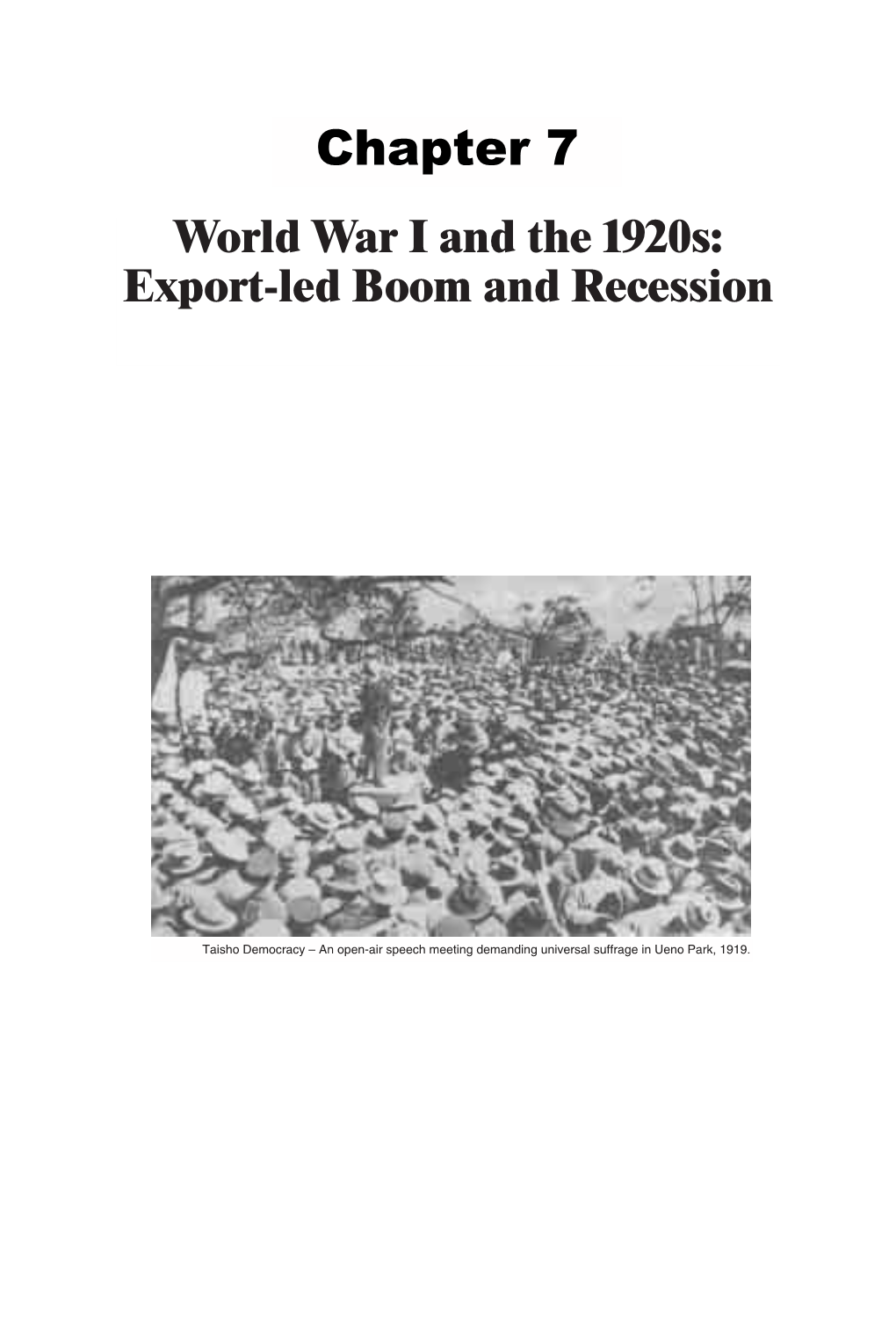

World War I and the 1920S: Export-Led Boom and Recession

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Institutions, Competition, and Capital Market Integration in Japan

