Policy for Prevention of Money Laundering & Combating The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sr. No. Boid Name Bankacnum Bankname Reject Reason 1

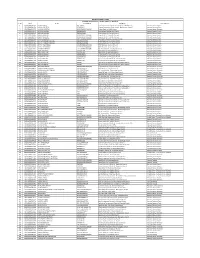

ORIENTAL HOTELS LIMITED Dividend Rejected List as of 01 Nov, 2019 ( F.Y. 2073/074) Sr. No. BoId Name BankAcNum BankName Reject Reason 1 1301160000055735 AALOK SUBEDI 001-2049PY Century Commercial Bank Ltd.- Putalisadak (HO) Branch Account Doesnot Exists. 2 1301480000091404 AARJYA SHRESTHA 0550003841 Century Commercial Bank Limited.-Manbhawan Branch 2 Account Doesnot Exists. 3 1301390000034276 AAVISHKAR REGMI 00101000026431000002 Prabhu Bank Ltd.-Main Branch Account Name Mismatch. 4 1301120000542574 ABHISHEK BAGALE 008008009450 Sunrise Bank Ltd.-Kalimati Branch Account Doesnot Exists. 5 1301120000542574 ABHISHEK BAGALE 008008009450 Sunrise Bank Ltd.-Kalimati Branch Account Doesnot Exists. 6 1301220000008452 ABHUSANI BHUJU 00000000181110005343 Laxmi Bank Ltd.-Lagankhel Branch Account Doesnot Exists. 7 1301220000008452 ABHUSANI BHUJU 00000000181110005343 Laxmi Bank Ltd.-Lagankhel Branch Account Doesnot Exists. 8 1301120000037386 ABISHA KANSAKAR 01711100022841000001 Jyoti Bikash Bank Ltd.- Sundhara Branch Account Doesnot Exists. 9 1301070000007664 ACHYUT PRASAD PYAKHUEL 012005011206866 Everest Bank Ltd.-Pulchowk Branch Account Doesnot Exists. 10 1301070000007664 ACHYUT PRASAD PYAKUREL 012005011206866 Everest Bank Ltd.-Pulchowk Branch Account Doesnot Exists. 11 1301470000028980 ACHYUT RAJ KHANAL 17020600183647000001 NMB Bank Ltd.-Chabahil Branch Account Doesnot Exists. 12 1301470000028980 ACHYUT RAJ KHANAL 17020600183647000001 NMB Bank Ltd.-Chabahil Branch Account Doesnot Exists. 13 1301120000514941 ADHATA SHRESTHA 1114016890524002NPR NIC -

English Annual Report 18-19.Pdf

ANNUAL REPORT 2018-19 TOGETHER WE RISE CONTENTS STRATEGIC REPORT An Overview (Vision, Mission, Objectives & Core Values) ................6 Bank’s Performance ..............................................................................................8 Financial Reviews ...................................................................................................9 Macroeconomic-Outlook ..................................................................................10 Customer Centric Business Model .............................................................. 13 CORPORATE GOVERNANCE REPORT OBJECTIVES Governance at A Glance ...................................................................................16 Board of Directors ............................................................................................... 18 The consolidated as well as standalone financial Profile of Directors ..............................................................................................20 statements, prepared in accordance with NFRS, remain the Chairman's Statement ...................................................................................... 23 The CEO’S Point of View ................................................................................. 25 primary source of communication with stakeholders. The Management Team .............................................................................................26 Department Heads .............................................................................................30 -

Sixty Years of Nepal Rastra Bank

Sixty Years of Nepal Rastra Bank Nepal Rastra Bank Kathmandu, Nepal April 2018 ©Nepal Rastra Bank, 2018 Address Central Office Baluwatar, Kathmandu Nepal Telephone: 977 1 4410386 Fax: 977 1 4410159 Sixty Years of Nepal Rastra Bank Published: April 2018 ISBN: Printed by UDAYA PRINT MEDIA PVT. LTD. Baneshwor-10, Kathmandu Phone No.: 01-5172093 [email protected] All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged. An electronic copy of this book is available at www.nrb.org.np. Foreword Nepal Rastra Bank (NRB) was established as the central bank of the country on April 26, 1956. During its six-decade long journey, NRB has made a significant progress in monetary, foreign exchange, and financial sectors. This publication 'Sixty Yeears of Nepal Rastra Bank' has been commissioned to commemorate NRB's reaching its sixty-year milestone by taking a walk down the memory lane of the major course of actions taken, progression of institutional development and evolution of its major functions. During the span of six decades, besides responsibly carrying out the traditional central banking roles and responsibilities, NRB has remained a firm anchor, constantly providing the solid foundation for ensuring monetary and financial stability. Over the years, monetary management has been streamlined and strengthened while the financial sector has been expanded and consolidated. For undertaking such responsibilities, NRB has transformed its organizational structure and management process for catalyzing the opportunities and proactively mitigating the challenges. Nepal Rastra Bank has sought to devise and implement appropriate and timely policy measures to promote financial sector development, orient monetary management towards improving price, balance of payments, financial sector and exchange rate stability, as well as facilitating the overall development of the economy. -

