Sports Products China Resources Beer WINNER China Telecom China Unicom Shenzhou International Group Holdings Best overall investor relations (small to mid-cap) Alibaba Pictures Group Far East Consortium International WINNER Health and Happiness H&H International Holdings Li-Ning NetDragon Websoft Holdings Best investor relations officer (large cap) ANTA Sports Products Suki Wong Cathay Financial Holdings Yajou Chang & Sophia Cheng China Resources Beer Vincent Tse WINNER China Telecom Lisa Lai China Unicom Jacky Yung Best investor relations officer (small to mid-cap) Agile Group Holdings Samson Chan BizLink Holding Tom Huang Far East Consortium International Venus Zhao WINNER Li-Ning Rebecca Zhang Yue Yuen Industrial (Holdings) Olivia Wang Best IR by a senior management team Maggie Wu, CFO & Daniel Zhang, Alibaba Group CEO Tomakin Lai Po-sing, CFO & China Resources Beer Xiaohai Hou, CEO Xiaochu Wang, CEO & Zhu WINNER China Unicom Kebing, CFO Wai Hung Boswell Cheung, CFO & Far East Consortium International David Chiu, Chairman & CEO Ma Jianrong, CEO & Cun Bo Wang, Shenzhou International Group Holdings CFO AWARDS BY REGION Best in region: China Alibaba Pictures Group ANTA Sports Products China Resources Beer WINNER China Telecom China Unicom Shenzhou International Group Holdings Best in region: Hong Kong AIA Group Far East Consortium International WINNER Health and Happiness H&H International Holdings Yue Yuen -

2016 Annual Report (PDF)

Table of Contents 2 Corporate Information 3 CEO’s Statement 6 Management Discussion and Analysis 23 Biographies of Directors and Senior Management 27 Corporate Governance Report 39 Report of the Directors 59 Independent Auditor’s Report 64 Consolidated Statement of Profit or Loss and Other Comprehensive Income 65 Consolidated Statement of Financial Position 67 Consolidated Statement of Changes in Equity 68 Consolidated Statement of Cash Flows 70 Notes to the Consolidated Financial Statements 166 Five-year Financial Summary Corporate Information BOARD OF DIRECTORS REGISTERED OFFICE Executive Directors Maples Corporate Services Limited PO Box 309 Ms. GAO Lina (Deputy Chairman and Chief Executive Officer) Ugland House Mr. HAN Chunlin (Chief Operation Officer) Grand Cayman, KY1-1104, Cayman Islands Non-Executive Directors HONG KONG OFFICE Mr. YU Xubo (Chairman) Unit 2402, 24/F, Mr. WOLHARDT Julian Juul Alliance Building 130-136 Mr. HUI Chi Kin, Max Connaught Road Central Sheung Wan Mr. ZHANG Ping Hong Kong Mr. SUN Yugang PRINCIPAL SHARE REGISTRAR AND Independent Non-Executive Directors TRANSFER OFFICE Mr. LI Shengli Maples Finance Limited Mr. LEE Kong Wai, Conway PO Box 1093, Mr. KANG Yan Queensgate House Mr. ZOU Fei Grand Cayman, KY1-1102 Cayman Islands AUDIT COMMITTEE HONG KONG BRANCH SHARE REGISTRAR Mr. LEE Kong Wai, Conway (Chairman) AND TRANSFER OFFICE Mr. HUI Chi Kin, Max Mr. ZOU Fei Computershare Hong Kong Investor Services Limited Rooms 1712-1716, 17/F, Hopewell Centre REMUNERATION COMMITTEE 183 Queen’s Road East Wanchai Hong Kong Mr. LI Shengli (Chairman) Mr. WOLHARDT Julian Juul LEGAL ADVISORS Mr. ZOU Fei NOMINATION COMMITTEE As to Hong Kong Law Mr. -

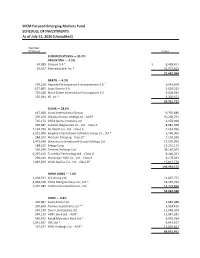

WCM Focused Emerging Markets Fund SCHEDULE of INVESTMENTS As of July 31, 2020 (Unaudited)

