Lupin Limited: Rating Removed from Watch with Developing Implications

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pharma Limited. Lupin Limited, Lupin

Case 8:15-cv-03437-GJH Document 1 Filed 11/10/15 Page 1 of 17 UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MARYLAND SHIRE PHARMACEUTICAL DEVELOPMENT INC., SHIRE DEVELOPMENT LLC, COSMO TECHNOLOGIES LIMITED, and NOGRA Civil Action No. PHARMA LIMITED. Plaintiffs, v. LUPIN LIMITED, LUPIN PHARMACEUTICALS INC., LUPIN INC., and LUPIN ATLANTIS HOLDINGS SA Defendants. COMPLAINT Plaintiffs Shire Pharmaceutical Development Inc., Shire Development LLC (collectively, "Shire"), Cosmo Technologies Limited ("Cosmo"), and Nogra Pharma Limited ("Nogra") (collectively, "Plaintiffs") by their undersigned attomeys, for their Complaint against defendants Lupin Limited ("Lupin Ltd."), Lupin Pharmaceuticals Inc. ("LPI"), Lupin Inc. ("Lupin Inc."), and Lupin Atlantis Holdings SA ("Lupin Atlantis") (collectively "Lupin" or "Defendants") herein, allege as follows: NATURE OF THE ACTION l. This is a civil action for patent infringement arising under the patent laws of the United States, Title 35, United States Code, involving United States Patent No.6,773,720 ("the '720 patent" or "the patent-in-suit"), attached hereto as Exhibit A. Case 8:15-cv-03437-GJH Document 1 Filed 11/10/15 Page 2 of 17 THE PARTIES 2. Plaintiff Shire Pharmaceutical Development Inc. is a corporation organized and existing under the laws of the state of Maryland, having its principal place of business at 1200 Morris Drive, Wayne, PA 19087. 3. Plaintiff Shire Development LLC is a limited liability company organized and existing under the laws of the State of Delaware, having its principal place of business at735 Chesterbrook Boulevard and 1200 Monis Drive, Wayne, Pennsylvania 19087. 4. Plaintiff Cosmo is a company organized and existing under the laws of Ireland, having its principal place of business at The Connolly Building, 42-43 Amiens Street, Dublin l, Ireland. -

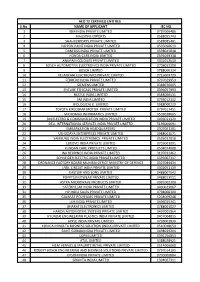

S.No. NAME of APPLICANT IEC NO. 1 IBM INDIA PRIVATE LIMITED 0797006486 2 MAGSONS EXPORTS 0588055743 3 SHAHI EXPORTS PRIVATE LIMI

AEO T2 CERTIFIED ENTITIES S.No. NAME OF APPLICANT IEC NO. 1 IBM INDIA PRIVATE LIMITED 0797006486 2 MAGSONS EXPORTS 0588055743 3 SHAHI EXPORTS PRIVATE LIMITED 0588085481 4 NIPPON PAINT INDIA PRIVATE LIMITED 0505090619 5 DANFOSS INDIA PRIVATE LIMITED 0598045848 6 HONDA CARS INDIA LIMITED 0595049338 7 ANUPAM COLOURS PRIVATE LIMITED 0301012610 8 BOSCH AUTOMOTIVE ELECTRONICS INDIA PRIVATE LIMITED 0708022308 9 BOSCH LIMITED 0788000314 10 VELANKANI ELECTRONICS PRIVATE LIMITED 0715009729 11 FERRERO INDIA PRIVATE LIMITED 0707029953 12 SIEMENS LIMITED 0388070005 13 ENCUBE ETHICALS PRIVATE LIMITED 0396057993 14 NESTLE INDIA LIMITED 0588000531 15 3M INDIA LIMITED 0793012112 16 BIOLOGICAL E. LIMITED 0988000229 17 TOYOTA KIRLOSKAR MOTOR PRIVATE LIMITED 0797012451 18 MICROMAX INFORMATICS LIMITED 0503028665 19 3M ELECTRO & COMMUNICATION INDIA PRIVATE LIMITED 0493021329 20 DELL INTERNATIONAL SERVICES INDIA PRIVATE LIMITED 5196000691 21 EMBARKATION HEADQUARTERS 0307061281 22 USHODAYA ENTERPRISES PRIVATE LIMITED 0988001071 23 SAMSUNG INDIA ELECTRONICS PRIVATE LIMITED 0595032818 24 LENOVO INDIA PRIVATE LIMITED 0705001091 25 KUNDAN CARE PRODUCTS LIMTED 0504074008 26 INA BEARINGS INDIA PRIVATE LIMITED 3197032462 27 SCHNEIDER ELECTRIC INDIA PRIVATE LIMITED 0595007317 28 ORDNANCE FACTORY BOARD MUMBAI OFFICE MINISTRY OF DEFENCE 0307084434 29 JABIL CIRCUIT INDIA PRIVATE LIMITED 0302051139 30 KASTURI AND SONS LIMITED 0488007542 31 POPPYS KNITWEAR PRIVATE LIMITED 0488013011 32 ASTRA MICROWAVE PRODUCTS LIMITED 0991002300 33 CATERPILLAR INDIA PRIVATE LIMITED 0400023067 -

