Gilbert Fiorentino

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Compusa Macintosh Products Guide Winter 1992.Pdf

Over 800 Macintosh l1t·oducts at Super Everyday Low Prices! How To Load An Apple Macintosh LC II. GreatWorks Eight full-featured At CompUSA, getting the perfect Apple® applications in one easy-to-use program. Macintosh®comp uter, configured just Word processing, data base, spreadsheet, illus the way you want is just this easy! tration and more. Everything you need to build the perfect system is right within #220)14 your reach. And of course, our friendly, knowledgeable staffers are always close by to help you load up not onlyyo ur cart, but your new computer, too! Appte• Macintosh• 12" RGB Monitor Apple's lowest cost display. Bright, vibrant colors on a high-contrast screen . .28 mm dot pitch. #9002 14 It just doesn't get any easier than this. In fact, we make • 16MHz030 it easy to load a full line of Apple• Macintosh• Processor Apple Macintosh computers, LC 4/40 Computer • 4MBRA'-.i peripherals, accessories and TI1e most affordable • 40 MB Hard Drive software . Over 800 different Madntosh color system • 1.4 MB Apple Mac• products in all! And of features a slender, modular SuperDrive· course, they're all priced design so it's easy to set up • 1 Video, 2 Serial Ports Authorized Dealer super low every day. So load and easy to use. Exce ll ent choice for business or education. • Keyboard #WJ24·1 some today. At CompUSA! Apple, the Apple logo, Mac, and ~1 a cimosh are registcrt>d tradcmarlc; of Apple Computer, In c. Quadra and SuperDrive arc trmlemarlc; of Apple Computer, Inc. A range of desktop mtd notebook contputers for business, hotne mul educati ,..~ Macintosh PCs .................. -

In the United States District Court for the Eastern District of Texas Tyler Division

Case 6:10-cv-00329-LED Document 485 Filed 08/09/11 Page 1 of 41 PageID #: 3621 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS TYLER DIVISION ADJUSTACAM LLC PLAINTIFF, v. Civil Action No. 6:10-cv-329-LED AMAZON.COM, INC.; AUDITEK CORPORATION; BALTIC LATVIAN UNIVERSAL ELECTRONICS, LLC D/B/A BLUE MICROPHONES, LLC D/B/A BLUE MICROPHONE; BEST BUY CO., INC. D/B/A BEST BUY D/B/A ROCKETFISH; BEST BUY STORES, LP; BESTBUY.COM, LLC; BLUE MICROPHONES, LLC; CDW CORPORATION F/K/A CDW COMPUTER CENTERS, INC.; CDW, INC.; COMPUSA.COM, INC.; CREATIVE LABS, INC.; DELL, INC.; DIGITAL INNOVATIONS, LLC; FRY’S ELECTRONICS, INC.; GEAR HEAD, LLC; HEWLETT-PACKARD COMPANY; J&R ELECTRONICS, INC. D/B/A J&R; KOHL'S CORPORATION D/B/A KOHL'S; KOHL'S ILLINOIS, INC.; LIFEWORKS TECHNOLOGY GROUP, LLC; MACALLY PERIPHERALS, INC. D/B/A MACALLY U.S.A; MACE GROUP, INC.; MICRO ELECTRONICS, INC. D/B/A MICRO CENTER; NEW COMPUSA CORPORATION; NEWEGG, INC.; NEWEGG.COM, INC.; OFFICE DEPOT, INC.; OVERSTOCK.COM, INC.; RADIOSHACK CORPORATION; Case 6:10-cv-00329-LED Document 485 Filed 08/09/11 Page 2 of 41 PageID #: 3622 ROSEWILL INC.; SAKAR INTERNATIONAL, INC.; SYSTEMAX, INC. D/B/A COMPUSA; TARGET CORP.; TIGERDIRECT, INC.; AND WAL-MART STORES, INC. DEFENDANTS. JURY TRIAL DEMANDED THIRD AMENDED COMPLAINT FOR PATENT INFRINGEMENT Plaintiff AdjustaCam LLC files this Third Amended Complaint against the foregoing Defendants, namely AMAZON.COM, INC.; AUDITEK CORPORATION; BALTIC LATVIAN UNIVERSAL ELECTRONICS, LLC D/B/A BLUE MICROPHONES, LLC D/B/A BLUE MICROPHONE; BEST BUY CO., INC. -

