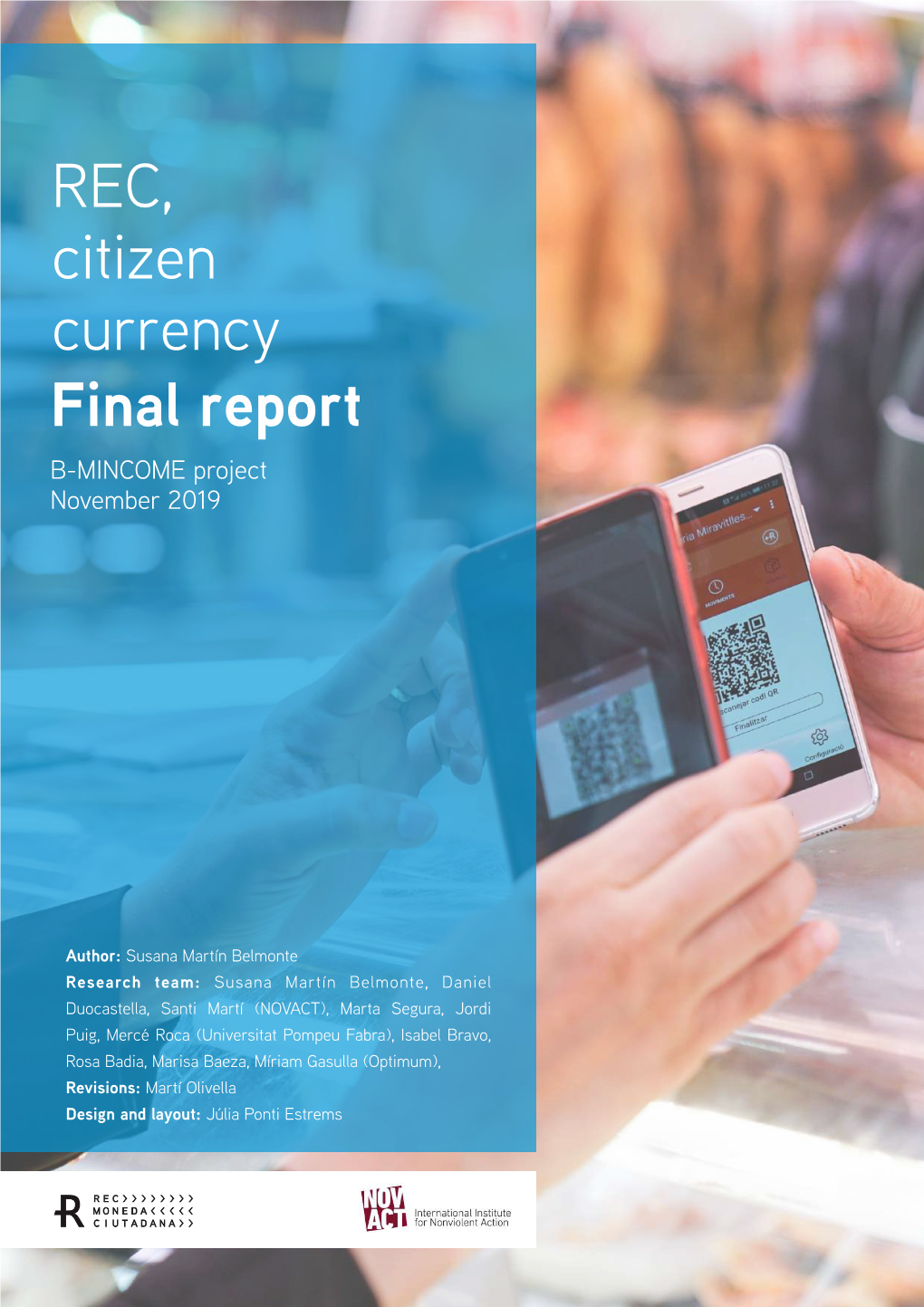

REC, Citizen Currency Final Report B-MINCOME Project November 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sion Discourse in REC Imaginario Catastrofista En REC Bajo El Yugo Del Discur- So Televisivo