WCM Focused Emerging Markets Fund SCHEDULE OF INVESTMENTS As of July 31, 2020 (Unaudited) Number of Shares Value COMMON STOCKS — 91.0% ARGENTINA — 4.5% 49,089 Globant S.A.* $ 8,489,451 20,427 MercadoLibre, Inc.* 22,972,613 31,462,064 BRAZIL — 4.3% 724,230 Hapvida Participacoes e Investimentos S.A.1 9,043,504 637,865 Lojas Renner S.A. 5,029,212 735,180 Notre Dame Intermedica Participacoes S.A. 9,408,545 135,494 XP, Inc.* 6,300,471 29,781,732 CHINA — 28.6% 467,060 Airtac International Group 9,797,686 200,258 Alibaba Group Holding Ltd. - ADR* 50,268,763 735,174 ANTA Sports Products Ltd. 6,978,998 346,687 Autobio Diagnostics Co., Ltd. - Class A 8,082,568 2,134,296 By-health Co., Ltd. - Class A 7,654,996 3,532,000 Kingdee International Software Group Co., Ltd.* 9,768,906 288,105 Meituan Dianping - Class B* 7,129,590 1,473,420 Shenzhou International Group Holdings Ltd. 17,599,596 188,215 Silergy Corp. 11,291,122 556,290 Tencent Holdings Ltd. 38,160,505 4,297,415 TravelSky Technology Ltd. - Class H 8,266,021 294,444 Wuliangye Yibin Co., Ltd. - Class A 9,178,043 1,049,069 WuXi AppTec Co., Ltd. - Class H1 15,817,778 199,994,572 HONG KONG — 7.8% 2,418,531 AIA Group Ltd. 21,807,752 3,869,330 China Mengniu Dairy Co., Ltd.* 18,156,740 1,407,385 Techtronic Industries Co., Ltd. 14,719,896 54,684,388 INDIA — 9.8% 204,687 Asian Paints Ltd. -

Wilmington Funds Holdings Template DRAFT

Wilmington International Fund as of 5/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS TAIWAN SEMICONDUCTOR MANUFACTURING CO LTD 2.82% ISHARES MSCI CANADA ETF 2.43% SAMSUNG ELECTRONICS CO LTD 1.97% TENCENT HOLDINGS LTD 1.82% DREYFUS GOVT CASH MGMT-I 1.76% MSCI INDIA FUTURE JUN21 1.68% AIA GROUP LTD 1.05% HDFC BANK LTD 1.05% ASML HOLDING NV 1.03% ISHARES MSCI EUROPE FINANCIALS ETF 1.02% USD/EUR SPOT 20210601 BNYM 1.00% ALIBABA GROUP HOLDING LTD 0.95% DSV PANALPINA A/S 0.90% TECHTRONIC INDUSTRIES CO LTD 0.88% JAMES HARDIE INDUSTRIES PLC 0.83% INFINEON TECHNOLOGIES AG 0.73% BHP GROUP LTD 0.67% SIKA AG 0.64% MEDIATEK INC 0.60% NOVO NORDISK A/S 0.56% OVERSEA-CHINESE BANKING CORP LTD 0.55% CSL LTD 0.55% LVMH MOET HENNESSY LOUIS VUITTON SE 0.54% RIO TINTO LTD 0.53% DREYFUS GOVT CASH MGMT-I 0.53% MIDEA GROUP CO LTD 0.53% TOYOTA MOTOR CORP 0.52% PARTNERS GROUP HOLDING AG 0.52% SAP SE 0.51% ADIDAS AG 0.49% NAVER CORP 0.49% HITACHI LTD 0.49% MERIDA INDUSTRY CO LTD 0.47% ZALANDO SE 0.47% SK MATERIALS CO LTD 0.47% CHINA PACIFIC INSURANCE GROUP CO LTD 0.45% HEXAGON AB 0.45% LVMH MOET HENNESSY LOUIS VUITTON SE 0.44% JD.COM INC 0.44% TOMRA SYSTEMS ASA 0.44% DREYFUS GOVT CASH MGMT-I 0.44% SONY GROUP CORP 0.43% L'OREAL SA 0.43% EDENRED 0.43% AUSTRALIA & NEW ZEALAND BANKING GROUP LTD 0.43% NEW ORIENTAL EDUCATION & TECHNOLOGY GROUP INC 0.42% HUAZHU GROUP LTD 0.41% CRODA INTERNATIONAL PLC 0.40% ATLAS COPCO AB 0.40% ASSA ABLOY AB 0.40% IMCD NV 0.40% HUTCHMED CHINA LTD 0.40% JARDINE MATHESON HOLDINGS LTD 0.40% HONG KONG EXCHANGES -

