Saving Power

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Next Generation Wind and Solar Power from Cost to Value FULL REPORT Next Generation Wind and Solar Power from Cost to Value INTERNATIONAL ENERGY AGENCY

FULL REPORT Next Generation Wind and Solar Power From cost to value FULL REPORT Next Generation Wind and Solar Power From cost to value INTERNATIONAL ENERGY AGENCY The International Energy Agency (IEA), an autonomous agency, was established in November 1974. Its primary mandate was – and is – two-fold: to promote energy security amongst its member countries through collective response to physical disruptions in oil supply, and provide authoritative research and analysis on ways to ensure reliable, affordable and clean energy for its 29 member countries and beyond. The IEA carries out a comprehensive programme of energy co-operation among its member countries, each of which is obliged to hold oil stocks equivalent to 90 days of its net imports. The Agency’s aims include the following objectives: Secure member countries’ access to reliable and ample supplies of all forms of energy; in particular, through maintaining effective emergency response capabilities in case of oil supply disruptions. Promote sustainable energy policies that spur economic growth and environmental protection in a global context – particularly in terms of reducing greenhouse-gas emissions that contribute to climate change. Improve transparency of international markets through collection and analysis of energy data. Support global collaboration on energy technology to secure future energy supplies and mitigate their environmental impact, including through improved energy efficiency and development and deployment of low-carbon technologies. Find solutions to global -

Development of the Electricity Sector

UCC Library and UCC researchers have made this item openly available. Please let us know how this has helped you. Thanks! Title Analysing evolutionary pathways for the European power system resulting from climate mitigation policy Author(s) Gaffney, Fiac Publication date 2019 Original citation Gaffney, F. 2019. Analysing evolutionary pathways for the European power system resulting from climate mitigation policy. PhD Thesis, University College Cork. Type of publication Doctoral thesis Rights © 2019, Fiac Gaffney. http://creativecommons.org/licenses/by-nc-nd/3.0/ Embargo information Not applicable Item downloaded http://hdl.handle.net/10468/9632 from Downloaded on 2021-10-01T19:36:26Z School of Engineering & MaREI Centre, Environmental Research Institute University College Cork Analysing Evolutionary Pathways for the European Power System resulting from Climate Mitigation Policy Fiac Gaffney B.Eng M.Sc Thesis submitted for the degree of Doctor of Philosophy to the National University of Ireland, Cork July 2019 Supervisors: Professor Brian P. Ó Gallachóir & Dr. Paul Deane Head of Department/School: Professor Liam P. Marnane i Declaration ________________________________________________________ vi Acknowledgements __________________________________________________ vii Executive Summary ________________________________________________ viii Units and Abbreviations______________________________________________ ix List of Figures ____________________________________________________ xiii List of Tables _____________________________________________________ -

The Effect of Wind Generation on Wholesale Electricity Prices in Ireland

The Effect of Wind Generation on Wholesale Electricity Prices in Ireland Kernan, R., Liu, X., McLoone, S., & Fox, B. (2017). The Effect of Wind Generation on Wholesale Electricity Prices in Ireland. Paper presented at 16th Wind Integration Workshop, Berlin, Germany. http://windintegrationworkshop.org/old_proceedings/ Document Version: Peer reviewed version Queen's University Belfast - Research Portal: Link to publication record in Queen's University Belfast Research Portal Publisher rights Copyright 2017 The Authors. This work is made available online in accordance with the publisher’s policies. Please refer to any applicable terms of use of the publisher. General rights Copyright for the publications made accessible via the Queen's University Belfast Research Portal is retained by the author(s) and / or other copyright owners and it is a condition of accessing these publications that users recognise and abide by the legal requirements associated with these rights. Take down policy The Research Portal is Queen's institutional repository that provides access to Queen's research output. Every effort has been made to ensure that content in the Research Portal does not infringe any person's rights, or applicable UK laws. If you discover content in the Research Portal that you believe breaches copyright or violates any law, please contact [email protected]. Download date:01. Oct. 2021 The Effect of Wind Generation on Wholesale Electricity Prices in Ireland Ron´ an´ Kernan Xueqin (Amy) Liu Sean´ McLoone Brendan Fox Queen’s University Belfast Queen’s University Belfast Queen’s University Belfast Queen’s University Belfast Northern Ireland Northern Ireland Northern Ireland Northern Ireland Abstract—The integrated electricity sector on the island of where loads are controlled or encouraged to coincide their Ireland has ambitious plans for 37% penetration of wind power demand with periods of increased wind generation. -

