Max Petroleum Plc, Whose Names Appear on Page 6, Accept Responsibility, Individually and Collectively, for the Information Contained in This Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ecology & Safety ISSN 1314-7234, Volume 11, 2017 Journal Of

Ecology & Safety Journal of International Scientific Publications ISSN 1314-7234, Volume 11, 2017 www.scientific-publications.net ASSESSMENT OF THE GENETIC STATUS OF ICHTHYOFAUNA IN KAZAKH PART OF THE CASPIAN SEA REGION USING MICRONUCLEUS TEST O. G. Cherednichenko, I. N. Magda, A. L. Pilyugina, E. G. Gubitskaya, L. B. Dzhansugurova Institute of General Genetics and Cytology CS MES RK, Almaty, Kazakhstan Abstract The analysis of micronucleus frequency in fish caught in the Kazakhstan part of the Caspian region in the territories of Mangistau and Atyrau regions was carried out. We determined the component composition of sediment samples in the field of fish catch. Fish from carp family was subjected by micronucleus analysis. The nature of violations indicates that in some places, anthropogenic pressure has chemical and radiological component. It noted the correspondence between the cytological and cytogenetic abnormalities in fish erythrocytes and the results of content of man-made pollutants in samples of sediments taken in the trapping field of test animals. Key words: micronucleus test, fish, genetic status, Caspian Sea, Kazakhstan 1. INTRODUCTION The complex interaction of mutagenic environmental factors differ in multilevel (environment, body, tissue, cell) and multi-directional characteristics. Since the experimental study of all possible options for assessing the potential mutagenicity of complex mixtures and combined mutagenic effects is not real, it is necessary to estimate the total mutagenicity in the habitat of living organisms. One approach to solving the complex problems of the organization and carrying out of genetic monitoring of environmental pollution is to conduct research in the field of environmentally contaminated regions. One of the modern and the most promising environmental assessment of the quality of the environment is bio indication methods. -

Investor's Atlas 2006

INVESTOR’S ATLAS 2006 Investor’s ATLAS Contents Akmola Region ............................................................................................................................................................. 4 Aktobe Region .............................................................................................................................................................. 8 Almaty Region ............................................................................................................................................................ 12 Atyrau Region .............................................................................................................................................................. 17 Eastern Kazakhstan Region............................................................................................................................................. 20 Karaganda Region ........................................................................................................................................................ 24 Kostanai Region ........................................................................................................................................................... 28 Kyzylorda Region .......................................................................................................................................................... 31 Mangistau Region ........................................................................................................................................................ -

Annual Bulletin of Monitoring of the Climate State and Climate Change in Kazakhstan: 2018

Ministry of Ecology, Geology and Natural Resources of the RK Republican State Enterprise “Kazhydromet” Scientific Research Center ANNUAL BULLETIN OF MONITORING OF THE CLIMATE STATE AND CLIMATE CHANGE IN KAZAKHSTAN: 2018 ºС 2 1 0 -1 -2 -3 2011 1941 1948 1955 1962 1969 1976 1983 1990 1997 2004 2018 Astana, 2019 CONTENTS SUMMARY 3 INTRODUCTION 5 1 REVIEW OF GLOBAL CLIMATE CHANGE AND ITS STATUS IN 2017 8 2 AIR TEMPERATURE 10 2.1 Air temperature anomalies in Kazakhstan in 2018 11 2.2 The changes of the air temperatures observed in Kazakhstan 22 2.3 Tendencies in extremes of surface air temperature 29 3. PRECIPITATION 35 3.1 Anomalies of precipitation in Kazakhstan in 2018 35 3.2 Observed changes in precipitation in Kazakhstan 42 3.3 Trends in precipitation extremes 48 ANNEX 1 51 ANNEX 2 53 SUMMARY Features of climate in 2018 In general, for the globe, 2018 entered the top ten warmest years for the period of instrumental observations (1850-2018), taking 4th place. Global average temperature in 2018 was by 0,99 °C above the preindustrial level (1850-1900). New record values of the heat content in the upper layers of the ocean, as well as the continued increase in global mean sea level, have been established. A decrease in the extent of the Arctic and Antarctic sea ice was noted. In 2018, 74 tropical cyclones were registered, which significantly exceeds their long-term average number (63). Floods, extreme rainfall and extratropical storms have caused hundreds of human lives and the destruction of tens of thousands of homes. -

