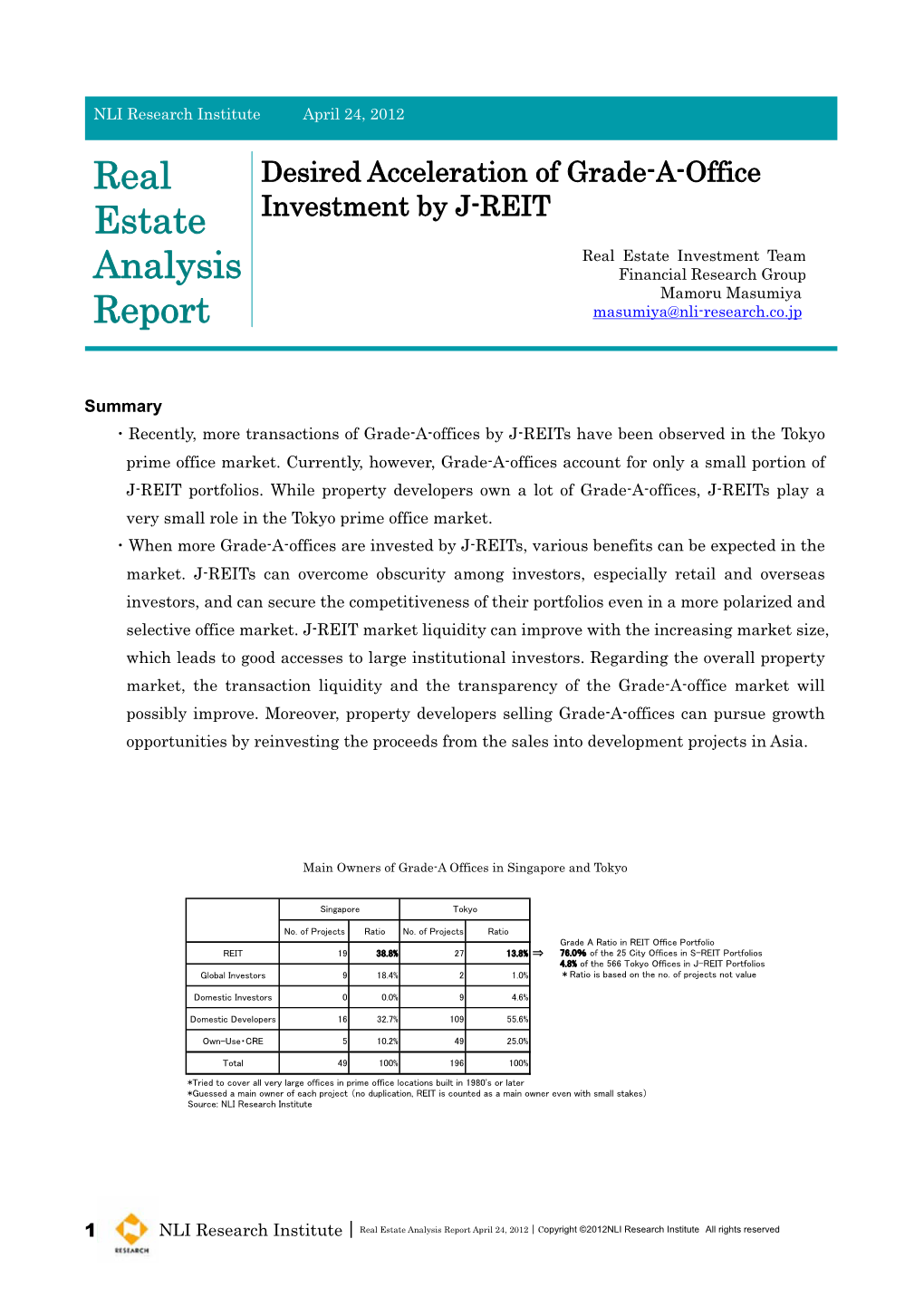

Desired Acceleration of Grade-A-Office Investment by J-REIT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Integrated Report 2019

