M Ov Ie Sand E N Te Rta in Ment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

February 26, 2021 Amazon Warehouse Workers In

February 26, 2021 Amazon warehouse workers in Bessemer, Alabama are voting to form a union with the Retail, Wholesale and Department Store Union (RWDSU). We are the writers of feature films and television series. All of our work is done under union contracts whether it appears on Amazon Prime, a different streaming service, or a television network. Unions protect workers with essential rights and benefits. Most importantly, a union gives employees a seat at the table to negotiate fair pay, scheduling and more workplace policies. Deadline Amazon accepts unions for entertainment workers, and we believe warehouse workers deserve the same respect in the workplace. We strongly urge all Amazon warehouse workers in Bessemer to VOTE UNION YES. In solidarity and support, Megan Abbott (DARE ME) Chris Abbott (LITTLE HOUSE ON THE PRAIRIE; CAGNEY AND LACEY; MAGNUM, PI; HIGH SIERRA SEARCH AND RESCUE; DR. QUINN, MEDICINE WOMAN; LEGACY; DIAGNOSIS, MURDER; BOLD AND THE BEAUTIFUL; YOUNG AND THE RESTLESS) Melanie Abdoun (BLACK MOVIE AWARDS; BET ABFF HONORS) John Aboud (HOME ECONOMICS; CLOSE ENOUGH; A FUTILE AND STUPID GESTURE; CHILDRENS HOSPITAL; PENGUINS OF MADAGASCAR; LEVERAGE) Jay Abramowitz (FULL HOUSE; GROWING PAINS; THE HOGAN FAMILY; THE PARKERS) David Abramowitz (HIGHLANDER; MACGYVER; CAGNEY AND LACEY; BUCK JAMES; JAKE AND THE FAT MAN; SPENSER FOR HIRE) Gayle Abrams (FRASIER; GILMORE GIRLS) 1 of 72 Jessica Abrams (WATCH OVER ME; PROFILER; KNOCKING ON DOORS) Kristen Acimovic (THE OPPOSITION WITH JORDAN KLEPPER) Nick Adams (NEW GIRL; BOJACK HORSEMAN; -

Kijkwijzer (Netherlands Classification) Some Content May Not Be Appropriate for Children This Age

ACCM Kijkwijzer (Netherlands Classification) Some content may not be appropriate for children this age. Parental Content is age Kijkwijzer Australian guidance appropriate for (Netherlands Year Netflix Classification recommended children this age Classification) Kijkwijzer reasons 1 Chance 2 Dance 2014 N 12+ Violence 3 Ninjas: Kick Back 1994 N 6+ Violence; Fear 48 Christmas Wishes 2017 N All A 2nd Chance 2011 N PG All A Christmas Prince 2017 N 6+ Fear A Christmas Prince: The Royal Baby 2019 N All A Christmas Prince: The Royal Wedding 2018 N All A Christmas Special: Miraculous: Tales of Ladybug & Cat 2016 N Noir PG A Cinderella Story 2004 N PG 8 13 A Cinderella Story: Christmas Wish 2019 N All A Dog's Purpose 2017 N PG 10 13 12+ Fear; Drugs and/or alcohol abuse A Dogwalker's Christmas Tale 2015 N G A StoryBots Christmas 2017 N All A Truthful Mother 2019 N PG 6+ Violence; Fear A Witches' Ball 2017 N All Violence; Fear Airplane Mode 2020 N 16+ Violence; Sex; Coarse language Albion: The Enchanted Stallion 2016 N 9+ Fear; Coarse language Alex and Me 2018 N All Saints 2017 N PG 8 10 6+ Violence Alvin and the Chipmunks Meet the Wolfman 2000 N 6+ Violence; Fear Alvin and the Chipmunks: The Road Chip 2015 N PG 7 8 6+ Violence; Fear Amar Akbar Anthony 1977 N Angela's Christmas 2018 N G All Annabelle Hooper and the Ghosts of Nantucket 2016 N PG 12+ Fear Annie 2014 N PG 10 13 6+ Violence Antariksha Ke Rakhwale 2018 N April and the Extraordinary World 2015 N Are We Done Yet? 2007 N PG 8 11 6+ Fear Arrietty 2010 N G 6 9+ Fear Arthur 3 the War of Two -