United States Court of Appeals for the Federal Circuit ______

Case: 16-1973 Document: 3-2 Page: 1 Filed: 07/20/2017 NOTE: This disposition is nonprecedential. United States Court of Appeals for the Federal Circuit ______________________ OTSUKA PHARMACEUTICAL CO., LTD., Plaintiff-Appellant v. ZYDUS PHARMACEUTICALS USA, INC., CADILA HEALTHCARE, LIMITED, MYLAN INC., MYLAN PHARMACEUTICALS INC., TORRENT PHARMACEUTICALS LIMITED, TORRENT PHARMA INC., HETERO LABS LIMITED, AJANTA PHARMA LIMITED, AJANTA PHARMA USA INC., AUROBINDO PHARMA LTD., INTAS PHARMACEUTICALS LIMITED, ACCORD HEALTHCARE, INC., AUROBINDO PHARMA USA INC., AUROLIFE PHARMA LLC, LUPIN LIMITED, LUPIN ATLANTIS HOLDINGS S.A., LUPIN PHARMACEUTICALS, INC., ALEMBIC PHARMACEUTICALS LIMITED, AMNEAL PHARMACEUTICALS, LLC, AMNEAL PHARMACEUTICALS INDIA PVT. LTD., Defendants-Appellees ______________________ 2016-1962, 2016-1963, 2016-1964, 2016-1966, 2016-1968, 2016-1970, 2016-1971, 2016-1972, 2016-1973, 2016-1974, 2016-1975, 2016-1978 ______________________ Appeals from the United States District Court for the District of New Jersey in Nos. 1:14-cv-03168-JBS-KMW, Case: 16-1973 Document: 3-2 Page: 2 Filed: 07/20/2017 1:14-cv-04508-JBS-KMW, 1:14-cv-04671-JBS-KMW, 1:14- cv-05876-JBS-KMW, 1:14-cv-06158-JBS-KMW, 1:14-cv- 06890-JBS-KMW, 1:14-cv-07105-JBS-KMW, 1:14-cv- 07252-JBS-KMW, 1:14-cv-07405-JBS-KMW, 1:14-cv- 08074-JBS-KMW, 1:14-cv-08077-JBS-KMW, 1:15-cv- 01585-JBS-KMW, Chief Judge Jerome B. Simandle. ______________________ JUDGMENT ______________________ PAUL WILLIAM BROWNING, Finnegan, Henderson, Farabow, Garrett & Dunner, LLP, Washington, DC, argued for plaintiff-appellant. Also represented by JAMES B. MONROE, CHARLES THOMAS COLLINS-CHASE, ERIC JAY FUES, ANDREA DENISE MAIN; JEFFREY ANDREW FREEMAN, Atlanta, GA. -

