Abu Dhabi Real Estate Report Q4 2016 Content

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sample 20. UAE: Abu Dhabi

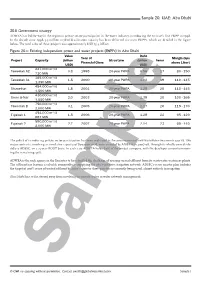

Sample 20. UAE: Abu Dhabi 20.11 Government strategy ADWEA has led the way in the region in private sector participation in the water industry, introducing the emirate’s first IWPP in 1998. In the decade since 1998, 3.3 million m3/d of desalination capacity has been delivered via seven IWPPs, which are detailed in the figure below. The total value of these projects was approximately USD 13.4 billion. Figure 20.x: Existing independent power and water projects (IWPPs) in Abu Dhabi Value Debt Year of Margin (bps Project Capacity (billion Structure (billion Tenor Financial Close above Libor) USD) USD) 227,000 m³/d Taweelah A2 0.8 1998 20-year PWPA 0.56 17 80 - 150 710 MW 385,000 m³/d Taweelah A1 1.5 2000 20-year PWPA 1.02 19 110 - 145 1,350 MW 454,000 m³/d Shuweihat 1.8 2001 20-year PWPA 1.28 20 110 - 145 1,500 MW 430,000 m³/d Umm al-Nar 2.0 2003 20-year PWPA 1.39 20 100 - 165 1,550 MW 750,000 m³/d Taweelah B 3.1 2005 20-year PWPA 2.17 20 115 - 170 2,000 MW 454,000 m³/d Fujairah 1 1.5 2006 20-year PWPA 1.28 22 65 - 120 887 MW 590,000 m³/d Fujairah 2 2.7 2007 20-year PWPA 2.14 23 65 - 110 2,000 MW The policy of introducing private sector participation has been replicated in the procurement of new wastewater-treatment capacity. Two major contracts, involving a cumulative capacity of 800,000 m3/d, were awarded by ADWEA in 2007-08, through its wholly owned sub- sidiary ADSSC, on a 25-year BOOT basis. -

Valustrat Abu Dhabi Real Estate Review Q2 2021

Abu Dhabi Real Estate Market 2021 Quartely Review www.valustrat.com 2nd Quarter Market Intelligence. VPI Simplified. ValuStrat Price Index REAL ESTATE PERFORMANCE VPI Residential VPI Residential Capital Values Rental Values 67.3 77.7 Base: Q1 2016=100 Base: Q1 2016=100 2.1% 4.3% Q-o-Q Q-o-Q Source: ValuStrat KEY INDICATORS Source: ValuStrat, REIDIN, STR Apartment Villa Apartment Villa Asking Sales Price Asking Sales Price Asking Rents Asking Rents 12,491 10,596 118,000 213,700 AED/sq m AED/sq m 2 Bedrooms (AED p.a.) 4 Bedrooms (AED p.a.) 3.5% 9.3% 4.9% 3.6% Q-o-Q Q-o-Q Q-o-Q Q-o-Q Hotel Hotel Office Office Average Daily Rate Occupancy Asking Sales Price Asking Rents 481.5 62% 10,370 860 (AED) Mar 2021 Mar 2021 AED/sq m AED/sq m p.a. 18.6% 4.2% -10.1% 1.9% Y-o-Y Y-o-Y Q-o-Q Q-o-Q Increase Stable Decline 1 | Abu Dhabi Real Estate Market 2nd Quarter 2021 Review Market Intelligence. VPI Simplified. ValuStrat Price Index RESIDENTIAL The valuation based ValuStrat Price VPI - ABU DHABI RESIDENTIAL CAPITAL VALUES Index (VPI) for capital values in 5 Villa and 5 Apartment Locations Abu Dhabi’s residential investment [Base: Q1 2016=100] zones for the second quarter 2021, increased 2.1% quarterly to 65.8 points. This was the first time the 4.1% VPI has witnessed three consecutive 92.4 90.3 88.5 87.1 85.5 83.8 quarters of growth since 2016, 81.1 2.1% 77.6 75.1 72.7 70.9 69.1 aggregating 7.2% since Q4 2020. -