Pr-Dvd-Holdings-As-Of-September-18

CALL # LOCATION TITLE AUTHOR BINGE BOX COMEDIES prmnd Comedies binge box (includes Airplane! --Ferris Bueller's Day Off --The First Wives Club --Happy Gilmore)[videorecording] / Princeton Public Library. BINGE BOX CONCERTS AND MUSICIANSprmnd Concerts and musicians binge box (Includes Brad Paisley: Life Amplified Live Tour, Live from WV --Close to You: Remembering the Carpenters --John Sebastian Presents Folk Rewind: My Music --Roy Orbison and Friends: Black and White Night)[videorecording] / Princeton Public Library. BINGE BOX MUSICALS prmnd Musicals binge box (includes Mamma Mia! --Moulin Rouge --Rodgers and Hammerstein's Cinderella [DVD] --West Side Story) [videorecording] / Princeton Public Library. BINGE BOX ROMANTIC COMEDIESprmnd Romantic comedies binge box (includes Hitch --P.S. I Love You --The Wedding Date --While You Were Sleeping)[videorecording] / Princeton Public Library. DVD 001.942 ALI DISC 1-3 prmdv Aliens, abductions & extraordinary sightings [videorecording]. DVD 001.942 BES prmdv Best of ancient aliens [videorecording] / A&E Television Networks History executive producer, Kevin Burns. DVD 004.09 CRE prmdv The creation of the computer [videorecording] / executive producer, Bob Jaffe written and produced by Donald Sellers created by Bruce Nash History channel executive producers, Charlie Maday, Gerald W. Abrams Jaffe Productions Hearst Entertainment Television in association with the History Channel. DVD 133.3 UNE DISC 1-2 prmdv The unexplained [videorecording] / produced by Towers Productions, Inc. for A&E Network executive producer, Michael Cascio. DVD 158.2 WEL prmdv We'll meet again [videorecording] / producers, Simon Harries [and three others] director, Ashok Prasad [and five others]. DVD 158.2 WEL prmdv We'll meet again. Season 2 [videorecording] / director, Luc Tremoulet producer, Page Shepherd. -

The Novel and Corporeality in the New Media Ecology

University of Rhode Island DigitalCommons@URI Open Access Dissertations 2017 "You Will Hold This Book in Your Hands": The Novel and Corporeality in the New Media Ecology Jason Shrontz University of Rhode Island, [email protected] Follow this and additional works at: https://digitalcommons.uri.edu/oa_diss Recommended Citation Shrontz, Jason, ""You Will Hold This Book in Your Hands": The Novel and Corporeality in the New Media Ecology" (2017). Open Access Dissertations. Paper 558. https://digitalcommons.uri.edu/oa_diss/558 This Dissertation is brought to you for free and open access by DigitalCommons@URI. It has been accepted for inclusion in Open Access Dissertations by an authorized administrator of DigitalCommons@URI. For more information, please contact [email protected]. “YOU WILL HOLD THIS BOOK IN YOUR HANDS”: THE NOVEL AND CORPOREALITY IN THE NEW MEDIA ECOLOGY BY JASON SHRONTZ A DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY IN ENGLISH UNIVERSITY OF RHODE ISLAND 2017 DOCTOR OF PHILOSOPHY DISSERTATION OF JASON SHRONTZ APPROVED: Dissertation Committee: Major Professor Naomi Mandel Jeremiah Dyehouse Ian Reyes Nasser H. Zawia DEAN OF THE GRADUATE SCHOOL UNIVERSITY OF RHODE ISLAND 2017 ABSTRACT This dissertation examines the relationship between the print novel and new media. It argues that this relationship is productive; that is, it locates the novel and new media within a tense, but symbiotic relationship. This requires an understanding of media relations that is ecological, rather than competitive. More precise, this dissertation investigates ways that the novel incorporates new media. The word “incorporate” refers both to embodiment and physical union. -

