Retail Industry Profile, 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

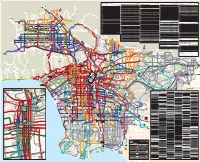

Metro Bus and Metro Rail System

Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Metro Bus Lines East/West Local Service in other areas Weekdays Saturdays Sundays North/South Local Service in other areas Weekdays Saturdays Sundays Limited Stop Service Weekdays Saturdays Sundays Special Service Weekdays Saturdays Sundays Approximate frequency in minutes Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Weekdays Saturdays Sundays 102 Walnut Park-Florence-East Jefferson Bl- 200 Alvarado St 5-8 11 12-30 10 12-30 12 12-30 302 Sunset Bl Limited 6-20—————— 603 Rampart Bl-Hoover St-Allesandro St- Local Service To/From Downtown LA 29-4038-4531-4545454545 10-12123020-303020-3030 Exposition Bl-Coliseum St 201 Silverlake Bl-Atwater-Glendale 40 40 40 60 60a 60 60a 305 Crosstown Bus:UCLA/Westwood- Colorado St Line Route Name Peaks Day Eve Day Eve Day Eve 3045-60————— NEWHALL 105 202 Imperial/Wilmington Station Limited 605 SANTA CLARITA 2 Sunset Bl 3-8 9-10 15-30 12-14 15-30 15-25 20-30 Vernon Av-La Cienega Bl 15-18 18-20 20-60 15 20-60 20 40-60 Willowbrook-Compton-Wilmington 30-60 — 60* — 60* — —60* Grande Vista Av-Boyle Heights- 5 10 15-20 30a 30 30a 30 30a PRINCESSA 4 Santa Monica Bl 7-14 8-14 15-18 12-18 12-15 15-30 15 108 Marina del Rey-Slauson Av-Pico Rivera 4-8 15 18-60 14-17 18-60 15-20 25-60 204 Vermont Av 6-10 10-15 20-30 15-20 15-30 12-15 15-30 312 La Brea -

Brea (Los Angeles), California Oil, Oranges & Opportunities

BUSINESS CARD DIE AREA 225 West Washington Street Indianapolis, IN 46204 (317) 636-1600 simon.com Information as of 5/1/16 Simon is a global leader in retail real estate ownership, management and development and an S&P 100 company (Simon Property Group, NYSE:SPG). BREA (LOS ANGELES), CALIFORNIA OIL, ORANGES & OPPORTUNITIES Brea Mall® is located in the heart of North Orange County, California, a few miles from California State University, Fullerton and their approximately 40,000 students and staff. — Brea and its surrounding communities are home to major corporations including American Suzuki Motor Corporation, Raytheon, Avery Dennison, Beckman Coulter and St. Jude Hospital. — The city’s Art in Public Places has integrated public art with private development. This nationally recognized collection features over 140 sculptures throughout the city including in Brea Mall. — The new master-planned communities of La Floresta and Blackstone, both in the city of Brea and less than four miles from Brea Mall, have added over 2,100 new luxury housing units to the area. — Brea City Hall and Chamber of Commerce offices are adjacent to the mall, located across the parking lot from Nordstrom and JCPenney. — One of the earliest communities in Orange County, Brea was incorporated in 1917 as the city of oil, oranges and opportunity. SOCAL STYLE Brea Mall has long served as a strategic fashion- focused shopping destination for the communities of North Orange County. The center continues in this tradition with a newly renovated property encompassing world-class shopping and dining. BY THE NUMBERS Anchored by Five Department Stores Nordstrom, Macy’s Women’s, Macy’s Men’s & Furniture Gallery, JCPenney Square Footage Brea Mall spans 1,319,000 square feet and attracts millions of visitors annually. -