81101 Matyzhanov 2019 E.Docx

International Journal of Innovation, Creativity and Change. www.ijicc.net Volume 8, Issue 11, 2019 The Kazakh Professional Song Traditions Matyzhanov Ka, Omarova Ab, Turmagambetova Bc, Kaztuganova Ad, a Doctor of Philology, Department of folklore, Institute of Literature and Art named for M. Auezov, Ministry of Education and Science of Kazakhstan. Republic of Kazakhstan, 050010, Almaty, Kurmangazy Street, 29., b Candidate of art History, Leader Research Fellow the Department "Musicology", Institute of Literature and Art named for M. Auezov, Ministry of Education and Science of Kazakhstan Republic of Kazakhstan, 050010, Almaty, Kurmangazy Street, 29, c Candidate of art History, Atyrau State University named after H. Dosmukhamedova Republic of Kazakhstan, 060011, Atyrau, Student Avenue, 212, d Candidate of art History, Head of the Department "Musicology", Institute of Literature and Art named for M. Auezov, Ministry of Education and Science of Kazakhstan Republic of Kazakhstan, 050010, Almaty, Kurmangazy Street, 29, The purpose of this study is to determine the features of singing traditions which were formed in the 2nd half of the 19th century in the Western region of Kazakhstan. In the course of this study, historical, musical-theoretical, comparative and other methods were used. Prior to this study, only two singing traditions were distinguished, whereas in this article the existence of three singing traditions was scientifically proven, with identification of another singing tradition in the history of music of Kazakhstan. In the musical culture of Kazakhstan, songs of the western region were known as “songs in a heroic spirit”, but this article discovers different temperament of songs. The latest songs are composed by “kayki”. -

Master Plan Study on Integrated Regional Development for Mangis

Japan International Cooperation Agency (JICA) Local Government of Mangistau Oblast Government of the Republic of Kazakhstan MASTER PLAN STUDY ON INTEGRATED REGIONAL DEVELOPMENT FOR MANGISTAU OBLAST IN THE REPUBLIC OF KAZAKHSTAN FINAL REPORT VOLUME III SECTOR REPORT August 2008 RECS International Inc. Yachiyo Engineering Co., Ltd. Currency Equivalents (average Interbank rates as of January 6, 2008) US$1.00=KZT 122.200 US$1.00=JPY 108.652 JPY 1=KZT 1.12570 Source: OANDA.COM, http://www.oanda.com. Master Plan Study on Integrated Regional Development for Mangistau Oblast in the Republic of Kazakhstan Final Report Volume III. Sector Report Table of Contents Chapter 1 Population and Social Conditions.......................................................................................1 1.1 Population and Employment.....................................................................................................1 1.1.1 Population ....................................................................................................................1 1.1.2 Employment.................................................................................................................2 1.2 Health........................................................................................................................................4 1.2.1 Health conditions .........................................................................................................4 1.2.2 Health facilities ............................................................................................................6 -

Environmental Performance Reviews Kazakhstan

ECONOMIC COMMISSION FOR EUROPE Committee on Environmental Policy ENVIRONMENTAL PERFORMANCE REVIEWS KAZAKHSTAN UNITED NATIONS New York and Geneva, 2000 Environmental Performance Reviews Series No. 8 NOTE Symbols of United Nations documents are composed of capital letters combined with figures. Mention of such a symbol indicates a reference to a United Nations document. The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city of area, or of its authorities, or concerning the delimitation of its frontiers or boundaries. UNITED NATIONS PUBLICATION Sales No. E.01.II.E.3 ISBN 92-1-116770-1 ISSN 1020-4563 iii Preface The EPR project in Kazakhstan had originally started in September 1997, but had to be interrupted for organizational reasons. A second preparatory mission therefore had to be organized and took place in October 2000. It resulted in a new structure for the report, which was adapted to the many changes in the country that had occurred in the meantime. The review team for the project was constituted following these decisions and included national experts from Finland, France, Denmark, Germany, Romania, Slovakia, Slovenia, Spain and Uzbekistan, together with the ECE secretariat, UNEP and the Bilthoven Division of the WHO European Centre for Environment and Health. The costs of the participation of experts from countries in transition, as well as the travel expenses of the ECE secretariat, were covered by extrabudgetary funds that had been made available from Finland, Germany and Italy. -