NBER WORKING PAPER SERIES INSTITUTIONS, COMPETITION, AND CAPITAL MARKET INTEGRATION IN JAPAN Kris J. Mitchener Mari Ohnuki Working Paper 14090 http://www.nber.org/papers/w14090 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 June 2008 A version of this paper is forthcoming in the Journal of Economic History. We gratefully acknowledge the assistance of Ronald Choi, Jennifer Combs, Noriko Furuya, Keiko Suzuki, and Genna Tan for help in assembling the data. Mitchener would also like to thank the Institute for Monetary and Economic Studies at the Bank of Japan for its hospitality and generous research support while serving as a visiting scholar at the Institute in 2006, and the Dean Witter Foundation for additional financial support. We also thank conference participants at the BETA Workshop in Strasbourg, France and seminar participants at the Bank of Japan for comments and suggestions. The views presented in this paper are solely those of the authors, and do not necessarily represent those of the Bank of Japan, its staff, or the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2008 by Kris J. Mitchener and Mari Ohnuki. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Institutions, Competition, and Capital Market Integration in Japan Kris J. Mitchener and Mari Ohnuki NBER Working Paper No. -

Hirohito the Showa Emperor in War and Peace. Ikuhiko Hata.Pdf

00 Prelims H:Master Testpages Enigma 6/6/07 15:00 Page i HIROHITO: THE SHO¯ WA EMPEROR IN WAR AND PEACE 00 Prelims H:Master Testpages Enigma 6/6/07 15:00 Page ii General MacArthur and Emperor Hirohito photographed in the US Embassy, Tokyo, shortly after the start of the Occupation in September 1945. (See page 187) 00 Prelims H:Master Testpages Enigma 6/6/07 15:00 Page iii Hirohito: The Sho¯wa Emperor in War and Peace Ikuhiko Hata NIHON UNIVERSITY Edited by Marius B. Jansen GLOBAL ORIENTAL 00 Prelims H:Master Testpages Enigma 6/6/07 15:00 Page iv HIROHITO: THE SHO¯ WA EMPEROR IN WAR AND PEACE by Ikuhiko Hata Edited by Marius B. Jansen First published in 2007 by GLOBAL ORIENTAL LTD P.O. Box 219 Folkestone Kent CT20 2WP UK www.globaloriental.co.uk © Ikuhiko Hata, 2007 ISBN 978-1-905246-35-9 All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying and recording, or in any information storage or retrieval system, without prior permission in writing from the Publishers. British Library Cataloguing in Publication Data A CIP catalogue entry for this book is available from the British Library Set in Garamond 11 on 12.5 pt by Mark Heslington, Scarborough, North Yorkshire Printed and bound in England by Athenaeum Press, Gateshead, Tyne & Wear 00 Prelims H:Master Testpages Enigma 6/6/07 15:00 Page vi 00 Prelims H:Master Testpages Enigma 6/6/07 15:00 Page v Contents The Author and the Book vii Editor’s Preface -

The American Economist Martin Bronfenbrenner (1914-1997) and the Reconstruction of the Japanese Economy (1947-1952): (A Version for Presentation in East Asia)

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Ikeo, Aiko Working Paper The American economist Martin Bronfenbrenner (1914-1997) and the reconstruction of the Japanese economy (1947-1952): (a version for presentation in East Asia) CHOPE Working Paper, No. 2011-11 Provided in Cooperation with: Center for the History of Political Economy at Duke University Suggested Citation: Ikeo, Aiko (2011) : The American economist Martin Bronfenbrenner (1914-1997) and the reconstruction of the Japanese economy (1947-1952): (a version for presentation in East Asia), CHOPE Working Paper, No. 2011-11, Duke University, Center for the History of Political Economy (CHOPE), Durham, NC This Version is available at: http://hdl.handle.net/10419/155446 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

