View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

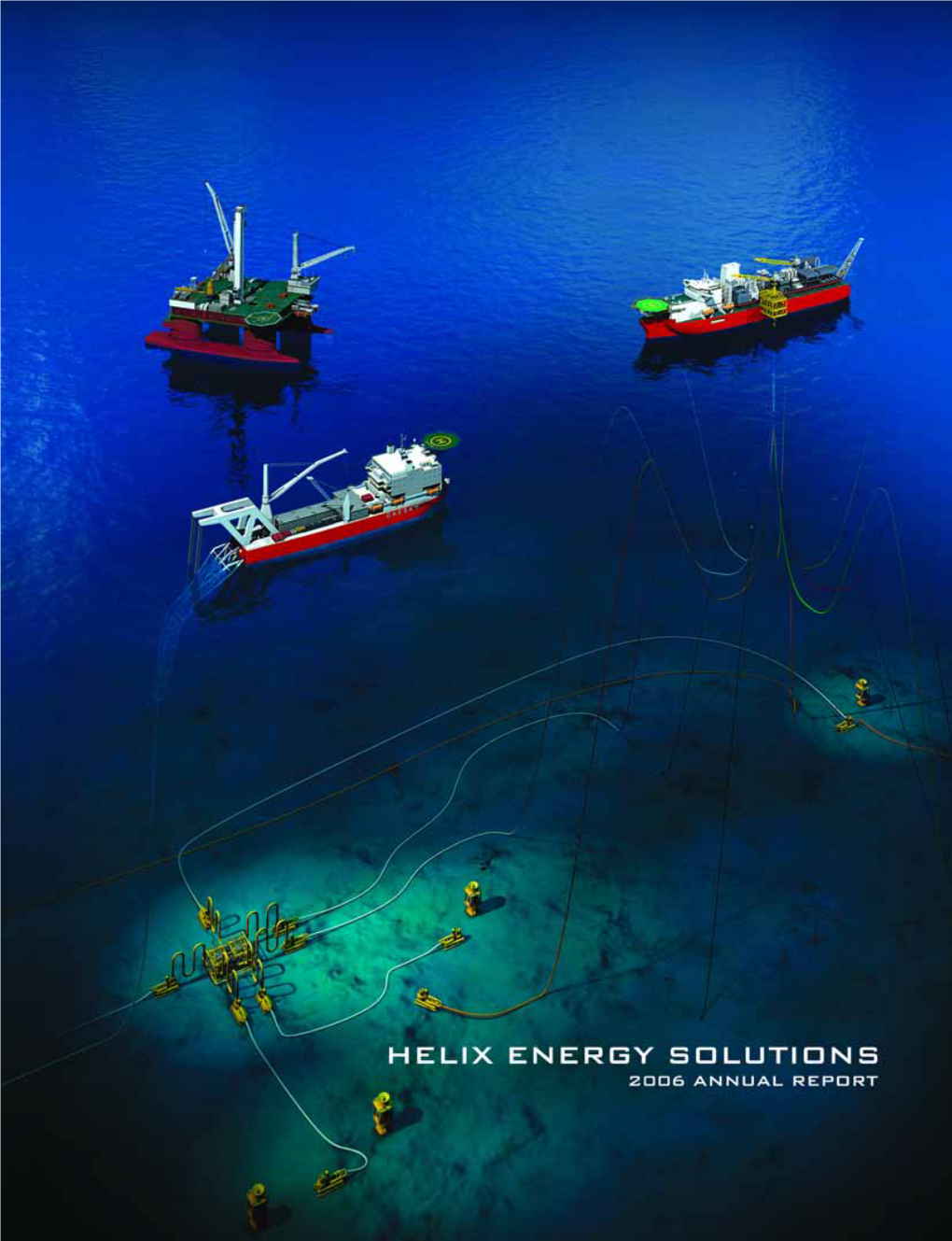

Annual Report

AAPG EMD Gas Hydrates Committee Report – 2009 By Bob Lankston and Art Johnson Progress toward commercialization of gas hydrates in North America and Asia is continuing in 2009, with some notable advancement in both resource assessment and technology. U.S. Exploration Activity With many challenges and unknowns remaining long-term, economically-viable production of natural gas from hydrates is as yet unproven. Gas hydrate R&D is the type of high cost, high-risk, high-potential endeavor that calls for government economic support. Progress in the U.S. has been limited by the relatively low budget levels of the Department of Energy (DOE) methane hydrate program, the primary source of funding for U.S. hydrate efforts. While Congress authorized $30 million for fiscal year 2008 and $40 million for fiscal year 2009 under the Energy Policy Act of 2005, the appropriation for each year was for only $16 million. The new administration has shown a higher level of interest in hydrate, particularly for its carbon sequestration potential. The areas of focus for U.S. hydrate efforts are the North Slope of Alaska and the Deepwater Gulf of Mexico. The companies that are most involved with gas hydrate programs in the U.S. include BP, Chevron, ConocoPhillips, Schlumberger, and Halliburton; although all of the operators on the North Slope are now becoming involved. Their in-kind contributions of labor and data are complemented by a substantial match of Federal funds. Several service companies are engaged in a support role as subcontractors. A long-term, industry-scale production test is planned for the North Slope in the summer of 2010 as a follow-up to BP’s successful “Mt. -

Parviz Izadjoo, Et Al. V. Helix Energy Solutions Group, Inc., Et Al. 15-CV

Case 4:15-cv-02213 Document 23 Filed in TXSD on 03/14/16 Page 1 of 29 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION PARVIZ IZADJOO, Individually and on behalf of all others similarly situated, Plaintiff, Civ. Action No. : 4:15-CV-2213 v. OWEN KRATZ, and HELIX ENERGY SOLUTIONS JURY TRIAL DEMANDED GROUP, INC. Defendants. AMENDED CLASS ACTION COMPLAINT Lead Plaintiffs Steven Strassberg (“Strassberg”) and Bruce R. Siegfried (“Siegfried” and together with Strassberg, “Plaintiffs”), by and through their counsel, individually and on behalf of all others similarly situated, for their Amended Class Action Complaint against defendants Helix Energy Solutions Group, Inc. (“Helix” or “Company”) Owen Kratz (“Kratz”) Anthony