Integrated Report 2019 Sumitomo Realty & Development Co., Ltd. 1 Sumitomo’s Business Philosophy The Sumitomo Realty Group, as the heir of Sumitomo Honsha, Ltd., has developed into a comprehensive real estate enterprise of Continue creating the Sumitomo Group with a history of 400 years. The business philosophy—“Placing prime importance on integrity and sound management in the conduct of its business” and “Under no circumstances, shall it pursue easy gains”—which have been new value with handed down as a guiding principle throughout the Sumitomo’s history, live on in the form of our corporate slogan, “Integrity and "Integrity and Innovation.” Innovation" Placing top priority on Integrity, we will go beyond simple development and relentlessly pursue value creation through our innovative and challenging spirit. Fundamental Mission “Create even better social assets for the next generation.” We have set forth our fundamental mission as “to create even better social assets for the next generation” through our businesses closely associated with people’s daily lives. Based on this fundamental stance, the Sumitomo Realty Group is engaging in business with the aim of creating cities and urban spaces that are resilient to disasters, friendly to people and the environment, and harmonious with history and culture. Contents 2 Sustainable Growth as Tokyo’s No.1 Office Owner 28 Addressing Social Issues through Business Activities 46 Financial Section History of Corporate Value Creation by "Land Innovation" 30 Feature 1 Sustainable urban redevelopment—Osaki -

Tel.03-3246-3236 時代を動かすランドマーク̶̶ 汐留シティセンター。

Specifications 物件概要 Building Profile 名 称 汐留シティセンター Name Shiodome City Center 所在地 東京都港区東新橋1丁目5番2号 Location Higashi-Shimbashi 1-Chome 5-2, Minato-ku, Tokyo 交 通 都営大江戸線「汐留」駅、新交通ゆりかもめ「新橋」駅:徒歩1分 Access 1-minute walk : Oedo Line-Shiodome Station, Yurikamome Line-Shimbashi Station 都営浅草線「新橋」駅:徒歩2分 2-minute walk : Asakusa line-Shimbashi Station JR線、東京メトロ「新橋」駅:徒歩3分 3-minute walk : JR, Ginza Line-Shimbashi Station 主要用途 事務所、店舗 Primary uses Office and retail 構 造 鉄骨造、鉄骨鉄筋コンクリート造 Primary structure type Steel, steel framed reinforced concrete 敷地面積 19,708.33㎡(B街区全体) Site area 19,708.33㎡ (Block B) 延床面積 210,154.24 ㎡(63,571.66坪) Building area 210,154.24㎡ (63,571.66 tsubo) 総貸付面積(事務所) 106,219.57 ㎡(32,131.42坪)[コア内3,132.12㎡(947.46坪)] Rentable area (offices) 106,219.57㎡(32,131.42 tsubo) [within core 3,132.12㎡(947.46 tsubo)] 階 数 地上43階、地下4階、塔屋1階 No. of stories 43 above-ground floors, 4 underground, 1 penthouse 最高高さ GL+215.75 m Max. height GL+215.75m 竣 工 2003年1月 Completion January, 2003 設 計 ケビンローシュ・ジョンディンカルー・アンド・アソシエイツ Architects Kevin Roche, John Dinkeloo and Associates 共同設計 日本設計 Co-Architect Nihon Sekkei Inc. 施 工 竹中工務店 Main contractor Takenaka Corporation プロジェクト・マネジメント 三井不動産 Project management Mitsui Fudosan Co., Ltd. Developers Alderney Investments Pte Ltd., Mitsui Fudosan Co., Ltd. 貸 主 アルダニー・インベストメンツ、三井不動産 Parking capacity 443 vehicles (for Shiodome City Center) 駐車台数 443台(汐留シティセンター分) Elevators (for passengers) Low-rise bank (1F, 4F-12F): Seven elevators (24 persons each) エレベーター設備(乗用) 低 層:24人乗×7基(1F・ 4F-12F) Mid-rise bank (1F, 13F-22F): Eight elevators (24 persons each) -