Systemax Launches All New Circuitcity.Com Website

Systemax Launches All New CircuitCity.com Website Features Low Prices; Wide Selection; Fast Shipping; 24/7 Customer ServiceExtends Company's Leadership in Online Computer and Consumer Electronics Sales PORT WASHINGTON, N.Y., May 22, 2009 (BUSINESS WIRE) -- Systemax Inc. (NYSE:SYX) today announced it has completed the acquisition of the Circuit City e-commerce business and launched the new and improved CircuitCity.com website. The new CircuitCity.com features low everyday prices, great deals, a wide selection of products, fast shipping, world-class 24/7 customer service, advanced search capabilities, and enhanced content, including photo galleries and videos of thousands of the most popular consumer electronics and computer products. Richard Leeds, Chairman and Chief Executive Officer of Systemax, commented, "This acquisition and quick launch of the all new CircuitCity.com further solidifies Systemax's position as a leader in online retailing of value-priced, branded computers and consumer electronics. Circuit City is one of the iconic brands in U.S. electronics retailing with a 60-year legacy. With the longstanding leadership of our TigerDirect.com business and the growing contribution of our CompUSA business acquired last year, we think Systemax is uniquely positioned to best carry forward the great Circuit City brand in the online space." On May 19, 2009 Systemax closed on its agreement to acquire certain trademarks, trade names, domains including www.CircuitCity.com, customer lists and information, and other intangible assets of Circuit City's e-commerce business. The purchase price was $14 million in cash plus a share of future revenue generated utilizing those assets over a 30-month period. -

Apple Computer: the Iceo Seizes the Internet

UC Irvine Globalization of I.T. Title Apple Computer: The iCEO Seizes the Internet Permalink https://escholarship.org/uc/item/4sq9672p Author West, Joel Publication Date 2002-10-01 eScholarship.org Powered by the California Digital Library University of California Apple Computer: The iCEO Seizes the Internet October 2002 JOEL WEST Center for Research on Information Technology and Organizations University of California, Irvine CRITO (Center for Research on Information Technology and Organization) University of California, Irvine 3200 Berkeley Place North Irvine, California 92697-4650 949.824.6387 Tel. 949.824.8091 Fax [email protected] ______________________________________________________________________________ Center for Research on Information Technology and Organizations University of California, Irvine | www.crito.uci.edu Apple Computer: The iCEO Seizes the Internet Joel West <[email protected]> Center for Research on Information Technology and Organizations University of California, Irvine http://www.crito.uci.edu/ October 20, 2002 Contents 1. From Innovation to Crisis...................................................................................... 2 Go-it Alone Standards Strategy .....................................................................3 Failure to Respond to Windows Challenge.................................................... 3 2. Revised Business Strategy .....................................................................................4 Technology.................................................................................................... -

Radioshack Generated Sales of Over $5 Billion in 2005 Mainly Through Its 4,972 Company Operated-Stores, 777 Kiosks, and 1,686 Dealer Outlets Located Across the US

April 24th, 2006 Matthieu Cocq Franck Legoux Patrick de Loe Genki Oka Alexander Zorn 1 TABLE OF CONTENT EXECUTIVE SUMMARY .............................................................................................. 5 PART I. INDUSTRY ANALYSIS................................................................................... 7 I. INDUSTRY OVERVIEW............................................................................................... 7 II. CONSUMER ELECTRONICS MARKET.................................................................... 7 A. Market Size & Growth................................................................................................... 7 B. Product and Service Description.................................................................................... 8 1. Products ...................................................................................................................... 8 2. Services..................................................................................................................... 11 3. Third-party retailing (wireless contracts).................................................................. 11 III. CUSTOMER............................................................................................................... 12 A. Household Penetration ................................................................................................. 12 B. Segmentation................................................................................................................ 13 -