Tripodo (“Tripodo”), and Clifford V. Chamblee (“Chamblee”), allege the following based upon personal knowledge as to themselves and their own acts, and information and belief as to all other matters, based upon, inter alia, the investigation conducted by and through their attorneys, which included, among other things, conversations with witnesses, a review of the defendants’ public documents, conference calls and announcements made by defendants, United States Securities and Exchange Commission (“SEC”) filings, wire and press releases published by and regarding Helix Energy Solutions Group, Inc. (“Helix” or “Company”), analysts’ reports and advisories about the Company, and information readily obtainable on the Internet. Plaintiffs believe that substantial Case 4:15-cv-02213 Document 23 Filed in TXSD on -

National Commission on the BP Deepwater Horizon Oil Spill and Offshore Drilling

National Commission on the BP Deepwater Horizon Oil Spill and Offshore Drilling STOPPING THE SPILL: THE FIVE-MONTH EFFORT TO KILL THE MACONDO WELL ---Draft--- Staff Working Paper No. 6 Staff Working Papers are written by the staff of the National Commission on the BP Deepwater Horizon Oil Spill and Offshore Drilling for the use of members of the Commission. They are preliminary, subject to change, and do not necessarily reflect the views either of the Commission as a whole or of any of its members. In addition, they may be based in part on confidential interviews with government and non-government personnel. The effort to contain and control the blowout of the Macondo well was unprecedented. From April 20, 2010, the day the well blew out, until September 19, 2010, when the government finally declared it “dead,” BP expended enormous resources to develop and deploy new technologies that eventually captured a substantial amount of oil at the source and, after 87 days, stopped the flow of oil into the Gulf of Mexico. The government organized a team of scientists and engineers, who took a crash course in petroleum engineering and, over time, were able to provide substantive oversight of BP, in combination with the Coast Guard and the Minerals Management Service (MMS).1 BP had to construct novel devices, and the government had to mobilize personnel on the fly, because neither was ready for a disaster of this nature in deepwater. The containment story thus contains two parallel threads. First, on April 20, the oil and gas industry was unprepared to respond to a deepwater blowout, and the federal government was similarly unprepared to provide meaningful supervision. -