The Country of the Subsoil Assets and Great Victories

Annual Report 2019 The Country of the Subsoil Assets and Great Victories 12 The Country of the Subsoil Assets and Great Victories The Kazakhstan Oil is 120 years old: Everything started in Emba In 2019 the national oil-and-gas industry celebrated the 120-year jubilee. Absolutely this is the remarkable date for all Kazakhstan and for Embamunaigas JSC. There was in the first Emba fields that the glorious future of the Kazakhstan oil industry was built, which is today the locomotive of the country socio-economic development. he history of the Kazakhstan oil industry The oil of Karashungul is decribed as “…very light Tbegins upon in Atyrau terrain, from the first oil, / specific weight of the freshly mined oil in 2–3 gush of oil in the well № 7 of the Karashungul days makes 0.849 /, transparent and prolific in structure in 1899 (now this is the contract territory gases”. of Embamunaigas JSC in Zhylyoyskiy district in Atyrau region). There is also the information on 20 wells in Karaton, drilled in 1900, and some wells drilled in Thsi event was the result of almost two hundred 1908. Karaton is characterozed as “dome-shaped years of research in this region, starting with occurence of oil-bearing strata”. the expeditions of Prince Alexander Bekovich- Cherkasskiy, the campaigns of Ivan Buchholz In 1908 in Iskine deposit, in the well № 5, from (1671–1741), the companion of Tsar Peter the Great, the depth 228 meters, the petroleum industrialist and other researchers. Stakheyev obtained the gush of the light oil with daily flow rate near 8 tons. -

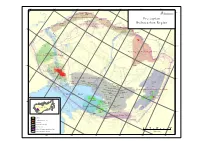

Precaspian Basin Hydrocarbon Province Map (Pdf 4262

42°0'0"E 44°0'0"E 46°0'0"E 48°0'0"E 50°0'0"E 52°0'0"E 54°0'0"E Zhdanovsk Mokrousovsk 54°0'0"N Krasnokutsk North Limansk Karpensk West Rovensk Buzuluk Lobodinsk-Teplovsk Uplift Zone 8 10 Pavlovsk Komsomol'sk Uzensk Talovsk 0 West Lipov 1 Starshinov Precaspian Kurilov 9 Lipov Soldatsk-Stepnovsk 8 South Kislovsk Kurilov-Novouzen Uplift Zone 8 Hydrocarbon Region Novonikol'sk Lobodinsk 12 Sportivnoe Tokarevsk 10 Tsyganovsk 9 W. Teplov 12 1 Kam'enskUl'yanovsk 0 Dar'insk Ural'sk Volgograd 12 Gremyachinsk Teplov 48°0'0"N 6 14 E. Gremyachinsk S Gremyachin 12 1 Chinarevka 10 4 Ural'sk 8 15 16 1 Kuznetsov V 0 o 15 14 l 16 g 14 a 10 10 2 16 1 R 9 1 14 . 2 15 8 16 1 . 14 16 R 1 16 l 2 a Karachaganak 16 7 r 1 2 Orenburg 0 1 U 1 1 0 10 9 10 10 1 1 15 4 1 Tsarynsk 12 16 18 52°0'0"N 4 14 1 11 1 5 8 1 1 2 17 4 14 13 1 16 5 12 1 14 1 2 Voropayevo Karachagan14ak-Troitsk Uplift Zone Sovkhoz North Shadzha 2 1 Bugrinsk Pustynnoe Verblyuzh'e 1 Sarpa Trough 1 2 6 11 6 1 12 10 11 Khalgynsk 1 4 1 9 8 10 1 2 10 1 9 6 1 6 1 1 0 Chingiz 46°0'0"N 1 2 8 13 8 Astrakhan Arch 9 18 20 1 1 1 11 8 Aktyubinsk Aksarai 1 8 11 1 4 Astrakhan 14 6 16 1 1 Karakul A1 rch12 0 2 10 1 16 8 2 2 Beshkul'sk 9 1 Kumisbek 0 1 1 14 1 Imashev 9 12 12 12 Astrakhan Zhaksymai 8 Kirkilinsk 50°0'0"N 12 Shchukatsk-North Caspian Uplift Zone 2 10 12 8 Dayramola 1 1 4 8 7 Sazankurak 7 Baklanii 9 Burbaytal Zhanatalap 10 Oktyabrsk 7 Gran SE Novobagatin Shubarkuduk 12 Karatal Martyshi 0 E Zhanatalap 1 Zhambay Saigak Zaburun'e Zhengel'dy 4 Rovnoe 1 1 SW Kamyshitovyi 6 Gryadov Tanatar Zholdybai N. -