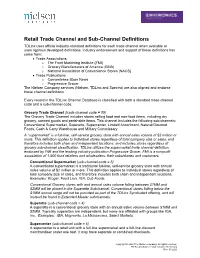

TD Retail Trade Channel and Sub-Channel Definitions

Retail Trade Channel and Sub-Channel Definitions TDLinx uses official industry-standard definitions for each trade channel when available or uses rigorous developed definitions. Industry endorsement and support of these definitions has come from: • Trade Associations: o The Food Marketing Institute (FMI) o Grocery Manufacturers of America (GMA) o National Association of Convenience Stores (NACS) • Trade Publications o Convenience Store News o Progressive Grocer The Nielsen Company services (Nielsen, TDLinx and Spectra) are also aligned and endorse these channel definitions. Every record in the TDLinx Channel Database is classified with both a standard trade channel code and a sub-channel code. Grocery Trade Channel (trade channel code = 05) The Grocery Trade Channel includes stores selling food and non-food items, including dry grocery, canned goods and perishable items. This channel includes the following sub-channels: Conventional Supermarket, Superette, Supercenter, Limited Assortment, Natural/Gourmet Foods, Cash & Carry Warehouse and Military Commissary A “supermarket” is a full-line, self-service grocery store with annual sales volume of $2 million or more. This definition applies to individual stores regardless of total company size or sales, and therefore includes both chain and independent locations; and includes stores regardless of grocery sub-channel classification. TDLinx utilizes the supermarket trade channel definition endorsed by FMI and the leading industry publication Progressive Grocer. FMI is a nonprofit association of 1,500 food retailers and wholesalers, their subsidiaries and customers. Conventional Supermarket (sub-channel code = 5) A conventional supermarket is a traditional full-line, self-service grocery store with annual sales volume of $2 million or more. This definition applies to individual stores regardless of total company size or sales, and therefore includes both chain and independent locations. -

Shirking, Opportunism, Self-Delusion and More: the Agency Problem Today Jayne W

College of William & Mary Law School William & Mary Law School Scholarship Repository Faculty Publications Faculty and Deans 2013 Shirking, Opportunism, Self-Delusion and More: The Agency Problem Today Jayne W. Barnard William & Mary Law School, [email protected] Repository Citation Barnard, Jayne W., "Shirking, Opportunism, Self-Delusion and More: The Agency Problem Today" (2013). Faculty Publications. 1720. https://scholarship.law.wm.edu/facpubs/1720 Copyright c 2013 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository. https://scholarship.law.wm.edu/facpubs SHIRKING, OPPORTUNISM, SELF-DELUSION AND MORE: THE AGENCY PROBLEM LIVES ON Jayne W. Barnard* One would think, after nearly a century of effort to limit the self-serving and wealth-destroying practices of corporate executives and their board of directors, Americans could finally feel confident that the goals of corporate leaders were now fully aligned with those of their investors.' We should now be able to observe these men and women acting with integrity, diligence, and grace. Investor anxiety about shirking, opportunism, self-promotion, and outsized greed should be, one would think, an artifact of the past. Alas, we cannot say we have achieved that enlightened state of affairs. It is still all too possible to find evidence of executive sloth, corruption, mendacity, and hubris. All the gatekeepers, media scoldings, scholarly inquiries, and judicial sermons aimed at curbing the agency problem have failed to restrain the worst in human impulses. Should we be surprised? In thinking about the failures of the law and the culture of business to counteract the predictable weaknesses (and sometimes worse) of human beings, several high-profile examples quickly come to mind: Richard Fuld of Lehman Brothers, Jon Corzine of MF Global Holdings, Ken Lewis of Bank of America, Angelo Mozilo of Countrywide Financial, Aubrey McClendon of Chesapeake Energy, and Rajat Gupta of McKinsey and Goldman Sachs. -

Downloaded in Jan 2004; "How Smartphones Work" Symbian Press and Wiley (2006); "Digerati Gliterati" John Wiley and Sons (2001)

HOW OPEN SHOULD AN OPEN SYSTEM BE? Essays on Mobile Computing by Kevin J. Boudreau B.A.Sc., University of Waterloo M.A. Economics, University of Toronto Submitted to the Sloan School of Management in partial fulfillment of the requirements for the degree of MASSACHUBMMIBE OF TECHNOLOGY Doctor of Philosophy at the AUG 2 5 2006 MASSACHUSETTS INSTITUTE OF TECHNOLOGY LIBRARIES June 2006 @ 2006 Massachusetts Institute of Technology. All Rights Reserved. The author hereby grn Institute of Technology permission to and to distribute olo whole or in part. 1 Signature ot Author.. Sloan School of Management 3 May 2006 Certified by. .............................. ............................................ Rebecca Henderson Eastman Kodak LFM Professor of Management Thesis Supervisor Certified by ............. ................ .V . .-.. ' . ................ .... ...... Michael Cusumano Sloan Management Review Professor of Management Thesis Supervisor Certified by ................ Marc Rysman Assistant Professor of Economics, Boston University Thesis Supervisor A ccepted by ........................................... •: °/ Birger Wernerfelt J. C. Penney Professor of Management Science and Chair of PhD Committee ARCHIVES HOW OPEN SHOULD AN OPEN SYSTEM BE? Essays on Mobile Computing by Kevin J. Boudreau Submitted to the Sloan School of Management on 3 May 2006, in partial fulfillment of the requirements for the degree of Doctor of Philosophy Abstract "Systems" goods-such as computers, telecom networks, and automobiles-are made up of mul- tiple components. This dissertation comprises three esssays that study the decisions of system innovators in mobile computing to "open" development of their systems to outside suppliers and the implications of doing so. The first essay considers this issue from the perspective of which components are retained under the control of the original innovator to act as a "platform" in the system. -

