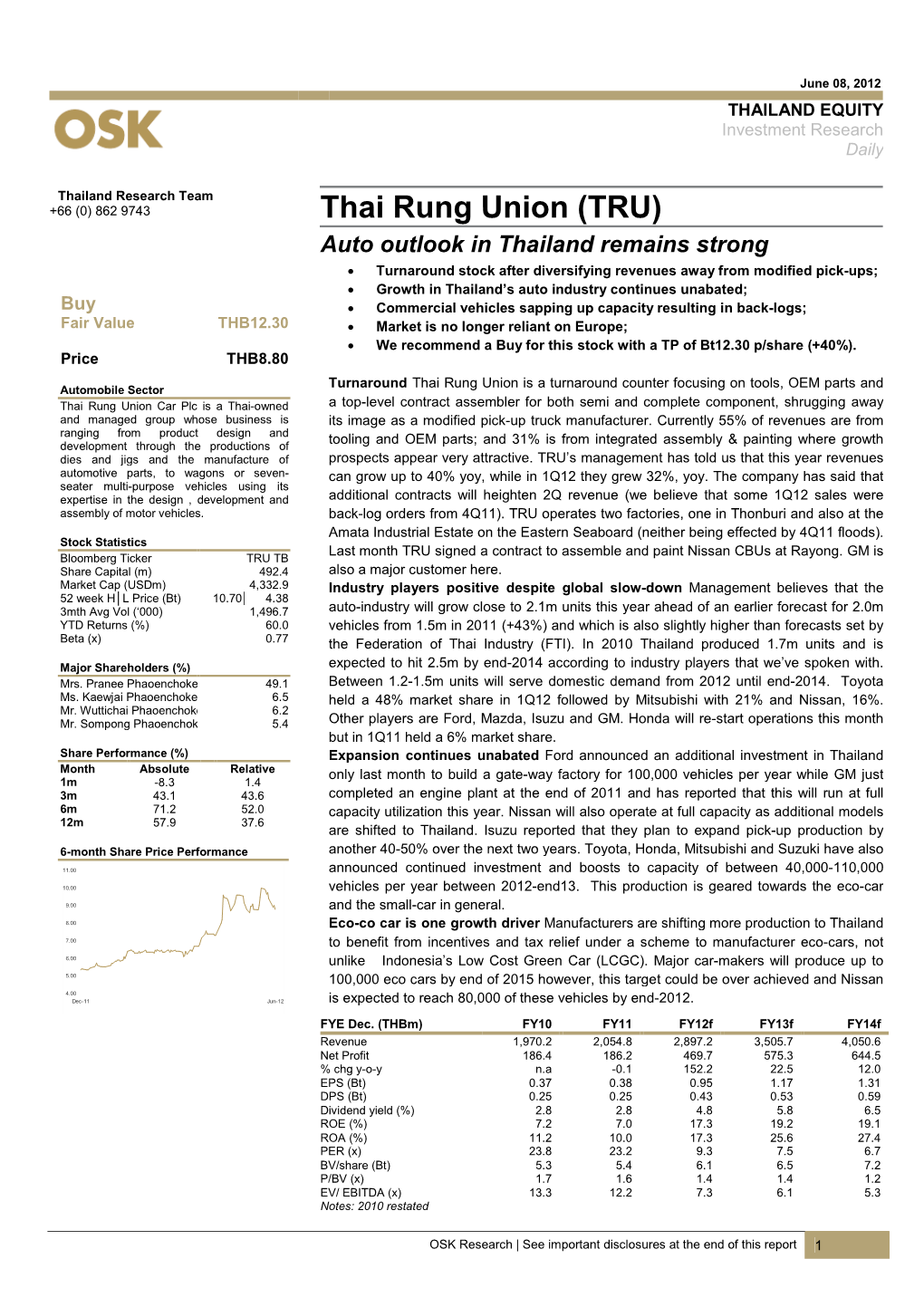

Thai Rung Union (TRU)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ar2008 EN.Pdf