Kazmunaigas Exploration Production Releases Its Annual Report for 2012

KazMunaiGas Exploration Production releases its Annual Report for 2012 Astana, 30 April 2013. JSC KazMunaiGas Exploration Production has published today its Annual Report for 2012*. The report is posted on the Company’s website at www.kmgep.kz. Further, the Company provides below the extracts from its Annual Report in unedited full text as required in accordance with DTR 6.3.5 (1) * Information presented in this annual report is as of April 18, 2013. COMPANY OVERVIEW Mission: KMG EP’s mission is to maximize benefits for the shareholders of the Company, by producing hydrocarbons in an efficient and expedient way, creating long-term economic and social value for the regions in which we operate and providing the development of each employee to reach their potential. Vision: KMG EP – a leading company in the field of hydrocarbon exploration and production in Kazakhstan, among the leaders of oil and gas business in the Caspian region, able to compete globally. KazMunaiGas Exploration Production JSC (“Company” or “KMG EP”) was formed in March 2004 through the merger of JSC Ozenmunaigas (“OMG”) and JSC Embamunaigas (“EMG”). KMG EP is one of the top three leaders in terms of oil production in Kazakhstan. By consolidated production volumes KMG EP controls around 15% of Kazakhstan’s total production and by consolidated proven reserves about 3%. The volume of proved and probable reserves including the Company’s share in Kazgermunai, CCEL and PKI as of 2011 year end were about 285 million tonnes1 (2,083 million barrels). Shares of the Company are listed on the Kazakhstan Stock Exchange (KASE) and global depositary receipts (GDRs) on the London Stock Exchange (LSE). -

Akmola Region F

List of companies in Akmola region Company Name of Address Type of activity name leadership Koksheatuskie Askar K. 475006, Kokshetau city, production Mineral Water Aliev Severny promzon of soft drinks Bottlers LLP t.(31622)65444,65400 and alcohol f 65400, e-mail:[email protected] Tynys OJSC Kairbek K. 475012, Kokshetau city, manufacture Kysainov 13 Mira str. of aviation spare parts, t. (31622) 57563, 33943 medical, gas, f. 54710 fire equipment e-mail:[email protected], [email protected] APK Savid-Astyk Kaidar T. 475005, Kokshetau city, post-harvest grain LLP. Islyamov 5 Pravda str. processing, grain T.(31622) 60110, 65991, storage; flour, groats f.60314 and mixed fodder production Dairy Factory Dulat N. 475000,Kokshetau city, dairy produces LLP Zhaksylykov District New Meat Packing. stocking, processing Tel./fax(31622) 71088, and sales e-mail:[email protected] Igilik JSC 475015, Kokshetau city, meat processing District New Meat Packing. Tel.(31622) 71378,70025, f. 71407 Kaz Sabton Franc E. 474456, Akmola oblast, extraction CJSC Malec Stepnogorsk city, District 4, of uranium ore, build. 2, mineral fertilizers, t. (31645) 91002, sulphuric acid f. 91016 production Vasilkovsky Hasen K. 475000, Kokshetau city, gold ore processing, GOK OJSC Absalyamov 29 "b" Gorky str., cathodic gold t. (31622) 55557,55547, production f. 55544, e-mail: [email protected] GMK Kazakhaltyn Kanat Sh. 474456, Akmola oblast, gold ore processing OJSC Asaybaev Stepnogorsk city, t. (31645) 91350,91660, f. 91660 Stepnogorsky Anatoly I. 474456,Akmola oblast, fabrication Bearing Factory Tomilov Stepnogorsk city, of roller bearings CJSC t. (31645) 59929,50959, for railway transport f. 59929 Herbicides Bayrzhan S. -

