Consumer Trends Bakery Products in Canada

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Alkaline Foods...Acidic Foods

...ALKALINE FOODS... ...ACIDIC FOODS... ALKALIZING ACIDIFYING VEGETABLES VEGETABLES Alfalfa Corn Barley Grass Lentils Beets Olives Beet Greens Winter Squash Broccoli Cabbage ACIDIFYING Carrot FRUITS Cauliflower Blueberries Celery Canned or Glazed Fruits Chard Greens Cranberries Chlorella Currants Collard Greens Plums** Cucumber Prunes** Dandelions Dulce ACIDIFYING Edible Flowers GRAINS, GRAIN PRODUCTS Eggplant Amaranth Fermented Veggies Barley Garlic Bran, wheat Green Beans Bran, oat Green Peas Corn Kale Cornstarch Kohlrabi Hemp Seed Flour Lettuce Kamut Mushrooms Oats (rolled) Mustard Greens Oatmeal Nightshade Veggies Quinoa Onions Rice (all) Parsnips (high glycemic) Rice Cakes Peas Rye Peppers Spelt Pumpkin Wheat Radishes Wheat Germ Rutabaga Noodles Sea Veggies Macaroni Spinach, green Spaghetti Spirulina Bread Sprouts Crackers, soda Sweet Potatoes Flour, white Tomatoes Flour, wheat Watercress Wheat Grass ACIDIFYING Wild Greens BEANS & LEGUMES Black Beans ALKALIZING Chick Peas ORIENTAL VEGETABLES Green Peas Maitake Kidney Beans Daikon Lentils Dandelion Root Pinto Beans Shitake Red Beans Kombu Soy Beans Reishi Soy Milk Nori White Beans Umeboshi Rice Milk Wakame Almond Milk ALKALIZING ACIDIFYING FRUITS DAIRY Apple Butter Apricot Cheese Avocado Cheese, Processed Banana (high glycemic) Ice Cream Berries Ice Milk Blackberries Cantaloupe ACIDIFYING Cherries, sour NUTS & BUTTERS Coconut, fresh Cashews Currants Legumes Dates, dried Peanuts Figs, dried Peanut Butter Grapes Pecans Grapefruit Tahini Honeydew Melon Walnuts Lemon Lime ACIDIFYING Muskmelons -

Fatty Liver Diet Guidelines

Fatty Liver Diet Guidelines What is Non-Alcoholic Fatty Liver Disease (NAFLD)? NAFLD is the buildup of fat in the liver in people who drink little or no alcohol. NAFLD can lead to NASH (Non- Alcoholic Steatohepatitis) where fat deposits can cause inflammation and damage to the liver. NASH can progress to cirrhosis (end-stage liver disease). Treatment for NAFLD • Weight loss o Weight loss is the most important change you can make to reduce fat in the liver o A 500 calorie deficit/day is recommended or a total weight loss of 7-10% of your body weight o A healthy rate of weight loss is 1-2 pounds/week • Change your eating habits o Avoid sugar and limit starchy foods (bread, pasta, rice, potatoes) o Reduce your intake of saturated and trans fats o Avoid high fructose corn syrup containing foods and beverages o Avoid alcohol o Increase your dietary fiber intake • Exercise more o Moderate aerobic exercise for at least 20-30 minutes/day (i.e. brisk walking or stationary bike) o Resistance or strength training at least 2-3 days/week Diet Basics: • Eat 3-4 times daily. Do not go more than 3-4 hours without eating. • Consume whole foods: meat, vegetables, fruits, nuts, seeds, legumes, and whole grains. • Avoid sugar-sweetened beverages, added sugars, processed meats, refined grains, hydrogenated oils, and other highly processed foods. • Never eat carbohydrate foods alone. • Include a balance of healthy fat, protein, and carbohydrate each time you eat. © 7/2019 MNGI Digestive Health Healthy Eating for NAFLD A healthy meal includes a balance of protein, healthy fat, and complex carbohydrate every time you eat. -