° Comunicación y Medios N 36 (2017) ISSN 0716-3991 / e-ISSN 0719-1529 www. comunicacionymedios.uchile.cl 71 Catastrophe imaginary under the yoke of televi- sion discourse in REC Imaginario catastrofista en REC bajo el yugo del discur- so televisivo Andoni Iturbe-Tolosa University of the Basque Country, Bilbao, Spain. [email protected] Abstract Resumen The present article focuses on the analysis of the El presente artículo se centra en el análisis de first part in the REC saga, one of the most im- la primera entrega de la saga de cine fantásti- portant fantasy-horror film franchises in Spanish co y de terror más importante del cine español. cinema. We believe that REC is paradigmatic for Creemos que REC es un ejemplo paradigmáti- the manner in which it links the catastrophe ima- co que entronca tanto con el imaginario catas- ginary with media discourse, and thusly, we op- trófico como con el discurso mediático, por lo ted to analyze this emblematic movie by exami- que se opta por la vía de la intertextualidad y el ning its discourse structures and intertextuality, análisis del discurso para analizar dicha película allowing us to underpin a close interrelation be- emblemática: estructuras de discurso que nos tween cinema and television. The investigation permiten apuntalar hacia una estrecha interrela- concludes that REC, in effect, is indebted not ción entre el cine y la televisión en el audiovisual only to traditional film narrative structures, but contemporáneo. La investigación concluye que, that it also draws on the conventions of contem- efectivamente, REC no es deudora solo de la porary TV reporting in its dealing with a fictional narrativa fílmica sino de los resortes del repor- news report. -

46Th Annual Sam Mcquade Sr Budweiser Charity Softball Tournament

46TH ANNUAL SAM MCQUADE SR BUDWEISER CHARITY SOFTBALL TOURNAMENT 16N=16th St North Diamond MEN’S REC 2 M=Mandan Diamonds TOP BRACKET CK=Clem Kelley Diamonds MC=Sam McQuade Diamonds BISMARCK - KEYSTONE/BANK OF GLEN ULLIN SCH=Scheels Complex (Near Pebble Creek GC) OMAHA, NE - ORIGINATORS SAT 12:10PM24 BISMARCK - KEYSTONE/BANK OF GLEN UCLLWINN=Cottonwood North CWS8 22 9 CWS=Cottonwood South 20 OMAHA, NE - ORIGINATORS OMAHA, NE - ORIGINATORS BYE BEULAH - JIMMYS LOUNGE/THE HUB SAT 4:50PM BYE SAT 7:30AM BYE SAT 4:50PM 9 14 CWS11 CWS7 CWS9 12 BYE 12 MINOT - NORTH HILL BOWL/LUCKY STRIKE LOUNGE SAT 12:10PM SAT 12:10PM BEULAH - JIMMYS LOUNGE/THE HUB CWS11 CWS10 MINOT - NORTH HILL BOWL/LUCKY STRIKE LOUNGE 11 MINOT - NORTH HILL BOWL/LUCKY STRIKE LOUNGE SAT 7:30AM BEULAH - JIMMYS LOUNGE/THE HUB CWS8 27 MINOT - REITER OIL AND GAS/CMT BEULAH - JIMMYS LOUNGE/THE HUB BEULAH - JIMMYS LOUNGE/THE HUB SUN 9:50AM SUN 9:50AM 2 CWS8 BISMARCK - HAYWARD ELECTRIC/SIZZLIN S CONSTRUCTIONCWS9 5 ULEN, MN - BRASETH/STALL CONSTRUCTION SAT 7:30AM 5 BISMARCK - HAYWARD ELECTRIC/SIZZLIN S CONSTRUCTION 14 CWS9 3 19 ULEN, MN - BRASETH/STALL CONSTRUCTION ULEN, MN - BRASETH/STALL CONSTRUCTION SAT 1:20PM SAT 12:10PM BISMARCK - HAYWARD ELECTRIC/SIZZLIN S CONSTRUCTION CWS7 CWS12 14 4 MINOT - DAVIS’ 18 13 5 FESSENDEN - KRAHLERS SOFTBALL SAT 7:30AM18 MINOT - DAVIS’ 15 CWS10 BISMARCK - HAYWARD ELECTRIC MINOT - REITER OIL AND GAS/CMT SUN 7 SUN SIZZLIN S CONSTRUCTION 7:30AM FESSENDEN - KRAHLERS SOFTBALL 7:30AM CWS12 CWS11 MINOT - REITER OIL AND GAS/CMT MINOT - REITER OIL AND GAS/CMT SAT 7:30AM 6 ABERDEEN, SD - DEMPSEYS/HKG 8 20 CWS11 16 16 3 ABERDEEN, SD - DEMPSEYS/HKG MINOT - REITER OIL AND GAS/CMT ABERDEEN, SD - DEMPSEYS/HKG SAT 1:20PM SAT 1:20PM 6CWS11 CWS8 BISMARCK - NEW NEST REALTY 6 RANSOM COUNTY - COBURN COBRAS SAT 7:30AM 13 BISMARCK - NEW NEST REALTY PIERRE, SD - VENOM CWS12 1 BISMARCK - WTP (WHATS THE PLAY) RANSOM COUNTY - COBURN COBRAS SUN 11:00AM SUN 11:00AM 5 CWS8 CWS9 4 BISMARCK - RUG RAT FARGO - BAR9/JENSEN BROS. -

