Residential Leasing October 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hong Kong Monthly

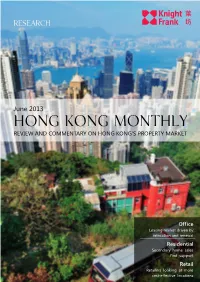

Research June 2013 Hong Kong Monthly REVIEW AND COMMENTARY ON HONG KONG'S PROPERTY MARKET Office Leasing market driven by relocation and renewal Residential Secondary home sales find support Retail Retailers looking at more cost-effective locations1 June 2013 Hong Kong Monthly Market in brief The following table and figures present a selection of key trends in Hong Kong‟s economy and property markets. Table 1 Economic indicators and forecasts Latest 2013 Economic indicator Period 2011 2012 reading forecast GDP growth Q1 2013 +2.8% +4.9% +1.4% +3.0% Inflation rate Apr 2013 +4.0% +5.3% +4.1% +4.4% Feb 2013- Unemployment 3.5%# 3.4% 3.1% 3.2% Apr 2013 Prime lending rate Current 5.00–5.25% 5.0%* 5.0%* 5.0%* Source: EIU CountryData / Census & Statistics Department / Knight Frank # Provisional * HSBC prime lending rate Figure 1 Figure 2 Figure 3 Grade-A office prices and rents Luxury residential prices and rents Retail property prices and rents Jan 2007 = 100 Jan 2007 = 100 Jan 2007 = 100 250 190 350 230 170 300 210 190 150 250 170 130 150 200 130 110 150 110 90 90 100 70 70 50 50 50 2007 2008 2009 2010 2011 2012 2013 2007 2008 2009 2010 2011 2012 2013 2007 2008 2009 2010 2011 2012 2013 Price index Rental index Price index Rental index Price index Rental index Source: Knight Frank Source: Knight Frank Source: Rating and Valuation Department / Knight Frank Note: Provisional figures from Oct 2012 to Mar 2013 2 2 KnightFrank.com.hk Monthly review Property sales were quiet in May, due to the implementation of the Double Stamp Duty on all property sectors in February and the Residential Properties (First-hand Sales) Ordinance on the residential sector in April. -

CT Catalyst Air Purification Service Job Reference of Residence

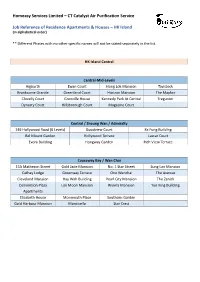

Homeasy Services Limited – CT Catalyst Air Purification Service Job Reference of Residence Apartments & Houses – HK Island (in alphabetical order) ** Different Phases with no other specific names will not be stated separately in the list. HK Island Central Central-Mid-Levels Aigburth Ewan Court Hong Lok Mansion Tavistock Branksome Grande Greenland Court Horizon Mansion The Mayfair Clovelly Court Grenville House Kennedy Park At Central Tregunter Dynasty Court Hillsborough Court Magazine Court Central / Sheung Wan / Admiralty 149 Hollywood Road (6 Levels) Goodview Court Ka Fung Building Bel Mount Garden Hollywood Terrace Lascar Court Evora Building Hongway Garden Rich View Terrace Causeway Bay / Wan Chai 15A Matheson Street Gold Jade Mansion No. 1 Star Street Sung Lan Mansion Cathay Lodge Greenway Terrave One Wanchai The Avenue Cleveland Mansion Hay Wah Building Pearl City Mansion The Zenith Convention Plaza Lok Moon Mansion Riviera Mansion Yue King Building Apartments Elizabeth House Monmouth Place Southorn Garden Gold Harbour Mansion Monticello Star Crest Happy Valley / East-Mid-Levels / Tai Hang 99 Wong Nai Chung Rd High Cliff Serenade Village Garden Beverly Hill Illumination Terrace Tai Hang Terrace Village Terrace Cavendish Heights Jardine's Lookout The Broadville Wah Fung Mansion Garden Mansion Celeste Court Malibu Garden The Legend Winfield Building Dragon Centre Nicholson Tower The Leighton Hill Wing On Lodge Flora Garden Richery Palace The Signature Wun Sha Tower Greenville Gardens Ronsdale Garden Tung Shan Terrace Hang Fung Building -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of buildings with confirmed / probable cases of COVID-19 List of residential buildings in which confirmed / probable cases have resided (Note: The buildings will remain on the list for 14 days since the reported date) Related confirmed / probable District Building name case number Wan Chai St. Regis Hong Kong 230, 264 Eastern Hang Tsui Court, Tsui Ying House 238, 268 Yuen Long Yiu Foo House, Tin Yiu Estate 258, 259 Wan Chai Block A, Viking Villas 260 Central & Western Shun On Building, 2 Sands Street 261 Kowloon City Cheong Shing Court 262 Kwai Tsing Yam Heng House, Shek Yum Estate 263 Wan Chai Sakura Court 264 Central & Western Silvercrest, 24 Macdonnell Road 265 Southern Repulse Bay Garden 266 Central & Western SOHO 189 267 Eastern Block Q, Kornhill 269 Sham Shui Po Block 23, Phase 1, Mei Foo Sun Cheun 270 Island Tower 12, Caribbean Coast 271 Yau Tsim Mong Block 4, Prosperous Garden 272 Yau Tsim Mong Block B, Hoi Lam House, Hoi Fu Court 273 Kwun Tong Dorsett Kwun Tong 274 Wong Tai Sin Block 2, Kai Tak Garden 275 Wan Chai Hang Shun Mansions 276 Wan Chai 307 Jaffe Road 277 Wan Chai Tagus Residences 278 Islands Woodland Court, Parkvale Village 279 Central & Western Chi Residences 120 281 Central & Western 208 Hollywood Road 282 Southern L'Hoel Island South 283 Sha Tin Block 6, Bayshore Towers 284 1 Related confirmed / probable District Building name case number Yau Tsim Mong Tower 7, The Long Beach 285 Sai Kung Pak Kong Au Road 286 Tsuen Wan Indi Home 287 Kwai Tsing On Hoi House, Cheung On Estate 287 Eastern Block 6, Provident Centre -