Annual Report Contents

2017 ANNUAL REPORT CONTENTS Corporate Information 2 Results Highlights 4 Chairman’s Statement 6 Biographies of Directors and Senior Management 8 Business Review 16 Financial Review 26 Corporate Governance Report 35 Directors’ Report 46 Independent Auditor’s Report 58 Consolidated Statement of Profit or Loss and 63 Other Comprehensive Income Consolidated Statement of Financial Position 65 Consolidated Statement of Changes in Equity 67 Consolidated Statement of Cash Flows 69 Notes to the Consolidated Financial Statements 71 Five year Summary 162 Glossary 164 CORPORATE INFORMATION Legal Name of the Company Company Secretary WH Group Limited Mr. CHAU Ho Place of Listing and Stock Code Audit Committee The shares of the Company were listed on the Main Board Mr. LEE Conway Kong Wai (Chairman) of the Stock Exchange on August 5, 2014 Mr. HUANG Ming Mr. LAU, Jin Tin Don Stock Code: 288 Remuneration Committee Company Website Mr. HUANG Ming (Chairman) www.wh-group.com Mr. LEE Conway Kong Wai Mr. JIAO Shuge Directors Executive Directors Nomination Committee Mr. WAN Long (Chairman and Chief Executive Officer) Mr. WAN Long (Chairman) Mr. GUO Lijun (Executive Vice President and Chief Mr. HUANG Ming Financial Officer) Mr. LAU, Jin Tin Don Mr. ZHANG Taixi (General Manager of Shuanghui Group) Mr. SULLIVAN Kenneth Marc (President and Chief Environmental, Social and Executive Officer of Smithfield) Governance Committee Mr. YOU Mu (Vice President of Shuanghui Development) Mr. GUO Lijun (Chairman) Mr. SULLIVAN Kenneth Marc Non-executive Director Mr. ZHANG Taixi Mr. JIAO Shuge (Deputy Chairman) Mr. LAU, Jin Tin Don Independent Non-executive Directors Food Safety Committee Mr. -

Annual Report – October 31 2018

THE CHINA FUND, INC. ANNUAL REPORT October 31, 2018 The China Fund, Inc. Table of Contents Page Key Highlights 1 Asset Allocation 2 Industry Allocation 3 Chairman’s Statement 4 Investment Manager’s Statement 7 About the Portfolio Manager 9 Schedule of Investments 10 Financial Statements 14 Notes to Financial Statements 18 Report of Independent Registered Public Accounting Firm 26 Other Information 27 Dividends and Distributions: Summary of Dividend Reinvestment and Cash Purchase Plan 29 Directors and Officers 33 THE CHINA FUND, INC. KEY HIGHLIGHTS (unaudited) FUND DATA NYSE Stock Symbol CHN Listing Date July 10, 1992 Shares Outstanding 15,722,675 Total Net Assets (10/31/18) $298,469,072 Net Asset Value Per Share (10/31/18) $18.98 Market Price Per Share (10/31/18) $16.98 TOTAL RETURN(1) Performance as of 10/31/18: Net Asset Value Market Price 1-Year Cumulative -16.55% -17.53% 3-Year Cumulative 10.26% 12.29% 3-Year Annualized 3.31% 3.94% 5-Year Cumulative 18.71% 20.78% 5-Year Annualized 3.49% 3.85% 10-Year Cumulative 176.01% 169.92% 10-Year Annualized 10.69% 10.44% DIVIDEND HISTORY Record Date Income Capital Gains 12/19/17 $0.5493 — 12/19/16 $0.4678 — 12/28/15 $ 0.2133 $ 1.2825 12/22/14 $ 0.2982 $ 3.4669 12/23/13 $ 0.4387 $ 2.8753 12/24/12 $ 0.3473 $ 2.9044 12/23/11 $ 0.1742 $ 2.8222 12/24/10 $ 0.3746 $ 1.8996 12/24/09 $ 0.2557 — 12/24/08 $ 0.4813 $ 5.3361 (1) Total investment returns reflect changes in net asset value or market price, as the case may be, during each period and assumes that dividends and capital gains distributions, if any, were reinvested in accordance with the dividend reinvestment plan. -

Buy WH Group

Deutsche Bank Markets Research Rating Company Date 27 February 2018 Buy WH Group Coverage Change Asia Hong Kong Reuters Bloomberg Exchange Ticker Price at 26 Feb 2018 (HKD) 9.65 Consumer 0288.HK 288 HK HSI 0288 Price target - 12mth (HKD) 11.50 Food & Beverage ADR Ticker ISIN 52-week range (HKD) 9.74 - 5.94 WHGLY US92890T2050 HANG SENG INDEX 31,499 Time to add more protein; resuming Mark Yuan Anne Ling coverage with Buy Research Analyst Research Analyst (+852 ) 2203 6181 (+852 ) 2203 6177 Well-positioned in pork price cycle; global trade profit to expand; Buy [email protected] [email protected] We like WH Group for three reasons. First, we expect both US and China’s segment margin to expand, backed by a lower hog price in 2018; second, we expect the global trading profit to improve in the long term, helped by Price/price relative increasing synergies within different subsidiaries; and third, product mix upgrade in China should drive sustainable sales growth. We believe the risk- Performance (%) 1m 3m 12m reward for the stock is attractive at 13.9x 2018E P/E vs. 11.4% earnings CAGR Absolute 4.0 19.1 59.2 in 2018-20. We resume coverage on the stock with a Buy. HANG SENG INDEX -5.0 5.5 31.4 Declining hog price to drive margin expansion in near-term Source: Deutsche Bank In 2018, we expect the pork price to continue to decline, by 10% in China, as the current hog-raising profit is still much higher than the historical average and should lead to increasing supply. -