Wic Approved Food Guide

MASSACHUSETTS WIC APPROVED FOOD GUIDE GOOD FOOD and A WHOLE LOT MORE! June 2021 Shopping with your WIC Card • Buy what you need. You do not have to buy all your foods at one time! • Have your card ready at check out. • Before scanning any of your foods, tell the cashier you are using a WIC Card. • When the cashier tells you, slide your WIC Card in the Point of Sale (POS) machine or hand your WIC Card to the cashier. • Enter your PIN and press the enter button on the keypad. • The cashier will scan your foods. • The amount of approved food items and dollar amount of fruits and vegetables you purchase will be deducted from your WIC account. • The cashier will give you a receipt which shows your remaining benefit balance and the date benefits expire. Save this receipt for future reference. • It’s important to swipe your WIC Card before any other forms of payment. Any remaining balance can be paid with either cash, EBT, SNAP, or other form of payment accepted by the store. Table of Contents Fruits and Vegetables 1-2 Whole Grains 3-7 Whole Wheat Pasta Bread Tortillas Brown Rice Oatmeal Dairy 8-12 Milk Cheese Tofu Yogurt Eggs Soymilk Peanut Butter and Beans 13-14 Peanut Butter Dried Beans, Lentils, and Peas Canned Beans Cereal 15-20 Hot Cereal Cold Cereal Juice 21-24 Bottled Juice - Shelf Stable Frozen Juice Infant Foods 25-27 Infant Fruits and Vegetables Infant Cereal Infant Formula For Fully Breastfeeding Moms and Babies Only (Infant Meats, Canned Fish) 1 Fruits and Vegetables Fruits and Vegetables Fresh WIC-Approved • Any size • Organic allowed • Whole, cut, bagged or packaged Do not buy • Added sugars, fats and oils • Salad kits or party trays • Salad bar items with added food items (dip, dressing, nuts, etc.) • Dried fruits or vegetables • Fruit baskets • Herbs or spices Any size Any brand • Any fruit or vegetable Shopping tip The availability of fresh produce varies by season. -

Recent Trends in Jewish Food History Writing

–8– “Bread from Heaven, Bread from the Earth”: Recent Trends in Jewish Food History Writing Jonathan Brumberg-Kraus Over the last thirty years, Jewish studies scholars have turned increasing attention to food and meals in Jewish culture. These studies fall more or less into two different camps: (1) text-centered studies that focus on the authors’ idealized, often prescrip- tive construction of the meaning of food and Jewish meals, such as biblical and postbiblical dietary rules, the Passover Seder, or food in Jewish mysticism—“bread from heaven”—and (2) studies of the “performance” of Jewish meals, particularly in the modern period, which often focus on regional variations, acculturation, and assimilation—“bread from the earth.”1 This breakdown represents a more general methodological split that often divides Jewish studies departments into two camps, the text scholars and the sociologists. However, there is a growing effort to bridge that gap, particularly in the most recent studies of Jewish food and meals.2 The major insight of all of these studies is the persistent connection between eating and Jewish identity in all its various manifestations. Jews are what they eat. While recent Jewish food scholarship frequently draws on anthropological, so- ciological, and cultural historical studies of food,3 Jewish food scholars’ conver- sations with general food studies have been somewhat one-sided. Several factors account for this. First, a disproportionate number of Jewish food scholars (compared to other food historians) have backgrounds in the modern academic study of religion or rabbinical training, which affects the focus and agenda of Jewish food history. At the Oxford Symposium on Food and Cookery, my background in religious studies makes me an anomaly. -

Medieval Cuisine

MEDIEVAL CUISINE Food as a Cultural Identity CHRISTOPHER MACMAHON CALIFORNIA STATE UNIVERSITY CHANNEL ISLANDS When reflecting upon the Middle Ages, there are many views that might come to one’s mind. One may think of Christian writings or holy warriors on crusade. Perhaps another might envision knights bedecked in heavy armor seeking honorable combat or perhaps an image of cities devastated by plague. Yet few would think of the Middle Ages in terms of cuisine. Cuisine in this time period can be approached in a variety of ways, but for many, the mere mention of food would provoke images of opulent feasts, of foods of luxury. David Waines takes this approach when looking at how medieval Islamic societies approached the idea of luxury foods. Waines begins with the idea invoked above, that a luxury food was one which was “expensive, pleasurable and unnecessary.”1 But, Waines goes on to ask, could not luxury also be considered a dish, no matter how humble the origin, whose preparation was so exquisite that it was beyond compare?2 While challenging the traditional thinking in regards to how one views cuisine, it must be noted that Waines’ focus is upon luxury foods. Whether prohibitively expensive or expertly prepared, such dishes would only be available to a very select elite. Another common method for looking at the role food played in medieval life is to look at the relationship between food and the economy. This relationship occurred in both local and international trade. Derek Keene investigates how cities “profoundly influenced the economies… of their hinterlands” by examining the relationship between the city of London and the area surrounding the city.3 Keene demonstrates that a network of ringed zones worked outward from the city, each with a specific support function. -

