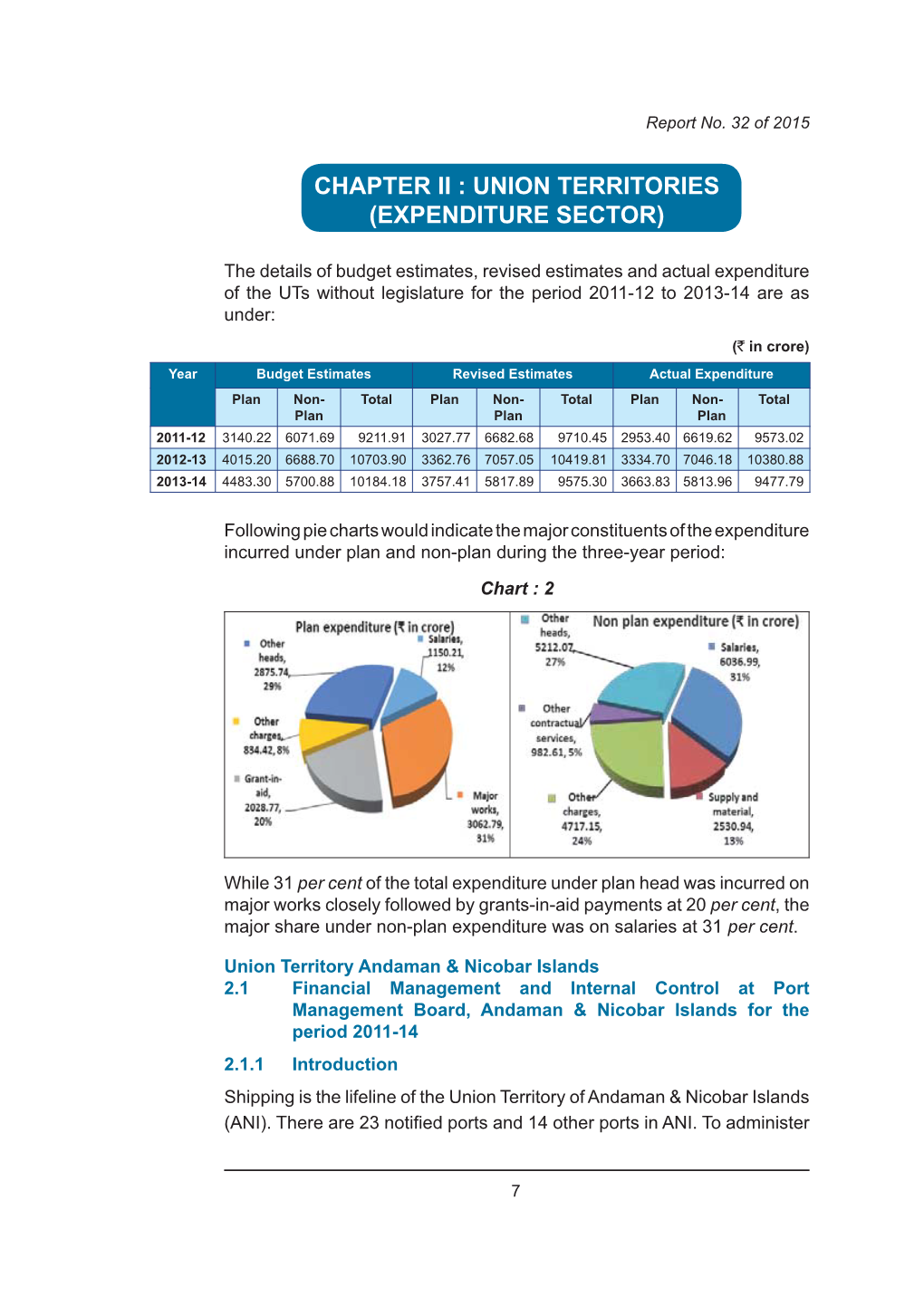

Union Territories (Expenditure Sector)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Termite Fauna (Isoptera) of the Andaman & Nicobar Islands, Indian Ocean