Issue 1211 – Octoberjanuary 20172018 [email protected]

CorporateCorporate NewsletterNewsletter HKEX Stock Code:288 IssueIssue 1211 – OctoberJanuary 20172018 [email protected] WH Group WH Group’s Smithfield Establishes Strategic Partnership with JD.com (24th October 2017) WH Group’s Smithfield Foods has jointly launched a Tripartite Strategic Partnership Agreement with JD.com and Shuanghui Development in New York. According to the agreement, JD Fresh will become the online sales platform for Smithfield’s pork products in China. The parties will sell more than ten kinds of exclusive products on JD.com, and further cooperate on big data, cold chain logistics and foods traceability. WH Group Announces Q3 2017 Results (30th October 2017) WH Group announced the unaudited consolidated results for the nine months ended September 30, 2017. In the period, turnover increased by 3.2% to US$16,285 million. Operating profit increased by 7.6% to US$1,379 million. Net profit increased by 11.1% to US$823 million (disregard any biological fair value adjustments and the non-recurrent debt extinguishment costs and related tax during the Period for the refinancing of certain existing indebtedness). WH Group Hosts Investors, Analysts and Media Tour (20th- 24th November 2017) More than 60 investors and analysts from Morgan Stanley, Citigroup and CICC and so on, 20 Chinese and foreign reporters from Reuters, the Hong Kong Economic Times and the South China Morning Post as well as Chinese mainstream financial media participated in two separate two- day tours. The investors, analysts and reporters visited the industrial park in Luohe, Henan Province, where the headquarters of Shuanghui Development is located, and Zhengzhou Production Plant. -

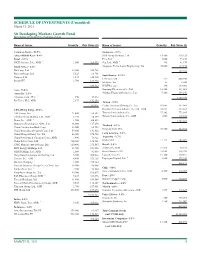

This Is the Message

SCHEDULE OF INVESTMENTS (Unaudited) March 31, 2021 Sit Developing Markets Growth Fund Investments are grouped by geographic region. Name of Issuer Quantity Fair Value ($) Name of Issuer Quantity Fair Value ($) Common Stocks - 93.9% Singapore - 4.2% Africa/Middle East - 8.4% DBS Group Holdings, Ltd. 14,500 310,329 Israel - 2.3% Flex, Ltd. * 4,000 73,240 NICE Systems, Ltd., ADR * 1,500 326,955 Sea, Ltd., ADR * 365 81,479 South Africa - 6.1% Singapore Technologies Engineering, Ltd. 44,000 127,238 * Bid Corp., Ltd. 13,200 255,781 592,286 Bidvest Group, Ltd. 5,525 63,781 South Korea - 12.0% Naspers, Ltd. 1,425 340,968 LG Chem, Ltd. 575 408,990 Prosus NV 1,700 188,992 Medytox, Inc. 15 2,500 849,522 NAVER Corp. 450 149,901 Asia - 73.4% Samsung Electronics Co., Ltd. 12,250 881,069 Australia - 2.1% Shinhan Financial Group Co., Ltd. 7,200 238,250 * Atlassian Corp., PLC 450 94,842 1,680,710 Rio Tinto, PLC, ADR 2,475 192,184 Taiwan - 9.0% 287,026 Cathay Financial Holding Co., Ltd. 82,085 137,945 China/Hong Kong - 40.6% Hon Hai Precision Industry Co., Ltd., GDR 26,835 235,611 AIA Group, Ltd. 21,400 259,582 Taiwan Semiconductor Co. 37,482 771,105 Alibaba Group Holding, Ltd., ADR * 3,150 714,199 Taiwan Semiconductor Co., ADR 1,000 118,280 * Baidu, Inc., ADR 1,700 369,835 1,262,941 Budweiser Brewing Co. APAC, Ltd. 46,000 137,276 Thailand - 1.1% China Construction Bank Corp.