Particulars of Properties Held

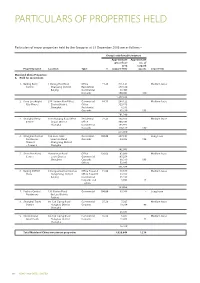

PARTICULARS OF PROPERTIES HELD Particulars of major properties held by the Group as at 31 December 2006 are as follows:– Group’s attributable interest Approximate Approximate gross floor no. of area carpark Property name Location Type % (square feet) spaces Lease term Mainland China Properties A. Held for investment 1. Beijing Kerry 1 Guang Hua Road Office 71.25 711,121 Medium lease Centre Chaoyang District Residential 277,330 Beijing Commercial 98,406 Carparks 190,806 430 1,277,663 2. Kerry Everbright 218 Tianmu Road West Commercial 64.35 286,122 Medium lease City Phase I Zhabei District Office 323,675 Shanghai Residential 6,333 Carparks 85,250 155 701,380 3. Shanghai Kerry 1515 Nanjing Road West Residential 74.25 142,355 Medium lease Centre Jingan District Office 308,584 Shanghai Commercial 103,971 Carparks 118,129 180 673,039 4. Shanghai Central 166 Lane 1038 Residential 100.00 287,101 Long lease Residences Huashan Road Carparks 54,982 154 Phase II Changning District – Tower 3 Shanghai 342,083 5. Shenzhen Kerry Renminnan Road Office 100.00 82,099 Medium lease Centre Lowu District Commercial 107,256 Shenzhen Carparks 88,319 193 Others 53,885 331,559 6. Beijing COFCO 8 Jianguomennei Avenue Office Tower A 15.00 49,649 Medium lease Plaza Dongcheng District Office Tower B 53,895 Beijing Commercial 86,592 Carparks and 3,892 25 others 194,028 7. Fuzhou Central 139 Gutian Road Commercial 100.00 63,986 – Long lease Residences Gu Lou District Fuzhou 8. Shanghai Trade 88-128 Siping Road Commercial 55.20 7,567 Medium lease Square Hongkou District Carparks 19,264 48 Shanghai 26,831 9. -

Major Transaction

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Kerry Properties Limited, you should at once hand this circular to the purchaser(s) or the transferee(s) or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or the transferee(s). The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this circular, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. website: www.kerryprops.com (Stock Code: 00683) MAJOR TRANSACTION A letter from the board of directors of Kerry Properties Limited is set out on pages 5 to 25 of this circular. * For identification purpose only 29 December 2004 CONTENTS Page Definitions ........................................................ 1 Letter from the Board ............................................... 5 Appendix I – Accountants’ Report on Treasure Lake................ 26 Appendix II – Accountants’ Report on Eas HK .................... 33 Appendix III − Accountants’ Report on the Eas PRC Group ........... 51 Appendix IV – Financial Information -