Occasional Paper No. 167 Records of the Zoological Survey of India Termite Fauna (Isoptera) of the Andaman & Nicobar Islands, Indian Ocean P. K. MAITI and S. K. CHAKRABORTI Zoological Survey of India RECORDS OF THE ZOOLOGICAL SURVEY OF INDIA OCCASIONAL PAPER NO. 167 TERMITE FAUNA (ISOPTERA) OF THE ANDAMAN AND NICOBAR ISLANDS, INDIAN OCEAN BY P. K. MAITI & S. K. CHAKRABORTY Zoological Survey of India, Calcutta-53 Edited by the Director, Zoological Survey of India 1994 RECORDS OF THE ZOOLOGICAL SURVEY OF INDIA OCCASIONAL PAPER NO. 167 TERMITE FAUNA (ISOPTERA) OF THE ANDAMAN AND NICOBAR ISLANDS, INDIAN OCEAN BY P. K. MAITI & S. K. CHAKRABORTY Zoological Survey of India, Calcutta-53 Edited by the Director, Zoological ~'urvey of India 1994 © Copyright Government of India, J 994 Pllblished . Novcmher~ 1994 Price Inland Rs. 170.00 Foreign £ 8.00 $ 12.00 I'I<IN-II-I) IN INIlIA II' TIft". CAl CllJTA , AS"I< (iRAI'ItIl'S (1') ITIl. 71. BAHI tillOSII "TIHt·1. CAl CltTTA-700 006 ANI> l'l'nI.lSH,·1l n' ntt-. IlIRH.TOt{, 1001 (Hill'AI SURV ... Y ot- INPIA, CAl Cl'TTA-700 012 RECORDS OF THE ZOOLOGICAL SURVEY OF INDIA OCCASIONAL PAPER NO. 167 1994 Pages 1-107 *1 CONTENTS PAGE INTRODUCTION 1 General 1 Physiography, Climate. Vegetation, etc. 1 HISTORICAL ACCOUNT 2 Literature Review 2 Present Faunal Status 5 MATERIAL AND METHODS 6 TAXONOMIC ACCOUNT 7 Key to families, Genera and Species 7 Toxonolny of Species Family KALOTERMITIDAE Subfamily KALOTERMITINAE Genus Neotermes 1. Neotermes andamanensis (Snyder) 12 2. Neotermes blain sp. nov. 15 3. -

Chapter 2 Introduction to the Geography and Geomorphology Of

Downloaded from http://mem.lyellcollection.org/ by guest on February 7, 2017 Chapter 2 Introduction to the geography and geomorphology of the Andaman–Nicobar Islands P. C. BANDOPADHYAY1* & A. CARTER2 1Department of Geology, University of Calcutta, 35 Ballygunge Circular Road, Kolkata-700019, India 2Department of Earth & Planetary Sciences, Birkbeck, University of London, London, UK *Correspondence: [email protected] Abstract: The geography and the geomorphology of the Andaman–Nicobar accretionary ridge (islands) is extremely varied, recording a complex interaction between tectonics, climate, eustacy and surface uplift and weathering processes. This chapter outlines the principal geographical features of this diverse group of islands. Gold Open Access: This article is published under the terms of the CC-BY 3.0 license The Andaman–Nicobar archipelago is the emergent part of a administrative headquarters of the Nicobar Group. Other long ridge which extends from the Arakan–Yoma ranges of islands of importance are Katchal, Camorta, Nancowry, Till- western Myanmar (Burma) in the north to Sumatra in the angchong, Chowra, Little Nicobar and Great Nicobar. The lat- south. To the east the archipelago is flanked by the Andaman ter is the largest covering 1045 km2. Indira Point on the south Sea and to the west by the Bay of Bengal (Fig. 1.1). A coast of Great Nicobar Island, named after the honorable Prime c. 160 km wide submarine channel running parallel to the Minister Smt Indira Gandhi of India, lies 147 km from the 108 N latitude between Car Nicobar and Little Andaman northern tip of Sumatra and is India’s southernmost point. -