Deposits of the Hydrocarbon Raw Materials of the Republic of Kazakhstan, Where It Is Possible to Introduce a Microbiological Method for Stimulating the Formation

E3S Web of Conferences 280, 01002 (2021) https://doi.org/10.1051/e3sconf/202128001002 ICSF 2021 Deposits of the hydrocarbon raw materials of the Republic of Kazakhstan, where it is possible to introduce a microbiological method for stimulating the formation Olga Kuderinova1,*, Makhambet Shmanov1, and Mykhailo Filatiev2 1Karaganda Technical University, Development of Mineral Deposits Department, 56 N. Nazarbayev Str., 100027, Karaganda, Republic of Kazakhstan 2Volodymyr Dahl East Ukrainian National University, 59a Central Ave., Severodonetsk, 93406, Ukraine Abstract. The article is devoted to the analysis and systematization of data on hydrocarbon deposits in the Republic of Kazakhstan, highlighting those aspects that will allow the use of this method. The microbiological method of exposure refers to the chemical methods of the tertiary stage of development of oil reservoirs. It has already proven its effectiveness in highly depleted, waterflooded formations with irregular, diffuse oil saturation. Its main advantages are its relative cheapness, it does not require additional equipment during injecting of the microorganisms into the reservoir, and for their nutrition, as a rule, food industry waste is used, and its implementation cannot cause harmful effects on the environment. Also, a fairly extensive database was compiled, according to which various classifications of the republic's deposits were created. 1 Introduction removed, plus gases that can be extremely hazardous to health will be released. And chemical solutions can The purpose of the study was to identify the parameters permanently poison underground waters, which will needed for the introduction of the method of entail the death of all flora on the surface. microbiological influence on oil reservoirs, justification of the need for its use, as well as collection, analysis and systematization of data on all known this type deposits of 2 About the method of the the republic. -

Access to Drinking Water and Sanitation in the Republic of Kazakhstan

Committee for Water Resources Ministry of Agriculture of the Republic of Kazakhstan UNDP Project National Plan for Integrated Water Resources Management and Water Efficiency in Kazakhstan RepORT AcceSS TO DrinkinG WATer and SaniTATION in THE RepuBLic OF KAZakHSTan January 2006 Foreword Supplying population of the Republic of Kazakhstan with adequate quality drinking water is one of the priority directions of the social-economic development of the country. For Kazakhstan the Millennium Development Goals are the long-term goals, which are closely related to the National Development Strategy “Kazakhstan-2030”. The problem of supply of population with drinking water is reflected in such national documents as the Conception of the Water Economic and Political Sector Development of the Republic of Kazakhstan until 2010, the Strategy for Industrial and Innovation Development of the Republic of Kazakhstan for 2003-2015, as well as the Water Code of the Republic of Kazakhstan. Kazakhstan carries out a systematic work on water supply and sanitation in the framework of the sectoral Program “Drinking water” and the National Program on Development of Rural Territories. Under these programs the construction and reconstruction of the water supply systems in urban and rural areas is carried out. For the next 10 years of the program implementation 115 billion tenge are planned to be allocated from the republican budget. At the same time the factors inhibitory to stable and successful programme implementation are the following: a high level of deterioration of water supply networks and units, insufficient development and equipment of the water pipes traffic departments, as well as insufficiency in reliable official data on the accessibility of drinking water to population of Kazakhstan.