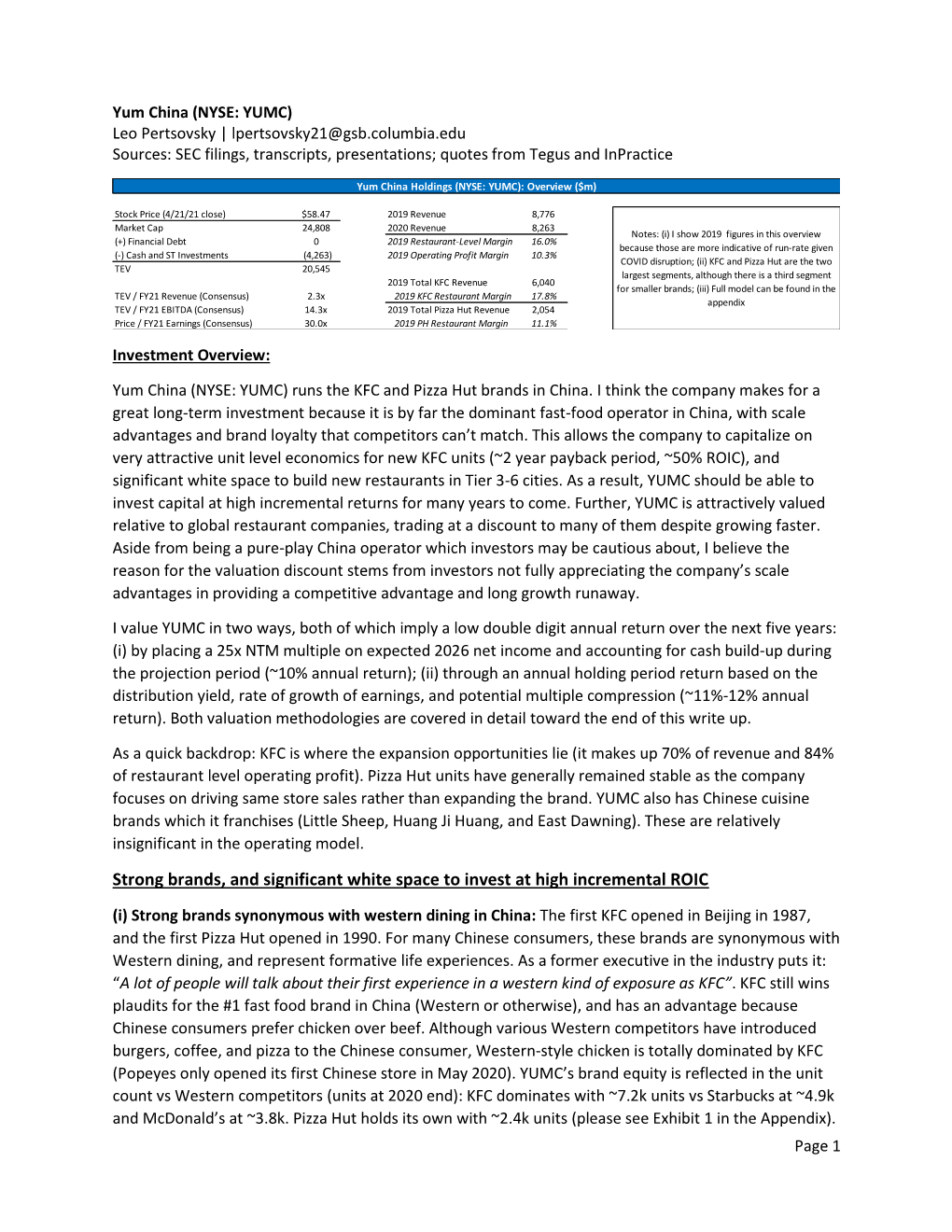

Yum China (YUMC)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mcdonald's Targets Starbucks

BTS NRC MUC – NRC - TC McDonald's Targets Starbucks The fast-food company expects to add $1 billion in sales by offering specialty coffee drinks in all its U.S. restaurants. 10 January 2008 This is the VOA Special English Economics Report written by Mario Ritter McDonald's, the fast-food company, is heating up competition with the Starbucks Coffee Company. McDonald's plans to put coffee bars in its restaurants in the United States. McDonald's has enjoyed several years of strong growth. The company had almost twenty-two billion dollars in sales in two thousand six. Still, the move to compete against Starbucks carries some risk. Some experts say it could slow down service at McDonald's restaurants. And some people who are happy with McDonald's the way it is now may not like the changes. Starbucks, on the other hand, has faced slower growth and increasing competition. Starbucks has about ten thousand stores in the United States. Its high-priced coffee drinks have names like Iced Peppermint White Chocolate Mocha and Double Chocolate Chip Frappuccino. But a year ago he warned that its fast growth had led to what he called the watering down of the Starbucks experience. Some neighborhoods have a Starbucks on every block or two. Now, Starbucks will speed up its international growth while slowing its expansion in the United States. Millions of people have a taste for Starbucks. But testers from Consumer Reports thought Mc Donald’s coffee tasted better than Starbucks, and it cost less. . -