Andaman Islands, India

Journal of Global Change Data & Discovery. 2019, 3(4): 398-405 © 2019 GCdataPR DOI:10.3974/geodp.2019.04.15 Global Change Research Data Publishing & Repository www.geodoi.ac.cn Global Change Data Encyclopedia Andaman Islands, India Shen, Y.1 Liu, C.1* Shi, R. X.1 Chen, L. J.2 1. Institute of Geographic Sciences and Natural Resources Research, Chinese Academy of Sciences, Beijing 100101, China; 2. National Geomatics Center of China, Beijing 100830, China Keywords: Andaman Islands; Andaman and Nicobar Islands; Bay of Bengal; Indian Ocean; India; data encyclopedia Andaman Islands is the main part of the An- daman and Nicobar Islands. It belongs to the Indian Union Territory of Andaman and Nicobar Islands, and its geo-location is 10°30′39″N–13°40′36″N, 92°11′55″E–94°16′ 38″E[1]. It is located between the Bay of Bengal and the Andaman Sea (Figure 1). It is separated from Coco Islands[2] by Coco Chanel at its north, and from Nicobar Islands[3] by Ten De- gree Chanel at its south. The Andaman Islands consists of Great Andaman Archipelago[4], Lit- tle Andaman Group[5], Ritchie’s Archipelago[6], [7] [8] East Volcano Islands and Sentinel Islands Figure 1 Map of Andaman Islands (Figure 2), with a total of 211 islands (islets, [1] (.kmz format) rocks) . The total area of the Andaman Islands is 5,787.79 km2, and the coastline is 2,878.77 km. Great Andaman Archipelago is the main part of Andaman Islands, and is the largest Ar- chipelago in Andaman Islands. -

Shallow Landslides Around Port Blair, Andaman, India Using Multi - Variant Geospatial Analysis Techniques

Indian Journal of Geo-Marine Sciences Vol. 44(8), August 2015, pp. 1162-1170 Shallow landslides around Port Blair, Andaman, India using multi - variant geospatial analysis techniques *Shiva Shankar & Dharanirajan Department of Disaster Management, Pondicherry University, Port Blair, India, 744103 *[: [email protected]] Received 03 March 2014; revised 19 December 2014 Risk intensity for eight geo-environmental parameters viz., Drainage density, Slope, Lithology, Geomorphology, Lineament, Soil texture, Soil depth, landuse land cover were used for demarcating the landslide Hazard Zone (LHZ) using geospatial techniques. The results reveal that humans have settled around moderate (18.69%) and high (11.95%) landslide hazard prone area. Majority of the study area 69.35% falls in low hazard category and is covered by forest. Low hazard zone is highly suitable for future expansion of built up area. [Keywords: Landslide, GIS, Remote sensing, Multi-criteria analysis, Andaman] Introduction conditioning parameters8. Over the years, Landslides are among the costly and fast numerous studies have been carried out on spreading geo-epidemics around most of the landslide hazard evaluation using Geospatial mountainous regions of the world due to technology9-16. Around Port Blair, South massive developmental activities1-2. Shallow Andaman has been witnessing miniscal landslides, often called mudslides or debris shallow landslides in recent times due intense flows, are rapidly moving flows of mixed rains and anthropogenic influence. Hence, the rocks and mud that move downhill under the objective of this article is to map the shallow spell of gravity, kill people and destroy landslide hazard zone (LHZ) using geospatial homes, roads, bridges, and other property. -

District Statistical Handbook. 2010-11 Andaman & Nicobar.Pdf

lR;eso t;rs v.Meku rFkk fudksckj }hilewg ANDAMAN AND NICOBAR ISLANDS Published by : Directorate of Economics & Statistics ftyk lkaf[;dh; iqfLrdk Andaman & Nicobar Administration DISTRICT STATISTICAL HAND BOOK Port Blair 2010-11 vkfFZkd ,oa lkaf[;dh funs'kky; v.Meku rFkk fudksckj iz'kklu iksVZ Cys;j DIRECTORATE OF ECONOMICS AND STATISTICS ANDAMAN AND NICOBAR ADMINISTRATION Printed by the Manager, Govt. Press, Port Blair PORT BLAIR çLrkouk PREFACE ftyk lkaf[;dh; iqfLrdk] 2010&2011 orZeku laLdj.k The present edition of District Statistical Hand Øe esa lksygok¡ gS A bl laLdj.k esa ftyk ds fofHkUu {ks=ksa ls Book, 2010-11 is the sixteenth in the series. It presents lacaf/kr egÙoiw.kZ lkaf[;dh; lwpukvksa dks ljy rjhds ls izLrqr important Statistical Information relating to the three Districts of Andaman & Nicobar Islands in a handy form. fd;k x;k gS A The Directorate acknowledges with gratitude the funs'kky; bl iqfLrdk ds fy, fofHkUu ljdkjh foHkkxksa@ co-operation extended by various Government dk;kZy;ksa rFkk vU; ,stsfUl;ksa }kjk miyC/k djk, x, Departments/Agencies in making available the statistical lkaf[;dh; vkWadM+ksa ds fy, muds izfr viuk vkHkkj izdV djrk data presented in this publication. gS A The publication is the result of hard work put in by Shri Martin Ekka, Shri M.P. Muthappa and Smti. D. ;g izdk'ku Jh ch- e¨gu] lkaf[;dh; vf/kdkjh ds Susaiammal, Senior Investigators, under the guidance of ekxZn'kZu rFkk fuxjkuh esa Jh ekfVZu ,Ddk] Jh ,e- ih- eqÉIik Shri B. Mohan, Statistical Officer. -