OFFICIAL GAZETTE ENGLISH EDITION Governmentprimssuheau

OFFICIAL GAZETTE ENGLISH EDITION governmentprimssuheau No. 69 TUESDAY, JUNE 25, 1946 IMPERIAL ORDINANCE Imperial Ordinance No. 341 I hereby give My Sanction to the Temporary A part of the Ordinance of the appointment of Establishment of the Bureau of Allowances in the the temporary personnel in th Ministry of Finance Ministry of Finance and cause the same to be shall be revised as follows: promulgated. In Article 1, regarding the number of secre- Signed: HIROHITO, Seal of the Emperor taries of the Ministry of Finance, " 3 full time " This twenty-fourth day of the sixth month of shall read "4 full-time"; " 77full-time" "85 the twenty-firstyearof Showa (June 24, 1946) full-time "; and " 230 full-time " " 258 full-time "; Countersigned: Prime Minister and in the same Article regarding the number of technical officialsof the Ministry of Finance, " 7 YOSHIDA Shigeru full-time " shall read " 9 full-time "; and " 2 full- Minister of Finance time " '4 full-time." ISHIBASHI Tanzan Supplementary Provision: Imperial Ordinance The present Ordinance shall come into force No. 340 as from the day of its promulgation. TEMPORARY ESTABLISHMENT OF THE BUREAU OF ALLOWANCES OF THEMINISTRY OF FINANCE MINISTERIAL ORDINANCE The Bureau of Allowances shallbe temporarily Ministry of Finance Ordinance establishedin the Ministry of Finance and shallbe No. 75 charged with the affairsregarding allowances in June 25, 1946 general, of government officials,those treated as The following amendment shallbe made in the such, " shokutakuin," " koin," "yonin," "k5in" Ministry of Finance Ordinance No. 118 of Dec. \ and others who receive allowances from the Trea- 1942: sury. Minister of Finance Supplementary Provision: Tanzan Ishibashi The present Ordinance shall come into force asfrom the day ofitspromulgation. -

The Identity Dilemma and the Road to the Pacific War by Daisuke Minami

Identity Clash: The Identity Dilemma and the Road to the Pacific War by Daisuke Minami B.A. in Political Science, May 2013, Macalester College A Dissertation submitted to The Faculty of The Columbian College of Arts and Sciences of The George Washington University in partial fulfilment of the requirements for the degree of Doctor of Philosophy May 19, 2019 Dissertation directed by Eric Grynaviski Associate Professor of Political Science and International Affairs The Columbian College of Arts and Sciences of The George Washington University certifies that Daisuke Minami has passed the Final Examination for the degree of Doctor of Philosophy as of April 8, 2019. This is the final and approved form of the dissertation. Identity Clash: The Identity Dilemma and the Road to the Pacific War Daisuke Minami Dissertation Research Committee: Eric Grynaviski, Associate Professor of Poiltical Science and International Affaris, Dissertation Director Mike M. Mochizuki, Associate Professor of Political Science and International Affairs, Committee Member Michael N. Barnett, University Professor of Political Science and International Affairs, Committee Member Charles L. Glaser, Professor of Political Science and International Affairs, Committee Member ii © Copyright 2019 by Daisuke Minami All rights reserved iii Acknowledgements This dissertation would have not been possible without the help of numerous people. I owe tremendous gratitude to those who have supported me. I first would like to thank the members of my dissertation committee: Eric Grynaviski, Mike Mochizuki, Michael Barnett, and Charlie Glaser. Eric Grynaviski has been crucial at every stage of my doctoral program. As a first-year faculty mentor, he helped me weather through the first two years of the coursework and develop my research agenda. -

Who Should Govern: the Political Reformation After the First World

Kobe University Repository : Kernel タイトル Who Should Govern: The Political Reformation after the First World Title War in Japan 著者 Murai, Ryouta Author(s) 掲載誌・巻号・ページ Kobe University law review,36:19-43 Citation 刊行日 2002 Issue date 資源タイプ Departmental Bulletin Paper / 紀要論文 Resource Type 版区分 publisher Resource Version 権利 Rights DOI JaLCDOI 10.24546/00387151 URL http://www.lib.kobe-u.ac.jp/handle_kernel/00387151 PDF issue: 2021-10-02 19 Who Should Govern: The Political Reformation after the First World War in Japan1 Ryota Murai2 In modern Japan, the Meiji Constitution created a bicameral Imperial Diet, which included a House of Representatives with members chosen by direct election. However, this was not what made the party cabinet system a necessity. Rather, it was because the Meiji Constitutional system was a multiple union of many organs, such as the Privy Council and the House of Peers. The House of Representatives was also one of them. The selection of the prime minister was not based on the intentions of the House of Representatives, but rather on the elder statesmen (genro)’s consensus directed by protocol. Nevertheless, under the slogans like “Protecting the Constitutional Government (Kensei-Yogo)” or “The Normal way of the Constitutional Government (Kensei-Jodo),” the situation slowly changed. The politics that made the House of Representatives and political parties an axis became the undercurrent that was hard to suppress. During the final stages of the First World War, Takashi Hara, the leader of the Seiyukai, the majority party of the House of Representatives, formed his own cabinet; and over a span of eight years, from 1924 to 1932, this was the time when the party leader possessed political power. -