Pirates Theaters 010308

The Pirates Who Don't Do Anything - A VeggieTales Movie - - - In Theaters January 11th Please note: This list is current as of January 3, 2008 and is subject to change. Additional theaters are being added over the next few days, so be sure to check back later for an updated list. To arrange for group ticket sales, please call 1-888-863-8564. Thanks for your support and we'll see you at the movies! Theater Address City ST Zip Code Sunridge Spectrum Cinemas 400-2555 32nd Street NE Calgary AB(CAN) T1Y 7X3 Scotiabank Theatre Chinook (formerly Paramoun 6455 Macleod Trail S.W. Calgary AB(CAN) T2H 0K4 Empire Studio 16 Country Hills 388 Country Hills Blvd., N.E. Calgary AB(CAN) T3K 5J6 North Edmonton Cinemas 14231 137th Avenue NW Edmonton AB(CAN) T5L 5E8 Clareview Clareview Town Centre Edmonton AB(CAN) T5Y 2W8 South Edmonton Common Cinemas 1525-99th Street NW Edmonton AB(CAN) T6N 1K5 Lyric 11801 100th St. Grande Prairie AB(CAN) T8V 3Y2 Galaxy Cinemas Lethbridge 501 1st. Ave. S.W. Lethbridge AB(CAN) T1J 4L9 Uptown 4922-49th Street Red Deer AB(CAN) T4N 1V3 Parkland 7 Cinemas 130 Century Crossing Spruce Grove AB(CAN) T7X 0C8 Dimond Center 9 Cinemas 800 Dimond Boulevard Anchorage AK 99515 Goldstream Stadium 16 1855 Airport Road Fairbanks AK 99701 Grand 14 820 Colonial Promenade Parkway Alabaster AL 35007 Cinemagic Indoor 1702 South Jefferson Street Athens AL 35611 Wynnsong 16-Auburn 2111 East University Drive Auburn AL 36831 Trussville Stadium 16 Colonial Promenade Shopping Center Birmingham AL 35235 Lee Branch 15 801 Doug Baker Blvd. -

Urban Land Institute Advisory Services Panel June 24-29, 2007

San Bernardino, California San Bernardino Crossroads of the Southwest California Urban Land Institute Urban Land Advisory Services Panel Institute June 24-29, 2007 Advisory Services Panel June 24-29, 2007 San Bernardino Our Sincere Thanks to California • Mayor Patrick J. Morris and staff • Chairman Paul Biane and staff Urban Land • The members of the City Council Institute • The members of the County Board of Supervisors • Other elected city officials • The City’s Economic Development Agency • Citizen leaders / Interviewees Advisory Services Panel June 24-29, 2007 San Bernardino Urban Land Institute California • Established in 1936 Urban Land • Independent non-profit Institute education and research organization • More than 37,000 members worldwide The mission of the Urban Land Institute is to provide leadership in the • Representing the entire responsible use of land and spectrum of land use, in creating and sustaining architecture, planning, thriving communities worldwide. Advisory academic and real estate Services Panel development disciplines June 24-29, 2007 San Bernardino ULI Advisory Services California • Applies the finest expertise in real estate, market analysis, land planning and public policy to Urban Land complex land use and development projects Institute • All volunteer, independent panel • Over 400 ULI-member teams assembled worldwide since 1947 to assist sponsors find creative and practical solutions. Approximately 15 national and international advisory panels per year Advisory Services Panel June 24-29, 2007 San Bernardino -

ORLANDO Vacation Guide & Planning Kit

ORLANDO Vacation Guide & Planning Kit Orlando, Florida Overview Table of Contents Orlando, the undisputed “Vacation Capital of the World,” boasts Orlando, Florida Overview 1 beautiful weather year round, world-class theme parks, thrilling water Getting To And Around Orlando 2 parks, unique attractions, lively dinner theaters, outdoor recreation, Orlando Theme Parks 3 luxurious health spas, fine dining, trendy nightclubs, great shopping Walt Disney World Resort 3 opportunities, championship golf courses and much more. The seat of Universal Orlando® Resort 4 Orange County, Florida, Orlando boasts a population of approximately SeaWorld® Orlando 4 228,000 – making it the sixth largest city in Florida. Easily accessible Orlando Attractions 5 via Interstate 4 and the Florida Turnpike, Orlando is also home to the Orlando Dining 8 Orlando International Airport – the 10th busiest airport in the United Orlando Live Entertainment 8 States and the 20th busiest in the world. Orlando Shopping 9 Orlando Golf 10 Experience the magic of Walt Disney World® Resort – Discover the Orlando Annual Events 11 enchanted lands of Disney’s Magic Kingdom® Park, blast off into the Orlando Travel Tips 13 future at Epcot®, journey through the fascinating history of Hollywood movies at Disney’s Hollywood Studios™ and take a fun-filled safari expedition at Disney’s Animal Kingdom® Theme Park. Don’t miss the thrilling rides at the two amazing theme parks of Universal Orlando® Resort – Universal Studios® Florida and Universal’s Islands of Adventure®, as well as the up-close animal encounters of SeaWorld® Orlando. Cool off at one of Orlando’s state-of-the-art water parks such as Aquatica, Wet ‘n Wild® Water Park, Disney’s Blizzard Beach or Disney’s Typhoon Lagoon. -