An Investigation of Priming, Self-Consciousness, and Allegiance in the Diegetic Camera Horror Film

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Oxford Brookes University: RADAR An investigation of priming, self-consciousness, and allegiance in the diegetic camera horror film by Peter Turner A thesis submitted in partial fulfilment of the requirements of the award of Doctor of Philosophy by Oxford Brookes University Submitted June 2017 Statement of originality Some of the discussion of The Blair Witch Project throughout this thesis has formed the basis for a book, Devil’s Advocates: The Blair Witch Project (Auteur, 2014). Some of the discussion of priming in chapter four was also used in a conference paper, Behind the Camera: Priming the Spectator of Found Footage Horror, delivered at The Society for Cognitive Studies of the Moving Image in 2015. Sections on personal imagining also formed the basis of a conference paper, Personal Imagining and the Point-of-View Shot in Diegetic Camera Horror Films, delivered at The Society for Cognitive Studies of the Moving Image in 2017. Finally, significant amounts of Chapter 3 and Chapter 5 will be featured in two chapters of an upcoming edited collection on found footage horror films with the working title [Rec] Terror: Essays on Found Footage Horror Films. i Abstract The main research question underpinning this study asks why and how the diegetic camera technique has become so popular to both contemporary horror filmmakers and audiences. In order to answer this question, this thesis adopts a mainly cognitive theoretical framework in order to address the mental schemata and processes that are elicited and triggered by these films. -

![[REC]² Dirigido Por/Directed by PACO PLAZA, JAUME BALAGUERÓ](https://docslib.b-cdn.net/cover/3493/rec-%C2%B2-dirigido-por-directed-by-paco-plaza-jaume-balaguer%C3%B3-2903493.webp)

[REC]² Dirigido Por/Directed by PACO PLAZA, JAUME BALAGUERÓ

REC 2 [REC]² Dirigido por/Directed by PACO PLAZA, JAUME BALAGUERÓ Productoras/Production Companies: CASTELAO PRODUCTIONS, S.A. Miguel Hernández, 81-87. Polígono Pedrosa. 08908 L'Hospitalet de Llobregat (Barcelona). Tel. 93 336 85 55. Fax 93 336 85 68. www.filmax.com E-mail: [email protected] Con la participación de/with the participation of: TVE, CANAL+ ESPAÑA Dirección/Directors: PACO PLAZA, JAUME BALAGUERÓ. Producción/Producer: JULIO FERNÁNDEZ. Producción ejecutiva/Executive Producers: JULIO FERNÁNDEZ, CARLOS FERNÁNDEZ. Coproducción ejecutiva/Co-Executive Producers: ALBERTO MARINI. Dirección de producción/Line Producer: TERESA GEFAELL, ORIOL MAYMÓ. Jefe de producción/Production Manager: MARTA SÁNCHEZ. Guión/Screenplay: JAUME BALAGUERÓ, PACO PLAZA, MANUEL DÍEZ. Fotografía/Photography: PABLO ROSSO. Música/Score: CARLOS ANN. Dirección artística/Production Design: GEMMA FAURÍA. Vestuario/Costume Design: GLORIA VIGUER. Montaje/Editor: DAVID GALLART. Montaje de sonido/Sound Editor: ORIOL TARRAGÓ. Sonido directo/Sound Mixer: XAVI MAS. Mezclas/Re-recording Mixer: MARC ORTS. Ayudante de dirección/Assistant Director: DANIELA FORN. Casting: CRISTINA CAMPOS. Efectos especiales de maquillaje/Special Make-up Effects: DAVID AMBIT, SANTI GIJÓN, JUAN OLMO, PAULA REQUENA. Peluquería/Hairdressing: IMMA PÉREZ. Web: www.rec2lapelicula.com Efectos digitales/Visual Effects: ÀLEX VILLAGRASA (Supervisión). Intérpretes/Cast: JONATHAN MELLOR, ÓSCAR SÁNCHEZ ZAFRA, ARIEL CASAS, ALEJANDRO CASASECA, PABLO ROSSO, MANUELA VELASCO (Ángela Vidal). Vídeo digital a 35 mm. Panorámico 1:1,85. Duración/Running time - Metraje/Metres: 88 minutos. 2.400 metros. Tipo de cámara/Camera model: Panasonic AJ-HPX3000, AG- HVX200, Sony XC-555 y Sony Handycam MiniDV DCR-HC38 40X. Laboratorios/Laboratories: IMAGE FILM. Lugares de rodaje/Locations: Barcelona. Fechas de rodaje/Shooting dates: 10/11/2008 - 19/12/2008. -

