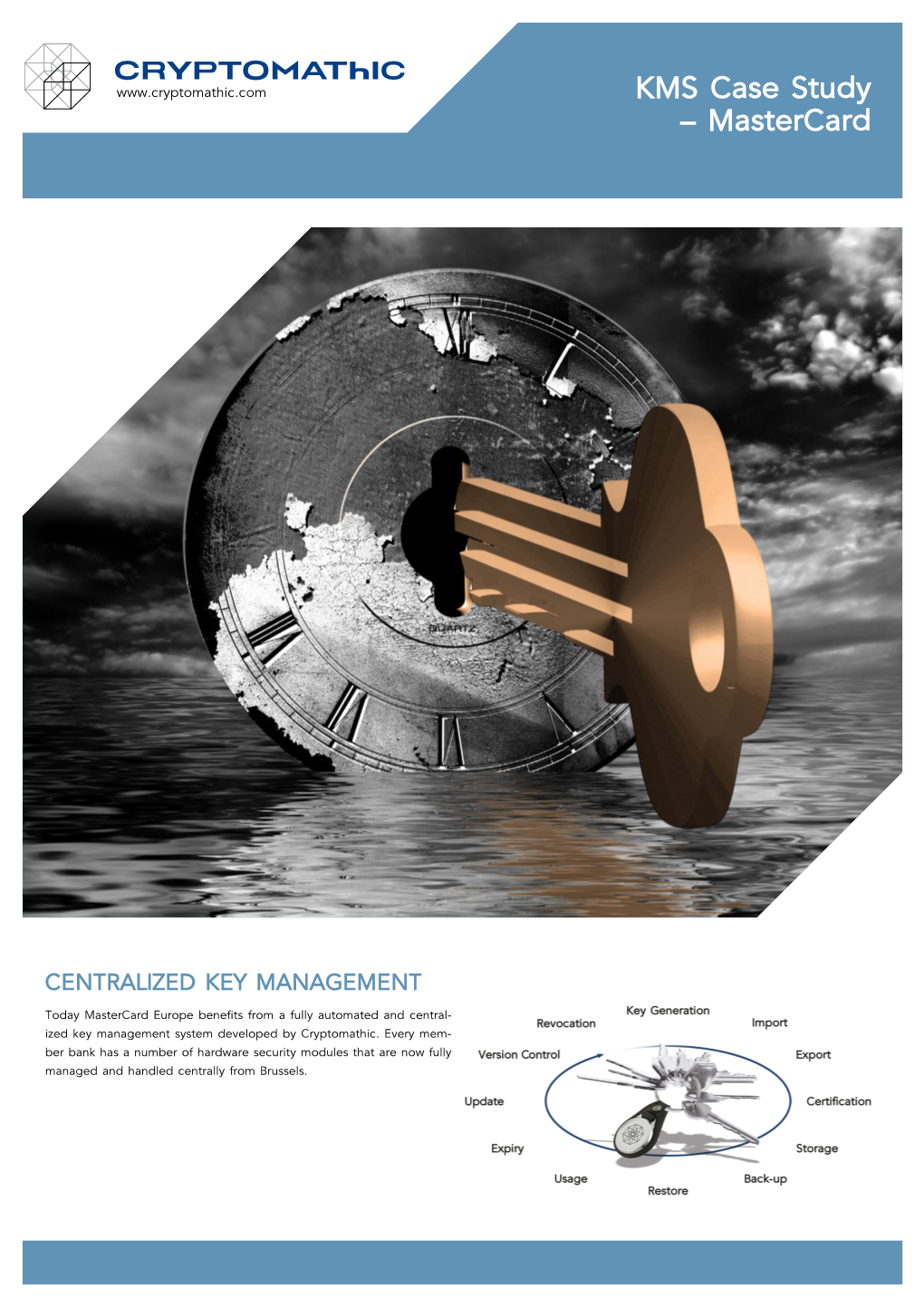

KMS Case Study – Mastercard

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

306-324 Angol Czimer Jozsef.Indd

306 JÓZSEF CZÍMER CHANGING PAYMENT LANDSCAPE1 József Czímer Th is paper is intended to be diff erent from others. I shall of course discuss almost all new achievements in the forefront of the payments industry – and there is a large number of them – but we shall see how very few systems in fact serve the vast numbers of diff erent payment tools. Also, this article tries not to be too technical, because the authors believe that even bankers claiming to be payments specialist are unfamiliar with the entire value chain of the payment service industry. Th e aim of this paper is to show what the customer sees and what is behind this front and accordingly, to show the interaction between the various elements of the system. JEL codes: G20, G21, G23 Keywords: payment services, bank card payments, mobile payments, payment infrastucure Although the European Parliament adopted European Commission proposal to create safer and more innovative European payments in Brussels on 8 October 2015, known as PSD2, this paper will refer to the PSD1 due to the fact that, fi rstly, the PSD2 has not yet entered into force and, secondly, the PSDs this paper deals with have not been changed signifi cantly. When PSD2 enters into force it will intend to amend and replace PSD1 to •reduce ambiguity; • level the playing fi eld for payments providers; • increase consumer protection; • stimulate innovation; • increase competition; and • enforce the implementation of new payments type. Th e two major provisions and implications of PSD2 will be the followings: • it accepts the Th ird Party Payment (TPP) provision; and • under the “Access to Accounts” (XS2A) rule it will force banks to provide customer account information to third parties via API, if the account holder agrees. -

Banktocustomerdebitcreditnoti

Usage Guideline BankToCustomerDebitCreditNotificationV06 - Mixed Bank to Corporate Messages Portfolio - Draft - January 31, 2017 This document describes a usage guideline restricting the base message MX camt.054.001.06. You can also consult this information online. Published by Payments Canada and generated by MyStandards. 30 January 2017 Usage Guideline Table of Contents .Message Functionality ................................................................................................................................................. 3 1 Restriction summary ......................................................................................................................................... 