Real Estate Sector 4 August 2015 Japan

Deutsche Bank Group Markets Research Industry Date Real estate sector 4 August 2015 Japan Real Estate Yoji Otani, CMA Akiko Komine, CMA Research Analyst Research Analyst (+81) 3 5156-6756 (+81) 3 5156-6765 [email protected] [email protected] F.I.T.T. for investors Last dance Bubbles always come in different forms With the big cliff of April 2017 in sight, enjoy the last party like a driver careening to the cliff's brink. Japan is now painted in a completely optimistic light, with the pessimism which permeated Japan after the Great East Japan Earthquake in 2011 forgotten and expectations for the 2020 Tokyo Olympics riding high. The bank lending balance to the real estate sector is at a record high, and we expect bubble-like conditions in the real estate market to heighten due to increased investment in real estate to save on inheritance taxes. History repeats itself, but always in a slightly different form. We have no choice but to dance while the dance music continues to play. ________________________________________________________________________________________________________________ Deutsche Securities Inc. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 124/04/2015. Deutsche Bank Group Markets Research Japan Industry Date 4 August 2015 Real Estate Real estate sector FITT Research Yoji Otani, CMA Akiko Komine, CMA Research Analyst Research Analyst Last dance (+81) 3 5156-6756 (+81) 3 5156-6765 [email protected] [email protected] Bubbles always come in different forms Top picks With the big cliff of April 2017 in sight, enjoy the last party like a driver Mitsui Fudosan (8801.T),¥3,464 Buy careening to the cliff's brink. -

(38Th Fiscal Period) Information Package

Fiscal Period Ended March 2021 (38th Fiscal Period) Information Package (Securities Code: 8961) https://www.mt-reit.jp/en/ (Asset Management Company) MEMO Contents 1. Overview of the Settlement and Forecasts 3 5. Reference 32 Fiscal Period Ended March 2021 Settlement Highlights 4 Balance Sheets 33 Overview of the Settlement for the Fiscal Period Ended March 2021 5 Statements of Income and Retained Earnings 34 Factors for Change in Distributions per Unit 6 Statement of Cash Distributions / Statements of Cash Flows 35 (the fiscal period ended March 2021) Changes in Indicators 36 Forecasts for the Fiscal Period Ending September 2021 7 Factors for Change in Distributions per Unit 8 Changes in Asset Size, LTV and Distribution Per Unit 37 (the fiscal period ending September 2021) Property Portfolio List as of the End of the Fiscal Period 38 Forecasts for the Fiscal Period Ending March 2022 9 Appraisal Values of Portfolio Properties at the Fiscal Period-End 39 2. Operation Status 10 Changes in Occupancy Rate 40 External Growth (Recognition of Conditions and Future Policies) 11 Overview of Occupancy Rate and Lease Contracts at the Fiscal 41 Asset Replacement (Sale of Part of the Tokyo Shiodome Building and 12 Period-End Purchase of Kamiyacho Trust Tower) Portfolio Summary and Breakdown of Property-Related 42 New Property Acquisition (Kamiyacho Trust Tower) 13 Revenues/Expenses Internal Growth (Recognition of Conditions and Future Policies) 14 Interest-Bearing Liabilities 45 Internal Growth (The present leasing status of the Tokyo Shiodome 15 Investors 46 Building/Situation of Rent Revision for Six Office Buildings) Changes in Unit Prices 47 Future response policy regarding Shinbashi Ekimae MTR Building 16 Financial Status (Management Results for the Fiscal Period Under Review 17 Changes in Vacancy Rate and Rent per Unit in Major Cities 48 and Loan Repayment Schedule Diversification) Asset Management Company Remuneration Methods 49 Financial Status (Status of Interest-Bearing Liabilities and Rating) 18 3. -

Fiscal Period Ended September 2018 (33Rd Fiscal Period) Information Package

(Securities Code: 8961) https://www.mt-reit.jp/en/ Fiscal Period Ended September 2018 (33rd Fiscal Period) Information Package (Asset Management Company) MEMO Contents 1. Overview of the Settlement and Forecasts 3 4. Initiatives Related to ESG 24 Fiscal Period Ended September 2018 Settlement Highlights 4 Initiatives Related to ESG 25 Overview of the Settlement for the Fiscal Period Ended September 5 5. Characteristics of MORI TRUST Sogo Reit, Inc. 28 2018 Basic Policy and Characteristics of MORI TRUST Sogo Reit, Inc. 29 Factors for Change in Distributions per Unit 6 (the fiscal period ended September 2018) Mori Trust Group 31 Forecasts for the Fiscal Period ending March 2019 7 Major Properties Held, Developed, etc. in Central Tokyo by Mori Trust Group 32 Factors for Change in Distributions per Unit 8 (the fiscal period ending March 2019) 6. Reference 33 Fiscal Period Ending September 2019 Forecasts and Changes in 9 Balance Sheets 34 Internal Reserves Statements of Income and Retained Earnings 35 Changes in Distributions 10 Statement of Cash Distributions / Statements of Cash Flows 36 11 2. Portfolio Operations Data Changes in Indicators 37 Investment Strategy 12 Changes in Occupancy Rate 38 Initiatives for Internal Growth (1) (Major Situations of Occupancy of 13 Portfolio Summary and Breakdown of Property-Related 39 Individual Properties) Revenues/Expenses Initiatives for Internal Growth (2) (Situation of Rent Revision and 14 Changes in Asset Size, LTV and Distribution Per Unit 42 Initiatives for Cost Reduction) Changes in Unit Prices 43 Property Portfolio List as of the End of the Fiscal Period 15 Asset Management Company Remuneration Methods 44 Appraisal Values of Portfolio Properties at the Fiscal Period-End 16 Overview of Occupancy Rate and Lease Contracts at the Fiscal 17 Period-End Disclaimer / Contact Information 3. -