Sommario Rassegna Stampa

Sommario Rassegna Stampa Pagina Testata Data Titolo Pag. Rubrica Anica Web AGCULT.IT 10/12/2019 LEGGE CINEMA, FRANCESCHINI INCONTRA ANICA: DIALOGO E 3 CONFRONTO PROSEGUE PROSSIMA SETTIMANA Cinemaitaliano.info 11/12/2019 ANICA - IL MINISTRO FRANCESCHINI A DIALOGO CON LA FILIERA 5 DELL'AUDIOVISIVO Cineuropa.org 10/12/2019 TEN ITALIAN WORKS YET TO BE RELEASED IN FRANCE WILL BE 6 SHOWCASED IN DE ROME A' PARIS Espresso.Repubblica.it 10/12/2019 LA MINACCIA DEEPFAKE: QUANDO NON BASTA PIU' VEDERE PER 7 CREDERE Rai.it 10/12/2019 L'ARTE DEL COMPROMESSO NON E' IL MIO FORTE 10 Larecherche.it 11/12/2019 TUTTO IL CINEMA CHE VUOI... CINEUROPA NEWS :: 12 Spettacolomusicasport.com 10/12/2019 CONCLUSI GLI SDC DAYS 2019: IL PAPA PARLA AL MONDO DEL 19 CINEMA. OLTRE QUATTROCENTO PARTECIPANTI PER I Rubrica Cinema 1 Avvenire 11/12/2019 "PETRUNYA", UN FILM CONTRO IL MASCHILISMO (A.De Luca) 20 25 Avvenire 11/12/2019 DOCUFILM SUL PAPA FIGLIO DI MIGRANTI (T.Viola) 22 78/84 Chi 11/12/2019 FILM DELLE FESTE BUON NATALE AL CINEMA (M.Comolli) 23 1 Il Fatto Quotidiano 11/12/2019 Int. a J.Binoche: BINOCHE: "ECCO PERCHE' FUGGII DA 29 HOLLYWOOD" (F.Pontiggia) 22 Il Fatto Quotidiano 11/12/2019 TERTIO MILLENNIO FILM FESTIVAL 31 25 Il Messaggero 11/12/2019 IL NOSTRO PAPA, ARRIVA IN SALA IL DOCUFILM SU BERGOGLIO 32 (F.Giansoldati) 21 Il Tempo 11/12/2019 NUOVA VITA PER IL PICCOLISSIMO (L.Pri.) 33 19 La Gazzetta del Mezzogiorno 11/12/2019 UN "MIGRANTE" SUL SOGLIO DI PIETRO (D.Gallo) 34 21 La Repubblica - Cronaca di Roma 11/12/2019 GIOVANI ATTORI IN SALA RICORDANDO VOLONTE' 35 27 La Stampa 11/12/2019 GENERAZIONE "OK BOOMER" COSI' I GIOVANI REGISTI 36 RACCONTANO GLI OVER 50 (E.Santolini) 28 La Stampa 11/12/2019 Int. -

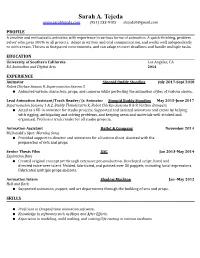

Sarah A. Tejeda (951) 233-9185 [email protected]

