Working Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Mineral Industry of Congo (Brazzaville) in 2011

2011 Minerals Yearbook CONGO (BRAZZAVILLE) U.S. Department of the Interior September 2013 U.S. Geological Survey THE MINERAL INDUSTRY OF CONGO (BRAZZAVILLE) By Philip M. Mobbs The economy of the Republic of the Congo, also known as refining and natural gas production and processing. International Congo (Brazzaville), was based primarily on the production oil companies operate many of the oilfields (table 2). of crude oil, which was estimated to account for 69% of the nominal gross domestic product in 2011. Petroleum was Commodity Review estimated to account for 79% of total Government revenues, but Metals many of the oilfields were mature. In the short term, decreased production from the older fields was expected to be offset by Copper, Gold, Lead, and Zinc.—SOREMI, which was a new offshore fields. International interest in the development of subsidiary of Gerald Metals, Inc. of the United States (90% the solid mineral resources of Congo (Brazzaville) has increased equity interest) and the Government (10%), operated the Grande in recent years, with much of the focus on the country’s iron ore Mines at Boko Songo and continued with the development of and potash resources (International Monetary Fund, 2012). the Yanga Koubanza lead-zinc project. La Société LULU, which Production was a subsidiary of a Chinese company, received operating permits to reopen base-metal mines on the Mindouli Mpassa Most of Congo (Brazzaville)’s hydrocarbons were produced prospect. from offshore fields, but much of the produced natural gas In September, Africa Holdings Ltd. of the United Kingdom was flared because of the lack of gas-gathering infrastructure. -

Cameron Civil Aviation Authority Statistical Bulletin No. 6

TABLE OF CONTENTS The traffic of Passengers recorded a tremendous increase between 2015 and 2016. The total number of passengers transported by air in Cameroon rose from 1 275 040 to 1 I. AIR TRAFFIC PERFORMANCE...........................................................P3 326 800. For regular commercial flights, departing passenger II. FLIGHT MOVEMENT........................................................................P4 number witnessed an annual growth of 26%, increasing from 635 559 passengers at departure of flights in 2015 to III. PASSENGER FLOWS.......................................................................P5 801 402 in 2016, for both paying and non paying passengers. IV. FREIGHT TRAFFIC..........................................................................P5 At the regional and international networks passenger traffic V. AIRPORT TRAFFIC............................................................................P6 grew from 1 023 800 in 2015 to 1 153 702 international passengers in 2016. This progress showed an annual growth rate of up to 40% (5720152-515266) increase in VI. PERFORMANCE OF AIR TRANSPORT COMPANIES ............................P7 departing passengers for all segments of international flights. ANNEX ...........................................................................................P 8 In the same light the traffic of cargo and mail transported via air to and from Cameroon recorded an exponential growth rate of 76%, rising from about 15 000 tons of freight carried in 2015 to 25 505 tons in 2016. -

CONGO: Peace and Oil Dividends Fail to Benefit Remaining Idps and Other

CONGO: Peace and oil dividends fail to benefit remaining IDPs and other vulnerable populations A profile of the internal displacement situation 25 September, 2009 This Internal Displacement Profile is automatically generated from the online IDP database of the Internal Displacement Monitoring Centre (IDMC). It includes an overview of the internal displacement situation in the country prepared by the IDMC, followed by a compilation of excerpts from relevant reports by a variety of different sources. All headlines as well as the bullet point summaries at the beginning of each chapter were added by the IDMC to facilitate navigation through the Profile. Where dates in brackets are added to headlines, they indicate the publication date of the most recent source used in the respective chapter. The views expressed in the reports compiled in this Profile are not necessarily shared by the Internal Displacement Monitoring Centre. The Profile is also available online at www.internal-displacement.org. About the Internal Displacement Monitoring Centre The Internal Displacement Monitoring Centre, established in 1998 by the Norwegian Refugee Council, is the leading international body monitoring conflict-induced internal displacement worldwide. Through its work, the Centre contributes to improving national and international capacities to protect and assist the millions of people around the globe who have been displaced within their own country as a result of conflicts or human rights violations. At the request of the United Nations, the Geneva-based Centre runs an online database providing comprehensive information and analysis on internal displacement in some 50 countries. Based on its monitoring and data collection activities, the Centre advocates for durable solutions to the plight of the internally displaced in line with international standards. -