The Institute of Chartered Accountants of Nepal CA Member List from 2074-04-01 to 2075-03-21 Sno

The Institute of Chartered Accountants of Nepal CA Member List From 2074-04-01 to 2075-03-21 SNo. M.No. Name Address Phone Email 1 1 KOMAL BAHADUR CHITRACAR P.O.Box: 2043, Lalitpur SMPC, Ward No. 1, K.B. 01 5528671 [email protected] Chitrakar & Co., Jwagal, Lalitpur. 2 2 TIRTHA RAJ UPADHYAYA 124 Lal Colony Margh Lal Durbar, Kathmandu 01 4470964,4410927 [email protected] 3 3 KAUSHALENDRA KUMAR SINGH 158\18 kha shreeram marga Battisputali kathmandu 01 4472463 4 4 GOPAL PRASAD RAJBAHAK battisputali-9 surya bikram marga kathmandu. 4470612 [email protected] 5 5 SUNDAR MAN SHRESTHA P.O.Box 3102, Sundarman & Co., Pulchowk, Lalitpur, 01 5521804 sundarmans@gmail,com House No. 20/8, Kathmandu. 6 6 KISHOR BANSKOTA 46, New Plaza Road, Putalisadak, Kathmandu. 01 5250354 [email protected] 7 7 DR. GOVINDA RAM AGRAWAL KMPC-33, Gyaneshwor, Shruti Marg, House No: 52, 01 4413117 Ktm. 8 8 SHASHI SATYAL 58 Amal Margh Gairidhara, Kathamandu 01 4444084 [email protected] 9 9 PRADEEP KUMAR SHRESTHA Pradeep & Co., Sanepa, Lalitpur, P.O.Box 12143, Ktm. 01 5551126 [email protected] 10 10 PRATAP PRASAD PRADHAN Sanepa, Lalitpur, 01 5551126 [email protected] 11 11 MADAN KRISHNA SHARMA CSC & Co, 175 Gairidhara Marga, Gairadhara, Ktm 014004580 [email protected] 12 14 JITENDRA BAHADUR RAJBHANDARY POB No. 23725, Sherpa Mall 2nd Floor, Durbar Marga 01 4228352, 4247177 [email protected] Kathmandu. 13 16 DHRUBA NARAYAN KARMACHARYA Kathmandu MPC, Ward No. 32, Saraswati Marga, 01 4602357 [email protected] Koteshwor, House No. -

Stimulating Demand and Designing Financial Literacy Campaign to Increase Sustainable Access to Finance in Nepal

STIMULATING DEMAND AND DESIGNING FINANCIAL LITERACY CAMPAIGN TO INCREASE SUSTAINABLE ACCESS TO FINANCE IN NEPAL Shriju Dhakal Rimal DAAYITWA SUMMER FELLOW 2016 WITH NEPAL RASTRA BANK List of figures…………………………………………………………………………………………………………. Pg. Figure 1: Growth of Financial Institutions…………………………………………………………………….4 Figure 2: Financial Inclusion…………………………………………………………………………………………6 Figure 3. Financial literacy strategy…………………………………………………………………………….10 List of Tables Table 1. Number of Branches of Banks anD Financial Institutions………………………………..5 Acknowledgement I woulD like to extenD my gratituDe to Daayitwa for giving me an opportunity to be part of the fellowship program anD Nepal Rastra Bank for allowing me to work unDer their guiDance. First of all, I woulD like to thank the Daayitwa team anD specially my mentors Manoj anD Prakriti who guiDeD me throughout the research. BesiDes I woulD also like to thank Mr. Trilochan Pangeni, Mr. Gunakar Bhatta, Mr. Bhubanesh Pant, Mr. Ram Hari Dahal, Mr. SuboDh Man Shrestha, Mr. Deepak Kc anD Mrs. Asmita Gorkhali. Their faith in me as a Daayitwa fellow anD willingness to help was instrumental for conDucting this research. BesiDes them, all the wonDerful anD supportive staff at NRB who were so welcoming. 2 Table of Contents Pg. 1.Introduction…………………………………………………………………………………………………………………1 1.1 BackgrounD………………………………………………………………………………………………………………….1 1.2 Rational anD Significance of the stuDy………………………………………………………………………….2 2.Methodology……………………………………………………………………………………………………………….3 3.Scenario of Financial Inclusion -