MORI HILLS REIT INVESTMENT CORPORATION (CODE:3234) Results of 13Th Fiscal Period (Ended January 31, 2013)

MORI HILLS REIT INVESTMENT CORPORATION (CODE:3234) Results of 13th Fiscal Period (Ended January 31, 2013) MORI HILLS REIT INVESTMENT CORPORATION Mori Building Investment Management Co., Ltd. http://www.mori-hills-reit.co.jp/en http://www.morifund.co.jp/english/ 00 Contents 1. Investment highlights 2 2. 13th period financial highlights 16 3. Operation highlights 20 4. Appendix 29 This document has been prepared by MORI HILLS REIT INVESTMENT CORPORATION (“MHR”) for informational purposes only and should not be construed as an offer of any transactions or the solicitation of an offer of any transactions. Please inquire with the various securities companies concerning the purchase of MHR investment units. This document’s content includes forward-looking statements about business performance; however, no guarantees are implied concerning future business performance. Although the data and opinions contained in this document are derived from what we believe are reliable and accurate sources, we do not guarantee their accuracy or completeness. The contents contained herein may change or cease to exist without prior notice. Regardless of the purpose, any reproduction and/or use of this document in any shape or form without the prior written consent from MHR is prohibited. We will send invitations to future financial results briefings to those who participated in the financial results briefing for the thirteenth period based on the personal information they have shared with us; we guarantee that we make every effort to adequately manage and/or use and protect the information in accordance with the private policy posted on the official website of Mori Building Investment Management Co., Ltd. -

20171214-1.Pdf

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) 4th Floor, Kioicho Building, 2017年12月 Aeon Group International 3-12 Kioi-cho, Chiyoda-ku, Tel: +81 3 4580 2113 www.aeongroup-intl.com (December 2017) Tokyo, ZIP 102-0094 16th Floor, Gran Tokyo South Tel: +81 3 4588 8167 2017年12月 Aichi BMO International Tower, 1-9-2, Marunouchi, ai-international.com/ Fax: +81 3 4510 3208 (December 2017) Chiyoda-ku, Tokyo, ZIP 100-6640 10F S-GATE Akasaka sanno, Tel: +81 3 4243 3187 www.theasquithgroup.co 2017年12月 Asquith Group 2, Akasaka, Minato-ku, Fax: +81 3 6740 2388 m (December 2017) Tokyo, ZIP 107-0052 Cerulean Tower,26-1 Sakuragaoka- 2017年12月 Cameo Consulting Ltd cho, Shibuya-ku, Tokyo, ZIP 150- Tel: +81 3 4578 9543 cameo-consulting.com/ (December 2017) 8512 ThinkPark Tower, 2-1-1, Osaki, cathaydupont.com/catha 2017年12月 Cathay DuPont Shinagawa-ku, Tokyo, ZIP 141- Tel: +81 3 4579 5738 ydupont/en/home.html (December 2017) 6001 4th Flr. Maya Bldg. 2-5, Minami Tel: +81 6 4560 4048 2017年12月 CHINATSU AND PARTNERS Hon-machi 1-chome Chuo-ku, chinatsupartners.com/ Fax: +81 6 7635 2860 (December 2017) Osaka, ZIP 541-0054 Level 9, 2-1-1 Edobori, Nishi- 2017年12月 Daiwa Asia ku, Osaka, ZIP 553-0002 (December 2017) 816-8, 2F, Akamichi, Uruma City, 2017年12月 Fuji Global Enterprise Corp Tel: +81 9 8989 5475 Okinawa (December 2017) Ito Bldg.6-14, Minami-Honmachi 2017年12月 Gina, Eri and Associates 3-chome -