5 2 Structure ................................................................................................................................................................. 6 3 Rules ......................................................................................................................................................................... 7 4 Message Building Blocks ............................................................................................................................... 8 5 Message Components .................................................................................................................................... 10 6 Message Datatypes ........................................................................................................................................ 226 7 Restriction appendix -

Cryptomathic EMV CA

Cryptomathic EMV CA EMV AND PKI A Regional EMV Solution The EMV standard is designed to provide an interoperability frame- work for payment cards. This covers many transaction types including credit, debit, contactless and mobile. Payment cards have been around for many years in various forms. The latest cards have become more sophisticated and now contain a microchip, which can store a wealth of information, including security information used for authentication and encryption. EMV card authentication is based on PKI (Public Key Infrastructure) but unlike traditional PKI, which is based on a standard called X.509, EMV EMV CA is a standard of its own. Even though EMV is a proprietary standard it The Cryptomathic EMV CA professionally manages all the Issuer's and is widely used across the globe, with billions of EMV smart cards issued Certification Authority’s tasks including: since its initial roll-out. • Lifecycle management of EMV Issuer CA (scheme issuers’) certificates • Issue certificates EMV Certification Authorities are central to the payment card framework, • Export certificates under which issuers and acquirers are certified by the payment schemes, • Revoke certificates acting as a trusted third party. A payment scheme can be a major • Certification authority CRL (Certificate Revocation List) international player such as MasterCard and Visa or it can be regional • Issuer CRL (Certificate Revocation List) or country wide, such as national debit schemes, which are found in many countries all over the world. Each payment scheme requires an Benefits EMV Certification Authority and the Cryptomathic EMV CA provides that Cryptomathic EMV CA offers all the features expected from professional exact functionality. -