The Integration of Geospatial Data Into the Surveillance and Management of HIV/AIDS in Cameroon

Y OF n The Integration of Geospatial Data Into the Surveillance and Management of HIV/AIDS in Cameroon Thesis submitted for the degree of Doctor of Philosophy Paul Foka Lukong 8.4., M. Env. St. School of Social Sciences Geographical and Environmental Smdies National Center for the Social Application of GIS IVlay 2004 . '. THE UÎüIVERSITV LËåät RE#fglruue IF TABLE OF CONTENTS Title page I Table of content ii Abstract X Declaration xiii Acknowledgement xiv Glossary and acronyms XV PART ONE CHAPTER 1 : Introduction 1 1.1 : The global HIV/AIDS situation I 1.2: The Cameroon context 5 1.3: Definition of HIV/AIDS 8 1.4: Origin and transmission of HIV/AIDS virus to humans ll 1.5: Thesis aims and objectives l3 1.6: Outline ofthe Thesis t4 CHAPTER2: Data and Methods t7 2.1: Introduction t7 2.2:}lIY/AIDS data t8 2.3 Types of HIV/AIDS data t9 2.4: Case reporting in Cameroon t9 2.5 : Sentinel surveillance 2l 2.6: Sentinel surveillance in Cameroon (March-July 2000) 24 2.7: Socio-economic data JJ 2.8: Population data 36 2.9:The HIV/AIDS suvey 2001-2002 37 2.10: Ethical clearance and authorizations 38 2.1 I : Pre-testing of questionnaires 40 ll 2.12: Major problems encounter in the field research 45 2.73:Dataon prevention of Mother-to-Child Transmission (PMTCT) of HIV 47 2:14:Data analysis 5l 2 15: Limitations of data from Cameroon 51 2:76: Conclusion 55 CHAPTER 3: The HIV/AIDS Situation in Sub Sahanan Africa and Cameroon 50 3.1: Introduction 56 3.2: Heterosexual transmission 63 3.3: Subpopulations at low-risk of HIV/AIDS: Pregnant women and blood donors 66 3.4: Subpopulations at high-risk of HIV/AIDS: Commercial sex workers, truckers and the military. -

List of Delegations to the Seventieth Session of the General Assembly

UNITED NATIONS ST /SG/SER.C/L.624 _____________________________________________________________________________ Secretariat Distr.: Limited 18 December 2015 PROTOCOL AND LIAISON SERVICE LIST OF DELEGATIONS TO THE SEVENTIETH SESSION OF THE GENERAL ASSEMBLY I. MEMBER STATES Page Page Afghanistan......................................................................... 5 Chile ................................................................................. 47 Albania ............................................................................... 6 China ................................................................................ 49 Algeria ................................................................................ 7 Colombia .......................................................................... 50 Andorra ............................................................................... 8 Comoros ........................................................................... 51 Angola ................................................................................ 9 Congo ............................................................................... 52 Antigua and Barbuda ........................................................ 11 Costa Rica ........................................................................ 53 Argentina .......................................................................... 12 Côte d’Ivoire .................................................................... 54 Armenia ........................................................................... -