Case Study: Gate Towers, Abu Dhabi

ctbuh.org/papers Title: Case Study: Gate Towers, Abu Dhabi Authors: Gurjit Singh, Chief Development Officer, Aldar Properties Hossam Eldin Elsouefi, Senior Project Manager, Aldar Properties Peter Brannan, Managing Director, Arquitectonica Subjects: Architectural/Design Building Case Study Keywords: Construction Design Process Façade Skybridges Publication Date: 2013 Original Publication: CTBUH Journal, 2013 Issue IV Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Gurjit Singh; Hossam Eldin Elsouefi; Peter Brannan About the Council The Council on Tall Buildings and Urban Habitat, based at the Illinois Institute of CTBUH Journal Technology in Chicago, is an international International Journal on Tall Buildings and Urban Habitat not-for-profi t organization supported by architecture, engineering, planning, development, and construction professionals. Founded in 1969, the Council’s mission is to disseminate multi-disciplinary information on Tall buildings: design, construction, and operation | 2013 Issue IV tall buildings and sustainable urban environments, to maximize the international interaction of professionals involved in creating Case Study: Gate Towers, Abu Dhabi the built environment, and to make the latest knowledge available to professionals in a useful Designing Tall to Promote Physical Activity in China form. The Monadnock Building, Technically Reconsidered The CTBUH disseminates -

Valustrat Abu Dhabi Real Estate Review Q4 2019

Real Estate Market 4th Quarter | 2019 Review VPI Residential VPI Residential Real Capital Values Rental Values Estate 69.1 71.5 Performance (Base Q1 2016=100) (Base Q1 2016=100) -11.0% -9.3% Y-o-Y Y-o-Y Market Intelligence. VPI Simplified. ValuStrat Price Index Source: ValuStrat Key Indicators Source: ValuStrat, REIDIN, DCTAD Apartment Asking Villa Asking Apartment Villa Sales Price Sales Price Asking Rents Asking Rents 13,005 9,943 112,500 187,734 AED/sq m AED/sq m 2 Bedrooms (AED p.a.) 4 Bedrooms (AED p.a.) -1.6% -3.4% -2.8% -3.6% Q-o-Q Q-o-Q Q-o-Q Q-o-Q Hotel Average Hotel Office Asking Office Asking Room Rate Occupancy Sales Price Rents 343 73% 10,889 827 (AED) Jan-Sep Jan-Sep AED/sq m AED/sq m p.a. 10.9% 1.1% 2.5% -1.1% Y-o-Y Y-o-Y Q-o-Q Q-o-Q Increase Stable Decline 1 | Abu Dhabi Real Estate Market 4th Quarter 2019 Review VPI ValuStrat Price Index Residential The valuation based ValuStrat Price VPI - Abu Dhabi Residential Capital Values Index (VPI) for capital values in Abu 5 Villa and 5 Apartment Locations Dhabi’s residential investment zones [Base: Q1 2016=100] for the fourth quarter 2019, declined 2.6% quarterly to 69.1 points. Annually, capital values were 11% 120 100.0 lower than the fourth quarter 2018. 96.4 95.4 94.1 100 92.4 90.3 88.5 87.1 85.5 83.8 81.1 The weighted average residential 77.6 80 75.1 72.7 value this quarter was AED 9,246 per 70.9 69.1 sq m (AED 859 per sq ft), apartments stood at AED 10,236 per sq m (AED 60 951 per sq ft), and villas at AED 6,910 per sq m (AED 642 per sq ft). -