Financial Highlights 2 Message from the Chairman 3 Board of Directors and Audit Committee 4 Social Activities 2008 8 General Information 11 Nature of Business 14 Risk Factors 17 Shareholders and Management 20 Contents Related Party Transactions 32 Corporate Governance 35 Supervisory Report on Audit Committee 46 Remuneration Committee’s Report 48 Board of Directors’ Responsibility for Financial Reports 49 Management’s Discussion and Analysis 50 Report of Independent Auditor 54 Financial Stetaments 55 () !"#$!% &! # & & '& *,$+ 2510 -./ $!# $3 () ! 4 *!,- $!',$ 2537 && $ &3 40 &$ () # # # , 9 ,& #$!%:,$!' !#$;<,,# =:<>$$!'&" &=":- &=# &%$ !?9 ?&: , () !, &,## -.=:<> <:--?!$ () Thai Rung Union Car Public Company Limited Thai Rung Union Car Plc. has long been established in the business of motor vehicle assembly Originally founded as a limited partnership under the name Thai Rung Engineering in 1967. its business success eventually led to its become a listed company on the Stock Exchange of Thailand in 1994 under the current name, Thai Rung Union Car Public Company Limited. For the last forty years, until the Present, Thai Rung Union Car Plc. has always been dedicated to developing creative and innovative products for the Thai automotive assembly industry, has also had success with imaginative exports to several countries in different parts of the world. lts products have been popular with consumers, and it has received the Prime MinisterGs Award for Best Exporter and the Car of the Year Award, to name just two of many awards. All this is a source of great pride to us at Thai Rung Union Car Plc. and it also strengthens our determination to continue ceaselessly creating and developing quality products for thai people and the thai nation. -

IHS Automotive Regional Report Supplierbusiness ASEAN Automotive Supplier Report

IHS Automotive Regional Report SupplierBusiness ASEAN Automotive Supplier Report 2013 Edition supplierbusiness.com IHS Automotive SupplierBusiness | ASEAN Automotive Suppliers Report Contents ASEAN automotive & supplier market overview ......................................................................................................... 7 Indonesia – Automotive Industry Overview ............................................................................................................... 17 Overview of Macro Economic Situation ................................................................................................................. 17 Planned Investment in Infrastructure Development Projects .............................................................................. 18 National Automotive Policy & Plans ........................................................................................................................ 19 Manufacturing Advantage ........................................................................................................................................ 22 Overview of Automotive Industry & Supply Chain ................................................................................................. 23 Overview of Vehicle Component Suppliers ............................................................................................................ 29 List of Joint-Ventures and Mergers & Acquisitions in 2012/2013 ........................................................................ 30 OEM Supplier -