Sarah A. Tejeda www.sarahtejeda.com (951) 233-9185 [email protected] PROFILE A creative and enthusiastic animator, with experience in various forms of animation. A quick-thinking, problem solver who gives 100% to all projects. Adept in written and oral communication, and works well independently or with a team. Thrives in fast-paced environments, and can adapt to meet deadlines and handle multiple tasks. EDUCATION University of Southern California Los Angeles, CA BA Animation and Digital Arts 2014 EXPERIENCE Animator Stoopid Buddy Stoodios July 2017-Sept 2018 Robot Chicken Season 9, Supermansion Season 3 ● Animated various characters, props, and cameras while perfecting the animation styles of various shows. Lead Animation Assistant/Track Reader/ Jr. Animator Stoopid Buddy Stoodios May 2015-June 2017 Supermansion Seasons 1 & 2, Buddy Thunderstruck, Robot Chicken Seasons 8 & 9, Verizon Bumpers ● Acted as a fill-in animator for studio projects. Supported and assisted animators and crews by helping with rigging, anticipating and solving problems, and keeping areas and materials well-stocked and organized. Proficient track reader for all studio projects. Animation Assistant Hello! & Company November 2014 McDonald’s Spot: Morning Song ● Provided support to director and animators for a location shoot. Assisted with the preparation of sets and props. Senior Thesis Film USC Jan 2013-May 2014 Expiration Date ● Created original concept art through extensive pre-production. Developed script, hired and directed voice-over talent. Molded, fabricated, and painted over 30 puppets, including facial expressions. Fabricated multiple props and sets. Animation Intern Shadow Machine Jan -May 2012 Hell and Back ● Supported animation, puppet, and art departments through the building of sets and props. -

Wonder Wheel Metropole Press Kit.Pdf

Amazon Studios présente En association avec Gravier Productions Une production Perdido Durée : 1h41 AU CINÉMA DÈS LE 15 DÉCEMBRE DISTRIBUTION PRESSE MÉTROPOLE FILMS STAR PR 5360 St-Laurent Bonne Smith Montréal, QC H1T 2S1 Tel: 416-488-4436 Twitter: info@métropolefilms.com Bonne@starpr2 [email protected] Photos, vidéos et dossier de presse téléchargeables sur www.métropolefilms.com SYNOPSIS WONDER WHEEL croise les trajectoires de quatre personnages, dans l’effervescence du parc d’attraction de Coney Island, dans les années 50 : Ginny, ex-actrice lunatique reconvertie serveuse ; Humpty, opérateur de manège marié à Ginny ; Mickey, séduisant maître- nageur aspirant à devenir dramaturge ; et Carolina, fille de Humpty longtemps disparue de la circulation qui se réfugie chez son père pour fuir les gangsters à ses trousses. NOTES DE PRODUCTION Woody Allen a toujours éprouvé une grande tendresse pour Coney Island. des situations, à la fois complexes, profondes, intenses, déroutantes et fortes. Ce n’est d’ailleurs pas un hasard si, dans ANNIE HALL, le petit Alvy Singer Je me suis toujours intéressé aux problèmes des femmes. Au fil des siècles, les grandit à proximité du parc d’attraction. Le cinéaste en garde des souvenirs hommes ont eu tendance à exprimer moins volontiers leurs souffrances : le d’enfance joyeux : « Quand je suis né, l’époque florissante de Coney Island était mot d’ordre masculin consiste à ne pas avouer qu’on souffre. C’est comme dans déjà révolue depuis un bon moment, mais c’était encore un endroit magique le base-ball où, quand un “batteur” est touché par un “lanceur”, il est censé ne pour moi, confie-t-il. -