EBP Network List JANUARY 2019

This list is provided by MedNet UAE to present information only regarding Participating Network Providers. All decisions about the type of care are the responsibility of the patient and the selected Physician. While every effort is made to maintain accurate information, MedNet UAE reserves the right to periodically coNduct modificatioNs as Provider ParticipatioN is updated. We request that Provider ParticipatioN be coNfirmed prior to hospitalizatioN. ImportaNt Note: Visiting doctors at the below providers who are not following contractual rates will not be available on direct billing access. **Government FacilitIes, eligible for contracted Insurance Companies only ABU DHABI AJMAN DUBAI FUJAIRAH SHARJAH RAS AL KHAIMAH UMM AL QUWAIN PROVIDER LICENSE CODE NAME OF PROVIDER EMIRATE REGION ADDRESS SPECIALITY TELEPHONE TYPE NUMBER EBP IP EBP OP GENERAL PRACTICE,INTERNIST,OB-GYNE, H619 NMC ROYAL WOMENS -ABU DHABI / MF3186 HOSPITAL ABU DHABI ABU DHABI ABU DHABI MF3186 02-5082000 ✓ PSYCHIA,PEDIA,UROLOGY H626 SEHA EMIRATES HOSPITAL HOSPITAL ABU DHABI ABU DHABI AL LEDEEM STREET MF2522 GENERAL PRACTICE 02-4438999 ✓ H207 AL RAHA HOSPITAL HOSPITAL ABU DHABI ABU DHABI AL NAJDA STREET , SECOND FLOOR , HYPER MARKET BUILDING MF254 MULTI-SPECIALITY 02-6330440 ✓ H419 LIFECARE HOSPITAL HOSPITAL ABU DHABI ABU DHABI BANIYAS STREET, WATHBA, GATE NO. 6 AL RAHA VILLAGE MF2349 MULTI-SPECIALITY 02-5856333 ✓ H4 NMC SPECIALTY HOSPITAL HOSPITAL ABU DHABI ABU DHABI ELECTRA STREET, AL KAMAL TOWERS MF394 MULTI-SPECIALITY 02-6332255 ✓ H172 LLH HOSPITAL L.L.C./MF1954 (FORM LIFELINE HOSPITAL) HOSPITAL ABU DHABI ABU DHABI ELECTRA STREET, AL MARWA BUILDING MF1954 MULTI-SPECIALITY 02-6335522 ✓ H6 AHALIA HOSPITAL HOSPITAL ABU DHABI ABU DHABI HAMDAN STREET, OPPOSITE BANK OF BARODA. -

Alkoot Insurance & Reinsurance UAE Network Providers List

AlKoot Insurance & Reinsurance Partner Contact Details: UAE network providers list Partner name: Vidal Health Tel: +91 80 491 66 777 Email: [email protected] Agreement type Provider Name Provider Type Provider Address City Country Partner UAE ABU SALMAN MEDICAL CENTRE CLINIC/POLYCLINIC Bldg 313, Flat 202, Near Islam Abad Pharmacy, Sector 10 Main Taxi Road Abu Dhabi UAE Partner ADVANCED CENTRE FOR DAYCARE SURGERY HOSPITAL Jasmine Tower Bldg, Beside RAK Bank Abu Dhabi UAE Partner AILABOUNI MEDICAL CLINIC CLINIC/POLYCLINIC Emirates Kitchen Equipment Bldg, Al Salam Street, Opp. AUH Municipality Abu Dhabi UAE Partner AL AFDAL PHARMACY PHARMACY ELECTRA STREET NEAR AL DHAFRA INSURANCE CO. PO BOX 131465 Abu Dhabi UAE Partner AL AHALIA NATIONAL PHARMACY`- BRANCH 1 PHARMACY Ahalia Hospital Musaffah Building Abu Dhabi UAE Partner AL AHLI HOSPITAL CO LLC BRANCH-1 HOSPITAL M 24, Musaffah, Near BMW Show Room, Abu Dhabi- Tarif Road Abu Dhabi UAE Partner AL AHLI HOSPITAL COMPANY L.L.C (ABU DHABI) HOSPITAL AHALIA HOSPITAL, HAMDANST. ABU DHABI, U.A.E Abu Dhabi AL AHLI HOSPITAL COMPANY LLC OP PHARMACY (ABU UAE Partner DHABI) PHARMACY Ahalia Hospital, Hamdan street, Abu Dhabi, UAE Abu Dhabi UAE Partner AL AHLIA CENTRAL PHARMACY (ABU DHABI) PHARMACY Hamdan Street, Abu Dhabi Abu Dhabi UAE Partner AL AHLIA NATIONAL PHARMACY LLC (ABU DHABI) PHARMACY Tariff Road, M-24 Mussafah, Abu Dhabi Abu Dhabi UAE Partner AL AIN ALAHILI MEDICAL CENTRE (AL AIN) CLINIC/POLYCLINIC SHABIYA KHALIFA STREET, NEAR NBAD BANK, AL AIN, U.A.E. Abu Dhabi UAE Partner AL AMEEN MEDICAL CENTRE (ABU DHABI) CLINIC/POLYCLINIC 37 Industrial Area, Near Best Bangla Supermarket Abu Dhabi UAE Partner AL AMEEN MEDICAL CENTRE LLC CLINIC/POLYCLINIC NEW VOLVO SHOWROOM, IST FLOOR, ELECTRA SHEIKH ZAYED 2 STREET, Abu Dhabi Partner AL BUSTAN HOSPITAL PHARMACY LLC PHARMACY PLOT NO. -