THAIRUNG ENGLISH.Indd

2017รายงานประจำป 2560 ANNUAL REPORT บรษิ ทั จำกดัั (มหาชน) Thai Rung Union Car Public Company Limited รางวลั นวตั กรรมแหง ชาต ิ 2560 National Innovation Awards 2017 รถยนต์ TR Transformer II ของไทยรุ่งฯ ได้รับ “รางวัลชนะเลิศนวัตกรรมแห่งชาติ ประจ�าปี 2560” จากส�านักงานนวัตกรรมแห่งชาติฯ กระทรวงวิทยาศาสตร์และเทคโนโลยี TR Transformer II has won a “National Innovation Awards 2017“ from the National Innovation Institute of the Ministy of Science and Technology บริษัท ไทยรุ่งยูเนี่ยนคาร์ จำกัด (มหาชน) Thai Rung Union Car Public Company Limited Content Company Background 2 Vision and Mission 3 Summary Financial Information 4 Message from the Chairman 5 Profiles of Directors of the Company 7 General Information 17 Organization Chart 21 Nature of Business 22 Risk Factors 26 Shareholders and Management 30 Corporate Governance 46 Sustainability Report 62 Related Party Transactions 80 Internal Control 83 Report of the Audit and Corporate Governance Committee 85 Report of the Nomination and Remuneration Committee 88 Report of the Risk Management Committee 90 Board of Directors’ Responsibility for Financial Reports 91 Management’s of Discussion and Analysis 92 Independent Auditor’s Report 97 Financial Statement 102 บริษัท ไทยรุ่งยูเนี่ยนคาร์ จำากัด (มหาชน) Thai Rung Union Car Plc., 1 บริษัท ไทยรุ่งยูเนี่ยนคาร์ จำกัด (มหาชน) Thai Rung Union Car Public Company Limited Company Background Company Background Thai Rung Union Car Plc has long been established as a maker of auto body parts and a vehicle assembler. Originally founded as a limited partnership under the name Thai Engineering in 1967 by Mr. Vichien Phaoenchoke, its business success eventually led to its becoming a listed company on the Stock Exchange of Thailand in 1994 under the current name, Thai Rung Union Car Public Company Limited. -

Dimensional Investment Group

SECURITIES AND EXCHANGE COMMISSION FORM N-Q Quarterly schedule of portfolio holdings of registered management investment company filed on Form N-Q Filing Date: 2008-04-29 | Period of Report: 2008-02-29 SEC Accession No. 0001104659-08-027772 (HTML Version on secdatabase.com) FILER DIMENSIONAL INVESTMENT GROUP INC/ Business Address 1299 OCEAN AVE CIK:861929| IRS No.: 000000000 | State of Incorp.:MD | Fiscal Year End: 1130 11TH FLOOR Type: N-Q | Act: 40 | File No.: 811-06067 | Film No.: 08784216 SANTA MONICA CA 90401 2133958005 Copyright © 2012 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM N-Q QUARTERLY SCHEDULE OF PORTFOLIO HOLDINGS OF REGISTERED MANAGEMENT INVESTMENT COMPANY Investment Company Act file number 811-6067 DIMENSIONAL INVESTMENT GROUP INC. (Exact name of registrant as specified in charter) 1299 Ocean Avenue, Santa Monica, CA 90401 (Address of principal executive offices) (Zip code) Catherine L. Newell, Esquire, Vice President and Secretary Dimensional Investment Group Inc., 1299 Ocean Avenue, Santa Monica, CA 90401 (Name and address of agent for service) Registrant's telephone number, including area code: 310-395-8005 Date of fiscal year end: November 30 Date of reporting period: February 29, 2008 ITEM 1. SCHEDULE OF INVESTMENTS. Dimensional Investment Group Inc. Form N-Q February 29, 2008 (Unaudited) Table of Contents Definitions of Abbreviations and Footnotes Schedules of Investments U.S. Large Cap Value Portfolio II U.S. Large Cap Value Portfolio III LWAS/DFA U.S. High Book to Market Portfolio DFA International Value Portfolio Copyright © 2012 www.secdatabase.com. -

Automotive Innovation Forum Asia 2007 Thailand

AutomotiveAutomotive InnovationInnovation ForumForum AsiaAsia 20072007 ThailandThailand Ms. Sudjit Inthaiwong Deputy Secretary Geneal Thailand Board of Investment Bangkok, 2007 1 AA CompetitiveCompetitive LocationLocation ThailandThailand ForefrontForefront forfor investmentinvestment World Bank Ease of Doing Business, Thailand ranks #18 in the world UNCTAD Global Investment Prospects Assessment, FDI prospects in Asia 2005 – 2008: Thailand ranks #3 JBIC 2006 Survey on promising countries for overseas business operations over next 3 years: Thailand ranks #4 JBIC 2006 Survey on promising countries for SMEs over next 3 years: Thailand ranks #4 Grant Thornton International Business Owners Survey 2006:“Thailand’s assets include an entrepreneurial population, abundant natural resources and a wonderful lifestyle and, if these strengths are promoted and supported, the country will continue to be a great place to do business” JBICJBIC FYFY 20062006 SurveySurvey When asked about profitability for each region, including Japan, “the percentage of companies answering “higher” was greatest for Thailand” Automotives, “strengthen or expand” response stronger in Thailand than any other region, including southern China and North America. JBICJBIC Survey:Survey: CompaniesCompanies LookingLooking toto StrengthenStrengthen oror ExpandExpand inin ASEANASEAN--44 250 238 200 150 Thailand Vietnam 118102 Indonesia 100 86 Malaysia 55 Philippines 50 50 33 31 22 12 24 10 15 105 0 All Industries E&E Automobile Source: JBIC 18th Annual Survey Report on Overseas -