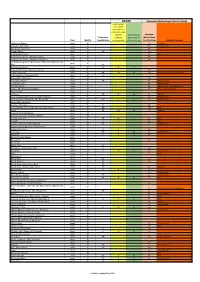

2017 DGA Episodic Director Diversity Report (By STUDIO)

2017 DGA Episodic Director Diversity Report (by STUDIO) Combined # Episodes # Episodes # Episodes # Episodes Combined Total # of Female + Directed by Male Directed by Male Directed by Female Directed by Female Male Female Studio Title Female + Signatory Company Network Episodes Minority Male Caucasian % Male Minority % Female Caucasian % Female Minority % Unknown Unknown Minority % Episodes Caucasian Minority Caucasian Minority A+E Studios, LLC Knightfall 2 0 0% 2 100% 0 0% 0 0% 0 0% 0 0 Frank & Bob Films II, LLC History Channel A+E Studios, LLC Six 8 4 50% 4 50% 1 13% 3 38% 0 0% 0 0 Frank & Bob Films II, LLC History Channel A+E Studios, LLC UnReal 10 4 40% 6 60% 0 0% 2 20% 2 20% 0 0 Frank & Bob Films II, LLC Lifetime Alameda Productions, LLC Love 12 4 33% 8 67% 0 0% 4 33% 0 0% 0 0 Alameda Productions, LLC Netflix Alcon Television Group, Expanse, The 13 2 15% 11 85% 2 15% 0 0% 0 0% 0 0 Expanding Universe Syfy LLC Productions, LLC Amazon Hand of God 10 5 50% 5 50% 2 20% 3 30% 0 0% 0 0 Picrow, Inc. Amazon Prime Amazon I Love Dick 8 7 88% 1 13% 0 0% 7 88% 0 0% 0 0 Picrow Streaming Inc. Amazon Prime Amazon Just Add Magic 26 7 27% 19 73% 0 0% 4 15% 1 4% 0 2 Picrow, Inc. Amazon Prime Amazon Kicks, The 9 2 22% 7 78% 0 0% 0 0% 2 22% 0 0 Picrow, Inc. Amazon Prime Amazon Man in the High Castle, 9 1 11% 8 89% 0 0% 0 0% 1 11% 0 0 Reunion MITHC 2 Amazon Prime The Productions Inc. -

Exploring Homelessness and Housing Insecurity in Chelsea, MA

Boston University MetroBridge Report: Exploring Homelessness and Housing Insecurity in Chelsea, MA Authors This report is a compilation of the work completed by Boston University graduate students in the Sociological Research Methods course instruct- ed by Assistant Professor Jessica Simes during the Fall 2018 semester. The content was compiled and edited by Stuti Das, PhD candidate in Sociol- ogy, and reviewed by Emily Robbins, MetroBridge Program Manager and Associate Professor David Glick, MetroBridge Faculty Director. This report was designed by Yufei Weng, master’s candidate in Graphic Design. Acknowledgments The MetroBridge program at Boston University’s Initiative on Cities wishes to thank our collaborators in the City of Chelsea for their assistance on this project, in particular: Tom Ambrosino, Chelsea City Manager; Luis Prado, Director of Health and Human Services; and Jessica Kahlenberg, Innovation and Strategy Advisor. We are also grateful for the service providers, city staff, and residents in Chelsea who participated in the interview process for this project. MetroBridge MetroBridge is a new Boston University program that empowers students across the university to tackle urban issues, and at the same time, helps city leaders confront key challenges. MetroBridge connects with local governments to understand their priorities, and then collaborates with Boston University faculty to translate each city’s unique needs into course projects. Students in undergraduate and graduate classes engage in city projects as class assignments while working directly with local govern- ment leaders during the semester. The goal of MetroBridge is to mutually benefit both the Boston University community and local governments by expanding access to experiential learning and by providing tailored sup- port to under-resourced cities. -

Netflix and the Development of the Internet Television Network

Syracuse University SURFACE Dissertations - ALL SURFACE May 2016 Netflix and the Development of the Internet Television Network Laura Osur Syracuse University Follow this and additional works at: https://surface.syr.edu/etd Part of the Social and Behavioral Sciences Commons Recommended Citation Osur, Laura, "Netflix and the Development of the Internet Television Network" (2016). Dissertations - ALL. 448. https://surface.syr.edu/etd/448 This Dissertation is brought to you for free and open access by the SURFACE at SURFACE. It has been accepted for inclusion in Dissertations - ALL by an authorized administrator of SURFACE. For more information, please contact [email protected]. Abstract When Netflix launched in April 1998, Internet video was in its infancy. Eighteen years later, Netflix has developed into the first truly global Internet TV network. Many books have been written about the five broadcast networks – NBC, CBS, ABC, Fox, and the CW – and many about the major cable networks – HBO, CNN, MTV, Nickelodeon, just to name a few – and this is the fitting time to undertake a detailed analysis of how Netflix, as the preeminent Internet TV networks, has come to be. This book, then, combines historical, industrial, and textual analysis to investigate, contextualize, and historicize Netflix's development as an Internet TV network. The book is split into four chapters. The first explores the ways in which Netflix's development during its early years a DVD-by-mail company – 1998-2007, a period I am calling "Netflix as Rental Company" – lay the foundations for the company's future iterations and successes. During this period, Netflix adapted DVD distribution to the Internet, revolutionizing the way viewers receive, watch, and choose content, and built a brand reputation on consumer-centric innovation. -