Shopping Centers and Central Business Districts Suffolk County, New York

Shopping Centers and Central Business Districts Suffolk County, New York July 2001 Suffolk County Department of Planning Suffolk County # New York Shopping Centers and Central Business Districts Suffolk County, New York July 2001 Suffolk County Department of Planning H. Lee Dennison Building - 4th Floor 100 Veterans Memorial Highway P.O. Box 6100 Hauppauge, New York 11788 This publication is on the WEB at: http://www.co.suffolk.ny.us/planning Suffolk County Planning Commission Donald Eversoll - At Large CHAIRMAN Robert Martin - Town of Smithtown VICE CHAIRMAN Louis Dietz - Town of Babylon SECRETARY Edward J. Rosavitch - Town of Brookhaven Thomas M. Thorsen - Town of East Hampton Michael J. Macco - Town of Huntington Frank A. Tantone - Town of Islip Richard M. O’Dea - Town of Riverhead George J. Dickerson - Town of Shelter Island David Casciotti - Town of Southampton William Cremers - Town of Southold Laure C. Nolan - Village over 5,000 population Richard London - Village under 5,000 population Ronald Parr - At Large Linda B. Petersen - At Large Suffolk County Department of Planning Thomas A. Isles, AICP DIRECTOR OF PLANNING REPORT PREPARATION Peter K. Lambert RESEARCH DIVISION Roy Fedelem Carol Walsh CARTOGRAPHY DIVISION Suffolk County Department of Planning Hauppauge, New York July 2001 Contents Page EXECUTIVE SUMMARY ............................................................................1 INTRODUCTION ...................................................................................5 DEMOGRAPHIC AND ECONOMIC TRENDS ..........................................................9 -

1 in the United States District Court for the Eastern

Case 6:10-cv-00676-LED Document 2 Filed 12/16/10 Page 1 of 32 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS TYLER DIVISION GUARDIAN MEDIA TECHNOLOGIES, LTD., Plaintiff, v. (1) ACER AMERICA CORPORATION; (2) APEX DIGITAL, INC.; (3) AT&T INC.; (4) CONN’S INC.; (5) FUJITSU AMERICA, INC.; (6) FUJITSU LIMITED; (7) GAMESTOP CORP.; (8) HAIER AMERICA TRADING, L.L.C.; CIVIL ACTION NO. ___________ (9) HISENSE USA CORPORATION; (10) HOPPER RADIO OF FLORIDA, INC.; (11) IMATION CORP.; (12) J & R ELECTRONICS INC.; (13) LASONIC ELECTRONICS JURY TRIAL DEMANDED CORPORATION; (14) LENOVO (UNITED STATES) INC.; (15) MEMOREX PRODUCTS, INC.; (16) MICRO CENTER SALES CORPORATION; (17) MICROSOFT CORPORATION; (18) MOTOROLA, INC.; (19) OFFICE DEPOT, INC.; (20) ON CORP US, INC.; (21) PROTON INTERNATIONAL AMERICA, INC.; (22) PROTRON DIGITAL CORPORATION; (23) RENT-A-CENTER, INC.; (24) ROBERT BOSCH, LLC; (25) SKYWORTH ELECTRONICS, INC.; (26) SOUND AROUND INC.; (27) STAPLES, INC.; (28) STARLITE CONSUMER ELECTRONICS (USA) INC.; (29) STARLITE INTERNATIONAL HOLDINGS, LTD.; (30) TATUNG COMPANY OF AMERICA, INC.; 1 Case 6:10-cv-00676-LED Document 2 Filed 12/16/10 Page 2 of 32 (31) TIGERDIRECT, INC.; (32) TIVO INC.; (33) TTE TECHNOLOGY, INC.; (34) VERIZON COMMUNICATIONS INC.; (35) VIDEOLAND, LLC; AND (36) VIEWSONIC CORPORATION. Defendants. ORIGINAL COMPLAINT FOR PATENT INFRINGEMENT Plaintiff GUARDIAN MEDIA TECHNOLOGIES, LTD. files this Original Complaint against the above-named Defendants, alleging as follows: PARTIES 1. Guardian Media Technologies, Ltd. (“Guardian”) is a Texas limited partnership. Guardian has its principal place of business in Longview, TX. 2. Upon information and belief, Defendant Acer America Corporation (“Acer”) is a corporation organized and existing under the laws of the State of California with its principal place of business located at 333 West San Carlos Street, Suite 1500, San Jose, California 95110. -