Wind Power in Ireland and USA Workshop Report

NEPP Workshop Workshop report September 2011 Wind power in Ireland and USA The “Joint Workshop NEPP and IEA (Wind Task 25)” was held at KTH, Stockholm on 4 April 2011. The main speakers were three experts from the IEA work group on design and operaƟ on of power systems with large amounts of wind power. The audience was representaƟ ves from the NEPP project and the Swedish industry. The Irish power system is rather small, and with weak interconnecƟ ons to Great Britain. Most of the balancing of wind power in the Irish system must be done in thermal generators. Nevertheless, the Irish system already has a large share of wind power, and the discussion is not Figures for end 2008 whether the system can manage situaƟ ons where wind Source: Global wind energy outlook 2008, EirGrid, UK National Grid, NORDEL, Euroelectric power account for up to 50% of the instantaneous power, but what technical adaptaƟ ons are necessary to manage shares between 50-80%. College Dublin, the Irish power system probably has the largest share of wind power in the world. As in the Nordic countries, the power systems in USA only have a small share of wind power so far (a few per cent of Already today, the Irish power system from time to time has the annual electrical energy supply). In order to increase to manage high wind power penetration. In 5 April 2010, the share of wind power, it is considered vital not only wind power accounted for in average 33% of the system to invesƟ gate how to provide the technical fl exibility to total demand, with a peak at 42% early in the morning. -

Gpi Energy Usa Inside 3.Qxd

energy [r]evolution A BLUEPRINT FOR SOLVING GLOBAL WARMING © LANGROCK/ZENIT/GP EUROPEAN RENEWABLE © DREAMSTIME ENERGY COUNCIL © VISSER/GREENPEACE report usa national energy scenario introduction 4 executive summary 6 1 climate protection 9 2 nuclear threats 13 3 the energy [r]evolution 16 4 scenarios for a future energy supply 24 5 the usa energy [r]evolution scenario 38 6 energy resources and security of supply 46 7 energy technologies 66 8 policy recommendations 79 appendix 84 energy [r]evolution Greenpeace International, European Renewable Energy Council (EREC) date January 2007 institute DLR, Institute of Technical Thermodynamics, Department of Systems Analysis and Technology Assessment, Stuttgart, Germany: Dr.Wolfram Krewitt, Sonja Simon, Stefan Kronshage Ecofys BV,(Demand Projection), P.O. Box 8408, NL-3503 RK Utrecht, Kanaalweg 16-G, NL-3526 KL Utrecht, The Netherlands: Wina Graus, Mirjam Harmelink Regional Partners: OECD North America WorldWatch Institute: Janet Sawin, Freyr Sverrisson; GP USA: John Coeguyt Latin America University of Sao Paulo: Ricardo J. Fujii, Prof. Dr. Stefan Krauter; GP Brazil: Marcelo Furtado OECD Europe EREC: Oliver Schäfer, Arthouros Zervos Transition Economies Vladimir Tchouprov Africa & Middle East Reference Project: “Trans-Mediterranean Interconnection for Concentrating Solar Power” 2006, Dr. Franz Trieb; GP Mediterranean: Nili Grossmann South Asia Rangan Banerjee, Bangalore, India; GP India: Srinivas Kumar East Asia ISEP-Institute Tokyo: Mika Ohbayashi; GP South East Asia: Jaspar Inventor,Tara Buakamsri -