In the United States District Court for the Eastern District of Michigan

Case 2:10-cv-10656-AC-MKM Document 1 Filed 02/16/10 Page 1 of 11 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN ABBOTT LABORATORIES and ) ABBOTT RESPIRATORY LLC, ) ) Plaintiffs, ) ) C.A. No. 2:10-cv-10656 v. ) ) SUN PHARMACEUTICAL INDUSTRIES, LTD. ) and SUN PHARMA GLOBAL FZE, ) ) Defendants. ) COMPLAINT Plaintiffs Abbott Laboratories and Abbott Respiratory LLC (collectively, “Abbott”), by their attorneys, hereby allege as follows: Nature of the Action This is an action for patent infringement of U.S. Patent Nos. 6,080,428 (“the ‘428 patent”) and 6,469,035 (“the ‘035 patent”), arising under the patent laws of the United States, Title 35, United States Code, 35 U.S.C. §§ 271 and 281. This action relates to Abbreviated New Drug Application (“ANDA”) No. 20-0484 filed by Sun Pharma Global FZE (“Sun FZE”) with the U.S. Food and Drug Administration (“FDA”) for approval to market 500 mg and 1000 mg niacin extended-release tablets that are generic versions of the 500 mg and 1000 mg strength versions of Abbott’s highly successful NIASPAN® drug product. Related Actions The present action is related to an identical patent infringement action pending before the United States District Court for the District of Delaware, Abbott Laboratories and Abbott Case 2:10-cv-10656-AC-MKM Document 1 Filed 02/16/10 Page 2 of 11 Respiratory, LLC v. Sun Pharmaceutical Industries, Ltd. and Sun Pharmaceuticals, Inc. (C.A. 10-cv-112) (the “Delaware Sun Action”), pertaining to ANDA No. 20-0484 filed by Sun FZE for approval to market generic versions of Abbott’s 500 mg and 1000 mg strength NIASPAN® tablets. -

Revision in Market Lot of Derivative Contracts on Individual Stocks

Department : FUTURES & OPTIONS Download Ref No: NSE/FAOP/45895 Date : September 30, 2020 Circular Ref. No: 87/2020 All Members, Revision in Market Lot of Derivative Contracts on Individual Stocks In pursuance of SEBI guidelines for periodic revision of lot sizes for derivatives contracts specified in the SEBI circular CIR/MRD/DP/14/2015 dated July 13, 2015, the market lots of derivatives contracts shall be revised as follows: Sr. Underlying whose Derivative Count of Annexure No Effective date contract size shall be Underlying Number October 30, 2020 (for Nov 1 Revised Downwards 15 1 2020 & later expiries) 2 Revised Upwards 12 October 30, 2020 (for Jan 2 2021 & later expiries) 3 Unchanged 108 - 3 Revised Downwards but new October 30, 2020 (for Jan 4 lot size is not a multiple of old 1 4 2021 & later expiries) lot size To avoid operational complexities, in case of Annexure 2 and 4 above, following will be applicable: 1. Only the far month contract i.e. January 2021 expiry contracts will be revised for market lots. Contracts with maturity of November 2020 and December 2020 would continue to have the existing market lots. All subsequent contracts (i.e. January 2021 expiry and beyond) will have revised market lots. 2. The day spread order book will not be available for the combination contract of Dec 2020 – Jan 2021 expiry. For the purpose of the computation, the average of the closing price of the underlying has been taken for one month period of September 1st – September 30th 2020. This circular shall come into effect from October 30, 2020. -

Cipla Limited

Cipla Limited Registered Office: Cipla House, Peninsula Business Park, Ganpatrao Kadam Marg, Lower Parel, Mumbai – 400 013 Phone: (9122) 2482 6000, Fax: (9122) 2482 6893, Email: [email protected], Website: www.cipla.com Corporate Identity Number: L24239MH1935PLC002380 Annexure to the Board’s Report Particulars of employee remuneration for the financial year ended 31st March, 2019 As required under section 197(12) of the Companies Act, 2013, read with rule 5(2) and (3) of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014. Employed throughout the year Name Designation Qualification Experience Age Date of Last employment Remuneration (in years) (in years) Employment (Rs.) Abhay Kumar Chief Talent Officer Master of Arts / 17 53 3/10/2016 Piramal Pharma 15,034,298.00 Srivastava Master of Personal Solutions Management Ademola Olukayode Head - Quality Doctorate / MPH / B. 17 48 20/6/2018 US FOOD AND DRUG 17,982,961.00 Daramola Compliance & Tech. ADMINISTRATION Sustainability (US FDA) Ajay Luharuka Head Finance - IPD, B.com,MMS,CFA 23 46 11/7/1996 NIIT Limited 11,922,994.00 API, Specialty & Global Respi Aliakbar Rangwala Senior Business Head M. Sc. / B. Sc. 19 42 19/1/2009 NA 10,677,779.00 - Chronic & Emerging - India Business Alpana Vartak Head - Talent MBA (HR) / B. Sc. 15 41 8/1/2018 Coco - Cola 10,312,782.00 Acquisition Company Anil Kartha Site Head - Bsc, Bpharm 28 56 27/5/1991 Vysali 12,525,338.00 Patalganga - Pharmaceuticals Formulations Anindya Kumar Shee Head - Organization B. Tech. / MBA 18 48 14/1/2016 Reliance Industries 11,084,298.00 Development Ltd. -