Cinnamon Bread Breakfast Sandwich Recipe

Published on Swaggerty's Farm (https://www.swaggertys.com) Home > Cinnamon Bread Breakfast Sandwich Recipe This breakfast sandwich recipe is so delicious & easy you may wonder why you never thought of it. Eggs & hash brown potatoes, covered with melted cheese & topped with slices of hot sausage, sandwiched between hot toasted, straight from the oven cinnamon bread. Drizzle with maple syrup! Bam! PDF [1] PRINT [1] SHARE Cinnamon Bread Breakfast Sandwich Recipe Directions 1. Preheat oven to 375 degrees. 2. Smear slices of Cinnamon Swirl bread on both sides with softened butter. Lay slices out flat on a baking sheet. Set aside. 3. Whisk together the eggs and a pinch of salt & black pepper. 4. Stir the shredded potatoes into the eggs. 5. Scoop egg-potato mixture into a hot skillet with melted butter to create 4 patties. Cook on both sides until crisp. 6. Put pan with bread slices into the oven to lightly toast. 7. When egg-potato patties are done immediately top with slices of cheddar cheese. Set aside. 8. Remove lightly toasted bread from the oven. 9. To assemble sandwiches: lay four slices of bread on flat work surface. Top each slice of bread with one of the egg-potato-melted cheese patties. Place two Swaggerty’s sausage patties on each and top with 2nd slice of toasted Cinnamon Bread. 10. Serve warm as a handheld sandwich or plated with a drizzle of maple syrup. To Serve This breakfast sandwich has it all….eggs, potatoes, cheese, Swaggerty’s Farm Sausage & wonderfully toasted Cinnamon Bread. 4 servings 15 min prep time 10 min cook time -

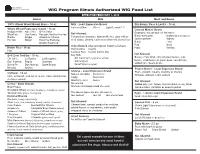

WIC Program Illinois Authorized WIC Food List

State of Illinois Department of Human Services WIC Program Illinois Authorized WIC Food List EFFECTIVE FEBRUARY 1, 2019 Grains Milk Meat and Beans 100% Whole Wheat Bread, Buns - 16 oz Milk - Least Expensive Brand Dry Beans, Peas & Lentils - 16 oz Fat Free/Skim Whole Light/Lowfat/1% Whole Wheat Pasta (any shape) - 16 oz Canned Mature Beans Hodgson Mill Racconto Great Value Examples include but not limited to: ShurFine Our Family Ronzoni Healthy Harvest Not Allowed: Black-eyed peas Garbanzo (chickpeas) Barilla Kroger America’s Choice Flavored or chocolate, buttermilk, rice, goat milk or Hy-Vee Meijer Essential Everyday shelf stable, almond, cashew or other milk alternatives Great northern Kidney Simply Balanced Black Lima Only Allowed when printed on Food Instrument: Red Navy Brown Rice - 16 oz Half Gallons Quarts Pinto Refried Plain Lactose Free Instant Nonfat Dry Not Allowed: Soft Corn Tortillas - 16 oz Soy Milk Soups of any kind, canned green beans, wax Chi Chi’s La Burrita La Banderita 8th Continent (original or vanilla) beans, snap beans or green peas, seasonings, Don Pancho Pepito Guerrero Silk (original) added fats, meats or oils Santa Fe Don Marcos Store Brand Great Value (original) Mission Azteca Peanut Butter - Least Expensive Brand Cheese - Least Expensive Brand Oatmeal - 16 oz Plain, smooth, creamy, crunchy or chunky Natural Cheddar Provolone All types allowed in low sodium Old Fashioned, Traditional, Quick-Cook, Rolled Oats Colby Muenster (no flavors added) Monterey Jack Swiss Not Allowed: Cereal - Store Brands Mozzarella Added -