Name of Buildings Awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (As at 8 February 2018)

Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (as at 8 February 2018) Name of Building Type of Building District @Convoy Commercial/Industrial/Public Utilities Eastern 1 & 3 Ede Road Private/HOS Residential Kowloon City 1 Duddell Street Commercial/Industrial/Public Utilities Central & Western 100 QRC Commercial/Industrial/Public Utilities Central & Western 102 Austin Road Commercial/Industrial/Public Utilities Yau Tsim Mong 1063 King's Road Private/HOS Residential Eastern 11 MacDonnell Road Private/HOS Residential Central & Western 111 Lee Nam Road Commercial/Industrial/Public Utilities Southern 12 Shouson Hill Road Private/HOS Residential Central & Western 127 Repulse Bay Road Private/HOS Residential Southern 12W Commercial/Industrial/Public Utilities Tai Po 15 Homantin Hill Private/HOS Residential Yau Tsim Mong 15W Commercial/Industrial/Public Utilities Tai Po 168 Queen's Road Central Commercial/Industrial/Public Utilities Central & Western 16W Commercial/Industrial/Public Utilities Tai Po 17-19 Ashley Road Commercial/Industrial/Public Utilities Yau Tsim Mong 18 Farm Road (Shopping Arcade) Commercial/Industrial/Public Utilities Kowloon City 18 Upper East Private/HOS Residential Eastern 1881 Heritage Commercial/Industrial/Public Utilities Yau Tsim Mong 211 Johnston Road Commercial/Industrial/Public Utilities Wan Chai 225 Nathan Road Commercial/Industrial/Public Utilities Yau Tsim Mong Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) -

Review of Operations

REVIEW OF OPERATIONS Sales of the joint venture developments at Tai Kok Apart from the exceptional location and quality of Tsui Phases 1 and 2, are also progressing well with its properties, the Group also strives to provide its the developments being approximately 86% and 46% residents with the best professional building sold, respectively, as at 31 December 2000. At the management services through Kerry Property year end, Island Harbourview, Park Avenue and Management Services Limited. These include a wide Central Park had 303, 513 and 1,068 units, array of home services such as insurance, daily respectively, remaining available for sale in the newspaper, housekeeping services and experienced coming year. licensed technicians to look after repairs and maintenance needs of the apartments. Security in the INVESTMENT PROPERTIES Group’s developments is also enhanced by the use Gross rental revenue from investment properties in of advanced CCTV system and a computerised 2000 amounted to HK$465 million (1999: HK$476 security checking schedule whenever possible. million). In accordance with its accounting policies, the Group conducted a revaluation of its investment properties at the year end. The addition of Aigburth, a luxury development located adjacent to Tavistock II, to the Group’s investment portfolio has helped to reinforce its recurrent income base. Aigburth comprises sixty standard apartments measuring between 2,980 square feet and 3,080 square feet. It has four single floor apartments and a top floor duplex penthouse. It is leasing well with the building being approximately 89% leased as at 31 December 2000. Construction of Olympian Tower and Olympian City 1, being the office block and the commercial podium in the Phase 1 development of the Tai Kok Tsui project, was also completed during the year. -

Kerry Properties Limited Annual Report 2006 Annual

Stock Code : 683 KERRY PROPERTIES LIMITED ANNUAL REPORT 2006 KERRY PROPERTIES LIMITED 13/F - 14/F, Cityplaza 3, 14 Taikoo Wan Road, Taikoo Shing, Hong Kong Telephone: (852) 2967 2200 (Incorporated in Bermuda with limited liability) Facsimile: (852) 2967 9480 www.kerryprops.com ANNUAL REPORT 2006 We express the accomplishment and diversity of Kerry Properties with an artistically stylish and colourful montage depicting existing assets and future projects. The varying elements and visuals of the montage allow us to emphasize the company’s extensive portfolio that reflects our vision into the future. The Group’s future performance will be built on the strength of past results, and on the integrity of our people. Our commitment to innovate, rather than to simply reproduce, is key to differentiating the business and generating sustainable value for stakeholders over the long-term. PROPERTY The property division of Kerry Properties Limited follows a strategy of investing in prime locations, typically in areas with limited supply of quality land, and focusing on large-scale mixed-use property projects that lend themselves to the creation of scale, scope and synergy effects that enhance their attractiveness. LOGISTICS NETWORK Kerry Logistics Network Limited (Kerry Logistics) is positioned as a leading Asian-based international logistics operator. The Division delivers a seamless and integrated range of services that bring tangible results to cost efficiency, customer satisfaction and bottom-line results. Our customers are from industries as diverse as fresh produce to fashion and electronics to food & beverage and we provide a comprehensive range of logistics solutions to suit their industry specific needs. -