Gimlette's Account of Nepal

Even as the~ i uslice Kh!l n hun drccl cl.t ~ unc~rtam whl held or not \ of the clc~.: ur needs a \lab l ramlc:r ol d1 rocked the 1 third tran\kl of one hunu '>lrong pnllut \ laoJSl wllll:h for l J\ , thl l I ikcly ~.:r~.:.l L I muaunn hw t govcrntnlnt' .l'>l:d 1)11 CC!nll1l, d gnvcrnmc.;nLc in ~ovcm hc r r~.:ma l n'> hk,d, at Lh~.: p11nr I c.t\'lng t en l:lWcr '>tory I pu hi n eel Ul rcccn •t·~ .1 l. 1 r~ \)u,~~'-" . " " " Dcsp1Lc '>l'Vl:r! scuor h,l., t! m.tint.un \t·p~ •\long with m.tnagcmcnl 1 t his wcc.;k. t~ l ' and ecology, ( 'cp,d, what U 1 the U J \,~ ignor,tn( dJsasterc, ~~ Keshab Po Editor iA UIC1 'CrriltSCi) De~ ffll. NEPAL INVESTMENT BANK LTD. tfru ( y a 1'/epa ( i (]J an l{. =---------- -------- From The Editor SPOT HL IG TFORTNIGHTLy Lven as the government led hy chid JUstice Khil RaJ Regmi completed JL'> hundred Jay~ 1n offrcc, ll ic, '>till uncenam \\ hethcrthc clccuonc, \\'Ill he held or not. \\'1th the .tnnnunu:mcnt of thL clet:llon date, the go\'Crnment need~ d. ~lo.~hlc Cl\'d ~ei'\ ' ICL But the lran~lc r ol dn=cns of ~ct:retanc<, has rot:ked the bure<\UcraL) I h1s 1~ the third lran~fcr 111 ,, row rn JU'>l.tm..lucr nf one hundred d..1ys 1\'> there I'> a strong political lorL'l under the t PN \ lan tsl whtch I'> opposi ng thl.' elect inns for(.,\ , t he h o~L i lc <.:iv tl scrdee \\'il l l1i<el) c reat e cl more u nI a Vnt'<t hlc 'illuauon lor the govern men L. -

List of Inactive Accounts for 10 Years and Above

LIST OF INACTIVE ACCOUNTS FOR 10 YEARS AND ABOVE S.N. ACCOUNT HOLDER’S NAME ACCOUNT NUMBER ADDRESS 1 SHREE GANESHAYA NAMO 01450001000001 KATHMANDU 2 SUNIL KUMAR BANSAL 01450001000060 KATHMANDU 3 ASHIT MEHTA 01450001000080 INDIA 4 SUCHITRA MAN SHAKYA 01450001000077 JWAGAL,LALITPUR 8/330, PYUKHA, NEWROAD, 5 SANJAY KUMAR SUREKA 01450101000027 KATHMANDU-31 6 BIJAY BAHADUR SHRESTHA 01450001000090 KATHMANDU 7 RAM NARAYAN SAH KALWAR 01450001000028 KANKAPUR-02,RAUTHAT RAJA KRISHNA / RAJENDRA BDR 8 / CHANDRA BKT / BIRENDRA / 01450001000035 GUCHATO-8/378,KATHMANDU RAJESHOWRI DUBACHOUR- 6, 9 KHADKA RAJ BHARATI 01450001000044 SINDHUPALCHAUK 10 SANJAY KUMAR AGRAWAL 01201101000063 BIRGUNJ-13,PARSA 11 BHAWANA DANGOL 01450001000050 KATHMANDU-21 12 SUSHMA SHRESTHA 01450001000092 BHAKTAPUR-07 WARD NO-11, 13 SABITA SAPKOTA 01450001000109 NAWALPUR,HETAUDA, MAKWANPUR 14 MAHESH PRASAD PARAJULI 01450001000105 BADHARA-09 WARD NO 07, CHITLANG, 15 LAXMI BALAMI 01450001000113 MAKWANPUR WARD NO.-19, NAGUWA, 16 PASHUPATI PLASTIC UDHYOG 01420001000050 BIRGUNJ 17 KESHAB PRASAD ADHIKARI 01450001000003 KUMARWARTI-06, NAWALPARASI 18 MANITA SINGH 01450001000126 WARD NO.22, KATHMANDU INTERACTIVE INVESTMENT & 19 01420001000019 WARD NO.11, KATHMANDU SECURITIES PVT. LTD. WARD NO-19, EKHA TOLE, 20 ECHHA TAMRAKAR 01450501000014 LALITPUR S.N. ACCOUNT HOLDER’S NAME ACCOUNT NUMBER ADDRESS WARD NO.32, DILLIBAZAR, 21 A.N. SECURITIES PVT. LTD. 01420001000006 KATHMANDU WARD NO1, TANKISINUWARI, 22 EKTA SHARMA 01450501000006 MORANG 23 UMDA BASNET 01450501000002 BALUWATAR, KATHMANDU 24 -