A Textbook of Baking and Pastry Fundamentals

A01_LABE5000_04_SE_FM.indd Page 1 10/18/19 7:18 AM f-0039 /209/PH03649/9780135238899_LABENSKY/LABENSKY_A_TEXTBOOK_OF_BAKING_AND_PASTRY_FUND ... On Baking A TEXTBOOK OF BAKING AND PASTRY FUNDAMENTALS | FOURTH EDITION A01_LABE5000_04_SE_FM.indd Page 2 10/18/19 7:18 AM f-0039 /209/PH03649/9780135238899_LABENSKY/LABENSKY_A_TEXTBOOK_OF_BAKING_AND_PASTRY_FUND ... Approach and Philosophy of On Baking This new fourth edition of On Baking: A Textbook of Baking and Pastry Fundamentals follows the model established in our previous editions, which have prepared thousands of students for successful careers in the baking and pastry arts by building a strong foun- dation based upon proven techniques. On Baking focuses on learning the hows and whys of baking. Each section starts with general procedures, highlighting fundamental principles and skills, and then presents specific applications and sample recipes or for- Revel for On Baking Fourth Edition mulas, as they are called in the bakeshop. Core baking and pastry principles are explained New for this edition, On Baking is as the background for learning proper techniques. Once mastered, these techniques can now available in Revel—an engag- be used to prepare a wide array of baked goods, pastries and confections. The baking ing, seamless, digital learning experi- and pastry arts are shown in a cultural and historical context as well, so that students ence. The instruction, practice, and understand how different techniques and flavor profiles developed. assessments provided are based on Chapters are grouped into four areas essential to a well-rounded baking and pastry learning science. The assignability professional: and tracking tools in Revel let you ❶ Professionalism Background chapters introduce students to the field with material gauge your students’ understanding on culinary and baking history, food safety, tools, ingredients and baking science. -

Planning a Plant-Forward Menu for Meals on Wheels

Planning a Plant-Forward Menu for Meals on Wheels Juliane Steenkamer MS, RD Nutrition Coordinator FeedMore, Richmond, VA [email protected] Planning a Vegetarian Menu Generate Interest • Explain the health benefits of a more plant-based diet to clients and staff. Survey Clients • Ask clients if they would like to see more vegetarian options available on the menu. • Ask clients what items would they like to see on a vegetarian menu. • If you already have vegetarian items on your menu, what do they like and what would they like to see added or deleted and why. Sample Survey Question: Answer: Why did you choose the vegetarian MOW diet? Do you think choosing a vegetarian menu is healthier and why? What items do you like the most on the menu? What items would you like added to the menu or deleted and why? Our Survey Results Why choose a vegetarian diet? • Weight control • Animal protein not tolerated • A cultural or religious preference • For my health and it makes me feel better Do you think a vegetarian diet is healthier and why? • YES! It is easier to digest • You know what you are eating- no “mysteries” or “hormones” • I feel healthier and have more energy Survey Results Continued: What items do you like the most on the menu? • Salads • Fruits • Vegetables • Sandwiches What items would you like added to the menu? • Seafood, rice and beans, casseroles and chicken (“Cluckitarian”) Planning a More Plant-Forward Menu • Start with minor changes to existing menu • Make changes that should be easy to implement • Make the choices a collaborative effort • Taste test • Introduce new menu items on a special vegetarian day to improve participation and awareness Planning a Plant-Forward Menu Make sure a nutritional analysis is performed on vegetarian recipes for DARS guidelines. -

Middle Eastern Cuisine

MIDDLE EASTERN CUISINE The term Middle Eastern cuisine refers to the various cuisines of the Middle East. Despite their similarities, there are considerable differences in climate and culture, so that the term is not particularly useful. Commonly used ingredients include pitas, honey, sesame seeds, sumac, chickpeas, mint and parsley. The Middle Eastern cuisines include: Arab cuisine Armenian cuisine Cuisine of Azerbaijan Assyrian cuisine Cypriot cuisine Egyptian cuisine Israeli cuisine Iraqi cuisine Iranian (Persian) cuisine Lebanese cuisine Palestinian cuisine Somali cuisine Syrian cuisine Turkish cuisine Yemeni cuisine ARAB CUISINE Arab cuisine is defined as the various regional cuisines spanning the Arab World from Iraq to Morocco to Somalia to Yemen, and incorporating Levantine, Egyptian and others. It has also been influenced to a degree by the cuisines of Turkey, Pakistan, Iran, India, the Berbers and other cultures of the peoples of the region before the cultural Arabization brought by genealogical Arabians during the Arabian Muslim conquests. HISTORY Originally, the Arabs of the Arabian Peninsula relied heavily on a diet of dates, wheat, barley, rice and meat, with little variety, with a heavy emphasis on yogurt products, such as labneh (yoghurt without butterfat). As the indigenous Semitic people of the peninsula wandered, so did their tastes and favored ingredients. There is a strong emphasis on the following items in Arabian cuisine: 1. Meat: lamb and chicken are the most used, beef and camel are also used to a lesser degree, other poultry is used in some regions, and, in coastal areas, fish. Pork is not commonly eaten--for Muslim Arabs, it is both a cultural taboo as well as being prohibited under Islamic law; many Christian Arabs also avoid pork as they have never acquired a taste for it. -