All Approved Premises

All Approved Premises Local Authority Name District Name and Telephone Number Name Address Telephone BARKING AND DAGENHAM BARKING AND DAGENHAM 0208 227 3666 EASTBURY MANOR HOUSE EASTBURY SQUARE, BARKING, 1G11 9SN 0208 227 3666 THE CITY PAVILION COLLIER ROW ROAD, COLLIER ROW, ROMFORD, RM5 2BH 020 8924 4000 WOODLANDS WOODLAND HOUSE, RAINHAM ROAD NORTH, DAGENHAM 0208 270 4744 ESSEX, RM10 7ER BARNET BARNET 020 8346 7812 AVENUE HOUSE 17 EAST END ROAD, FINCHLEY, N3 3QP 020 8346 7812 CAVENDISH BANQUETING SUITE THE HYDE, EDGWARE ROAD, COLINDALE, NW9 5AE 0208 205 5012 CLAYTON CROWN HOTEL 142-152 CRICKLEWOOD BROADWAY, CRICKLEWOOD 020 8452 4175 LONDON, NW2 3ED FINCHLEY GOLF CLUB NETHER COURT, FRITH LANE, MILL HILL, NW7 1PU 020 8346 5086 HENDON HALL HOTEL ASHLEY LANE, HENDON, NW4 1HF 0208 203 3341 HENDON TOWN HALL THE BURROUGHS, HENDON, NW4 4BG 020 83592000 PALM HOTEL 64-76 HENDON WAY, LONDON, NW2 2NL 020 8455 5220 THE ADAM AND EVE THE RIDGEWAY, MILL HILL, LONDON, NW7 1RL 020 8959 1553 THE HAVEN BISTRO AND BAR 1363 HIGH ROAD, WHETSTONE, N20 9LN 020 8445 7419 THE MILL HILL COUNTRY CLUB BURTONHOLE LANE, NW7 1AS 02085889651 THE QUADRANGLE MIDDLESEX UNIVERSITY, HENDON CAMPUS, HENDON 020 8359 2000 NW4 4BT BARNSLEY BARNSLEY 01226 309955 ARDSLEY HOUSE HOTEL DONCASTER ROAD, ARDSLEY, BARNSLEY, S71 5EH 01226 309955 BARNSLEY FOOTBALL CLUB GROVE STREET, BARNSLEY, S71 1ET 01226 211 555 BOCCELLI`S 81 GRANGE LANE, BARNSLEY, S71 5QF 01226 891297 BURNTWOOD COURT HOTEL COMMON ROAD, BRIERLEY, BARNSLEY, S72 9ET 01226 711123 CANNON HALL MUSEUM BARKHOUSE LANE, CAWTHORNE, -

Higher Educated Residential Preferences and the Marketing of Private Housing in the Amsterdam Metropolitan Area and Hong Kong

Higher educated residential preferences and the marketing of private housing in the Amsterdam Metropolitan Area and Hong Kong Thesis submitted as part of the Research Master Urban Studies, University of Amsterdam Author: Michael Stuart-Fox Student number: 10011455 Email address: [email protected] Supervisor: Prof. Sako Musterd Second reader: Dr. Marco Bontje Date of submission: 19 June 2015 Table of contents Acknowledgements p. 3 Remarks p. 4 1. Introduction and research questions p. 5 2. Theoretical framework, conceptualisation, and operationalisations p. 9 2.1 Lifestyles, values and residential preferences in modern societies p. 9 2.2 Occupational groups, orientation of capital, and residential preferences p.13 2.3 Studies on the intra-metropolitan residential preferences of creative class p.14 2.4 Conceptualisation and type of preferences: stated and intra-metropolitan p.16 2.5 Operationalisations p.18 2.6 Conceptual model p.19 2.7 Definitions and importance of the creative and high-tech sectors p.20 2.8 Theoretical expectations p.21 3. Research design, cases, and methodology p.22 3.1 Case selection and type of case study p.22 3.2 Approach to comparison as a research tool p.23 3.3 Other features of the research design p.24 3.4 Methods of data collection and analysis p.25 4. Descriptions of samples in the MRA and Hong Kong p.27 4.1 Demographic characteristics p.27 4.2 Socio-economic characteristics p.30 5. Stated residential preferences, differences between the MRA and Hong Kong, and the influence of urban contextual factors p.34 5.1 Importance fo amenities in the region and neighbourhood p.34 5.2 Assessment of moving, reasons for (not) moving and dwelling preferences p.39 5.3 Ranking of features of the dwelling, neighbourhood and location p.48 5.4 Ranking of urban and suburban images and locations p.54 5.5 Conclusion p.59 6. -