![[ REC ] 3 GÉNESIS Otros Títulos/Other Titles: [REC]3 GENESIS Dirigido Por/Directed by PACO PLAZA](https://docslib.b-cdn.net/cover/6628/rec-3-g%C3%A9nesis-otros-t%C3%ADtulos-other-titles-rec-3-genesis-dirigido-por-directed-by-paco-plaza-3986628.webp)

[ REC ] 3 GÉNESIS Otros Títulos/Other Titles: [REC]3 GENESIS Dirigido Por/Directed by PACO PLAZA

[ REC ] 3 GÉNESIS Otros títulos/Other titles: [REC]3 GENESIS Dirigido por/Directed by PACO PLAZA Productoras/Production Companies: REC GENESIS, A.I.E. (99%) Miguel Hernández, 81-87. Polígono Pedrosa. 08908 L'Hospitalet de Llobregat (Barcelona). Tel.: 93 336 85 55. Fax: 93 336 85 68. www.filmax.com ; [email protected] CASTELAO PICTURES, S.L. (1%) Miguel Hernández, 81-87. Polígono Pedrosa. 08908 L'Hospitalet de Llobregat (Barcelona). Tel.: 93 336 85 55. Fax: 93 336 85 68. www.filmax.com ; [email protected] Con la participación de/With the participation of: TVE, CANAL+ ESPAÑA, ONO. Con la colaboración de/With the collaboration of: TELEVISIÓ DE CATALUNYA. Director: PACO PLAZA. Producción/Producer: JULIO FERNÁNDEZ. Producción ejecutiva/Executive Producers: JULIO FERNÁNDEZ, CARLOS FERNÁNDEZ, ALBERTO MARINI. Producción asociada/Associate Producer: ELISA SALINAS. Dirección de producción/Line Producers: TERESA GEFAELL, ORIOL MAYMÓ. Productor creativo/ Creative Producer: JAUME BALAGUERÓ. Guión/Screenplay: LUISO BERDEJO, PACO PLAZA. Fotografía/Photography: PABLO ROSSO. Música/Score: MIKEL SALAS. Dirección artística/Production Design: GEMMA FAURÍA. Vestuario/Costume Design: OLGA RODAL. Montaje/Editing: DAVID GALLART. Montaje de sonido/Sound Design: GABRIEL GUTIÉRREZ. Ayudante de dirección/Assistant Director: FERNANDO IZQUIERDO. Casting: CRISTINA CAMPOS, ANA ISABEL VELÁZQUEZ. Maquillaje/Make-up: PATRICIA REYES. Efectos especiales de maquillaje/Special Make-up Effects: DAVID AMBIT. Peluquería/Hairdressing: PATRICIA REYES. Web: www.recoficial.com Efectos digitales/Visual Effects: ÀLEX VILLAGRASA. Intérpretes/Cast: LETICIA DOLERA (Clara), DIEGO MARTÍN (Koldo), ISMAEL MARTÍNEZ (Rafa), ÀLEX MONNER (Primo Adrián), CLAIRE BASCHET (Natalia), SR. B (Atún), JANA SOLER (Tita Hermana Clara), EMILIO MENCHETA (Tío Víctor), ADOLF BATALLER (Domingo), DOLORES MARTÍN (Manoli), BLAI LLOPIS (Quiquín), MIREIA ROS (Menchu), JOSÉ DE LA CRUZ (Abuelo Matías), XAVIER RUANO (Cura). -