ABCD Life Sciences Top Titles

ABCD springer.com Life Sciences Top Titles September 2009 springer.com Biochemistry (general) 2 Biochemistry (general) powerful tool that enables us to seek a deeper under- ine the relevant physiological, emotional, cognitive standing of the complex mechanisms underpinning so and social processes. The resulting understanding of many vital biologic systems. In this fully revised and the functional interplay of these processes gives valu- updated second edition of Bioluminescence: Meth- able insights into the biological roots and benefits of ods and Protocols, expert researchers contribute a religion. readable and utilitarian compilation of the newest More on www.springer.com/978-3-642-00127-7 and most innovative techniques that have emerged in this rapidly expanding and progressively diverse Available field including methods to assess cell trafficking, pro- 2009. X, 304 p. 13 illus. (The Frontiers Collection, ) tein-protein interactions, intracellular signaling, and 978-3-642-00127-7 ▶ 69,95 € apoptosis. Also opening up the possibility to visual- ize and quantify biological mechanisms in real-time and in in vivo settings, the volume also describes the in vivo study of bacterial or viral infections, trans- planted cells, stem cells proliferation, vascular flow, E. Jacoby and tumors. Written in the highly successful Meth- ods in Molecular Biology™ series format, chapters Chemogenomics include brief introductions to their respective top- Methods and Applications ics, lists of the necessary materials, equipment, and reagents, step-by-step, readily reproducible laboratory The establishment, analysis, prediction, and expan- protocols, and notes on troubleshooting and avoiding sion of a comprehensive ligand-target Struc- known pitfalls. Authoritative and cutting-edge, Bio- ture-Activity Relationship (SAR) in the post-genomic luminescence: Methods and Protocols, Second Edi- era presents a key research challenge for this cen- tion provides protocols that are detailed enough to tury. -

Bin Qty Brand Code Bank Level Type Country 180006 1

BIN QTY BRAND CODE BANK LEVEL TYPE COUNTRY 180006 1 Unknown 120 Unknown Unknown Unknown Unknown 180015 1 Unknown 120 Unknown Unknown Unknown Unknown 180028 1 Unknown 120 Unknown Unknown Unknown Unknown 180036 1 Unknown 120 Unknown Unknown Unknown Unknown 180039 1 Unknown 101 Unknown Unknown Unknown Unknown 180050 1 Unknown 120 Unknown Unknown Unknown Unknown 180051 1 Unknown 101 Unknown Unknown Unknown Unknown 213168 1 Unknown 221 Unknown Unknown Unknown Unknown 300000 2 Unknown 101 Unknown Unknown Unknown Unknown 300070 1 Unknown 101 Unknown Unknown Unknown Unknown 300087 1 Unknown 101 Unknown Unknown Unknown Unknown 300100 1 Unknown 101 Unknown Unknown Unknown Unknown 300400 1 Unknown 101 Unknown Unknown Unknown Unknown 300583 1 Unknown 101 Unknown Unknown Unknown Unknown 300600 1 Unknown 101 Unknown Unknown Unknown Unknown 300718 1 Unknown 101 Unknown Unknown Unknown Unknown 300752 35 Unknown 101 Unknown Unknown Unknown Unknown 300763 17 Unknown 101 Unknown Unknown Unknown Unknown 300800 6 Unknown 101 Unknown Unknown Unknown Unknown 300901 1 Unknown 101 Unknown Unknown Unknown Unknown 300903 1 Unknown 101 Unknown Unknown Unknown Unknown 300928 4 Unknown 101 Unknown Unknown Unknown Unknown 300940 1 Unknown 101 Unknown Unknown Unknown Unknown 300941 1 Unknown 101 Unknown Unknown Unknown Unknown 300947 2 Unknown 101 Unknown Unknown Unknown Unknown 301305 1 Unknown 101 Unknown Unknown Unknown Unknown 301460 1 Unknown 101 Unknown Unknown Unknown Unknown 301702 1 Unknown 101 Unknown Unknown Unknown Unknown 301801 1 Unknown 101 Unknown Unknown -