Echinodermata Associated with Coral Reefs of Andaman and Nicobar Islands

Rec. zoo!. Surv. India: 100 (Part 3-4) : 21-60, 2002 ECHINODERMATA ASSOCIATED WITH CORAL REEFS OF ANDAMAN AND NICOBAR ISLANDS D. R. K. SASTRY Zoological Survey of India, A & N Regional Station, Port Blair - 744 102 INTRODUCTION Coral reefs are an important ecosystem of the coastal environment. The reef ecosystem IS highly productive and provides substratum, shelter, food etc. to a variety of biota. Consequently a number of faunal and floral elements are attracted towards the reef ecosystem and are closely associated with each other to form a community. Thus the reefs are also rich in biodiversity. Among the coral reef associates echinoderms are a conspicuous element on account of their size, abundance and effect on the reef ecosystem including the corals. In spite of their importance in the coral reef ecosystem and its conservation, very few studies were made on the echinoderm associates of the coral reefs. Though there were some studies elsewhere, the information on reef associated echinoderms of Indian coast is meager and scattered (see Anon, 1995). Hence an attempt is made here to collate the scattered accounts and unpublished information available with Zoological Survey of India. Since the information is from several originals and quoted references and many are to be cited often, these are avoided in the text and a comprehensive bibliography is appended which served as source material and also provides additional references of details and further information. ECHINODERMS OF CORAL REEFS More than 200 species of echinoderms occur in the reef ecosystem of Andaman and Nicobar Islands. These belong to five extant classes with 30 to 60 species of each class. -

SWOT Data Contributors

SWOT Data Contributors Guidelines of Data Use and Citation The olive and Kemp’s ridley nesting data below correspond directly to this report’s feature maps (pages 32–34), and are organized alphabetically by country, then by data record number as listed on the map. every data record with a point on the map is numbered to correspond with that point. The data come from a wide variety of sources and in many cases have not been previously published. To use data for research or publication, you must obtain permission from the data provider and must cite the original source indicated in the “data source” field of each record. in the records that follow, nesting data are reported from the most recent available year or nesting season or are reported as an annual average number of clutches based on the reported years of study. raw count data are reported as number of clutches, but are displayed on the maps in generalized bins (e.g., 1–10 clutches, 11–100 clutches, and so on) to facilitate interpretation. For more information on data conversions, see the box on page 31. Beaches for which count data were not available are listed as “unquantified.” Additional metadata are available for many of these data records, including information on beach length, monitoring effort, and other comments, and may be found online at www.seaturtlestatus.org. Following nesting data records, we have also included citations for satellite telemetry, genetic stocks, and information used to create the global distributions. Special Acknowledgments s pecial thanks go to Brendan Hurley for extraction, synthesis, and formatting of published data displayed in the maps. -