Luíza Uehara De Araújo.Pdf

Pontifícia Universidade Católica de São Paulo Programa de Estudos Pós-Graduados em Ciências Sociais Luíza Uehara de Araújo um anarquismo menor: práticas libertárias no Japão Imperial Doutorado em Ciências Sociais São Paulo Abril de 2019 Luíza Uehara de Araújo um anarquismo menor: práticas libertárias no Japão Imperial Doutorado em Ciências Sociais Tese apresentada à Banca Examinadora da Pontifícia Universidade Católica de São Paulo, como exigência parcial para obtenção do título de Doutora em Ciências Sociais (Ciência Política) sob a orientação do Prof. Dr. Edson Passetti. Abril de 2019 Banca Examinadora ____________________________________ ____________________________________ ____________________________________ ____________________________________ ____________________________________ O presente trabalho foi realizado com apoio da Coordenação de Aperfeiçoamento de Pessoal de Nível Superior- Brasil (CAPES)- Código de Financiamento 001. This study was financed in part by the Coordenação de Aperfeiçoamento de Pessoal de Nível Superior- Brasil (CAPES)- Finance Code 001. agradecimentos ao edson passetti, coração desperto e existência intensa. pelas inquietações anarquistas no agora. por me acompanhar nas intempéries e nas transformações desse percurso. pela orientação libertária, generosa, paciente e delicada. em minha timidez e em singelas palavras: muito obrigada. à beatriz scigliano carneiro, pela revisão atenta, pelos belos desenhos, e também pelos bichos e biblioteca. à flávia lucchesi, pelas conversas, paciência, força no final e pelo destemor nas partidas de futebol e na vida. à eliane carvalho, doce existência, pelas traduções, leitura e pela saudade. ao acácio augusto, pela força do punk. ao vitor osório, de olhar atento. à lúcia soares, elegante trovão. ao gustavo simões, pelos sons anti-harmonia, pela leitura e problematizações na qualificação. à salete oliveira, pela vitalidade e pelos lindos tons azuis na cerâmica. -

The Japanese Press and Japanese Foreign Policy

THE JAPANESE PRESS AND JAPANESE FOREIGN POLICY 1927-1933 by Tsutomu David Yamamoto for Ph.D. School of Oriental and African Studies ProQuest Number: 11010590 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 11010590 Published by ProQuest LLC(2018). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 Preface Considering the indirect linkage between public opinion, as reflected in the press, and government policy, in particular in the foreign policy sphere where the government is at its most secretive, it is not surprising that very little research into their inter-relationship has been carried out. It is easy to understand, therefore, that this situation applies with regard to pre-War Japan which had a more authoritarian tradition than most Western nations. Even the Japanese press, however, had a role to play in the formation of government policy and its attitude at times did have serious implications for foreign policy and diplomacy. In this sense, the decline of the Japanese press as an Opposition force between 1927 and 1933, which is the subject of this study, is significant. -

The Japanese Conservative Camp's Bridging Method for China–Japan

International Journal of Asian Studies (2021), 1–18 doi:10.1017/S1479591421000449 RESEARCH ARTICLE . The Japanese conservative camp’s bridging method for China–Japan relations under the separation of politics and the economic policy: investigation of the case of the Kenzo Matsumura Group, 1959–1972 Zhai Xin Shanghai Jiao Tong University, Shanghai, China Author for correspondence: Zhai Xin, E-mail: [email protected] https://www.cambridge.org/core/terms (Received 12 June 2021; revised 3 August 2021; accepted 3 August 2021) Abstract From the signing of the Treaty of San Francisco to the resumption of diplomatic relations between China and Japan, Japan has always adopted a political and economic separation policy that maintains diplomacy with Taiwan and economic and cultural relations with China. Within the ruling Liberal Democratic Party, to break the existing deadlock, Kenzo Matsumura of the Japanese House of Representatives and others formed a foreign policy group in 1959. This group spoke highly of China’s importance to Japan’s devel- opment on the grounds of national interests rather than ideology and national sentiments, played a bridg- ing role in the political communication between China and Japan, and created a precedent for the nontraditional improvement of international relations in Japan. Key words: Political and economic separation policy; Sino–Japanese relations; the Kenzo Matsumura Group; The Liberal , subject to the Cambridge Core terms of use, available at Democratic Party’s China Channel; Treaty of San Francisco Genesis of the issue After the establishment of the People’s Republic of China in 1949, consistent with international prin- ciples, such as peaceful coexistence, the Chinese government pursued normalization of the China– 27 Sep 2021 at 17:53:25 Japan relationship. -