Sale of Asset (Mita MT Building)

November 28, 2014 Press Release Issuer of Real Estate Investment Trust Securities MORI TRUST Sogo Reit, Inc. 2-11-7 Akasaka, Minato-ku, Tokyo Satoshi Horino, Executive Director (TSE code 8961) Asset Management Company: MORI TRUST Asset Management Co., Ltd. Satoshi Horino, President and Representative Director Contact: Michio Yamamoto Director and General Manager, Planning and Financial Department Phone: +81-3-3568-8311 Sale of Asset (Mita MT Building) Tokyo, November 28, 2014— Mori Trust Asset Management Co., Ltd. (hereinafter “the asset manager”), the asset management company which manages assets on behalf of Mori Trust Sogo Reit, Inc. (MTR), has announced the sale of an asset. Details are as follows: 1. Sale Summary (1) Type of asset: Real estate (2) Property name: Mita MT Building (hereinafter “the Property”) (3) Sale price: 13,000 million yen (excluding sale overheads and taxes) <reference> Appraisal value of the real estate: 12,000 million yen (appraisal date: October 31, 2014) (4) Book value: 15,616 million yen (at the end of September 2014) (5) Loss: Approximately 2.6 billion yen (Because of unconfirmed elements, including expenses for the sale, the amounts above are approximate estimates.) (6) Contract date: November 28, 2014 (7) Planned closing date: December 10, 2014 (8) Buyer: MORI TRUST CO., LTD. (Please refer to 4. Buyer Overview.) (9) Settlement method: Single payment at the time of delivery Disclaimer: This English language document is provided as a service and is not intended to be an official statement. Should a discrepancy be found, the Japanese original will always govern the meaning and interpretation. 2. -

ARK Hills Sengokuyama Mori Tower

ARK Hills Sengokuyama Mori Tower ■Toranomon-Roppongi District Class 1 Urban Redevelopment Project : Redevelopment Project Overview and History …2 ■ARK Hills Sengokuyama Mori Tower: Overall Plan/Building Site Environment with Rich Greenery …4 ■ARK Hills Sengokuyama Mori Tower (Offices)/Realizing Greatly Flexible Space …5 ■ARK Hills Sengokuyama Residence/ARK Hills Sengokuyama Terrace (Residences) /Proposing a new way of living in Tokyo …7 ■Commercial Space/Supporting Office Workers, Residents, and Neighbors …8 ■Safety and Security …9 ・High earthquake resistance by incorporating the latest technology ・Ensure business continuity with an emergency power generation system that uses city gas ■Environment …11 ・Promotes realization of a low-carbon society: Officially certified with an S Rank, the highest evaluation granted by CASBEE ・Creation of a green area to promote biodiversity: First project in Japan to be awarded the highest rank (AAA) by the JHEP evaluation ・New gate system “Passmooth” to strengthen energy conservation, safety, and security. ■Culture …14 ・Artwork that will be a symbol of the district: Public art “Infinite” 1 ■ Toranomon-Roppongi District Class 1 Urban Redevelopment Project: Redevelopment Project Overview and History This redevelopment project involves a project site covering approximately 2.0 ha. The district is next to the “Roppongi-Toranomon District Redevelopment Project” designated by Minato Ward (designed in 1988 and revised thereafter to become the “Roppongi-Toranomon District Comprehensive Urban Redevelopment Project -

Toranomon Hills Mori Tower for 5,070 Million Yen and Holland Hills Mori Tower for 9,330 Million Yen As of August 2017