DR REDDYS LABORATORIES LTD Form 20-F Filed 2020-06-15

SECURITIES AND EXCHANGE COMMISSION FORM 20-F Annual and transition report of foreign private issuers pursuant to sections 13 or 15(d) Filing Date: 2020-06-15 | Period of Report: 2020-03-31 SEC Accession No. 0001575872-20-000145 (HTML Version on secdatabase.com) FILER DR REDDYS LABORATORIES LTD Mailing Address Business Address 8-2-337, ROAD NO.3 8-2-337, ROAD NO.3 CIK:1135951| IRS No.: 000000000 | Fiscal Year End: 0331 BANJARA HILLS BANJARA HILLS Type: 20-F | Act: 34 | File No.: 001-15182 | Film No.: 20963158 HYDERABAD K7 500-034 HYDERABAD K7 500-034 SIC: 2834 Pharmaceutical preparations 91 40 49002900 Copyright © 2020 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT ¨ OF 1934 OR þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended March 31, 2020 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF ¨ 1934 Commission File Number: 1-15182 DR. REDDY’S LABORATORIES LIMITED (Exact name of Registrant as specified in its charter) Not Applicable TELANGANA, INDIA (Translation of Registrant’s name (Jurisdiction of incorporation or into English) organization) 8-2-337, Road No. 3, Banjara Hills Hyderabad, Telangana 500 034, India +91-40-49002900 (Address of principal executive offices) Saumen Chakraborty, Chief Financial Officer, +91-40-49002004, [email protected] 8-2-337, Road No. -

List of Nodal Officer

List of Nodal Officer Designa S.No tion of Phone (With Company Name EMAIL_ID_COMPANY FIRST_NAME MIDDLE_NAME LAST_NAME Line I Line II CITY PIN Code EMAIL_ID . Nodal STD/ISD) Officer 1 VIPUL LIMITED [email protected] PUNIT BERIWALA DIRT Vipul TechSquare, Golf Course Road, Sector-43, Gurgaon 122009 01244065500 [email protected] 2 ORIENT PAPER AND INDUSTRIES LTD. [email protected] RAM PRASAD DUTTA CSEC BIRLA BUILDING, 9TH FLOOR, 9/1, R. N. MUKHERJEE ROAD KOLKATA 700001 03340823700 [email protected] COAL INDIA LIMITED, Coal Bhawan, AF-III, 3rd Floor CORE-2,Action Area-1A, 3 COAL INDIA LTD GOVT OF INDIA UNDERTAKING [email protected] MAHADEVAN VISWANATHAN CSEC Rajarhat, Kolkata 700156 03323246526 [email protected] PREMISES NO-04-MAR New Town, MULTI COMMODITY EXCHANGE OF INDIA Exchange Square, Suren Road, 4 [email protected] AJAY PURI CSEC Multi Commodity Exchange of India Limited Mumbai 400093 0226718888 [email protected] LIMITED Chakala, Andheri (East), 5 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 6 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 7 NECTAR LIFE SCIENCES LIMITED [email protected] SUKRITI SAINI CSEC NECTAR LIFESCIENCES LIMITED SCO 38-39, SECTOR 9-D CHANDIGARH 160009 01723047759 [email protected] 8 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 9 SMIFS CAPITAL MARKETS LTD. -