Rec 2007 Movie Download in Hindi

Rec 2007 Movie Download In Hindi 1 / 4 Rec 2007 Movie Download In Hindi 2 / 4 3 / 4 Rec is a 2007 Spanish found-footage horror film co-written and directed by Jaume Balagueró and Paco Plaza. The film centers on a news reporter and her .... Feb 16, 2015 - "Rec" > 2007 > Directed by: Jaume Balagueró & Paco Plaza > Horror / Mystery / Avant-garde / Experimental / Psychological Thriller / Sci-Fi .... Amazon.com: Rec 1 [Blu-ray] [2007]: Movies & TV.. rec 2007 movie download in hindiinstmank.. [Rec] (in Hollywood Movies) [Rec] (2007) - Download Movie for mobile in best quality 3gp and mp4 format. Also stream [Rec] on your mobile, tablets and ipads.. It is full movie Rec 2007 720p in Bluray. REC (2007) ... Bluray HEVC 300MB · Download Dead Silence 2007 Dual Audio Hindi English 480p BluRay 300MB .... Synopsis Film [Rec] (2007) BluRay 720p MP4 + MKV: "REC" turns on a ... rec 2007 movie download in hindi 480p (65); rec 2007 full movie .... Athidhi Movie Free Download In Hindi 3gp. ... Free Download Bollywood Hollywood Full HD. Movies .Download Free ... Rec 2007 Movie .... [REC] 2007 Ending Explained (Hindi) is here!!Watch movie here!!link : https://youtu.be/EMj5CQrk2yoInstagram link..please follow .... Latest 2020 Nollywood Movies, Latest 2020 Action Movies, Latest 2020 Nigerian Movies, Latest 2020 American Movies, Latest 2020 Love Movies, Latest 2020 .... but then jump on the mindless bandwagon for movies like REC., which are just carbon copies of every other lame movie ever made. If you've seen any other .... Rec [2007][BRRip][Spanish][1280-688]350MB. [Movie Title ]….[ Rec [Release Year ]…[ 2007 [iMDb Rating ]….[ 7.7/10 [Genre ]……….[ Drama ... -

Genre, Culture and the Semiosphere New Horror Cinema and Post-9/11

International Journal of Cultural Studies 1–17 © The Author(s) 2014 Reprints and permissions: sagepub.co.uk/journalsPermissions.nav DOI: 10.1177/1367877914528123 ics.sagepub.com Article Genre, culture and the semiosphere New Horror cinema and post-9/11 Angela Ndalianis University of Melbourne, Australia Abstract What has been labelled ‘New Horror’ cinema has opened up its boundaries to incorporate signs specific to social and political events that accompanied and followed the events of 9/11. The reality of terror is transported into the fictional universe of horror. This article presents an interpretation of New Horror cinema using Yuri Lotman’s theory of the semiosphere and Wilma Clark’s extension of his theory in order to engage in a critical rethinking of how genres intersect with culture. The primary focus is on contemporary horror films that function as allegories that address post-9/11 and, in turn, to apply Lotman’s theory of the semiosphere and the concept of cultural ‘explosions’ to account for the generic shifts that have transformed the structure of the horror genre. Keywords 9/11, allegory, cultural explosions, genre theory, horror cinema, Yuri Lotman, semiosphere, terror, torture porn, zombies The semiosphere, genre and post-9/11 In the wake of the terror attacks that took place on 11 September 2001 film critics have commented on the increasing popularity of a new kind of horror film that is not only dark and vicious in the worlds it depicts but which is also socially aware and critical of the cultural context that gave birth to it. What has been labelled ‘New Horror’ cinema has opened up its boundaries to incorporate signs specific to social and political events that accompanied and followed the events of 9/11. -