Leveraging Our Global Capabilities

Subsea 7 S.A. Annual Report and Financial Statements 2010 Leveraging our global capabilities Subsea 7 S.A. (Formerly Acergy S.A.) Annual Report and Financial Statements 2010 Leveraging our global capabilities Subsea 7 S.A. is a global leader in seabed-to-surface engineering, construction and services. The Combination of Acergy S.A. and Subsea 7 Inc. in January 2011 created a global leader in seabed-to-surface engineering, construction and services able to offer clients access to a high end, diversified fleet, comprising 42 vessels supported by extensive fabrication and onshore facilities able to deliver the full spectrum of subsea engineering, construction and services. Subsea 7 S.A. is well positioned to take advantage of future growth opportunities in the global seabed-to-surface market. We are leveraging our global capabilities through our greater depth of project management, engineering and technical expertise along with our high-end diversified fleet to secure and deliver complex offshore projects on behalf of our clients, in safe and sustainable ways. For all the latest up-to-date information visit www.subsea7.com Subsea 7 S.A. Registered office: 412F, route d’Esch L-2086 Luxembourg Registered number: B 43 172 Creating a new force in seabed-to-surface May 2010 Awarded $120 million Dec 2009 Dec 2009 contract, offshore Acquires Borealis Awarded three-year Nigeria Acergy acquired Borealis, a DSV contract Awarded Conventional state-of-the-art deepwater Awarded three-year project for the removal construction and pipelay contract for the provision of existing risers, vessel. Borealis is ideally of Dive Support Vessel the installation of new suited to meeting the services to the DSVi pipelines and associated exacting requirements of Collective of companies risers, together with ultra-deep and deepwater in the North Sea. -

Innovation in Non Destructive Testing

Innovation in Non Destructive Testing Entrepreneurship Casper Wassink Innovation in Non Destructive Testing Proefschrift Ter verkrijging van de graad van doctor aan de Technische Universiteit Delft, op gezag van de Rector Magnificus prof.ir. K.C.A.M. Luyben, voorzitter van het College van Promoties, in het openbaar te verdedigen op donderdag 12 januari 2012 om 12:30 uur door Casper Harm Philip WASSINK Natuurkundig Ingenieur geboren te Aalsmeer Dit proefschrift is goedgekeurd door de promotor: Prof. dr. ir. A.J. Berkhout Copromotor: Dr. J.R. Ortt Samenstelling promotiecommissie: Rector Magnificus, Technische Universiteit Delft, Voorzitter Prof. dr. ir. A.J. Berkhout, Technische Universiteit Delft, Promotor Dr. J.R. Ortt, Technische Universiteit Delft, Copromotor Prof. dr. A.H. Kleinknecht, Technische Universiteit Delft Prof. dr. ir. J.G. Slootweg, Technische Universiteit Eindhoven Prof. dr. B.J.M. Ale, Technische Universiteit Delft Prof. dr. U. Ewert, Bundesanstalt für Materialforschung und -prüfung Dr. ir. M. Lorenz, Shell Global Solutions Prof. dr. ir. P.M. Herder, Technische Universiteit Delft, reservelid ISBN 978-90-8570-795-0 Copyright © 2011 Casper Wassink, Rotterdam, The Netherlands Printed by: Wöhrmann Print Service All rights reserved, No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior consent of the author. Samenvatting Innovatie is vandaag de dag geen activiteit meer die kan worden overgelaten aan een aparte afdeling of een kennisinstituut. Het is een kerncompetentie van succesvolle ondernemingen. Echter, in veel gevestigde ondernemingen is de snelheid van innovatie laag. De Niet Destructie Onderzoek sector is een voorbeeld van een sector waar de snelheid van innovatie zeer laag is. -