What Went Wrong with Ontario's Energy

What went wrong with Ontario’s energy policy? Comparing spin & reality Compiled for CENTRAL BRUCE-GREY WIND CONCERNS ONTARIO By Keith Stelling, MA, (McMaster) MNIMH, Dip. Phyt., MCPP (England) 10 April, 2010 http://windconcernsontario.wordpress.com/ [email protected] Table of Contents Executive Summary 3 Introduction 4 Background 4 About this report 9 I. Feasibility: Where are the CO2 emission savings? 9 II. Cost/benefit accounting: How much? Who pays? Who knows? 17 III. Job creation: 50,000 new “green” jobs? But how many job losses? 39 Conclusion 56 References 55 2 Executive Summary By referring to the economic experience of those European countries that have vigorously promoted wind energy over the last two decades, this report demonstrates that the decisions of the Ontario government did not take into consideration the reality of introducing large scale industrial wind energy onto the grid. In fact, the government’s enthusiasm to embrace what it claimed to be cheap, “clean”, environmentally benign electricity at the same time as diminishing CO2 emissions appears to have ignored all the realistic information that was available, leaving an energy policy based on little more than a leap of faith. Wind energy is neither cheap nor environmentally benign, as this report will demonstrate. This compilation of recently published information demonstrates that Ontario’s energy policy is seriously flawed. It is based upon assumptions that never have and never will be substantiated in practice. Using European reports, it shows that industrial wind turbine and solar panel complexes do not lower CO2 emissions when added in any quantity to the grid. -

The State of Renewable Energy in India 2019 a Citizen's Report the State of Renewable Energy in India 2019 a Citizen's Report

THE STATE OF RENEWABLE ENERGY IN INDIA 2019 A CITIZEN'S REPORT THE STATE OF RENEWABLE ENERGY IN INDIA 2019 A CITIZEN'S REPORT 00Cover, credit and contents.indd 1 17/01/19 3:52 PM Research direction: Chandra Bhushan Authors: Priyavrat Bhati, Priya Sreenivasan, Mandvi Singh, Shweta Miriam Koshy, Pratha Jhawar and Swati Sambyal Research support: Soundaram Ramanathan and Richa Agarwal External contributors: Nikita Das and Jatin Sarode, Prayas, Pune (Chapter 7: Discoms) Editor: Souparno Banerjee Editorial support: Arif Parrey Layouts: Kirpal Singh and Surender Singh Cover design: Ajit Bajaj Infographics and design support: Raj Kumar Singh and Vijayendra Pratap Singh Production: Rakesh Shrivastava and Gundhar Das Research supported and funded by: Shakti Sustainable Energy Foundation We are grateful for the support provided by Shakti Sustainable Energy Foundation (https://shaktifoundation.in). However, the views espoused in this report do not necessarily reflect that of the foundation. The Foundation does not guarantee the accuracy of the data not does it accept any responsibility for the consequences of its use. © 2019 Centre for Science and Environment Material from this publication can be used, but with acknowledgement ISBN: 978-81-86906-27-9 Price: Rs.750 (US $45) Maps used in this report are indicative and not to scale. Citation: Chandra Bhushan, Priyavrat Bhati, Priya Sreenivasan, Mandvi Singh, Pratha Jhawar, Shweta Miriam Koshy and Swati Sambyal 2019, The State of Renewable Energy in India, Centre for Science and Environment, New Delhi Published by Centre for Science and Environment 41, Tughlakabad Institutional Area New Delhi 110 062 Phone: 91-11-40616000 Fax: 91-11-29955879 E-mail: [email protected] Website: www.cseindia.org Printed at Multi Colour Services 00Cover, credit and contents.indd 2 17/01/19 3:52 PM Contents Foreword v Executive summary 1 1. -