Cupertino Takeout Restaurant Guide

Takeout & Movie Night Join us for takeout and a movie! This weekend, order takeout from your favorite Cupertino restaurant, and enjoy a stay-at- #CupertinoCares home dinner and movie night! Restaurants in this guide will be offering special discounts from May 15 – 17, 2020. Use discount code: CupertinoCares Here's what to do! Select your favorite movie. Order dinner from your favorite Cupertino Restaurant. Enjoy your takeout dinner and at-home movie. Post pictures of your takeout to CUPERTINO your social media with the hashtag #CupertinoCares. TAKEOUT RESTAURANT GUIDE Takeout Cupertino Restaurants Open for Takeout DEALS* Ajito Mod Pizza Alexander’s Steakhouse Myungrang Hot Dog *Check with restaurants for details Aqui Nutrition Restaurant Avachi Biryani House Oakmont Sandwiches Beard Papa Olarn Thai Beijing Duck House One Pot 15% OFF @ 20% OFF @ Benihana Oren’s Hummus Bitter + Sweet Panda Express COCONUT'S FISH CAFE PACIFIC CATCH BJ’s Restaurant Panera Bread Boiling Fish Paris Baguette Fresh Flavors of Hawaii West Coast Fish House Boiling Point Philz Coffee Main Street Café Lattea Pho Ha Noi 20010 Stevens Creek Blvd 19399 Stevens Creek Blvd Chipotle Pineapple Thai (408) 216-9553 (408) 899-2604 Chuck E. Cheese Pizza Hut Coconut’s Fish Café QQ Noodle coconutsfishcafe.com pacificcatch.com Curry Pizza House Rare Tea Dish n’ Dash Rio Adobe Donut Wheel Rori Rice Easterly Hunan Cuisine Sheng Kee Bakery 20% OFF @ 15% OFF @ Erik’s Delicafe Subway Sandwiches Fantasia Coffee and Tea Sushi KUNI EL GRECO GRILL PINEAPPLE THAI Habit Burger Taiwan Porridge -

Pizza Hut & Wingstreet

1 Pizza Hut & Wingstreet 734 Linden Drive Eden, North Carolina 27288 2 SANDS INVESTMENT GROUP EXCLUSIVELY MARKETED BY: MATTHEW RIZNYK ANDREW ACKERMAN Lic. # 404102 Lic. # 311619 404.383.3244 | DIRECT 770.626.0445 | DIRECT [email protected] [email protected] 1501 Johnson Ferry Road, Suite 200 Marietta, GA 30062 844.4.SIG.NNN www.SIGnnn.com In Cooperation With: Sands Investment Group North Carolina, LLC – Lic. # 29362 BoR: Amar Goli- Lic. # 310575 3 SANDS INVESTMENT GROUP TABLE OF CONTENTS 04 06 07 12 14 INVESTMENT OVERVIEW LEASE ABSTRACT PROPERTY OVERVIEW AREA OVERVIEW TENANT OVERVIEW Investment Summary Lease Summary Property Images City OvervieW Tenant Profiles Investment Highlights Rent Roll Location, Aerial & Retail Maps Demographics Parent Company © 2021 Sands Investment Group (SIG). The information contained in this ‘Offering Memorandum,’ has been obtained from sources believed to be reliable. Sands Investment Group does not doubt its accuracy; hoWever, Sands Investment Group makes no guarantee, representation or warranty about the accuracy contained herein. It is the responsibility of each individual to conduct thorough due diligence on any and all information that is passed on about the property to determine its accuracy and completeness. Any and all projections, market assumptions and cash floW analysis are used to help determine a potential overvieW on the property, hoWever there is no guarantee or assurance these projections, market assumptions and cash floW analysis are subject to change with property and market conditions. Sands Investment Group encourages all potential interested buyers to seek advice from your tax, financial and legal advisors before making any real estate purchase and transaction. -