Dr. Reddy's Laboratories . Company Dr

BY SHIVAM RAJPUT Dr. Reddy's Laboratories . Company Dr. Reddy's Laboratories Ltd, is a pharmaceutical company based in Hyderabad, Andhra Pradesh, India. Headquarters: HYDERABAD, india Founder: Kallam Anji Reddy Founded: 1984 Company Profile The company's first international move took it to Russia in 1992. There, Dr. Reddy's formed a joint venture with the country's biggest pharmaceuticals producer, Biomed. They pulled out in 1995 amid accusations of scandal, involving "a significant material loss due to the activities of Moscow's branch of Reddy's Labs with the help of Biomed's chief executive". Reddy's sold the joint venture to the Kremlin-friendly Sistema group. In 1993, Reddy's entered into a joint venture in the Middle East and created two formulation units there and in Russia. Reddy's exported bulk drugs to these formulation units, which then converted them into finished products. In 1994, Reddy's started targeting the US generic market by building state of art manufacturing facility. In March 2002 Dr Reddy’s acquired BHM Laboratories ,Beverley, and its wholly owned subsidiary meridian health care, EURO 14.81 million. Recently Dr. Reddy’s entered into R & D and Commercialization agreement with Argenta Discovery Ltd, for the treatment of COPD. In march 2006 Dr.reddy’s acquired Betapharm arzneimittel GmbH from 3i for euro 480 million. Betapharm employs more than 350 personnel and its turnover amounts to Euro 186 million . It commands a share of 3.5 % in the German pharmaceutical market. In 2006 – 2007, Dr Reddy’s generated a revenue of EUR 80.5 million from Europe , which accounted for 18% of the company’s total revenue. -

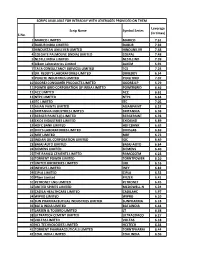

S.No. Scrip Name Symbol Series Leverage (In Times) 1 MARICO

SCRIPS AVAILABLE FOR INTRADAY WITH LEVERAGES PROVIDED ON THEM Leverage Scrip Name Symbol Series (in times) S.No. 1 MARICO LIMITED MARICO 7.61 2 DABUR INDIA LIMITED DABUR 7.92 3 HINDUSTAN UNILEVER LIMITED HINDUNILVR 7.48 4 COLGATE PALMOLIVE (INDIA) LIMITED COLPAL 7.48 5 NESTLE INDIA LIMITED NESTLEIND 7.39 6 Alkem Laboratories Limited ALKEM 6.91 7 TATA CONSULTANCY SERVICES LIMITED TCS 7.24 8 DR. REDDY'S LABORATORIES LIMITED DRREDDY 6.54 9 PIDILITE INDUSTRIES LIMITED PIDILITIND 7.07 10 GODREJ CONSUMER PRODUCTS LIMITED GODREJCP 5.79 11 POWER GRID CORPORATION OF INDIA LIMITED POWERGRID 6.46 12 ACC LIMITED ACC 6.61 13 NTPC LIMITED NTPC 6.64 14 ITC LIMITED ITC 7.05 15 ASIAN PAINTS LIMITED ASIANPAINT 6.52 16 BRITANNIA INDUSTRIES LIMITED BRITANNIA 6.98 17 BERGER PAINTS (I) LIMITED BERGEPAINT 6.78 18 EXIDE INDUSTRIES LIMITED EXIDEIND 6.89 19 HDFC BANK LIMITED HDFCBANK 6.63 20 DIVI'S LABORATORIES LIMITED DIVISLAB 6.69 21 MRF LIMITED MRF 6.73 22 INDIAN OIL CORPORATION LIMITED IOC 6.49 23 BAJAJ AUTO LIMITED BAJAJ-AUTO 6.64 24 SIEMENS LIMITED SIEMENS 6.40 25 THE RAMCO CEMENTS LIMITED RAMCOCEM 6.23 26 TORRENT POWER LIMITED TORNTPOWER 6.10 27 UNITED BREWERIES LIMITED UBL 6.16 28 INFOSYS LIMITED INFY 6.82 29 CIPLA LIMITED CIPLA 6.52 30 Pfizer Limited PFIZER 6.41 31 PETRONET LNG LIMITED PETRONET 6.45 32 UNITED SPIRITS LIMITED MCDOWELL-N 6.24 33 CADILA HEALTHCARE LIMITED CADILAHC 5.97 34 WIPRO LIMITED WIPRO 6.10 35 SUN PHARMACEUTICAL INDUSTRIES LIMITED SUNPHARMA 6.18 36 BATA INDIA LIMITED BATAINDIA 6.44 37 LARSEN & TOUBRO LIMITED LT 6.38 38 ULTRATECH CEMENT -