Case 1:14-Cr-20854-JEM Document 25 Entered on FLSD Docket 02/11/2015 Page 1 of 26

Case 1:14-cr-20854-JEM Document 25 Entered on FLSD Docket 02/11/2015 Page 1 of 26 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE № 14-20854-CR-MARTINEZ UNITED STATES OF AMERICA, Plaintiff, vs. GILBERT FIORENTINO, Defendant, ___________________________/ DEFENDANT GILBERT FIORENTINO’S RESPONSE TO THE PRESENTENCE INVESTIGATION REPORT AND REQUEST FOR AN ALTERNATIVE SENTENCE The Defendant, GILBERT FIORENTINO, by and through his undersigned counsel, and pursuant to U.S.S.G. § 6A1.2-3, p.s., Fed. R. Crim. P. 32 (d), (e)(2) and (f), and the Fifth and Sixth Amendments to the United States Constitution, respectfully file this Response to the Presentence Investigation Report (hereafter “PSR”) and Request for an Alternative Sentence, and as grounds therefore state as follows: I. INTRODUCTION Pursuant to U.S. v. Booker, 543 U.S. 220 (2005), the federal sentencing process has adopted a three-step approach. See Fed. R. Crim. P. 11(M), amended December 1, 2007, U.S. v. Pugh, 515 F.3d 1179 (11th Cir. 2008); and, most recently, Amendment 741 of the Sentencing Guidelines, effective November 1, 2010. First, the Court is to resolve any disputed guideline issues and determine the advisory guideline range. In MR. FIORENTINO’S case, the parties agree that pursuant to paragraphs 9 and 10 of the written Plea Agreement § 2B1.1 of the Sentencing Guidelines is the applicable guideline. Therefore, the base offense level in this case is 6, which is increased based upon the Page 1 of 26 Law Offices of Samuel J. Rabin, Jr., P.A., 800 Brickell Avenue, Suite 1400, Miami, FL 33131, Telephone (305) 358-1064 Case 1:14-cr-20854-JEM Document 25 Entered on FLSD Docket 02/11/2015 Page 2 of 26 amount of loss, the use of sophisticated means and MR. -

CITY of SOUTH MIAMI Vendor Listing by Vendor Name

CITY OF SOUTH MIAMI Vendor Listing by Vendor Name Report Date:11/27/2013 PE ID PE Name 1099 EIN Status 0002954 @ Comm Corporation N AC 0003951 @XI COMPUTER CORP. N AC 0004764 1-866-JUNK-BE-GONE/MIAMI N AC 0000308 10-S SUPPLY N AC 0004997 12 AVENUE COPY SERVICE INC N 59-1950226 AC 0002003 1999 APWA ANNUAL MEETING N AC 0001091 20/20 INSIGHTS INC. Y 65-0505147 AC 0002648 2000 JUNIOR ORANGE BOWL PARADE N AC 0001491 20TH CENTURY PLASTICS N 95-2084551 AC 0002630 3 CMA MEMBERSHIP N AC 0005512 33143 N AC 0001465 500 ROLE MODELS OF EXCELLENCE PROJ. N AC 0004684 911 RESTORATION INC N AC 0000846 A & C CLEANING SERVICE N 0 AC 0004713 A & D FENCING SPECIALIST N 65-0904958 AC 0006006 A & Q FENCE CORPORATION N 65-0835598 AC 0001186 A & R CONCRETE PRODUCTS N AC 0000186 A ABBEY LOCKSMITH CO N AC 0000620 A ADVANCED FIRE N 0 AC 0000623 A B DICK COMPANY N 0 AC 0001500 A BEKA BOOK INC N AC 0005939 A BETTER AIM SEPTIC N 0 AC 0001990 A CONCEPT IN BRONZE INC N AC 0000621 A DRAIN ALL INC N 0 AC 0003889 A FANTASY JUMP N AC 0001041 A KID''S PARTY EXPRESS N 65-0250719 AC 0000616 A LIKELY STORY N 0 AC 0000203 A NAVAS PARTY PRODUCTION N AC 0000619 A SECOND CHANCE INC. N 0 AC 0001312 A T & T N AC 0001593 A T & T N AC 0000622 A TEAM OFFICE PRODUCTS N 0 AC 0003578 A WILLETS-O''NEIL COMPANY N AC 0001405 A WOMAN''S TOUCH STUDIO N 0 AC 0000617 A&C CLEANING SERVICE N 0 AC 0002471 A&D QUALITY LANDSCAPING CORP.