Sustainable Desirable Reliable

SUSTAINABLE DESIRABLE RELIABLE ALDAR PROPERTIES ANNUAL REPORT 2020 About Us Aldar Properties PJSC is the leading real estate SUSTAINABLE CONTENTS We aim to create a business culture where STRATEGIC REPORT developer, manager and owner in Abu Dhabi and sustainability is at the heart of everything we 2 Financial Highlights do, and where the concept of sustainability 4 Highlights of 2020 informs the way we operate, collaborate, through its iconic developments, it is one of the At a Glance innovate and grow. Our responsibility towards 8 most well known in the United Arab Emirates our stakeholders, the community, and the 10 Chairman’s Statement environment will continue to drive our business 12 Chief Executive Officer’s and the wider Middle East region. decisions and long-term value creation. Statement Statement 14 Why Abu Dhabi? Read more on page 20. 20 Case Studies Since Aldar was established, it has 26 Business Model continued to shape and enhance the DESIRABLE 28 Our Strategy urbanisation of the UAE’s capital city Customers are at the heart of all aspects of our 32 Our Strategic Themes by delivering desirable destinations business. Our mission is to create exceptional 42 Sustainability where communities can work, live and and memorable experiences that maximise 48 Operational Review value for all customers and outperform their visit. Those destinations include Yas 76 Financial Review Island, Reem Island, Al Raha Beach, expectations. We are engaged with our 80 EPRA Reporting Saadiyat Island and now Mina Zayed. customers in all areas of the customer journey from design and development, to purchase 84 Historical Financial Performance and handover to ensure a better process and 86 Risk Management increased satisfaction. -

List of Projects

084-CB-QMS / EMS / OHSMS ISO 9001:2015, ISO 14001:2015 & OHSAS 18001:2007 01-26 01 02 03 05 07 08 09 10 11 13 14 15 24 25 PAGE 01 PAGE 02 PAGE 03 PAGE 04 Abi Baker El Siddique Road Riyadh, KSA Abu Dhabi International Airport - Midfield Terminal Building Abu Dhabi, UAE ADIC Development Tower Abu Dhabi, UAE ADNIC Project Abu Dhabi, UAE ADNOC 7010C1 - Ruwais Housing Complex Expansion Phase IV, New Water Pipeline Abu Dhabi, UAE ADNOC New Medical Centre at Khalidiya Villas Abu Dhabi, UAE Al Bustan Street North (P007 C7 P2) Doha, Qatar Al Furjan Dubai, UAE Al Mafraq Interchange Abu Dhabi, UAE Al Marjan Island Development for Island 3 & 4 Ras Al Khaima, UAE Al Maryah Island Infrastructure Abu Dhabi, UAE Al Ra'idah Housing Complex at Jeddah Riyadh, KSA Al Reef Villas Abu Dhabi, UAE Al Reem Island Development, Plot 4, Central Business District of Plot RT-4-C33, Abu Dhabi, UAE C34, C38 and C39 ADNOC Consultancy Agreement Abu Dhabi, UAE Chilled Water Piping Network at Sector 2 & 3, Canal South & North Side Abu Dhabi, UAE Tamouh, Reem Island Danet Abu Dhabi District Cooling Works Abu Dhabi, UAE Development of Eastern Part of King Abdullah Road Riyadh, KSA Development of Roads in Dubai & All Infrastructure Works Dubai, UAE Dragon Mart Dubai, UAE Eastern Part of King Abdullah Road (P2B1) Riyadh, KSA Eastern Province - Water Transmission System Dammam, KSA Empower Project Dubai, UAE EPC Project with ARAMCO at Eastern Province Riyadh, KSA Falcon Eye Project in 7089 Drive 1 Zone D1 & D2 Abu Dhabi, UAE PAGE 05 Fire Station at Al Meena Abu Dhabi, UAE Ibn Battuta Mall Expansion - E4 & E5 Buildings Dubai, UAE ICAD Project, 992 Abu Dhabi, UAE Infrastructure Project in West Bank Palestine Jerusalem, Palestine Internal Roads and Services in Al Rahba City Abu Dhabi, UAE Lusail Commercial Boulevard - Public Realm Doha, Qatar Mafraq to Al Ghwaifat Border Post Highway Section No. -