Women's Rec 2

Campbell County Parks & Recreation 2021 Fall Volleyball League Women’s Rec 2 All Games Played at the Thunder Basin Team Name Captain’s Name Home Phone Work Phone 1 First Interstate Wealth Management Lisa Vnoucek 257-0655 686-4716 2 Where’s The Beaches? Natosha Parks 689-1266 3 Kiss My Ace Kaydie Merrill 406-939-5051 4 Wernsmann Real Estate Team Jamie Knickerbocker 680-5743 5 Notorious D.I.G. Desha Matuska 660-6039 6 Pass Set Hit Tiffany Price 256-8172 7 No Limits Amber Martinez 331-8527 Date Time Site Team VS Team 7:00p Aux 1 First Interstate Wealth Management Where’s The Beaches? Tuesday, September 7 7:00p Aux 2 Kiss My Ace Wernsmann Real Estate Team 7:45p Aux 1 First Interstate Wealth Management Kiss My Ace 7:45p Aux 2 Where’s The Beaches? Notorious D.I.G. 8:30p Aux 1 Wernsmann Real Estate Team No Limits 8:30p Aux 2 Notorious D.I.G. Pass Set Hit 9:15p Aux 1 Pass Set Hit No Limits 7:00p Main 1 First Interstate Wealth Management Wernsmann Real Estate Team Tuesday, September 14 7:00p Main 2 Where’s The Beaches? Kiss My Ace 7:45p Main 1 Where’s The Beaches? Wernsmann Real Estate Team 7:45p Main 2 Kiss My Ace Notorious D.I.G. 8:30p Main 1 First Interstate Wealth Management Pass Set Hit 8:30p Main 2 Notorious D.I.G. No Limits 9:15p Main 1 Pass Set Hit No Limits 7:00p Main 1 Wernsmann Real Estate Team Notorious D.I.G. -

Apocalyptic Imagination in the Hispanic World Hispanic Issues on Line Issue 23 (2019) MORENO-NUÑO U 207

u 9 When One Apocalypse is Not Enough: Representations of the End Times in Spanish Cinema (1962–2017) Carmen Moreno-Nuño The explosive eruption of Donald Trump into the political arena has put the topic of the apocalypse on the table. The anxiety that Trump’s policies gener- ate has been denounced by Mexicans, Middle Eastern immigrants, Muslims, women, the LGTB minority, people with disabilities, scientists, humanists, and also by all those who fear that the president’s erratic decisions in in- ternational affairs could have disastrous consequences. The gloomy tone of Trump’s Inauguration Day speech on January 20th 2017, which can be con- densed in the cry “This American carnage stops here” (emphasis added), is just one example of the fact that fear has become one of the pivotal forces within American politics.1 Although the invocation of the catastrophic has been frequently used as a trope by other populist political movements across the globe, the uncertainties brought forth by this president are unprecedent- ed in American history. The showing of the movie 1984 (Michael Radford, 1984), based on George Orwell’s eponymous novel, at theaters in 43 states in April 4th 2017 reflects the widespread belief that life as we know it is under threat. Countries around the world are responding to the new international order in different ways, from serious political debate to lighter fare. For exam- ple, in Spain, the TV comedy-show El Acabose, led by comedian José Mota and shown in prime time on channel La 1 de TVE, has opted for cathartic humor. -

REC 2 Appendix G

Appendix G River-Related Recreation Survey Results River-Related Recreation Survey Results Lewis River Hydroelectric Projects FERC Nos. 2111, 2213, 2071, and 935 Prepared by: EDAW, Inc. WDFW Prepared for: PacifiCorp and Cowlitz PUD December 2000 RIVER-RELATED RECREATION SURVEY (REC 4) The River-Related Recreation Survey, 1 of 2 surveys being conducted in REC 4, addresses river-oriented (non-flatwater) recreation resources that may be affected by the projects. This river-related recreation survey was conducted to expand upon surveys previously conducted for the Yale Project and reported in the Final Technical Report for Recreation Resources (PacifiCorp 1999). This survey, once finalized, will be compiled into the Recreation Demand Analysis report (REC 2). Study Objectives The objectives of this River-Related Recreation Survey are to help identify: (1) river- oriented recreation values in the study area and relationships to the projects, if any; (2) user relationships to lower river flow volumes, if any; and (3) visitor impressions of project recreation facilities in the lower river area. Results will be used to analyze the potential effects of hydropower development and operations on recreation resources and to develop protection and enhancement measures, if needed. Study Area The study area consists of 2 areas: (1) the Lewis River corridor just above Swift Reservoir to Curly Falls; and (2) a 5-mile reach of the lower river containing 5 boat launch/fishing access sites below Merwin Dam (Merwin Hatchery, Lewis River Hatchery, Cedar Creek, Island, and Haapa). Methods Methods for this study are described on pages REC 4-2 to REC 4-4 of the Study Plan Document (PacifiCorp and Cowlitz PUD 1999). -