Thai Rung Union Car Plc

Thai Rung Union Car Plc. Opportunity Day, 24 May 2011 Thai Rung Union Car Plc. Opportunity Day, 24 May 2011 Contents • Industry Overview • TRU’s Sales Breakdown • TRU’s Strategy • Appendix Contents • Industry Overview • TRU’s Sales Breakdown • TRU’s Strategy • Appendix Production Volume in Thailand Q1/2011 Units +5% QoQ Q1' 53 600,000 +22% YoY Q4' 53 468,981 Q1' 54 500,000 448,074 382,841 400,000 300,000 200,000 100,000 0 Q1/10 Q4/10 Q1/11 Production Source : The Federation of Thai Industries Domestic Sales in Thailand Q1/2011 -2% QoQ +43% YoY Units Commercial car 244,008 QoQ 238,619 YoY Passenger 250,000 Pick Up 14,855 - 14,857 +38% 200,000 166,802 109,631 10,770 +0.60% 110,292 +60% 150,000 68,970 100,000 119,522 -5% 113,470 +30% 50,000 87,062 0 Q1/10 Q4/10 Q1/11 Domestic Sales Source : The Federation of Thai Industries CBU Export Q1/2011 Units +1% QoQ Q1' 53 300,000 +8% YoY Q4' 53 231,002 234,407 Q1' 54 250,000 216,685 200,000 150,000 100,000 50,000 0 Q1/10 Q4/10 Q1/11 CBU Export Source : The Federation of Thai Industries CBU Export by Brand Q1/2011 ISUZU GM Units 78,594 HONDA 5% 2% 80,000 6% PPV 1,832 2% MAZDA 6% Passenger Car 70,000 TOYOTA 16,520 21% FORD 33% 1Ton Pickup 12% 60,000 NISSAN MITSUBISHI 17% 19% 50,000 44,563 38,939 40,000 13,024 29% 240 28,306 30,000 60,242 1% 17,972 46% 77% 1,685 6% 7,652 27% 20,000 13,520 13,087 12,240 31,299 70% 210 2% 54% 47% 10,000 20,967 18,969 67% 6,287 5,050 12,030 98% 28% 7,233 53% 1,423 3,627 72% 0 TOYOTA MITSUBISHI NISSAN FORD MAZDA HONDA ISUZU GM Source : The Federation of Thai Industries Thai Auto Industry 2004-2015 (Forecast) Units Round 10% effect from Japan Earthquake & Growth from Eco car 3,000,000 Tsunami, reduce from 1.80 to 1.67 mil. -