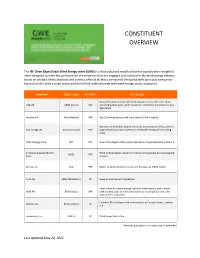

Constituent Overview

CONSTITUENT OVERVIEW The ISE Clean Edge Global Wind Energy Index (GWE) is a float-adjusted modified market capitalization-weighted index designed to track the performance of companies that are engaged and involved in the wind energy industry based on analysis of the products and services offered by those companies (including both pure play companies focused on the wind energy sector and diversified multinationals with wind energy sector exposure). COMPANY STOCK TICKER PP / NPP* AT A GLANCE Diversified with considerable wind exposure across the value chain, ABB Ltd. ABBN (Swiss) NPP including turbine parts, grid connectors, converters, transmission, and digitization Acciona S.A. ANA (Madrid) NPP Top 25 wind producer with more than 8.3 GW installed Operator of Australia's largest electricity generation portfolio, and the AGL Energy Ltd. AGL (Australian) NPP largest listed Australian investor in renewable energy (RE) including wind Alliant Energy Corp. LNT NPP One of the largest utility owner-operators of regulated wind in the U.S. American Superconductor Wind turbine design, electronic controls and systems, and engineering AMSC NPP Corp. services Arcosa, Inc. ACA NPP Maker of wind and transmission and distribution (T&D) towers Arise AB ARISE (Stockholm) PP Swedish onshore wind developer Swiss-based European energy operator (hydroelectric and nuclear) BKW AG BKW (Swiss) NPP with growing sales of wind and services to municipalities and other Swiss and EU customers Canadian RE developer with wind projects in Canada, France, and the Boralex, Inc. BLX (Toronto) PP U.K. Broadwind, Inc. BWEN PP Wind tower fabrication *Denotes pure play vs. non pure play or diversified Last updated May 28, 2021 China Datang Corp. -

RENEWABLE ENERGY in IRELAND 2020 Update

RENEWABLE ENERGY IN IRELAND 2020 Update RENEWABLE ENERGY IN IRELAND 2020 Report RENEWABLE ENERGY IN IRELAND 2020 Report April 2020 1 RENEWABLE ENERGY IN IRELAND 2020 Report Sustainable Energy Authority of Ireland The Sustainable Energy Authority of Ireland (SEAI) is Ireland’s national energy authority, investing in and delivering appropriate, effective and sustainable solutions to help Ireland’s transition to a clean energy future. We work with the Government, homeowners, businesses and communities to achieve this, through expertise, funding, educational programmes, policy advice, research and the development of new technologies. SEAI is funded by the Government of Ireland through the Department of Communications, Climate Action and Environment. SEAI is the official source of energy data for Ireland. We develop and maintain comprehensive national and sectoral statistics for energy production, transformation and end-use. These data are a vital input in meeting international reporting obligations, advising policymakers and informing investment decisions. SEAI’s core statistics functions are to: • Collect, process and publish energy statistics to support policy analysis and development in line with national needs and international obligations • Conduct statistical and economic analyses of energy services sectors and sustainable energy options • Contribute to the development and promulgation of appropriate sustainability indicators. Acknowledgements SEAI gratefully acknowledges the cooperation of all the organisations, agencies, energy suppliers and distributors that provided data and responded to questionnaires throughout the year. © Sustainable Energy Authority of Ireland Reproduction of the contents is permissible provided that the source is acknowledged. 2 RENEWABLE ENERGY IN IRELAND 2020 Report 2018 Highlights Progress towards targets Renewable heat • Overall renewable energy supply was 11% of gross • The amount of renewable energy used for heat final consumption. -