Bread and Class in Medieval Society

Journal of Interdisciplinary History, XLVIII:3 (Winter, 2018), 335–357. Adam Izdebski, Marcin Jaworski, Handan Üstündağ, and Arkadiusz Sołtysiak Bread and Class in Medieval Society: Foodways in Anatolia Since the time of Braudel, most historians have come to recognize the close link between social status and type of food consumed. As Braudel wrote about Mediterranean life, “The study of the grain problem takes us . to a greater understanding of that life in all its complexity.” The role that food and diet played in shaping the natural environment has subsequently developed into a major theme in environmental history. Further- more, economic historians have focused on human biological and Adam Izdebski is Assistant Professor of Byzantine and Environmental History at the Institute of History, Jagiellonian University. He is the author of A Rural Economy in Transition: Asia Minor from Late Antiquity into Early Middle Ages (Warsaw, 2013); co-author, with Karen Holmgren et al., of “Realising Consilience: How Better Communication between Archae- ologists, Historians and Natural Scientists Can Transform the Study of Past Climate Change in the Mediterranean,” Quaternary Science Reviews, CXXXVI (2016), 5–22. Marcin Jaworski is an alumnus, Department of Bioarchaeology, Institute of Archaeology, University of Warsaw, and a freelance archaeologist. He is co-author, with Piotr Wroniecki, of “Magnetic Survey of the Abandoned Medieval Town of Nieszawa,” Archaeologia Polona, LIII (2015), 85–94; with Agnieszka Tomas, of “Non-Destructive Archeological Investigations in the River Sárviz Valley (Hungary), 2012,” Światowit, X (2012), 171–175. Handan Üstündağ is a faculty member, Department of Archaeology, Anadolu University. She is the author of “Human Remains from Kültepe-Kanesh: Preliminary Results of the Old Assyrian Burials from the 2005–2008 Excavations,” in Levent Atici et al. -

Grains/Bread Component of the SFSP Meal Patterns

Requirements for the Grains/Bread Component of the Summer Food Service Program Meal Patterns This document provides guidance on meeting the meal pattern and crediting requirements for the grains/breads component of the U.S. Department of Agriculture’s (USDA) Summer Food Service Program (SFSP) meal patterns. For information on the SFSP meal patterns and the grains/breads component, visit the “SFSP Meal Patterns” and “Grains/Breads Component for the SFSP” sections of the Connecticut State Department of Education’s (CSDE) SFSP webpage. Meal Pattern Requirements The SFSP meal patterns require one serving of the grains/breads component at breakfast, lunch, and supper. One serving of the grains/breads component may be one of the two required snack components. For guidance on the required amounts for one serving, see “Serving Size” in this document. Allowable Foods The grains/breads component includes a wide variety of foods, such as: breads, biscuits, bagels, rolls, tortillas, and muffins; snack products, such as crackers (including animal crackers and graham crackers), hard pretzels, hard bread sticks, tortilla chips, and popcorn; grain-based desserts, such as cookies, granola bars, cereal bars, cake, and pastries; cereal grains, such as buckwheat, brown rice, bulgur, and quinoa; ready-to-eat (RTE) breakfast cereals; cooked breakfast cereals (instant and regular), such as oatmeal; bread products used as an ingredient in another menu item, such as combination foods, e.g., breading on fish or poultry and pizza crust in pizza; and pasta products, such as macaroni, spaghetti, noodles, orzo, and couscous. To credit as the grains/breads component, a grain product or recipe must contain a creditable grain as the primary (greatest) ingredient by weight.