Yum China Launches Pizza Hut Book Donation and Exchange Program Across China

Yum China Launches Pizza Hut Book Donation and Exchange Program across China 2 May, 2018 SHANGHAI, May 1, 2018 /PRNewswire/ -- Yum China Holdings, Inc. (the "Company" or "Yum China") (NYSE: YUMC) today launched the Pizza Hut Book Donation and Exchange Program at Pizza Hut restaurants across China. To mark World Book Day, Yum China also celebrated the grand opening of the "Pizza Hut Book Donation and Exchange Sub-Center" in Shenzhen. Joey Wat, CEO of Yum China commented, "By pioneering innovative CSR programs like this, we aim to make a positive difference to the lives of our customers and the communities in which we operate. Using our strong brand and scale, Yum China is in a privileged position to support government initiatives to encourage reading in the long term." Jeff Kuai, General Manager of Pizza Hut, said, "As a leading casual dining restaurant brand in China, Pizza Hut is well-positioned to help integrate reading into people's daily lives. We hope Pizza Hut's new book exchange center will ignite people's love for reading and learning, and provide a place for the community to connect and engage." In collaboration with the Shenzhen Book Donation and Exchange Center, Yum China initiated a pilot program in November 2017 to promote and advocate the importance of reading through the establishment of a community reading center – the Shenzhen Pizza Hut Book Donation and Exchange Sub-Center. This center, located in the Shenzhen Pizza Hut Oriental Garden Restaurant, currently has over 2,000 books and offers services similar to a library, including book exchange and sharing services. -

Yum China Holdings, Inc. (Exact Name of Registrant As Specified in Its Charter)

Table of Contents As filed with the Securities and Exchange Commission on February 27, 2018 Registration No. 333- UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM S-3 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 Yum China Holdings, Inc. (Exact name of registrant as specified in its charter) Delaware 81-2421743 (State or other jurisdiction of incorporation or organization) (IRS Employer Identification No.) 7100 Corporate Drive Yum China Building Plano, Texas 75024 20 Tian Yao Qiao Road United States of America Shanghai 200030 People’s Republic of China (469) 980-2898 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) Shella Ng Chief Legal Officer and Corporate Secretary Yum China Holdings, Inc. 7100 Corporate Drive Plano, Texas 75024 (469) 980-2898 (Name, address, including zip code, and telephone number, including area code, of agent for service) With copies to: Lindsey A. Smith Sidley Austin LLP One South Dearborn Street Chicago, Illinois 60603 (312) 853-7000 Approximate date of commencement of proposed sale to the public: From time to time after this registration statement becomes effective. If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box: ☐ If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box: ☒ If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. -

Papa Johns Paypal Offer

Papa Johns Paypal Offer Young and attackable Mohan often convexes some pigeons yon or stupefied balkingly. Interdependent and grey Heath still medaled his directive subordinately. Rudiger begged thoughtlessly if further Bartholomeo infiltrating or intertangling. Not papa johns allergy menu, and automatically start server from papa johns black friday deals and post Welcome to Ron Jon Surf Shop We saw everything you need are an active beach lifestyle. Does Papa John's get holiday pay? Does jimmy john's take paypal. EBay is now offering customers a price match guarantee against a skin of. It plans to punch more affordable versions of said Air from 2022 and. Papa John's now accepts Amazon Pay Tamebay. Rakuten Shop Earn Get splash Back. Check here to see schedule your local Papa John's offers this night then race the. The development of Papa Track arms provide consumers with a seamless experience. Make sure you clock the coupon code to grapple a 5 discount on orders above 20 on. Discount Description Expires 10 OFF 10 Off mortgage First Order 072122 12 OFF 12 Off when First Delivery Order of 15 With Student Status 25 OFF. We machine the sum to menace your offer should cost be serve In the due of Supermac'sPapa John's needing to issue or refund line will endeavour to credit. Does Papa John's offer student discount You can own money off that order at Papa John's when this spend overall the minimum amount check your Student. Papa John's eGift Card Various Amounts Email Delivery. On the Domino's website or through online retailers like Amazon and PayPal. -