Abu Dhabi Report H22012

Abu Dhabi Report H2 2012 “2012 was a pivotal year for the Abu Dhabi real estate market with the delivery of significant new developments which have raised the quality of living and working standards in the capital. The residential sub-sectors are now becoming more clearly defined by qualitative factors with tenants seeking value for money. In 2013 we expect to see a widening segregation in rental rates between the popular new developments, which, with occupancy levels rising, will be able to sustain rental levels and in some cases achieve growth, and the less popular older stock, that will continue to see rents come under downward pressure as landlords compete to maintain occupancy.“ Paul Maisfield, Associate Director & General Manager Abu Dhabi, Asteco Property Management Abu Dhabi Supply Estimates 2012 New Supply 2013 Scheduled New Supply Average Apartment Rental Rates (AED’000/pa) Apartments (in units) 9,000 12,000 Studio 1 BR 2 BR 3 BR Villas (in units) 6,000 5,000 From To From To From To From To Offices (in m2) 312,000 290,000 Marasy -- 87 110 135 170 185 237 Marina Square 55 65 75 85 110 130 140 180 Nation Towers - - 95 100 145 170 165 300 Reef Downtown - - 55 65 70 75 85 95 Residential Market Overview Rihan Heights -- 95 122 130 150 155 190 We estimate that approximately 15,000 new homes have been delivered to the Abu Dhabi market Saadiyat Beach Apartments -- 81 128 130 163 165 206 over the course of 2012, with a further 17,000 scheduled for completion in 2013. -

Infrastructure

INFRASTRUCTURE The new era of economic transition is characterised by public-private partnerships that are playing key roles in infrastructure development. 165 INFRASTRUCTURE The booming UAE economy, as outlined in the previous chapter, is fuelling infrastructure development on an unprecedented scale. This has been depicted as a ‘new era of economic transition’, characterised by a public-private partnership that is gradually taking over the role traditionally held by government in infrastructure development. Housing, tourist, industrial and commercial facilities, education and healthcare amenities, transportation, utilities, communications, ports and airports are all undergoing massive redevelopment, radically altering the urban environment in the UAE. Reform of property laws has also added impetus to urban development. URBAN DEVELOPMENT ABU DHABI Housing, tourist, In Abu Dhabi more than US$100 billion (Dh367 billion) will be industrial and invested over the next four to five years on infrastructure commercial projects. In addition to major investment in energy and industry, facilities, plans include a new airport, a new world-scale port and education and industrial zone in Taweelah, another port and industrial zone healthcare at Mussafah, the 11,000-unit Showayba City at Mussaffah, amenities, Mohammed bin Zayed City, the completion of several projects at transportation, Shahama, Khalifa Cities A and B, and the building of massive utilities, mixed-use communities on Saadiyat Island, Reem Island, Lulu communications, Island and at Al Raha Beach. Many of these projects will also go ports and some way towards meeting the infrastructural needs of a rapidly airports are all increasing and urbanised population. Abu Dhabi has embarked on a major undergoing Abu Dhabi has already embarked on a major remodelling of remodelling of buildings and roads in the massive city centre. -