Mori Hills REIT Investment Corporation Results of the 23rd Fiscal Period ended January 31, 2018 Presentation Material March 19, 2018 TSE Code: 3234 (Asset Manager) Mori Building Investment Management Co., Ltd. http://www.mori-hills-reit.co.jp/en/ http://www.morifund.co.jp/en/ Disclaimer This document has been prepared by Mori Hills REIT Investment Corporation (“MHR”) for informational purposes only and should not be construed as an offer of any transactions or the solicitation of an offer of any transactions. Please inquire with the various securities companies concerning the purchase of MHR investment units. This document’s content includes forward-looking statements about business performance; however, no guarantees are implied concerning future business performance. Although the data and opinions contained in this document are derived from what we believe are reliable and accurate sources, we do not guarantee their accuracy or completeness. The contents contained herein may change or cease to exist without prior notice. Regardless of the purpose, any reproduction and/or use of this document in any shape or form without the prior written consent from MHR is prohibited. This document contains charts, data, etc. that were prepared by Mori Building Investment Management Co., Ltd. (hereafter, the “Asset Manager”) based on charts, data, indicators, etc. released by third parties. Furthermore, this document includes statements based on analyses, judgments, and other observations concerning such matters by the asset manager as of the date of -

October 31, 2019 Report on the Management Structure and System

[Translation] October 31, 2019 Report on the Management Structure and System of the Issuer of Real Estate Investment Trust Units and Related Parties Issuer of Real Estate Investment Trust Units Mori Hills REIT Investment Corporation Hideyuki Isobe, Executive Director (Securities Code: 3234) Asset Manager Mori Building Investment Management Co., Ltd. Hideyuki Isobe, President & CEO Inquiries: TEL: 03-6234-3234 1. Basic Information (1) Basic Policy concerning Compliance The directors of Mori Hills REIT Investment Corporation (the “Company”) ensure thorough compliance by complying with the Act on Investment Trusts and Investment Corporations (Act No. 198 of 1951, as amended) (the “Investment Trust Act”), the Financial Instruments and Exchange Act (Act No. 25 of 1948, as amended) (the “Financial Instruments and Exchange Act”), and other relevant laws and regulations and internal rules. In addition, in order to ensure that the supervisory directors exercise their supervisory rights and investigative rights, the Company has established a system by which executive directors report to supervisory directors concerning execution of business 1 and ensures that the Company’s board meetings can be held flexibly (such as by utilizing telephone conference or similar means of communication). With respect to the two supervisory directors, the Company is making efforts to build a strong governance structure by appointing outside experts, namely as a lawyer and a real estate appraiser and by fully utilizing internal checking functions. Mori Building Investment Management Co., Ltd. (the “Asset Manager”) is required to perform its business operations in good faith and with due care of a prudent manager for the Company in line with the purpose of the investment management business, and accordingly performs sincere asset investment and management pertaining to real estate properties based on an appropriate compliance structure and internal control structure in order for the Company to gain high trust from the securities market and investors. -

MARKET TREND SURVEY of LARGE-SCALE OFFICE BUILDINGS in TOKYO's 23 WARDS (“Ku”)

MARKET TREND SURVEY OF LARGE-SCALE OFFICE BUILDINGS IN 23 TOKYO WARDS April 27, 2004 MARKET TREND SURVEY of LARGE-SCALE OFFICE BUILDINGS IN TOKYO’S 23 WARDS (“Ku”) (As of December 2003) The Year 2003 Revealed the Dawn of “Urban Regeneration” ~Supply Volume and Absorption Capacity in 2003 Reached Highest Levels Since the Survey was Started ~ ¾Concentration of office buildings to continue in the 3 central wards (Tokyo’s Central Business District) ¾By offering global-standard “Total Area Management Services”, fully mixed- use areas will set the pace for competition Since 1986, Mori Building Company Ltd. (Headquarters: Minato-ku, Tokyo; President and CEO: Minoru Mori) has been regularly conducting surveys of large office buildings with floor space of over 10,000 m2 (hereafter referred to as “Large-Scale Office Buildings”) throughout Tokyo’s 23 wards on the basis of publicly posted project plans (projected construction start and completion dates), on-site observation, and direct interviews with developers. In addition, we are now projecting office market trends, by analyzing from a variety of angles, data taken from a survey of the trends in demand (absorption capacity). The following are the findings of our latest research. ■Outline of Market Trend Survey Survey period : December end 2003 Coverage : Tokyo’s 23 wards Type of property : Large office buildings with total floor space of over 10,000 m2 (built after 1986) (Notes on the contents) ※ Supply volume in this survey refers to the gross total floor space of office accommodation in all large-scale office buildings completed after 1986, excluding floor space in those buildings reserved for other purposes, such as retail, residences, hotels and others.