LUPIN LIMITED Registered Office: 3Rd Floor, Kalpataru Inspire, Off Western Express Highway, Santacruz (East), Mumbai - 400 055

LUPIN LIMITED Registered Office: 3rd Floor, Kalpataru Inspire, Off Western Express Highway, Santacruz (East), Mumbai - 400 055. Tel:+91 22 6640 2323 Ext: 2402/2403 E-mail: [email protected]; Website: www.lupin.com Corporate Identity Number: L24100MH1983PLC029442 NOTICE OF POSTAL BALLOT Dear Members, Notice pursuant to Section 110 of the Companies Act, 2013 Notice is hereby given pursuant to the provisions of Sections 108 and 110 of the Companies Act, 2013 (Act) read with Rule 22 of the Companies (Management & Administration) Rules, 2014, as amended by the Companies (Management & Administration) Amendment Rules, 2015 and other applicable laws and Regulations that Ordinary Resolutions are proposed to be passed by the Members of the Company through Postal Ballot for the following matters: - 1. To approve the appointment of Mr. K. B. S. Anand (DIN: 03518282), as an Independent Director of the Company, for a period of five years, effective August 12, 2020; 2. To approve the appointment of Dr. Punita Kumar-Sinha (DIN: 05229262), as an Independent Director of the Company, for a period of five years, effective August 12, 2020; 3. To approve the appointment of Mr. Robert Funsten (DIN: 08950420), as an Independent Director of the Company, for a period of six months, effective November 10, 2020; and 4. To approve the appointment of Mr. Mark D. McDade (DIN: 09037255), as an Independent Director of the Company, for a period of five years, effective January 28, 2021. The proposed Resolutions and Explanatory Statements under Section 102(2) of the Act, stating material facts are annexed to this Notice for your consideration. -

Lupin Limited: Rating Reaffirmed

January 25, 2021 Lupin Limited: Rating reaffirmed Summary of rating action Instrument* Previous Rated Current Rated Rating Action Amount Amount (Rs. crore) (Rs. crore) Short-term, Fund-based Limits 1,100.0 1,100.0 [ICRA]A1+; re-affirmed Short-term, Non-fund Based Limits 400.0 400.0 [ICRA]A1+; reaffirmed Total 1,500.00 1,500.00 *Instrument details are provided in Annexure-1 Rationale The rating continues to derive comfort from Lupin Limited’s (Lupin’s) robust liquidity position, its strong business profile and geographically diversified revenue mix, with an established position in the key US and Indian pharmaceutical markets. The financial performance of Lupin remained subdued in FY2020 and H1 FY2021, due to its muted performance in the US market. This, in turn, was due to fewer limited competition product launches and weaker-than-expected performance of its key speciality product, Solosec, which was severely impacted during the Covid-19 pandemic owing to reduced doctor visits. Lupin also undertook its second impairment (of $227 million) in the acquired Gavis’ portfolio in FY2020, owing to its lower-than-expected returns. While Lupin’s domestic formulations business continued to outperform the Indian pharmaceutical market (IPM) with respect to chronic therapies in FY2020 and H1 FY2021, sharp decline in acute therapies amid reduced patient footfalls due to the pandemic, adversely impacted its revenues in H1 FY2021. Coupled with high overheads and continued research and development (R&D) expenses, this impacted its operating profit margin (OPM) in H1 FY2021. Despite this, the credit profile of the company remained adequately supported by JPY 33,328 million (~$300 million) cash proceeds received from the divestment of its Japan operations, which were used for debt prepayment.