Ce Devait Être Le Plus Beau Jour De Ma Vie

Wild Side Films en association avec Le Pacte présente Ce devait être le plus beau jour de ma vie... Un film de Paco Plaza WILD SIDE FILMS EN ASSOCIATION AVEC LE PACTE PRÉSENTE RELATIONS PRESSE : LE NOUVEL OPUS DE LA SAGA [REC] RÉALISÉ PAR PACO PLAZA Céline PETIT & Clément RÉBILLAT 40, rue Anatole France - 92594 Levallois-Perret cedex Tél.: +33 (0)1 41 34 23 50/21 26 AVEC [email protected] [email protected] LETICIA DOLERA www.lepublicsystemecinema.fr ET DIEGO MARTÍN Distribution : PRODUIT PAR JAUME BALAGUERÓ ESPAGNE – 1H20 – 2.35 – 5.1 42, rue de Clichy - 75009 Paris www.wildside.fr En association avec 5, rue Darcet - 75017 Paris Tél.: 01 44 69 59 59 • Fax : 01 49 69 59 41 SORTIE NATIONALE LE 4 AVRIL 2012 www.le-pacte.com www.recgenesis-lefilm.com L’histoire C’est le plus beau jour de leur vie : Koldo et Clara se marient ! Entourés de leur famille et de tous leurs amis, ils célèbrent l’événement dans une somptueuse propriété à la campagne. Mais tandis que la soirée bat son plein, certains invités commencent à montrer les signes d’une étrange maladie. En quelques instants, une terrifiante vague de violence s’abat sur la fête et le rêve vire au cauchemar... Séparés au milieu de ce chaos, les mariés se lancent alors, au péril de leur vie, dans une quête désespérée pour se retrouver... Note d’intention La saga La réalisation Il y a une frontière psychologique très importante entre faire la suite d’un film à succès et en réaliser En rompant avec le langage classique de [REC], c’est-à-dire une caméra subjective portée à l’épaule, le troisième opus. -

The Post- 9/11 Aesthetic: Repositioning the Zombie Film in the Horror Genre Alan Edward Green, Jr

University of South Florida Scholar Commons Graduate Theses and Dissertations Graduate School January 2013 the post- 9/11 aesthetic: repositioning the zombie film in the horror genre Alan Edward Green, Jr. University of South Florida, [email protected] Follow this and additional works at: http://scholarcommons.usf.edu/etd Part of the Film and Media Studies Commons Scholar Commons Citation Green, Jr., Alan Edward, "the post- 9/11 aesthetic: repositioning the zombie film in the horror genre" (2013). Graduate Theses and Dissertations. http://scholarcommons.usf.edu/etd/4798 This Dissertation is brought to you for free and open access by the Graduate School at Scholar Commons. It has been accepted for inclusion in Graduate Theses and Dissertations by an authorized administrator of Scholar Commons. For more information, please contact [email protected]. The Post-9/11 Aesthetic: Repositioning the Zombie Film in the Horror Genre by Alan Edward Green, Jr. A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy Department of English College of Arts and Sciences University of South Florida Major Professor: Phillip Sipiora, Ph.D. Victor Peppard, Ph.D. Elizabeth Metzger, Ph.D. Amy Rust, Ph.D. Date of Approval: May 1, 2013 Keywords: Film Studies, Post-9/11 Cinema, Zombie Films, Non-Zombie Cinema Copyright © 2013, Alan Edward Green, Jr. Dedication I dedicate this scholarly enterprise to my daughter, Tousey Green; I love you always and forever. To my parents, Tom and Judy Trowbridge, all my love; your belief in me was immeasurable in seeing me through completion of this project.