Opportunity Day 2011 Results Presentation

Opportunity Day 2011 Results Presentation 12th March 2012 At Stock Exchange of Thailand Present by: Mr. Sompong Phaoenchoke, MD. Ms. Naiyana Prachotrattanakul, IR Mgr. Agenda • Company Profile • Industry Overview • Financial Review • Future Outlook 2 Group Structure & Business Thai Rung Union Car Plc. “TRU” ‐R&D, Auto Assembly ‐Press Metal Parts, Plastic Parts, Car Seat Subsidiary Companies Associated Companies Thai Rung Tools and Dies Co. Ltd. 94% 20% Thai Auto Conversion Co. Ltd. “TRT” “TAC” (JV. with Toyota group) ‐ Tooling (Dies/Jigs/CF) ‐ Special Purpose Vehicles Thai Auto Pressparts Co. Ltd. 91% 30% Delta Thairung Co. Ltd. “TAP” “DTC” (JV. with Delta Kogyo, Japan) ‐ Pressed Metal Parts ‐ Seat & Seat Components Thai V.P. Auto Service Co. Ltd. 94% “TVS” ‐ After‐sales Services & Spare Parts 99.53% Thai Ultimate Car Co. Ltd. “TUC” ‐ Automotive, consulting & admin. services Delta‐TR Co. Ltd., Associated company, was liquidated as at 6 March 2012. 3 Scope of Business •Research & Development (R&D) •Tooling (Dies/Jigs/CF/1) •Pressed metal part & plastic part •EDP/2 & Painting •Auto Assembly •Seat •After‐sales service & Spare parts Note : 1. CF = Checking Fixture 2. EDP = Electro Deposit Primer 4 Business Units Tooling (Dies/Jigs/CF) OEM Parts Special Purpose Vehicles Contract Assembly 5 Agenda • Company Profile • Industry Overview • Financial Review • Future Outlook 6 Thai Auto Industry 2004‐2015F CAGR (2004‐2008) CAGR (2012‐2015F) Mil. Units 3.00 Production 10%, Domestic NA., Export 25% Production 8%, Domestic NA., Export 8% (From Eco -

Acronimos Automotriz

ACRONIMOS AUTOMOTRIZ 0LEV 1AX 1BBL 1BC 1DOF 1HP 1MR 1OHC 1SR 1STR 1TT 1WD 1ZYL 12HOS 2AT 2AV 2AX 2BBL 2BC 2CAM 2CE 2CEO 2CO 2CT 2CV 2CVC 2CW 2DFB 2DH 2DOF 2DP 2DR 2DS 2DV 2DW 2F2F 2GR 2K1 2LH 2LR 2MH 2MHEV 2NH 2OHC 2OHV 2RA 2RM 2RV 2SE 2SF 2SLB 2SO 2SPD 2SR 2SRB 2STR 2TBO 2TP 2TT 2VPC 2WB 2WD 2WLTL 2WS 2WTL 2WV 2ZYL 24HLM 24HN 24HOD 24HRS 3AV 3AX 3BL 3CC 3CE 3CV 3DCC 3DD 3DHB 3DOF 3DR 3DS 3DV 3DW 3GR 3GT 3LH 3LR 3MA 3PB 3PH 3PSB 3PT 3SK 3ST 3STR 3TBO 3VPC 3WC 3WCC 3WD 3WEV 3WH 3WP 3WS 3WT 3WV 3ZYL 4ABS 4ADT 4AT 4AV 4AX 4BBL 4CE 4CL 4CLT 4CV 4DC 4DH 4DR 4DS 4DSC 4DV 4DW 4EAT 4ECT 4ETC 4ETS 4EW 4FV 4GA 4GR 4HLC 4LF 4LH 4LLC 4LR 4LS 4MT 4RA 4RD 4RM 4RT 4SE 4SLB 4SPD 4SRB 4SS 4ST 4STR 4TB 4VPC 4WA 4WABS 4WAL 4WAS 4WB 4WC 4WD 4WDA 4WDB 4WDC 4WDO 4WDR 4WIS 4WOTY 4WS 4WV 4WW 4X2 4X4 4ZYL 5AT 5DHB 5DR 5DS 5DSB 5DV 5DW 5GA 5GR 5MAN 5MT 5SS 5ST 5STR 5VPC 5WC 5WD 5WH 5ZYL 6AT 6CE 6CL 6CM 6DOF 6DR 6GA 6HSP 6MAN 6MT 6RDS 6SS 6ST 6STR 6WD 6WH 6WV 6X6 6ZYL 7SS 7STR 8CL 8CLT 8CM 8CTF 8WD 8X8 8ZYL 9STR A&E A&F A&J A1GP A4K A4WD A5K A7C AAA AAAA AAAFTS AAAM AAAS AAB AABC AABS AAC AACA AACC AACET AACF AACN AAD AADA AADF AADT AADTT AAE AAF AAFEA AAFLS AAFRSR AAG AAGT AAHF AAI AAIA AAITF AAIW AAK AAL AALA AALM AAM AAMA AAMVA AAN AAOL AAP AAPAC AAPC AAPEC AAPEX AAPS AAPTS AAR AARA AARDA AARN AARS AAS AASA AASHTO AASP AASRV AAT AATA AATC AAV AAV8 AAW AAWDC AAWF AAWT AAZ ABA ABAG ABAN ABARS ABB ABC ABCA ABCV ABD ABDC ABE ABEIVA ABFD ABG ABH ABHP ABI ABIAUTO ABK ABL ABLS ABM ABN ABO ABOT ABP ABPV ABR ABRAVE ABRN ABRS ABS ABSA ABSBSC ABSL ABSS ABSSL ABSV ABT ABTT -