China Oil Futures Are Here: What You Need to Know

CHINA MOVE | Page 3 Q1 HIT | Page 10 First steps to Barclays to pay for oil in pay $2bn yuan in 2018 fi ne in US Friday, March 30, 2018 Rajab 13, 1439 AH LOSING MOMENTUM: Page 12 Consumer spend GULF TIMES up slightly in US; jobless claims BUSINESS at 45-year low Banks, industrials help QSE-listed firms enhance 2017 profitability By Santhosh V Perumal in the corresponding period of the The sector, whose share was 55% in listed entities, witnessed its net profit profitability, saw its index shrink 15.85% listed companies, recorded a 18.16% Business Reporter previous year. The Qatar Index, the the overall net profitability, witnessed drop 3.71% to QR3.98bn compared to year-to-date ended December 31, 2017. shrinkage in cumulative net profit to headline index of the bourse, fell more its index trim 7.9% year-to-date ended more than 25% slump a year ago. However, the insurance sector, which QR1.53bn against a 17.27% fall in the than 18% year-to-date ended December December 31, 2017. The sector, which constituted 10% of has five listed companies, reported previous year. The improved earnings performance 31, 2017. The industrials sector, which has nine the overall net profitability, witnessed the maximum decline of 39.83% in The sector, which contributed about 4% of the banking and industry helped The listed companies’ net profit listed constituents, saw its cumulative its index register a 14.66% shrinkage cumulative net profit to QR0.84bn in to the overall net profitability, saw its Qatar Stock Exchange-listed companies cumulated at QR38.56bn during 2017 net profit grow 5.99% to QR7.43bn year-to-date ended December 31, 2017. -

Political Economy in Transition Docking Nepal's Economic Analysis

NEPAL ECONOMIC FORUM ISSUE 44 | MARCH 2021 POLITICAL ECONOMY IN TRANSITION DOCKING NEPAL'S ECONOMIC ANALYSIS DOCKING NEPAL’S ECONOMIC ANALYSIS ISSUE 44 | MARCH 2021 FACTSHEETNEPAL FACTSHEET KEY ECONOMIC INDICATORS GDP (2021) *** USD 30.6 billion GDP growth rate (%)*** 0.2% GNI (PPP, 2021) *** USD 3610 Inflation (y-o-y) **** 4.05% Gross Capital Formation as of 2021, preliminary 50.2% Agriculture sector (% share of GDP)** 27.65% estimate (% of GDP) *** HDI * 0.602 Industry sector (% share of GDP)** 14.27% Rank 142 Service sector (% share of GDP)** 58.08% *HDI figure from Human Development Report of the UNDP-2020 ** Based on Nepal Rastra Bank's 12 months data of 2019/20 *** Based on World Bank Data ****Based on 4 months' Data (2020/21) CONTENTS MARCH 2021 | ISSUE 44 CONTENTS NEPAL FACTSHEET 1 EDITORIAL 4 1 GENERAL OVERVIEW 5 Political Overview 6 International Economy 8 2 MACROECONOMIC OVERVIEW 10 3 SECTORAL REVIEW 13 Agriculture 14 Energy 16 Infrastructure 17 Telecommunications 20 Real Estate 23 Education 24 Health 27 Tourism 29 Trade and Debt 31 Foreign Aid 34 Remittance 36 Environment 39 4 MARKET REVIEW 40 Financial Market 41 Capital Market 45 5 SPECIAL SECTION: POLITICAL ECONOMY IN TRANSITION 48 ENDNOTES 57 NEF Profile 61 Issue 44: March 2021 Executive Board Members: Publisher: Nepal Economic Forum Alpa B. Shakya Website: www.nepaleconomicforum.org Chandni Singh Shayasta Tuladhar P.O Box 7025, Krishna Galli, Lalitpur — Sudip Bhaju 3, Nepal Sujeev Shakya Phone: +977 1 554-8400 Email: [email protected] Advisory Board: Arnico Panday Contributors: Kul Chandra Gautam Nasala Maharjan Mahendra Krishna Shrestha Raju Dhan Tuladhar Prativa Pandey Sugam Nanda Bajracharya Shankar Sharma Sambriddhi Acharya Shraddha Gautam Sampada Shah Sneh Rajbhandari Sarik Koirala Tanushree Agrawal Senior Distinguished Fellows: Bibhakar Shakya Design & Layout: Giuseppe Savino Thuprai Solutions Suman Basnet [email protected] Senior Fellows: This issue of nefport takes into account Apekshya Shah news updates from November 16 2020 Ashraya Dixit to February 16 2021. -