Deepwater Horizon Blowout Preventer Failure Analysis Report to the U

Deepwater Horizon Blowout Preventer Failure Analysis Report To the U. S. Chemical Safety and Hazard Investigation Board CSB-FINAL REPORT-BOP(06-02-2014) The Deepwater Horizon BOP stack at NASA-Michoud (with the upper LMRP portion on left) This analysis considered the BOP examinations that were conducted by Det Norske Veritas (DNV) at the NASA Michoud facility near New Orleans, Louisiana. The examinations were in two phases, the first conducted for the Joint Investigation Team and a Phase 2 funded by BP. CSB and Engineering Services were excluded from Phase 2, but subsequently obtained examination information from that period. Contents 1. Introduction...............................................................................................................................3 2. Summary of incident failures and new opinions.......................................................................4 3. Incident summary timeline.......................................................................................................8 4. Incident progression: initial fluid displacement for the negative pressure test.....................13 5. Incident progression: negative pressure test..........................................................................14 6. Incident progression: final displacement and initial oil flow starts.......................................18 7. Incident progression: oil flow increases..................................................................................20 8. Failure of the upper annular and sealing by a -

1 April 2011

April 2011 UT3 The ONLINE magazine of the Society for Underwater Technology Offshore Engineering Tidal Energy Underwater Equipment 1 UT2 April 2011 Contents Processing Pilot Ready for Testing 4 April 2011 UT2 The magazine of the Offshore Jubarte, Wellstream 6, Gygrid, Tahiti, Gudrun, West Boreas 8, Society for Underwater Technology News Clov, Liuhua, Abkatun, FMC, Cameron/SLB 9, Deepwater Pipelay System 10, McDermott FEED, Brazil, Goliat, Ekofisk, Mariscal Sucre Dragon/Patao, BP 11, Ultra High Flow Injection, Omni- Choke 12 Underwater Flow Assurance Using Radioisotope Technology 14, Pipelines Deepwater Composite Riser 16, Hyperbaric Test Chamber Offshore Engineering Tidal Energy 17, High Pressure Swagelining, Plough in Baltic for Nord- Underwater Equipment Stream, SCAR 18 1 UT2 April 2011 The stern of Saipem’s new vessel showing the pipelay Underwater Subsea UK, RBG 20, Subspection, flexGuard 21, tower. Equipment Laser Scanning 22, HMS Audacious, TOGS, HULS, PAVS 24, Image: IHC Engineering Mojave in China 25, Tsunami Detection, Motion Sensor 26, Cable Survey 27, Cameras and Underwater Digital Stills 28, University of Plymouth Flora Lighting and Fauna Survey, True Lumens 30, Pan and Tilt Camera, April 2011 Aurora 31 Vol 6 No 1 Underwater Multi-Sensor AUV Pipeline Inspection, Integration 32, New Vehicles Markets for the AC-ROV 33, Cougar, CDS 34 2 Sonar 4000m Imaging, UUV, SALT 36, Sonar 294 37 UT Society for Underwater The Tide is Turning 36, MCT, Beluga 9 40, Bio Power 41, Technology Tidal 80 Coleman St The Bourne Alternative, Nexus Positioning, Hales Turbine 42, London EC2R 5BJ Norwegian Ocean Power 43, ORPC Turbine Generator 44, Oyster 2 45, Wave and Tidal 45 +44 (0) 1480 70007 Exhibitions UDT 46 Editor: John Howes [email protected] SUT Advanced Instrumentation for Research in Diving and Hyperbaric Medicine 47, AGM 48, Aberdeen Sub Editor: Michaelagh Shea [email protected] AGM and Dinner 49, AGM Perth 50 US: Published by UT2 Publishing Ltd for and on behalf of the Society for Underwater Stephen Loughlin Technology. -