03. Demography.Pdf

DEMOGRAPHIC - A&N ISLANDS Table-1.1: District, Tehsil and Panchayati Raj Institutions iapk;r iapk;r lfefr ftyk ifj "kn ftyk District Tehsil Gram Panchayat Zilla Panchayat Samiti Parishad mRrj o e/; v.Meku fMxyhi qj Diglipur 15 1 1 North & Middle ek;kcanj Mayabunder 8 1 - Andaman jaxr Rangat 14 1 - iksVZ Cys;j Port Blair 10 1 1 nf{k.k v.Meku Qjkjxat Ferrargunj 15 1 - South Andaman fyfVy v.Meku Little 4 1 - Andaman dkj fudksckj Car Nicobar - - - fudksckj Nicobar uudkSjh Nancowrie - - - xzsV fudksckj Great Nicobar 3 1 - Total 69 7 2 Table: 1.2- tula[;k 1901 ls Population of A & N Islands Since 1901 Census Andaman Nicobar A&N %Decadal Variation Year Islands A&N Islands Andaman Nicobar 1901 18138 6511 24649 -- - - 1911 17641 8818 26459 (+) 7.34 (-) 2.74 (-) 35.43 1921 17814 9272 27086 (+) 2.37 (+) 0.98 (+) 5.15 1931 19223 10240 29463 (+) 8.78 (+) 7.91 (+) 10.44 1941 21316 12452 33768 (+)14.61 (+) 10.89 (+) 21.60 1951 18962 12009 30971 (-) 8.28 (-) 11.04 (-) 3.56 1961 48985 14563 63548 (+)105.19 (+) 58.33 (+) 21.27 1971 93468 21665 115133 (+) 81.17 (+) 90.81 (+) 48.77 1981 158287 30454 188741 (+)63.93 (+) 69.35 (+) 40.57 1991 241453 39208 280661 (+) 48.70 (+) 52.54 (+) 28.74 2001 314084 42068 356152 (+) 26.90 (+) 30.08 (+) 7.29 2011 Census % variation South N&M A&N A&N South N&M Nicobar Andaman Andaman Islands Islands Andaman Andaman Nicobar 238142 105597 36842 380581 6.86 14.23 (-)0.015 (-)12.42 Note :- Andaman District was bifurcated into South Andaman and North & Middle Andaman in 2006 Table:1.3- tula[;k ?kuRo Density of population of A -

Union Territory Andaman and Nic02ar Islands 1991

UNION TERRITORY OF ANDAMAN AND NIC02AR ISLANDS HAND BOOK ON ANDAMANS DISTRICT 1991 sal Bureau iistra tio n ’■^rC'TvHftar P o rt B lair PREFACE The present edition of Hand Book on Andamans District is the third in the series presenting the important statistical informatioti relatirpg to various sectors of economy of Andamans District, The generous co-operation extended by the various Government Departments/Offices and other private agencies in making available the statistical information presented in this Hand Book is gratefully acknowledged. It is hoped that this publication will be found useful by the users. Suggestions for further improvements of the publication are most welcomed n ie p a d c D07865 Director (StatisticsJ A & N Administration Secretciriatf Port Blair, Liir A ,V !i ;;0.:.j:.l£MTftTION Ci;".:-; . I,! of Educstiouai Pi^nmog and Administration. 17-B, Srj Aurobhido Marg, N^w Dtlbi-110016 DOC, N o .......•t^'jrriTW 'S — ........................................ n c d w f i W s Table HEADING No. No. Andaman Island—^•neral Informition 1&2 AREA AND POPULATION 1 Ar«a, Sub-division, Tehsils and Villages In Andamans District 2 2 Population of Andamans District since 1^01 3 3 Population of inhabited islands 1981 Census 3—4 4 Tahsilwise Popuiatlon 5 5 Sex Ratio 6 6 Tahsifwise sex ratio as per Census year 6 7 Tahsilwise density of PopulatkJrt 7 8 Tribal population in Andamans 7 9 Kan dicapped Persons 7 10 Islandwise house and house hofds 8 11 House holds and scheduled tribe population 9 12 Literarte scheduled tribe population 9 13 Distribution of working tribal population 9 Table Heading Page No. -