Energy Storage Needs in Ireland

Facilitating energy storage to allow high penetration of intermittent renewable energy Power system overview and RES integration Ireland Source: (ESB) Acknowledgements This report has been produced as part of the project “Facilitating energy storage to allow high penetration of intermittent renewable energy”, stoRE. The logos of the partners cooperating in this project are shown below and more information about them and the project is available on www.store-project.eu The work for this report has been coordinated by UCC and HSU. Author(s) and Contributors Name Organisation Email Thomas Weiss (Author) HSU [email protected] Annicka Wänn (Author) UCC [email protected] Paul Leahy UCC [email protected] Edward Mc Garrigle UCC [email protected] The sole responsibility for the content of this report lies with the authors. It does not necessarily reflect the opinion of the European Union. Neither the EACI nor the European Commission are responsible for any use that may be made of the information contained therein. 2 / 54 Table of Contents EXECUTIVE SUMMARY ...................................................................................................................... 4 1. INTRODUCTION ....................................................................................................................... 13 2. SYSTEM DATA AND FUTURE SCENARIOS .................................................................................. 15 2.1. Power Plant Mix and Energy Production ................................................................................. -

Coversheet for Thesis in Sussex Research Online

A University of Sussex PhD thesis Available online via Sussex Research Online: http://sro.sussex.ac.uk/ This thesis is protected by copyright which belongs to the author. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the Author The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the Author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given Please visit Sussex Research Online for more information and further details The emergence of innovation systems in new locations: theoretical explorations and an in-depth case study of wind energy technologies in Ireland, 1990-2014 Cian O'Donovan Submitted in partial fulfilment for the degree of Doctor of Philosophy SPRU { Science Policy Research Unit University of Sussex November 2016 iii UNIVERSITY OF SUSSEX Cian O'Donovan, Doctor of Philosophy in Science and Technology Policy Studies The emergence of innovation systems in new locations: theoretical explorations and an in-depth case study of wind energy technologies in Ireland, 1990-2014 Summary This thesis is about the processes of creating renewable electricity systems in new locations. Specifically it addresses the challenges and drivers of building-up renewable energy system in a `fast follower' country, Ireland. With increasing scientific, political, civil society and private sector agreement on the need to reduce green-house gas emissions from the provision of electricity, the rolling out of complex, renewable electricity systems from countries in which initial system building activities have taken place to others is an important issue. -

RENEWABLE ENERGY in IRELAND 2019 Report

RENEWABLE ENERGY IN IRELAND 2019 Report RENEWABLE ENERGY IN IRELAND IN ENERGY RENEWABLE 2019 Report RENEWABLE ENERGY IN IRELAND 2019 Report RENEWABLE ENERGY IN IRELAND 2019 Report January 2019 1 RENEWABLE ENERGY IN IRELAND 2019 Report Sustainable Energy Authority of Ireland The Sustainable Energy Authority of Ireland (SEAI) is Ireland’s national energy authority, investing in and delivering appropriate, effective and sustainable solutions to help Ireland’s transition to a clean energy future. We work with Government, homeowners, businesses and communities to achieve this, through expertise, funding, educational programmes, policy advice, research and the development of new technologies. SEAI is funded by the Government of Ireland through the Department of Communications, Climate Action and Environment. SEAI is the official source of energy data for Ireland. We develop and maintain comprehensive national and sectoral statistics for energy production, transformation and end-use. These data are a vital input in meeting international reporting obligations, advising policymakers and informing investment decisions. SEAI’s core statistics functions are to: • Collect, process and publish energy statistics to support policy analysis and development in line with national needs and international obligations • Conduct statistical and economic analyses of energy services sectors and sustainable energy options • Contribute to the development and promulgation of appropriate sustainability indicators. Acknowledgements SEAI gratefully acknowledges the cooperation of all the organisations, agencies, energy suppliers and distributors that provided data and responded to questionnaires throughout the year. © Sustainable Energy Authority of Ireland Reproduction of the contents is permissible provided that the source is acknowledged. 2 RENEWABLE ENERGY IN IRELAND 2019 Report Highlights Progress towards targets, 2017 • Overall renewable energy supply was 10.6% of • Renewable ambient energy captured by heat- gross final consumption.