Abu Dhabi Skyline Assessment of the Key Drivers of City Success

World Winning Cities Real value in a changing world Global Foresight Series A wobrlduwinnDing chityainbthei making World Winning Cities Jones Lang LaSalle’s World Winning Cities programme is a multi-year research initiative designed to assess future city competitiveness and to predict the rising urban stars amongst the world’s emerging markets in Asia, Central and Eastern Europe, North Africa, the Middle East and Latin America. The programme was launched in 2002 and over the past six years we have assessed the city competitiveness of many of the world’s emerging cities, based on rigorous and objective Cover: The Abu Dhabi skyline assessment of the key drivers of city success. Our research covers not only the standard Abu Dhabi is in a measures of future performance (relating to the economy and demography), but we have also strong position to developed a framework for embracing softer metrics such as sustainability, quality of life, culture and city governance; issues that are just as crucial in determining a city’s long term success. punch well above its weight in terms of In our first study back in 2002, we highlighted Dubai as being amongst a new wave of city winners, influence on the world possessing many of the pre-conditions to develop into a “World Winning City”. Dubai is now firmly stage. We believe the established as one of 21 Emerging World Winning Cities; cities that have achieved success through a city is on its way to variety of attributes ranging from economic size, global influence, human resources and infrastructure becoming a city of investment through to socio-cultural dynamism, innovation capability and strong, visionary governance. -

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 a B C D E F G N

A B C D E F G N O P 1 2 Important Note: Visiting doctors at the below providers who are not following contractual rates will not be available on direct billing access. Gold PROVIDER Dental NAME OF PROVIDER EMIRATE ADDRESS SPECIALITY TELEPHONE TYPE Alternative Vaccination 3 4 BRIGHT POINT HOSPITAL HOSPITAL ABU DHABI Abu Dhabi GENERAL PRACTICE,INTERNIST,OB-GYNE,02-5082000 ✓ PSYCHIA,PEDIA,UROLOGY 5 UNIVERSAL HOSPITAL LLC - ABU DHABI HOSPITAL ABU DHABI Airport Road, Behind Abu Dhabi Educational Council MULTI-SPECIALITY 02-6435555 ✓ 6 AL NOOR HOSPITAL HOSPITAL ABU DHABI Airport Road, Shk. Mohd Bin Butti Bldg. MULTI-SPECIALITY 02-4446655 ✓ 7 MAGRABI SPECIALIZED HOSPITAL- BRANCH HOSPITAL ABU DHABI Al Khaleej Al Arabi Street, Al Mushrif OPHTHALMOLOGY 02-4446565 ✓ 8 IMPERIAL COLLEGE LONDON DIABETES CENTRE HOSPITAL ABU DHABI Al Khaleej Al Arabi Street, Embasies Area NEPHROLOGY,DIABETOLOGIST,OPTHALMOLOGY,FAMILY02-4040800 ✓ MEDICINE,GENERAL PRACTICE,INTERNAL MEDICINE,ENDOCRINOLOY 9 GULF DIAGNOSTIC CENTER HOSPITAL HOSPITAL ABU DHABI Al Khaleej Al Arabi Street, Musasfa Road , After Shk Mohammed Palace CARDIOGENERAL SURGEONDERMA,ENDO,ORTHO,ENT,PED,URO02-6658090 ✓ 10 SEHA EMIRATES HOSPITAL HOSPITAL ABU DHABI Al Ledeem Street GENERAL PRACTICE 02-4438999 ✓ Al Maqam Tower, Al Falah Street, Abu Dhabi Global Market Square, Al Maryah CLEVELAND CLINIC ABU DHABI LLC HOSPITAL ABU DHABI GENERAL PRACTICE, ANESTHESIOLOGY,CARDIOLOGY,02-6590200 ✓ GASTROENTEROLOGY, INTERNAL MEDICINE, PULMONOLOGY, CRITICAL CARE MEDICINE, OPTHALMOLOGY, GENERAL SURGERY, VASCULAR SURGERY, CARDIOTHORACIC SURGERY, NEUROLOGY, PAIN MANAGEMENT, 11 Island 12 DAR AL SHIFA HOSPITAL HOSPITAL ABU DHABI Al Najda Street , Corner Of Defense Road MULTI-SPECIALITY 02-6416999 ✓ 13 AL RAHA HOSPITAL HOSPITAL ABU DHABI Al Najda Street , Second Floor , Hyper Market Building MULTI-SPECIALITY 02-6330440 ✓ ✓ 14 MAGRABI EYE & EAR CENTER HOSPITAL ABU DHABI Baniyas Street, Al Nakheel Tower OPTHA,ENT 02-6345000 ✓ 15 LIFECARE HOSPITAL HOSPITAL ABU DHABI Baniyas Street, Wathba, Gate No.