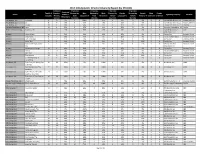

Fidelity® Total Market Index Fund

Quarterly Holdings Report for Fidelity® Total Market Index Fund May 31, 2021 STI-QTLY-0721 1.816022.116 Schedule of Investments May 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 99.3% Shares Value Shares Value COMMUNICATION SERVICES – 10.1% World Wrestling Entertainment, Inc. Class A (b) 76,178 $ 4,253,780 Diversified Telecommunication Services – 1.1% Zynga, Inc. (a) 1,573,367 17,055,298 Alaska Communication Systems Group, Inc. 95,774 $ 317,970 1,211,987,366 Anterix, Inc. (a) (b) 16,962 838,941 Interactive Media & Services – 5.6% AT&T, Inc. 11,060,871 325,521,434 Alphabet, Inc.: ATN International, Inc. 17,036 805,292 Class A (a) 466,301 1,099,001,512 Bandwidth, Inc. (a) (b) 34,033 4,025,764 Class C (a) 446,972 1,077,899,796 Cincinnati Bell, Inc. (a) 84,225 1,297,065 ANGI Homeservices, Inc. Class A (a) 120,975 1,715,426 Cogent Communications Group, Inc. (b) 66,520 5,028,912 Autoweb, Inc. (a) (b) 6,653 19,028 Consolidated Communications Holdings, Inc. (a) 110,609 1,035,300 Bumble, Inc. 77,109 3,679,641 Globalstar, Inc. (a) (b) 1,067,098 1,707,357 CarGurus, Inc. Class A (a) 136,717 3,858,154 IDT Corp. Class B (a) (b) 31,682 914,343 Cars.com, Inc. (a) 110,752 1,618,087 Iridium Communications, Inc. (a) 186,035 7,108,397 DHI Group, Inc. (a) (b) 99,689 319,005 Liberty Global PLC: Eventbrite, Inc. (a) 114,588 2,326,136 Class A (a) 196,087 5,355,136 EverQuote, Inc. -

A Documentary Film Romeoisbleedingfilm.Com Is Bleeding SYNOPSIS

AUDIENCE AWARD BEST DOCUMENTARY FEATURE SAN FRANCISCO INTʼL FILM FESROMEOT A Documentary Film RomeoIsBleedingFilm.com IS BLEEDING SYNOPSIS From Executive Producer Russell Simmons and Director Jason Zeldes, comes an award-winning documentary following Donté Clark, a young poet transcending the violence in his hometown by writing about his experiences. Growing DAMN up in Richmond, CA, a city haunted by a fatal WHERE I’M FROM BULLETS FLY FROM turf war, Donté and the like-minded youth BLACK HANDS TO BE LODGED IN THE HEAD of the city mount an OF A BLACK MAN. WE urban adaptation of Shakespeare’s Romeo and Juliet, with the hope of starting a dialogue about violence in the city. Will Richmond crush Donté’s idealism? Or will Donté end Richmond’s cycle of trauma? LOSING romeo is bleeding • a documentary film bacKground Donté Clark’s poetry captures the violence and heartbreak that haunt certain neighborhoods of richmond, ca. the turf war between North and Central Richmond has raged for decades, with each generation having their own folkloric stories of how the war began. Donté was born in the heart of North Richmond, but found self-empowerment by writing about his experiences there. Now as a young man, Donté offers that same opportunity to Richmond’s youth, through an arts organization called RAW talent. “Romeo is Bleeding” is structured around one year in the raW talent classroom, as donté leads a cast of high school students in an effort to mount an urban adaptation of “Romeo and Juliet”. As Montague vs. Capulet transforms into North vs.