Cryptographic Algorithm Analysis and Implementation

EasyChair Preprint № 3210 Cryptographic Algorithm Analysis and Implementation Nandkumar Niture EasyChair preprints are intended for rapid dissemination of research results and are integrated with the rest of EasyChair. April 20, 2020 Cryptographic Algorithm Analysis and Implementation By: - Nandkumar A Niture 1 Abstract The impact and necessity of information security has increased exponentially over the last f ew decades as the denial-of-service attacks are increasing, information is being stolen, hackers are using more sophisticated and smart methods with help of agile tools for stealing sensitive information. Do small/mid-size/large corporate organizations need the security of their system? Yes. They have sensitive user data, employee data, trading data, customer data and other sensitive confidential information stored in office systems. Do common people need the security of their systems at home? Yes. They may have their taxes files, social security card information, bank account details, private pictures, marketing strategy for their small business and many more private things. Computer cryptography was the exclusive domain for long period of time since World War II but now is practiced outside of military agencies. Cryptography is both science and art, it uses known obscurity and mathematical formulae. Cryptographic systems should have ability to assure the authenticity of source from where message gets originated and proof of complete message delivery. It is sometimes insufficient to protect ourselves from the rules and laws, but we need to protect ourselves with applying sufficient mathematical equations. So, it is individuals and legal organizations responsibility to protect their own data. By combining the digital signature with public-key cryptography, we can develop a protocol that combines the security of encryption with the authenticity of digital signatures. -

E-Admin Terms and Conditions Administrator Is Appointed by the Login Credentials Company, Is Responsible for E-Admin Temporary Password and User ID

E-admin Terms and Conditions administrator is appointed by the Login Credentials Company, is responsible for e-admin Temporary password and User ID. 2020/04 within the Company and will be the contact person that Eurocard sends PCI DSS 1. Introduction information regarding e-admin to. The The Payment Card Industry Data Security E-admin is Eurocard's online system for super administrator is able to access all Standard (PCI DSS) is a widely accepted the administration of Cards and Accounts. functions and modules that the Company set of policies and procedures intended to has been granted access to and has optimize the security of credit, debit and E-admin offers a number of different immediate access to all Cards and cash card transactions and protect functions that the Company has Accounts connected to the Company in e- cardholders against misuse of their immediate access to, as well as a number admin. Super administrators also have the personal information. Websites of the PCI of optional modules that the Company right to appoint new administrators and Security Standards Council, (www. pcisecuritystandards.org) include can request access to. update and delete administrators’ access rights. A super administrator is not instructions and information concerning The Company has access to the following allowed to appoint new super safe handling of card data. functions in e-admin: administrators. Temporary password Card An eight-digit OTP (One-Time Password) • View Cards and Accounts Refers to Eurocard Corporate cards with sent to the Administrator’s mobile phone • Apply for and close Cards and the exception of Eurocard Corporate Limit number . -

Cryptomathic Signer V 1.0

Signer Case Study – LuxTrust CENTRAL SIGNING SERVICE Residents in Luxembourg are now able to securely access a variety of web applications such as eBanking and public services, as well as digitally sign legally binding transactions and official documents from an online PC or mobile device, anywhere in the world. With just one LuxTrust certificate, users can remotely access and sign multiple online forms from any organisation connected to the service, whether they are registering their new home or applying for a loan. This highly innovative and flexible authentication and digital signature service has been imple- mented by LuxTrust, using Cryptomathic’s solutions. LUXTRUST LuxTrust approached Cryptomathic to solve the challenging issue of establishing legal value by way of high security (using PKI and 2FA) As Luxembourg’s primary provider of digital identity and electronic without costs escalating and destroying the business case. Today, most data security services, LuxTrust provides various IT services, aimed at Luxembourg based institutions, including eGovernment and eBanking, delivering and enforcing digital trust between parties, including certifi- utilise the benefits delivered by LuxTrust’s SSC – a mutual security infra- cate issuance, strong authentication, digital signatures, time stamping, structure service. The SSC combines this high level of security in the and long term storage to enable secure electronic commerce and most convenient and portable service, allowing users to authenticate to meet the future security requirements -