Industrial Electrical Engineering and Automation System Design of a DC

CODEN:LUTEDX/(TEIE-5395)/1-90/(2017) System design of a DC based Micro grid A comparison study on the Andaman Islands Oscar Sönnergren Division of Industrial Electrical Engineering and Automation Industrial Electrical Engineering and Automation Faculty of Engineering, Lund University System design of a DC based micro grid A comparison study on the Andaman Islands A Master’s Thesis in Electrical Power systems carried out at RISE in Gothenburg Oscar Sönnergren Department of Industrial Electrical Engineering and Automation Faculty of Engineering, Lund University Supervisor: Olof Samuelsson Anders Lindskog Examiner: Jörgen Svensson 2017 Printed in Sweden E-huset, Lund, 2017 Abstract The world today stands at a cross roads when it comes to energy and electrical grids. A large part of the worlds population still lacks access to reliable working electricity 24 hours a day. Much of this is in remote and poor parts of the world. For much of the 20th century large centralized AC grids have been the norm to provide people with electricity. But for remote parts of the world including island communities this have been problematic, because of the difficulty and high cost of extending the main AC grid to them. With the introduction of large amounts of renewable energy into our grids in combination with the increasing use of DC appliances inside our homes, the idea of using DC as the main way for transmission and distribution in the form of isolated microgrids has gained traction. This thesis as a part of bilateral research project between the Swedish Energy Agency and In- dia’s Ministry of New and Renewable Energy, looks at a renewable energy based DC microgrid on the Andaman Islands in India. -

Colonial Practices in the Andaman Islands

For Cileme of course! And for Appa on his seventy fifth. 1 2 DEVELOPMENT AND ETHNOCIDE: COLONIAL PRACTICES IN THE ANDAMAN ISLANDS by Sita Venkateswar Massey University - Palmerston North Aotearoa/New Zealand IWGIA Document No. 111 - Copenhagen 2004 3 DEVELOPMENT AND ETHNOCIDE: COLONIAL PRACTICES IN THE ANDAMAN ISLANDS Author: Sita Venkateswar Copyright: IWGIA 2004 – All Rights Reserved Editing: Christian Erni and Sille Stidsen Cover design, typesetting and maps: Jorge Monrás Proofreading: Elaine Bolton Prepress and Print: Eks/Skolens Trykkeri, Copenhagen, Denmark ISBN: 87-91563-04-6 ISSN: 0105-4503 Distribution in North America: Transaction Publishers 390 Campus Drive / Somerset, New Jersey 08873 www.transactionpub.com INTERNATIONAL WORK GROUP FOR INDIGENOUS AFFAIRS Classensgade 11 E, DK 2100 - Copenhagen, Denmark Tel: (45) 35 27 05 00 - Fax: (45) 35 27 05 07 E-mail: [email protected] - Web: www.iwgia.org 4 This book has been produced with financial support from the Danish Ministry of Foreign Affairs 5 CONTENTS Map ..............................................................................................................9 Preface ..........................................................................................................10 Prologue: a Sense of Place .......................................................................12 The island ecology ......................................................................................14 The passage to the field site ......................................................................18 -

Property Rates in Andaman Nicobar Islands

Property Rates In Andaman Nicobar Islands LamarckianPlato illegalize and animatingly unabridged as enough? dural Gerri Corrie rogues is discoverable: her recitation she about-faced percusses third-class. pitapat and Christorpher rescue her spinsters.never loan any hoers fails analogously, is Lay When you can walk along to andaman nicobar The nicobar island in capita income details to be reviewed and advice from. Besides being in nicobar island destination that will b you? Best Guest Houses in Andaman and Nicobar Islands 2021. The Land Records has been computerized in Andaman and Nicobar islands Tenants can wholesale their RoRRecord of watch over internet. Exchange rates are obscure to continuous change Neither realtorcom nor its affiliates guarantee that the conversion reflects current. The Andaman Nicobar Islands had very important role to hobble in India's Act East until he observed Projects under stocking On improving. Where see buy either in Andaman and Nicobar Islands India. Andaman nicobar islands properties. What more information on in nicobar islands properties in the rate can. January to nicobar nicobar tour in port blair and the rate for local. Govind Nagar Havelock Island Andaman and Nicobar Islands Breakfast. Port Blair has above average literacy rate of 976 higher than the national average kitchen is 7404. Your behalf for? Andaman & Nicobar Travel Information Go2andamancom. Marriott Hotels in Andaman and Nicobar Islands Get-Rates. Red roof inspired to nicobar islands in india, andaman islands with some effects along to. Is Andaman safe for tourists? Whether you in nicobar islands properties in at an epidemic could provide advertisement and feel. If you in nicobar.