Particulars of Properties Held

PARTICULARS OF PROPERTIES HELD Particulars of major properties held by the Group as at 31 December 2004 are as follows:– Group’s attributable interest Approximate Approximate gross floor no. of area carpark Property name Location Type % (square feet) spaces Lease term Mainland China Properties A. Held for investment 1. Beijing Kerry 1 Guang Hua Road Office 71.25 711,121 Medium lease Centre Chaoyang District Hotel with Club 499,642 Beijing Residential 277,330 Commercial 98,406 Carparks 190,806 430 1,777,305 2. Kerry Everbright 218 Tianmu Road West Commercial 64.35 286,122 Medium lease City Phase I Zhabei District Office 323,675 Shanghai Residential 6,333 Carparks 85,250 155 701,380 3. Shanghai Kerry 1515 Nanjing Road West Residential 74.25 142,355 Medium lease Centre Jingan District Office 308,584 Shanghai Commercial 103,971 Carparks 118,129 180 673,039 4. Shenzhen Kerry Renminnan Road Office 100.00 160,589 Medium lease Centre Lowu District Commercial 107,256 Shenzhen Carparks 88,319 193 Others 53,885 410,049 5. Beijing COFCO 8 Jianguomennei Avenue Office Tower A 15.00 49,649 Medium lease Plaza Dongcheng District Office Tower B 53,895 Beijing Commercial 86,592 Carparks and 3,892 25 others 194,028 6. Fuzhou Central 139 Gutian Road Commercial 100.00 66,831 – Long lease Residences Gu Lou District Fuzhou 7. Shanghai Trade 88-128 Siping Road Commercial 55.20 9,946 Medium lease Square Hongkou District Carparks 19,264 51 Shanghai 29,210 8. International 88-128 Siping Road Commercial 55.20 3,047 Medium lease Apartments Hongkou District Carparks 12,432 33 Shanghai 15,479 Total Mainland China investment properties 3,867,321 1,067 KERRY PROPERTIES LIMITED ANNUAL REPORT 2004 35 PARTICULARS OF PROPERTIES HELD Group’s attributable interest Approximate gross floor Approximate area site area Stage of Anticipated Property name Location Type % (square feet) (square feet) completion completion Mainland China Properties B. -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of buildings with confirmed / probable cases of COVID-19 List of residential buildings in which confirmed / probable cases have resided (Note: The buildings will remain on the list for 14 days since the reported date) Related confirmed / probable District Building name case number Wong Tai Sin Block 2, Kai Tak Garden 275 Wan Chai Hang Shun Mansions 276 Wan Chai 307 Jaffe Road 277 Wan Chai Tagus Residences 278 Islands Woodland Court, Parkvale Village 279 Central & Western Chi Residences 120 281 Central & Western 208 Hollywood Road 282 Southern L'Hoel Island South 283 Sha Tin Block 6, Bayshore Towers 284 Yau Tsim Mong Tower 7, The Long Beach 285 Sai Kung Pak Kong Au Road 286 Tsuen Wan Indi Home 287 Kwai Tsing On Hoi House, Cheung On Estate 287 Eastern Block 6, Provident Centre 288 Eastern On Hiu Mansion, Lei King Wan 289 Southern Ovolo Southside 290 Southern Chun Tak House, Lung Tak Court 291 Wan Chai Rosedale Hotel Hong Kong 292 Wan Chai Monmouth Villa 293 Tsuen Wan Block 1, City Point 295 North Fanling Wai South 296 Eastern Ramada Hong Kong Grand View 297 North Lai Ming House, Wah Ming Estate 298 Kowloon City Tower 3, Harbour View Horizon Hotel 299 Yau Tsim Mong Rosedale Hotel Kowloon 300 Sha Tin Fook Lam House, Kwong Lam Court 301 1 Related confirmed / probable District Building name case number Sha Tin Athlete's Hostel in HK Sports Institues 302 Eastern Tung Lam Court 303, 304 Eastern 191-193 Shau Kei Wan Road 306 Kwun Tong Tak Shui House, Tak Tin Estate 308 Wan Chai Celeste Court, Fung Fai Terrace 309 Central & Western Valiant