Cryptomathic Signer SAM V. 5.0 Security Target for Utimaco Cryptoserver CP5

Cryptomathic Signer SAM v. 5.0 Security Target for Utimaco Cryptoserver CP5 Document Version: 5.0 Document ID: ASE_ST_UTIMACO Date: September 19, 2019 Cryptomathic Signer Security Target for Utimaco Cryptoserver CP5 ASE_ST_UTIMACO 5.0 September 19, 2019Error! Unknown document property name. Document Identification Document Title: Cryptomathic Signer Security Target for Utimaco Cryptoserver CP5 Document ID: ASE_ST_UTIMACO Document Version: 5.0 Date of version: September 19, 2019 Origin: Cryptomathic Author: Lone Asferg Laursen, Thomas Brochmann Pedersen TOE Reference: Cryptomathic Signer SAM v 5.0 for Utimaco Cryptoserver CP5 Product Type: QSCD 2 Cryptomathic Signer Security Target for Utimaco Cryptoserver CP5 ASE_ST_UTIMACO 5.0 September 19, 2019Error! Unknown document property name. Terms Term Meaning CA Certification Authority. CM Cryptographic Module. Recides within the HSM. Cryptographic Module Cryptographic Module certified according to [EN 419 221-5]. Utimaco CryptoServer Se-Series Gen2 CP5, version 5.1.0.0. DTBS/R Data To Be Signed Representation. A hash value of the document to be signed. HSM Hardware Security Module. IdP Identity Provider. Privileged User The users who administrate the TOE and the signer users. This is the Common Criteria term for administrator users. Administrator The Signer SAM term for a privileged user. QSCD Qualified Electronic Signature (or Electronic Seal) Creation Device as defined in [eIDAS]. RA Registration Authority. SAD Signature Activation Data SAM Signature Activation Module SAP Signature Activation Protocol. Protocol use to perform the signature operation. SCA Signature Creation Application. Application responsible for creating the document to be signed. SIC Signer Interaction Component. Signer User End user who can sign documents. Signing key A cryptographic key used for signing under the sole control of a signer. -

Eurocard Corporate Private Liability - Page 1 Arrangement ID Product No

Eurocard Corporate Private liability - page 1 Arrangement ID Product no. Completed by the commpany Company name Address Postal code Town/City Country code (not DK) Telephone + Contact person (required field) Desired payment method Payment of consumption on corporate cards desired via Private account – regarding private account, please provide payment information on page 2. Company account – please provide desired payment method below. Reg. no. (sort code) Account no. Betalingsservice Bank Giro form - invoice to be sent to company address. If another address is to be used, please provide it here Attn. name Invoice address Postal code Town/City Country code (not DK) Electronic payment via EAN no.: Authorised signatory We hereby confirm the company information provided above, and that the card applicant is an employee of the company. We approve the issue of a Eurocard Corporate Card to the stated emplo- yee/card applicant. We accept that the card must be returned to Eurocard if the employee leaves the company. 201119 Date Company seal and signature – authorised signatory Company reg. no. Name in print Social security number* – Name in print Social security number* – * If a signatory lacks a Nordic social security number, a copy of the signatory’s passport must be attached (certified by another person with name, contact information and signature) together with the address details in the country of residence. Information card applicant 1505 Eurocard is issued by SEB Kort Bank Danmark branch of SEB Kort Bank AB (Sweden) CVR-nr.: 25804759 Business ID. 556574-6624. eurocard.com * Eurocard Corporate Private liability - page 2 Completed by the card applicant – Please enclose copy of latest pay check and picture ID, copy of passport or driving license. -