Auditor's Review Report to the Shareholders and the Board Of

nd ANS Audit Co., Ltd. 100/72, 22 Floor, Telephone: (662) 645 0109 100/2 Vongvanij Building B., Fax : (662) 645 0110 Rama 9 Rd., Huaykwang, http://www.ans.co.th Bangkok 10310, Thailand Auditor’s Review Report To the Shareholders and the Board of Directors of Thai Rung Union Car Public Company Limited I have reviewed the accompanying consolidated balance sheet of Thai Rung Union Car Public Company Limited and its subsidiaries as at March 31, 2009, and the related consolidated statements of income, changes in shareholders’ equity and cash flows for the three-month period ended March 31, 2009, and the separate financial statements of Thai Rung Union Car Public Company Limited for the same period. These financial statements are the responsibility of the Company’s management as to their correctness and the completeness of the presentation. My responsibility is to issue a report on these financial statements based on my review. Except as discussed in the next paragraph, I conducted my review in accordance with the auditing standard applicable to review engagements. This standard requires that I plan and perform the review to obtain moderate assurance as to whether the financial statements are free of material misstatement. A review is limited primarily to inquiries of company personnel and analytical procedures applied to financial data and thus provides less assurance than an audit. I have not performed an audit and, accordingly, I do not express an audit opinion. The Company’s consolidated financial statements as at March 31, 2009, and for the three-month period then ended, included investments in three associated companies accounted for under the equity method amounting to Baht 152.97 million and shares of profit from these companies amounting to Baht 3.46 million (as discussed in Note 10 to the financial statements). -

Supplier Selection in the Thai Automotive Industry

Hi-Stat Discussion Paper Series No.186 Supplier Selection in the Thai Automotive Industry Somsupa Nopprach October 2006 Hitotsubashi University Research Unit for Statistical Analysis in Social Sciences A 21st-Century COE Program Institute of Economic Research Hitotsubashi University Kunitachi, Tokyo, 186-8603 Japan http://hi-stat.ier.hit-u.ac.jp/ Supplier Selection in the Thai Automotive Industry Somsupa Nopprach Abstract This paper uses agglomeration theory to analyze the impact of Thai government policies on the development of the Thai automotive industry and cluster formation in Central and Eastern Thailand. Using cross-section data on 162 auto-parts suppliers from the Thailand Automotive Directory 2003-2004, the paper examines the criteria of supplier selection in the Thai automotive industry. Using logit models and cross-section data on 162 auto-parts suppliers from the Thailand Automotive Directory 2003-2004, the paper examines the effects of economies of scale, technology, distance between suppliers and assembler plants, and nationality on the likelihood of a supplier being selected as a subcontractor. Furthermore, the paper compares the role of these factors for different types of assemblers – Japanese and American, automobile and motorcycle. The findings suggest that scale of production is a dominant factor while there is no significant preference for suppliers of the same nationality as the assembler. In addition, assemblers are more likely to choose parts makers located in close proximity as their subcontractors, as the agglomeration theory predicts. Finally, the comparison of supplier selection criteria for different types of assemblers shows that there exists commonalities in valuing economies of scale while the automobile assemblers is the group that mostly concern technological level of suppliers. -