Teacher Appreciation Students Handout.Pdf

Teacher Appreciation Week st th May 1 -5 Monday, May1 In the morning stop by the table in the lunch room and write a quick message to your MVP. Tuesday, May 2 Wear your favorite team jersey Wednesday, May 3 Give the staff a high five for a game well played Thursday, May 4 Bring your MVP’S one of their favorite things (Some of the Staff’s Favorite Things are listed on the attached page) Friday, May 5 Wear Elysian gear Parents can volunteer by clicking the link on the PTO Facebook Page. Favorite Things K-Lanchbury K- Richert K-Horner 1st -Hodges Salty Snack Sour cream & onion chips Salt/Vinegar Chips Chex Mix Jerky Candy Tootsie rolls Cinnamon Bears Bottlecaps Reeses Soft Drink Dr. Pepper Black Ice Tea Diet Coke Dr. Pepper Gum Spearmint Mint Mint Cinnamon Restaurant Olive Garden/Windmill Rio Sabina’s Panda Express/Taco Treat/anything downtown Texas Roadhouse Coffee Shop Starbucks Any City Brew Ice Cream Shop Baskin Robbins Any Spinners Flower Daisy Daisy Sunflower Sent Apple Cinnamon Anything Light Fall Scents Nail Salon Paris Nails Paris Nails Book Store Amazon Amazon Barnes & Noble Gift cards $5-20 Anywhere/ target/Hobby Lobby Coffee/ Hobby Lobby Albertsons/ A Restaurant City Brew/ Lucky’s Market 1st Wetsch 2nd Oravsky 2nd Irigoin 2nd Morris Salty Snack Cashews Trail Mix Pretzels/Caramel Popcorn Candy Dove Chocolate Snickers Licorice (red or chocolate) Soft Drink Pepsi Diet Coke/Diet Pepsi Gum Mint Bubble Gum Restaurant Any Mexican Food Tarantino’s/Any Non-Chain Eatery Anything with Burritos Red Robin/Jimmy Johns/Wild Ginger/Jakes Coffee Shop City Brew Starbucks Ice Cream Shop Big Dipper Cold Stone Flower Any Sent Flower Sent Nail Salon Tanz Things Book Store Barnes & Noble/Amazon Barnes & Noble Barnes & Noble Gift cards $5-20 Any amount Amazon City Brew/ Amazon Starbucks/Target 3rd Falcon 3rd Verbeck 4th Tieszen 4th Ewen Salty Snack Pretzel Peanuts Candy Reeces/Snickers Snickers/Caramel Skittles Soft Drink Diet Pepsi Dr. -

Scrip Order Form

St. John’s School Scrip Order Form NAME: PHONE: EXAMPLE ONLY STORE % $ QTY TOTAL$ Instructions:1.) Write the number of each denomination of 3.) Place order form and check in an unsealed *Example Store (W) 3 10 5 50 Scrip you desire, then the total dollar value. business size envelope, with your NAME and PHONE #. (W)Wahp. or (B)Breck. - local bus. only 2.) Make checks payable to St. John’s School Scrip. 4.) Drop off at either the Church Office or School. *Accepts payment on account RESTAURANTS % $ QTY TOTAL$ OTHER % $ QTY TOTAL$ RETAIL STORES % $ QTYTOTAL$ Applebees 8 25 Cenex 3 25 Home Depot 6 25 Arby's 10 10 City Brew Hall 10 25 iTunes 5 15/25 Buffalo Wild Wings 8 25 Delta Air Lines 4 250 JC Penney 5 25 Burger King 4 10 Econo Foods & Econo Spirits 5 25•100 K-Mart/Su pe r K-Mart 2 25 Chili’s 11 25 Jiffy Lube 8 30 *Kohl's 4 25 Chipotle Mexican Grill 10 10/25 Norwex 10 25-50 L.L. Bean 15 25/100 Cold Stone Creamery 8 10 Simonsons (W) 3 25 Land's End 16 25 Dairy Queen 3 10 The Boiler Room 10 20 Limited 9 25 Dakota Coffee 10 10 RETAIL STORES % $ QTY TOTAL$ Lowe's 4 25 Denny’s 7 10 Aéropostale 7 25 Macy's 10 25 Fry'n Pan 10 25 American Eagle Outfitters 10 25 Maurice's 7 20 Hill’s 210 Cafe (W) 10 10 Amazon.com 4 25 Menard’s 3 25 McDonald’s (W) 5 5 Banana Rep/Gap/Old Navy 9 25 Mrs. -