Ein Gemeinschaftsunternehmen Der Deutschen Banken Und Sparkassen Sehr Geehrte Leserin, Sehr Geehrter Leser

Ein Gemeinschaftsunternehmen der deutschen Banken und Sparkassen Sehr geehrte Leserin, sehr geehrter Leser, die deutschen Bezahlsysteme befinden sich in In dieser Broschüre finden Sie Informationen über ständigem Wandel. Einerseits wirken Innovationen unsere Kernkompetenzen – Business Development, und neue Technologien auf sie ein, andererseits Vermarktung, Sicherheitsmanagement und Lizenz- stellen uns europäische Regularien und die Harmo- management – und wie diese sich aus unserer nisierung des internationalen Zahlungsverkehrs vor Historie herleiten. Natürlich erfahren Sie darüber stetig neue Herausforderungen. Neue Regelungen hinaus, wie wir Sie mit unseren Geschäftsfeldern müssen europaweit praktikabel sein und natürlich konkret unterstützen können. auch den hohen Ansprüchen der Bürgerinnen und Bürger in Deutschland genügen. Wir freuen uns auf den Austausch mit Ihnen! In diesem Spannungsfeld – nationale versus länder- übergreifende Anforderungen, technologischer Ihr Fortschritt versus traditionelle Denkmuster, Effizienz und Optimierung versus vertraute, erlernte Prozes- se – bewegt sich die EURO Kartensysteme GmbH als Gemeinschaftsunternehmen der Banken und Karl F. G. Matl Sparkassen. Geschäftsführer der EURO Kartensysteme GmbH Was sich nach ideellem Spagat anhört, ist vielmehr ein Anspruch an die Arbeit unserer Institution. Dabei setzen wir auf technologische Innovationen „Made in Germany“ und die hohen Sicherheits- und Datenschutzstandards der Deutschen Kreditwirt- schaft. Unser Selbstverständnis ist es daher, dass wir jederzeit als Partner bereitstehen, Vernetzung fördern und das bargeldlose Bezahlen in Deutsch- land vorantreiben. Die Bezahlverfahren der Deutschen Kreditwirt- schaft orientieren sich stets an den hohen Quali- täts- und Sicherheitsansprüchen von Banken und Sparkassen sowie Handel und Verbrauchern. Dafür betreiben wir ein aktives Sicherheitsmanagement. Auch beim Bezahlen wollen wir Deutschland als Innovationsstandort positionieren und den Weg in eine modernere Gesellschaft ebnen. Diesen Weg möchten wir gemeinsam mit Ihnen gehen. -

Industry Terms Defined

Industry Terms Defined General Network: Visa, MasterCard, Interac are the main networks in Canada they established and maintain the networks through which credit and debit card transactions are processed Acquirer: In Canada a bank that does the heavy lifting of processing credit card processing. The largest in Canada are Chase Paymentech, Dejardin, Elavon, First Data, Global Payments, Moneris, People’s Trust and TD Merchant Services. There are others but if you are a business in Canada most likely you are processing through one of the above. Processor: There is not official definition for processor. Acquirers, ISOs and MSPs often are referred to as Processors. ISO: Independent Sales Organization are exactly what the name suggests and resell the services of the Acquirers. Best way to look at the ISO - Acquirer relationship is supplier and customer. MSP: Merchant Service providers are best described as self-employed salespeople who sell Acquirers services. The difference to ISOs is independence, ISOs are independent can write their own contracts add their own fees etc. Qualified Credit Card Transactions: For Visa it is classic, platinum and gold cards, for MasterCard they are classified as “Core” cards the attract the lowest Interchange fees and to be qualified must be a card present transaction, face to face. Non-Qualified Credit Card Transactions: All other cards other than above including rewards, business, purchasing, commercial etc and cards that are not presented in person including online transactions, keyed/phone transactions and any transaction where the card is not swiped or emv (chip & pin). EMV stands for Eurocard, MasterCard and Visa and refers to cards with chip and pin.