Republic of Congo’, Special Report, April 2002

REPUBLIC OF THE ASSESSMENT OF DEVELOPMENT RESULTS EVALUATION OF UNDP CONTRIBUTION CONGO Evaluation Office, August 2008 United Nations Development Programme REPORTS PUBLISHED UNDER THE ADR SERIES Bangladesh Lao PDR Benin Montenegro Bhutan Mozambique Bulgaria Nicaragua China Nigeria Colombia Rwanda Republic of the Congo Serbia Egypt Sudan Ethiopia Syrian Arab Republic Honduras Ukraine India Turkey Jamaica Viet Nam Jordan Yemen EVALUATION TEAM Team Leader Carrol Faubert, Abacus International Management L.L.C. Team Members Abdenour Benbouali, Abacus International Management L.L.C. Hyacinthe Defoundoux-Fila, Abacus International Management L.L.C. Task Manager Michael Reynolds, UNDP Evaluation Office ASSESSMENT OF DEVELOPMENT RESULTS: REPUBLIC OF THE CONGO Copyright © UNDP 2008, all rights reserved. Manufactured in the United States of America The analysis and recommendations of this report do not necessarily reflect the views of the United Nations Development Programme, its Executive Board or the United Nations Member States. This is an independent publication by UNDP and reflects the views of its authors. This independent evaluation was carried by the evaluators from Abacus International Management L.L.C. (NY,USA) Report editing and design: Suazion Inc. (NY,suazion.com) Production: A.K. Office Supplies (NY) FOREWORD This is an independent country-level evaluation, capita GDP, combined with acute poverty and a conducted by the Evaluation Office of the United low human development index, under which the Nations Development Programme (UNDP) in country ranks 139th out of 177. the Republic of the Congo. This Assessment of Development Results (ADR) examines the This evaluation report concludes that UNDP relevance and strategic positioning of UNDP interventions in the Republic of the Congo support and its contributions to the country’s correspond to expressed national priorities and development from 2004 to 2007. -

Suburbanization and Inequality in Transport Mobility in Yaoundé, Cameroon

Global Development Network GDN Working Paper Series Suburbanization and Inequality in Transport Mobility in Yaoundé, Cameroon: Drawing Public Policy for African Cities Ongolo Zogo Valérie Boniface Ngah Epo Faculty of Economics and Management, CEREG, University of Yaoundé II, Cameroon Working Paper No. 78 September, 2013 The Global Development Network (GDN) is a public International Organization that builds research capacity in development globally. GDN supports researchers in developing and transition countries to generate and share high quality applied social science research to inform policymaking and advance social and economic development. Founded in 1999, GDN is headquartered in New Delhi, with offices in Cairo and Washington DC. This paper was produced as part of the research which was conducted in the context of the research project “Urbanization and Development: Delving Deeper into the Nexus” managed by the Global Development Network (GDN). The funds for the present study were provided by the French Ministry of Foreign and European Affairs. The views expressed in this publication are those of the author(s) alone. © GDN, 2013 Suburbanization and Inequality in Transport Mobility in Yaoundé, Cameroon: Drawing Public Policy for African Cities Abstract This study sets to explore the nature of inequality in mobility in the metropolitan region of Yaoundé city using data from the urban displacement plan, to identify pertinent orientations in the transfer of competencies towards local councils. A series of methodologies are combined; Multiple Correspondence Analysis to construct a mobility index, the decomposition framework to explore the nature inequality of mobility in the different Councils of the Yaoundé city and the Regression-based decomposition to identify factors that determine both cost of mobility and inequality in cost of mobility. -

The Metalanguage of Corruption in Cameroon-Part I: the Registers of General Administration, Transport and Education

International Journal of English Linguistics; Vol. 5, No. 2; 2015 ISSN 1923-869X E-ISSN 1923-8703 Published by Canadian Center of Science and Education The Metalanguage of Corruption in Cameroon-Part I: The Registers of General Administration, Transport and Education Gilbert Tagne Safotso1 1 Department of English, University of Maroua, Cameroon Correspondence: Gilbert Tagne Safotso, P. O. Box 282, Dschang, Cameroon. Tel: 237-677-813-172. E-mail: [email protected] Received: January 3, 2015 Accepted: January 30, 2015 Online Published: March 29, 2015 doi:10.5539/ijel.v5n2p47 URL: http://dx.doi.org/10.5539/ijel.v5n2p47 Abstract This paper analyses the metalanguage of corruption in Cameroon. Using examples from the registers of General Administration, Transport and Education, from the sociolinguistic frame, the paper shows that the widespread corruption in Cameroon has led to the development of a rich specialized language to discuss it. In the sectors of General Administration, Transport and Education, simple and neutral expressions in Cameroon French, Cameroon English and Cameroon Pidgin English have acquired subtle meanings that they need the interpretation of someone who knows the system to be fully understood. This study thus tries to throw some light on this domain so far unexplored. Keywords: metalanguage, corruption, bribery, general administration, transport, education 1. Introduction In recent years, corruption has become so rampant across the globe that for some time now a German-based NGO, Transparency International has been ranking many countries of the world according to their index of corruption. These ill practices are generally seen as the plague of the poor countries. -