Non-Equity Modes of Trade in ASEAN PAPER 9 Promoting New Forms of Trade Between APRIL Japan and ASEAN 2020

Non-Equity Modes of Trade in ASEAN PAPER 9 Promoting new forms of trade between APRIL Japan and ASEAN 2020 nd aila Th For inquiries, contact ASEAN-Japan Centre (ASEAN Promotion Centre on Trade, Investment and Tourism) 1F, Shin Onarimon Bldg., 6-17-19, Shimbashi, Minato-ku, Tokyo 105-0004 Japan Phone/Fax: +81-3-5402-8002/8003 (Office of the Secretary General) +81-3-5402-8004/8005 (Research and Policy Analysis (RPA) Cluster) +81-3-5402-8116/8005 (Capacity Building (CB) Cluster) +81-3-5402-8006/8007 (Trade and Investment (TI) Cluster) +81-3-5402-8008/8009 (Tourism and Exchange (TE) Cluster) +81-3-5402-8118/8003 (PR) e-mail address: [email protected] https://www.asean.or.jp Copyright © ASEAN Promotion Centre on Trade, Investment and Tourism. All Rights Reserved. Paper 9 / April 2020 / Non-Equity Modes of Trade in ASEAN: Thailand Promoting new forms of trade between Japan and ASEAN Non-Equity Modes of Trade in ASEAN PAPER 9 Promoting new forms of trade between APRIL Japan and ASEAN 2020 NON-EQUITY MODES OF TRADE IN ASEAN – APRIL 2020 ii PROMOTING NEW FORMS OF TRADE BETWEEN JAPAN AND ASEAN NOTES The terms country and/or economy as used in this study also refer, as appropriate, to territories or areas; the designations employed and the presentation of the material do not imply the expression of any opinion whatsoever on the part of the ASEAN-Japan Centre concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. -

"Thailand's Competitiveness: Meeting the Challenges of Globalization and Environmental Sustainability." (Pdf)

Thailand’s competitiveness: Meeting the challenges of globalization and environmental sustainability Dr. Christian H. M. Ketels Institute for Strategy and Competitiveness Harvard Business School Asia Competitiveness Institute Lee Kuan Yew School of Public Policy The Role of Competitiveness Quality of Life (Prosperity) Economic Outcomes (Productivity) Competitiveness Competitiveness is not everything that matters, but without competitiveness everything that matters is much harder to achieve 2 Traditional Views on Achieving Competitiveness • Conceptual research has increasingly focused on endogenous growth-models • Empirical literature has looked at “deep” drivers of prosperity differences; recent work at unsustainable “growth spurts” • The general principles (Washington consensus, etc.) derived from this work provide often insufficient guidance to policy makers • Emerging consensus for policy advice to become more context-, i.e. country-specific • But without a clear framework, the move from general recipes to country-specific approaches opens the door for old-style intervention • The competitiveness framework offers a systematic structure to make evidence-based policy choices in a concrete situation 3 © Christian Ketels, 2009 The Competitiveness Framework Microeconomi c C ompetiti veness Sophistication Quality of the of Company State of Cluster National Operations and Development Business Strategy Environment Macroeconomic Competitiveness Social Quality of Infrastructure Macroeconomic and Political Policy Institu tions Endowments Natural