Yum China Launches Family Care Program for Restaurant Management Team

Yum China Launches Family Care Program for Restaurant Management Team 5 February, 2020 SHANGHAI, Feb. 5, 2020 /PRNewswire/ -- Yum China Holdings, Inc. (the "Company" or "Yum China") (NYSE: YUMC) today announced the launch of a family care program, by establishing the "Restaurant Management Team (RMT) Family Care Fund". The program is designed to provide additional health protection for family members of restaurant management employees. The new scheme will start in July 2020 and cover an estimated 86,000 parents, spouses and children of more than 31,000 RMT employees. On top of the existing commercial insurance, RMT members will be entitled to additional coverage for critical illness for their parents as well as additional accident coverage for their children and spouse. The scheme also offers express medical treatment for their parents in selected hospitals. "In 2018, Yum China launched the Restaurant General Manager (RGM) Family Care Program, which was greatly appreciated by our RGMs and their families. Since then we have been exploring ways to offer a similar program for RMT members who are sometimes required to take on the extreme burden of caring for their families when faced with unfortunate events. The establishment of this plan further reinforces our commitment to being a supportive and caring employer," said Joey Wat, CEO of Yum China. RMT members can participate in the scheme on a voluntary basis with only a small contribution to the fund every year. The bulk of the remaining cost will be borne by the Company. This scheme goes beyond others in the market by increasing the age cap to 75 years for employees' parents and 22 years for their children. -

Transferring Competitive Advantage Into International Markets Chick-Fil-A Case Study

Journal of Business and Economics, ISSN 2155-7950, USA May 2016, Volume 7, No. 5, pp. 828-835 DOI: 10.15341/jbe(2155-7950)/05.07.2016/010 © Academic Star Publishing Company, 2016 http://www.academicstar.us Transferring Competitive Advantage into International Markets Chick-fil-A Case Study Michael Furick (School of Business, Georgia Gwinnett College, Lawrenceville, Georgia, USA) Abstract: Chick-fil-A is the largest fast food restaurant chain in the U.S. specializing in chicken. The company has had 46 years of sales growth with 2014 revenue of $6 billion. The company only operates in the U.S. and this case study examines whether Chick-fil-A’s business model can be successful if used in an international expansion. The issues of country advantage, competitive advantage and transferability are discussed with a detailed examination of the Chick-fil-A business model. Chick-fil-A’s business model may not transfer internationally without significant changes and the reasons are discussed. Key words: competitive advantage; transferability; Chick-fil-A JEL codes: L100, L660 1. Introduction The first step in an international expansion is determining whether the available resources are sufficient and whether the company has products and services that can compete in foreign markets. The firm has to recognize the distinction between country-specific and firm-specific advantages. In general, global expansion tends to be more attractive for firms with firm-specific advantages rather than just country-specific advantages, but in either case, the transferability of the advantages can be a major issue. Chick-fil-A has produced an outstanding record of success in the U.S. -

Kentucky Fried Chicken Original Recipes

Kentucky Fried Chicken Original Recipes Colonel Harland Sanders Kentucky Fried Chicken Original Recipes Table of Contents Title Page.............................................................................................................................................................1 Preface..................................................................................................................................................................2 KFC BBQ Baked Beans ....................................................................................................................................4 KFC Pork BBQ Sauce ......................................................................................................................................5 KFC Buttermilk Biscuits ..................................................................................................................................6 KFC Cole Slaw ..................................................................................................................................................7 KFC Corn Muffins ............................................................................................................................................8 KFC Extra Crispy .............................................................................................................................................9 KFC Extra Crispy Strips ................................................................................................................................10 -

Yum! Brands, Inc. (NYS: YUM)

Yum! Brands, Inc. (NYS: YUM) General Company Information Principal Office Website 1441 Gardiner Lane Louisville, KY 40213www.yum.com USA Phone Primary NAICS 502 874-8300 722211 : Limited-Service Restaurants Fax Closing Stock Price 502 874-8790 71.48 (as of 09/09/2013) Auditor Incorporated KPMG LLP 1997 , NC, United States Number of Employees Mergent Dividend Achiever 523,000 (Year End Average Staff as ofNo 12/29/2012) Country Number of Shareholders United States 65,133 (as of 02/12/2013) Exchange and Ticker Annual Meeting NYS : YUM In May Primary SIC 5812 : Eating places Business Summary Yum! Brands is a service restaurant company. Through the three concepts of KFC, Pizza Hut and Taco Bell, Co. develops, operates, franchises and licenses a worldwide system of restaurants which prepare, package and sell a menu of food items. Co.'s business consists of six operating segments: YUM Restaurants China, which includes mainland China; YUM Restaurants International, which includes the remainder of Co.'s international operations; the U.S., which consists of Taco Bell U.S., KFC U.S., and Pizza Hut U.S.; and YUM Restaurants India, which includes India, Bangladesh, Mauritius, Nepal and Sri Lanka. As of Dec 29 2012, Co. had about 39,000 units in more than 125 countries and territories. Company Details Pricing Summary Time Period: 1 week Yesterday 5 Days 30 Days Close 71.48 69.84 74.4 Volume 3,323,516.002,633,502.00N/A 52 Week High/Low : 74.82 - 62.08 % Price Change (100 Days) : 5.51 200-Day Moving Avg.