Rapport 05 Niari

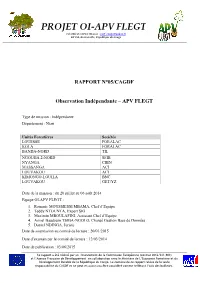

PROJET OI -APV FLEGT Tel (242) 06 660 24 75Email : [email protected] BP 254, Brazzaville, République du Congo RAPPORT N°05/CAGDF Observation Indépendante – APV FLEGT Type de mission : Indépendante Département : Niari Unités Forestières Sociétés LOUESSE FORALAC KOLA FORALAC BANDA-NORD TIL NGOUHA 2-NORD SFIB NYANGA CIBN MASSANGA ACI LOUVAKOU ACI KIMONGO-LOUILA BNC LOUVAKOU GET/YZ Date de la mission : du 20 juillet au 06 août 2014 Equipe OI-APV FLEGT : 1. Romaric MOUSSIESSI MBAMA, Chef d’Equipe 2. Teddy NTOUNTA, Expert SIG 3. Maximin MBOULAFINI, Assistant Chef d’Equipe 4. Armel Baudouin TSIBA -NGOLO, Chargé Gestion Base de Données 5. Daniel NDINGA, Juriste Date de soumission au comité de lecture : 20/01/2015 Date d’examen par le comité de lecture : 12/03/2014 Date de publication : 03/06/2015 Ce rapport a été réalisé par un financement de la Commission Européenne (contrat 2013/323 -903) et l’Agence Française de Développement en collaboration avec le Ministère de L’Economie Forestière et du Développement Durable de la République du Congo. Le contenu de ce rapport relève de la seule responsabilité du CAGDF et ne peut en aucun cas être considéré comme reflétant l’avis des bailleurs . TABLE DES MATIERES Introduction _____________________________________________________________________ 7 1. Disponibilite des documents à la DDEF-N _________________________________________ 8 2. Suivi de l’application de la loi par la DDEF-N _____________________________________ 8 2.1. Capacité opérationnelle de la DDEF-N _______________________________________________________ 8 2.2. Analyse documentaire _____________________________________________________________________ 9 2.2.1. procédures et conditions de délivrance des autorisations de coupe et autres droits _________________ 10 2.2.2. -

Cost-Effectiveness of Enforcing Axle-Load Regulations the Douala

Transportation Research Part A 107 (2018) 216–228 Contents lists available at ScienceDirect Transportation Research Part A journal homepage: www.elsevier.com/locate/tra Cost-effectiveness of enforcing axle-load regulations: The Douala- ☆ ☆☆ N’Djamena corridor in Sub-Saharan Africa , T ⁎ Antonio José Torres Martíneza, Sergio Oliete Josaa, , Francesc Magrinyàb, Jean-Marc Gauthierc a Directorate General for International Cooperation and Development, European Commission, Rue de la Loi 41, B-1049 Brussels, Belgium b Departament d’Enginyeria Civil i Ambiental, Universitat Politècnica de Catalunya, C. Jordi Girona, 1-3, 08034 Barcelona, Spain c Direction générale des infrastructures, des transports et de la mer, Ministère de la Transition écologique et solidaire, Tour Séquoia, 1, place Carpeaux, 92055 Paris La Défense Cedex, France ARTICLE INFO ABSTRACT Keywords: Road conditions in Sub-Saharan Africa are typically poor, and only a subset of the newly con- Transport structed or rehabilitated roads reach their design life. Truck overloading generally causes this Road rapid deterioration. In Africa, there are few success stories on the imposition of axle-load limits. Overloading This study examines the existing regulations on the Douala-N’Djamena international road, which Vehicle operating costs is the main transport corridor in Central Africa and the backbone for internal transport in Axle-load Cameroon. It benefits from the detailed existing weighing data recorded since 1998 in the cor- Africa ridor’s 10 weighing stations. This vast amount of traffic data, together with available information on road structure and deterioration over time, has been used to conduct an accurate calculation of load equivalency factors. The HDM 4 model has been applied to three scenarios between 2000 and 2015: (1) no axle-load control, (2) the real situation and (3) no overloading tolerance. -