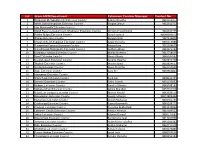

S.N Branch/RO/Department Extension Counter Manager Contact No

S.N Branch/RO/Department Extension Counter Manager Contact No 1 Biratnagar Metropolitan City Extension Counter Rubina Shrestha 9841562477 2 Itahari Sub-Metropolitan Extension Counter Sangita Dhakal 9842340732 3 Ilam Municipality Extension Counter 4 lnland Revenue Department, Bhadrapur Extension Counter Nirdesh Prasad Dahal 9842637735 5 Phidim Malpot Extension Counter Narad Tumrok 98049999079 6 Dharan Extension Counter Sanyam Shah 9829316808 7 Dharan Sub- Metropolitan Extension Counter Sawal Shrestha 9804359088 8 Purwanchal Campus Extension Counter Kabita Bista 9852076625 9 Suryabinayak Municipality Extension Counter Sadhana Bhuju 9843073189 10 Bhaktapur- Malpot Extension Counter Malika Shrestha 9813758535 11 Byasi Extension Counter Shova Dhanju 9849347687 12 Neupanegaun Extension Counter Sangita Shyama 9843453750 13 Tikathali Extension Counter Meenu Suwal 9818824657 14 Sirutar Extension Counter Navin Shrestha 9841159590 15 Bode Extension Counter Sony Giri 9849966824 16 Narayantar Extension Counter 17 Shivachowk Extension Counter Rajib Giri 9808323105 18 Danchhi Extension Counter Sushil Subedi 9851195662 19 Mulpani Extension Counter Sumitra Ghimire 9843748181 20 Mahadevsthan Extension Counter Sabina Bhandari 9857017318 21 Nepal Law Campus Extension Counter Monica Poudel 9843936559 22 Baluwakhani Extension Counter Seema Adhikari 98612804444 23 Manamaiju Extension Counter Dinesh Maharjan 9803761195 24 Goldhunga Extension Counter Sujata Gotame Kc 9843296171 25 Phutung Extension Counter Prasanna Budhathoki 9841315699 26 Loktantrik Chowk Extension -