Acergy S.A. Announces Second Quarter Results

Acergy S.A. Announces Second Quarter Results London, England – July 14, 2010 – Acergy S.A. (NASDAQ-GS: ACGY; Oslo Stock Exchange: ACY), announced today results for the second quarter which ended on May 31, 2010. The Group’s accounts are prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB) and as adopted by the European Union and were approved by the Board on July 14, 2010. Highlights - Revenue from continuing operations was $581 million (Q2 2009: $526 million) - Adjusted EBITDA(a) from continuing operations was $121 million (Q2 2009: $113 million) corresponding to an Adjusted EBITDA margin of 20.9% (Q2 2009: 21.5%) - Income from continuing operations was $63 million (Q2 2009: $76 million) - Strong cash and cash equivalents position of $631 million (February 28, 2010: $667 million) - Awarded $120 million Conventional contract, offshore Nigeria - As part of our ongoing fleet development programme, Acergy acquired two vessels post quarter end; the Polar Queen and the Antares, a shallow water barge for the West African Conventional market - Post quarter end, on June 21, 2010 the Boards of Directors of Acergy S.A. and Subsea 7 Inc. announced that they had agreed to combine the two companies Jean Cahuzac, Chief Executive Officer, said: “We have delivered a solid quarterly performance driven by excellent project execution, additional variation orders on ongoing projects and strong Conventional activity. We remain on track to deliver our 2010 expectations. In line with our strategy to develop the fleet, we acquired the Antares and Polar Queen, reinforcing our commitment to capture opportunities and invest in the business. -

RA BRS 2007 Int GB

Shipping and Shipbuilding Markets 2 0 0 7 Shipping and Shipbuilding Markets in 2006 THE BRS ANNUAL REVIEW OF WORLD SHIPPING AND SHIPBUILDING DEVELOPMENTS IN 2006 AND PROSPECTS FOR THE COMING MONTHS… 1 Foreword 3 The shipbuilding market in 2006 23 The cruise market in 2006 29 The tanker market in 2006 45 The offshore and specialised ships markets in 2006 51 The chemical carrier market in 2006 57 The liquefied petroleum gas shipping market in 2006 67 The liquefied natural gas shipping market in 2006 73 The dry bulk market in 2006 81 The containership market in 2006 97 The ro-ro market in 2006 101 The marine insurance markets in 2006 107 French shipyards deliveries and orderbook in 2006 110 French orders to foreign shipyards in 2006 Crystal Ball AFTER FOUR YEARS OF BUOYANT the world’s population, originating from SHIPPING MARKETS, GIVING STATIS- a group of countries known as B.R.I.C. TICS NEVER SEEN BEFORE, THERE (Brazil, Russia, India, China), in the global ARE A NUMBER OF DISQUIETING VOI- economy. CES BEING HEARD PREDICTING A However, recent forecasts published by SEVERE CORRECTION OF THE MARK- the World Bank over the next 25 years ETS OR EVEN A NEW CRISIS RECALL- lead us to believe that a collapse in the ING THE SAD DAYS OF THE 80’S. markets, following the historic increases, It is true that we are in a cyclical industry is neither a necessity nor a compulsory and that the current swelling of the passage. Certainly growth is seldom orderbooks, which equates to an average linear and we should prepare ourselves of 25 % of the existing fleet, and even for market corrections, linked to tempor- close to 50 % in some sectors, gives ary imbalances between supply and cause for concern even to the most demand, especially in the tanker and serene spirits. -