Annual Report 2007 Annual Report 2007 Basic Credo of the Asahi Kasei Group

Annual Report 2007 Annual Report 2007 Basic Credo of the Asahi Kasei Group Basic tenets We the Asahi Kasei Group, through constant innovation and advances based in science and the human intellect, will contribute to human life and human livelihood. Guiding precepts We will create new value, thinking and working in unison with the customer, from the perspective of the customer. We will respect the employee as an individual, and value teamwork and worthy endeavor. We will contribute to our shareholders, and to all whom we work with and serve, as an international, high earnings enterprise. We will strive for harmony with the natural environment and ensure the safety of our products, operations, and activities. We will progress in concert with society, and honor the laws and standards of society as a good corporate citizen. Contents The Asahi Kasei History .................................................................................................................. 01 Consolidated Financial Highlights ................................................................................................. 04 To Our Shareholders ....................................................................................................................... 05 Driving the Strategic Advance: Growth Action – 2010 ................................................................... 06 Asahi Kasei Group Operations, Worldwide ................................................................................... 12 At a Glance ..................................................................................................................................... -

Japan-Republic of China Relations Under US Hegemony: a Genealogy of ‘Returning Virtue for Malice’

Japan-Republic of China Relations under US Hegemony: A genealogy of ‘returning virtue for malice’ Joji Kijima Department of Politics and International Studies, School of Oriental and African Studies, University of London Thesis submitted for the degree of Doctor of Philosophy November 2005 ProQuest Number: 10673194 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10673194 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 Abstract Japan-Republic of China relations under US hegemony: A genealogy of ‘returning virtue for malice’ Much of Chiang Kai-shek’s ‘returning virtue for malice’ (yide baoyuan ) postwar Japan policy remains to be examined. This thesis mainly shows how the discourse of ‘returning virtue for malice’ facilitated Japan’s diplomatic recognition of the Republic of China (ROC) on Taiwan during the Cold War era. More conceptually, this study re- conceptualizes foreign policy as discourse—that of moral reciprocity—as it sheds light on the question of recognition as well as the consensual aspect of hegemony. By adopting a genealogical approach, this discourse analysis thus traces the descent and emergence of the ‘returning virtue for malice’ trope while it examines its discursive effect on Tokyo’s recognition of Taipei under American hegemony. -

Burn Before Reading: the Japanese Atomic Bomb Program, the Battles of the Chosin Reservoir, and the Cave at Koto-Ri

Draft Burn before Reading: The Japanese Atomic Bomb Program, the Battles of the Chosin Reservoir, and the Cave at Koto-ri. The Cell. Dwight R. Rider Dwight R. Rider: 14 May 2016 Draft “The higher the headquarters, the more important is calm…nothing is ever as bad as it first seems.” General Joseph Stillwell. "If everybody is thinking alike, then somebody isn't thinking." George S. Patton Jr. “The task of government in this enlightened time does not extend to actually dealing with problems. Solving problems might put bureaucrats out of work. No, the task of government is to make it look as though problems have been solved, while continuing to keep the maximum number of consultants and bureaucrats employed dealing with them.” Bob Emmers Dwight R. Rider: 14 May 2016 Draft Foreword The conflict that became popularly known as “The Korean War” (but was never truly a declared war nor did it end) was one that I experienced only vicariously, as I was a few months underage for the draft or enlistment when it entered the perpetual truce phase. Still, through newspapers and radio, as well as having slightly older friends who went “over there,” I was as immersed as one could be without wearing the uniform. These avenues of input were woven into my novel about a man of a little older than my age who served in WW-2 and Korea, two conflicts that imprinted me deeply. My son was in the Air Force during the end of the Vietnam era, a period that highlighted the end of an era in which the USA actually won wars.