Cafi Project Formulation Allocation to Fao

FO:UNJP/PRC/019/UNJ Terminal Report CAFI PROJECT FORMULATION ALLOCATION TO FAO CONGO PROJECT FINDINGS AND RECOMMENDATIONS FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS ROME, 2020 FO:UNJP/PRC/019/UNJ Terminal Report CAFI PROJECT FORMULATION ALLOCATION TO FAO CONGO PROJECT FINDINGS AND RECOMMENDATIONS Report prepared for the Government of Congo by the Food and Agriculture Organization of the United Nations acting as executing agency for the Central African Forest Initiative CENTRAL AFRICAN FOREST INITIATIVE FOOD AND AGRICULTURE ORGANIZATION OF THE UNITED NATIONS Rome, 2020 The designations employed and the presentation of the material in this document do not imply the expression of any opinion whatsoever on the part of the Food and Agriculture Organization of the United Nations concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. iii The Food and Agriculture Organization is greatly indebted to all those who assisted in the implementation of the project by providing information, advice and facilities. iv TABLE OF CONTENTS Page PROJECT INFORMATION AND RESOURCES 5 ACRONYMS 6 EXECUTIVE SUMMARY 7 I. Purpose 7 II. Assessment of Programme Results 8 i) Narrative reporting on results 8 ii) Indicator-based performance assessment 17 iii) Evaluation, best practices and lessons learned 20 iv) Specific stories 21 v) Progress under the governance indicators of the CAFI results framework 23 Page iv of 25 [Central African Forest Initiative-CAFI] -

THE REPUBLIC of CONGO (BRAZZAVILLE) OCTOBER 2003 Country Information and Policy Unit I. SCOPE of DOCUMENT II. GEOGRAPHY III

Congo - Brazzaville, Country Information Page 1 of 42 THE REPUBLIC OF CONGO (BRAZZAVILLE) OCTOBER 2003 Country Information and Policy Unit I. SCOPE OF DOCUMENT II. GEOGRAPHY III. ECONOMY IV. HISTORY V. STATE STRUCTURES VIA. HUMAN RIGHTS ISSUES VIB. HUMAN RIGHTS - SPECIFIC GROUPS ANNEX A - CHRONOLOGY OF MAJOR EVENTS ANNEX B - POLITICAL ORGANISATIONS ANNEX C - MILITIA GROUPS ANNEX D - PROMINENT PEOPLE ANNEX E - REFERENCES TO SOURCE MATERIAL Annex D Prominent People Frederic Bitsangou aka Pasteur Ntoumi Leader of the Ninja rebel faction that was recently fighting the Government. Stated that he would come to Brazzaville if he were offered the post of general in the armed forces. The Government rejected this proposal. Bernard Kolelas Mayor of Brazzaville in 1994 and Prime Minister in 1997. A Lari, Kolelas' main support, and that of his Ninja militia, comes from the Pool region. The Lari ethnic group comprise a large portion of the Ninjas, but not exclusively so. After defeat in 1997, Kolelas fled to the USA and is now in Abidjan, Côte d'Ivoire. In May 2000, he was convicted in absentia of running a private prison, mistreating prisoners and causing their deaths. He was sentenced to death and ordered to pay compensation. Kolelas has denied the charges. http://www.ind.homeoffice.gov.uk/ppage.asp?section=3396&title=Congo%20-%20Brazzaville%2C%20Country%20Information... 11/17/2003 Congo - Brazzaville, Country Information Page 2 of 42 Pascal Lissouba Formed the UPADS party in 1991. President from 1992-1997. Ousted by Sassou-Nguesso after losing the 1997 civil war. Fled to the UK. Cocoyes militia is loyal to him, though whether it still exists as a fighting force is not known.