Acergy and Subsea 7 Agree to Combine

Acergy and Subsea 7 Agree to Combine Creating a global leader in seabed-to-surface engineering and construction Monday 21, 2010 Speakers • Karen Menzel – Group Manager, Investor Relations, Acergy S.A. • Kristian Siem – Chairman, Subsea 7 Inc. • Jean Cahuzac - Chief Executive Officer, Acergy S.A. • Mel Fitzgerald – Chief Executive Officer, Subsea 7 Inc. • Sir Peter Mason KBE – Chairman, Acergy S.A. Operator: Thank you for standing by and welcome to the Acergy and Subsea 7 Agree to Combine Conference Call. At this time, all participants are in a listen-only mode. There will be a presentation followed by question-and-answer session [Operator Instructions]. I must advise you that this conference is being recorded today, Monday, the 21st of June 2010 and I would now like to hand the conference over to your host today, Karen Menzel. Please go ahead, madam. Karen Menzel: Thank you and good afternoon. Joining us on the line today are: • Kristian Siem, Chairman of Subsea 7; • Sir Peter Mason, Chairman of Acergy; • Jean Cahuzac, Chief Executive Officer of Acergy; and • Mel Fitzgerald, Chief Executive Officer of Subsea 7. A copy of this morning’s announcement, along with the presentation slides we will be using during this call, can be found on Acergy’s and Subsea 7’s websites. Before we start the presentation may I remind you that certain statements contained in today’s communication and made in the course of this conference call, which express the two company’s intentions, beliefs and expectations are Page 1 of 28 forward-looking statements within the meaning of the US Federal Securities laws. -

The Bureau of Ocean Energy Management, Regulation and Enforcement

THE BUREAU OF OCEAN ENERGY MANAGEMENT, REGULATION AND ENFORCEMENT REPORT REGARDING THE CAUSES OF THE APRIL 20, 2010 MACONDO WELL BLOWOUT September 14, 2011 TABLE OF CONTENTS Executive Summary ................................................................................................1 I. Introduction ..................................................................................................... 10 A. The Investigation ......................................................................................... 10 B. Background Regarding Deepwater Drilling in the Gulf of Mexico ............ 13 C. Companies Involved in the Macondo Well.................................................. 16 D. The Deepwater Horizon............................................................................... 18 E. The Macondo Well....................................................................................... 19 F. The Blowout................................................................................................. 23 II. Well Design...................................................................................................... 25 A. Cost of the Macondo Well............................................................................ 25 B. Drilling Margin........................................................................................... 27 C. Casing Program........................................................................................... 31 D. Mud Program and Type ............................................................................. -

IN the UNITED STATES DISTRICT COURT for the EASTERN DISTRICT of LOUISIANA in Re: Oil Spill by the Oil Rig “Deepwater Horizon

Case 2:10-md-02179-CJB-DPC Document 14021 Filed 01/15/15 Page 1 of 44 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF LOUISIANA In re: Oil Spill by the Oil Rig “Deepwater * Horizon” in the Gulf of Mexico, * MDL 2179 on April 20, 2010, * * * SECTION J This Document Applies To: * * No. 10-2771, In re: The Complaint and Petition * JUDGE BARBIER of Triton Asset Leasing GmbH, et al. * * and * MAG. JUDGE SHUSHAN * No. 10-4536, United States of America v. BP * Exploration & Production, Inc., et al. * ——————————————————————————————————————— FINDINGS OF FACT AND CONCLUSIONS OF LAW PHASE TWO TRIAL Case 2:10-md-02179-CJB-DPC Document 14021 Filed 01/15/15 Page 2 of 44 Pursuant to Federal Rule of Civil Procedure 52(a), the Court enters these Findings of Fact and Conclusions of Law relative to the Phase Two trial. If any finding is in truth a conclusion of law or any conclusion stated is in truth a finding of fact, it shall be deemed so, labels notwithstanding. CONTENTS I. Introduction and Procedural History ................................................................................. 3 II. Source Control Segment ....................................................................................................... 5 A. Parties to the Source Control Segment ............................................................................. 5 B. Stipulated Facts; Timeline of Source Control Events ...................................................... 6 i. Terms and Definitions.....................................................................................................