Shareholder No. Bankacnum Bankname Reject Reason 1

NIBL Samriddhi Fud Dividend Rejected List as of 5th March, 2021 ( F.Y. 2074/075) BoId/ Shareholder Sr. No. BankAcNum BankName Reject Reason No. 1 1301010000037836 210100000338524 Bank of Kathmandu Ltd.-Thamel Branch Account Freezed. 2 1301010000076390 03300033326011 CIVILBankLtd.-MainCTC Account Name Mismatch. 3 1301010000104995 0341007977017 CIVIL Bank Ltd.-Kuleshwor Branch Account Doesnot Exists. 4 1301010000118881 21415241401126 Nepal SBI Bank Ltd.-Dallu Branch Account Doesnot Exists. 5 1301010000118894 00403469101 Siddhartha Bank Ltd.- Kantipath Branch Account Doesnot Exists. 6 1301010000164111 00800800642LK Sunrise Bank Ltd.-Kalimati Branch Account Doesnot Exists. 7 1301020000000395 00201000159650000001 Excel Development Bank Ltd.- Birtamode Main Branch Account Doesnot Exists. 8 1301020000008702 0240050045002 Mega Bank Nepal Ltd.- Maitidevi Branch Account Name Mismatch. 9 1301020000045333 0207010001982 Global IME Bank Ltd.-New Road Branch debit freeze 10 1301020000060022 02-116-00185168-01-1 Agriculture Development Bank Ltd.-Lagankhel Branch Account Doesnot Exists. 11 1301020000095309 56235244932012 Machhapuchhre Bank Ltd.-Chabahil Branch Account Doesnot Exists. 12 1301020000163725 2461060907563000001 Nepal Bank Ltd.-Koteshwor Branch Account Doesnot Exists. 13 1301020000194591 020100000051 Bank of Kathmandu Ltd.-Thamel Branch Account Doesnot Exists. 14 1301040000003449 1810007501283 Nabil Bank Ltd.-Tripureshwar Branch Account Doesnot Exists. 15 1301040000003643 03498gb Nepal Bangladesh Bank Ltd.- Lalitpur Branch Account Doesnot Exists. 16 1301040000003658 03464gb Nepal Bangladesh Bank Ltd.- Lalitpur Branch Account Doesnot Exists. 17 1301040000013489 0690421495214001 Sunrise Bank Ltd.-Kamalpokhari Branch Account Freezed. 18 1301040000013951 037122000676524 Bank of Kathmandu Ltd.-Bhaktapur Branch Account Freezed. 19 1301040000025473 007000220940-A Nepal Credit & Commerce Bank Ltd.-New Road Branch Account Doesnot Exists. 20 1301040000091049 013013000032508 Nepal Credit & Commerce Bank Ltd.-New Baneshwor Branch ID Account Doesnot Exists. -

Open Market Operations Statistics

GOVERNMENT SECURITIES AND OPEN MARKET OPERATIONS STATISTICS As on Baisakh 2078 (May 2021) NEPAL RASTRA BANK PUBLIC DEBT MANAGEMENT DEPARTMENT KATHMANDU, NEPAL Phone No: 4419805/6/7 Ext no. 222 Fax No: 4412306 CONTENTS Table Particular Page No. 1 Domestic Debt Liability of the Government of Nepal 1 2 Ownership Structure of Government Securities (Summary) 2 3 Ownership Structure of Government Securities (Detail) 3 4 Repayment Schedule of Government Securities 4 5 Ownership Structure of 91- Days Treasury Bills Issued Through Primary Market 5 6 Ownership Structure of 28 &182 Days- Treasury Bills Issued Through Primary Market 6 7 Ownership Structure of 364-Days Treasury Bills Issued Through Primary Market 7 8 Ownership Structure of Treasury Bills of NRB Secondary Market (Pure Secondary) 8 9 Ownership Structure of Treasury Bills (Summary) 9 10 Ownership Structure of Development Bonds 10 11 Ownership Structure of Citizen Saving Bonds 11 12 Ownership Structure of Foreign Employment Saving Bonds 12 13 Government Securities Held by NRB 13 Interest/Discount Amount Received from Government for Different Securities in Current 14 14 Fiscal Year ( 2077/78) 15 Repayment of Principal Amount of Government Securities in Current Fiscal Year (2077/78) 15 16 Government Securities Issued in Current Fiscal Year (2077/78) 16 17 Open Market Operations (Outright Sale) in Current Fiscal Year (2077/78) 17 18 Open Market Operations (Outright Purchase) in Current Fiscal Year (2077/78) 17 19 Open Market Operations (Repo Regular) in Current Fiscal Year (2077/78) 18 20 Open Market Operations (Repo Overnight) in Current Fiscal Year (2077/78) 18 21 Open Market Operations (Reverse Repo) in Current Fiscal Year (2077/78) 19 22 Open Market Operations (Deposit Collection IRC) in Current Fiscal Year (2077/78) 20 23 Open Market Operations (Deposit Collection Regular) in Current Fiscal Year (2077/78) 20 24 Standing Liquidity Facility (SLF) Transactions in Current Fiscal Year (2077/78) 21 Table 1 Domestic Debt Liability of the Government of Nepal As on Baisakh 2078 (May 2021) S.N.