NATO Feb 07.Indd

February 2007 NATO of California/Nevada February 2007 NATO of California/Nevada Information for the California and Nevada Motion Picture Theatre Industry CALENDAR Spring/Summer Film Product Seminar of EVENTS & Set for April HOLIDAYS Be among the first to see the adventure, animation, drama and comedy that awaits the movie-going public this coming season. Attend the NATO of California/Nevada 2007 Spring/ Valentine’s Day Summer Film Product seminar on Thursday, April 12th at the February 14 Regal Hacienda Crossing Theatre in Dublin or Tuesday, April 17th at Krikorian Premiere Theatres’ Metroplex 18 At Buena President’s Day Park Downtown. February 19 The full day seminars will begin at 9:00 AM with a conti- Regal’s Hacienda Crossing Theatre nental breakfast, continue in the auditorium at 10:00 AM where Academy Awards the marketing reps from the major studios will present upcoming presentation promotions and product reels from their exciting spring and February 25 summer line-ups. A lunch break will allow time for meeting and visiting with other managers, followed by the concluding Daylight Saving presentations and the ever-popular Goodie Bag distribution. Time Begins Attendance is open to NATO of CA/NV member companies March 11 and is by reservation only, no walk-ins and no substitutions. Due to space limitations we can accommodate no more than ShoWest two persons from each theatre location. Reservation deadline March 12-15 is Friday, March 23rd. See registration on page 2 Krikorian’s Metroplex 18 at Buena Park St. Patrick’s Day March 17 Regal’s Curtis Ewing Joins Spring Begins March 21 Board of Directors Curtis M. -

2018 EARLY DECEMBER 2018 Text & Photos by Mike Ritto [email protected] Fullerton Photo Quiz NEW in TOWN

OBSERVER 40 TH B-D AY page 20 COMMUNITY Fullerton bsCeALErNDAvR Peage 1r 3-15 O EAR FULLERTON’S ONLY INDEPENDENT NEWS • Est.1978 (printed on 20% recycled paper) • Y 40 #20 • EARLY DECEMBER 2018 Submissions: [email protected] • Contact: (714) 525-6402 • Read Online at : www.fullertonobserver.com Vinny De La Torre Honored by Fullerton and France by Ed Paul The City of Fullerton proudly recognized long-time resident, Ventura “Vinny” De La Torre, for his heroic service to his country over 70 years ago. The presentation was made at the November 19 Council meeting and Vinny was given a standing ovation by all present. Vinny De La Torre was also recognized by receiving France’s Legion of Honor, the coun - try’s highest honor, on November 11, 2018, in recognition for his service with Gen. George Patton’s Third Army during WWII. Vinny was in more than 200 days of contin - uous combat, liberating many French cities and in 1945, was part of the division that fought at the Battle of the Bulge and liberated two concentration camps, Buchenwald and Ebensee. He was almost 21 years old at that time. Like many of the WW II generation, Vinny kept much of this story to himself. But in recent years his family, mostly his grandchil - dren, slowly obtained bits and pieces of his service. They conducted some research and provided it to the French Consulate General who, after reviewing it for over a year, made the presentation to Vinny on November 11 at the National Cemetery in West Los Angeles. -

Historic Erie Canal Aqueduct & Broad Street Corridor

HISTORIC ERIE CANAL AQUEDUCT & BROAD STREET CORRIDOR MASTER PLAN MAY 2009 PREPARED FOR THE CITY OF ROCHESTER Copyright May 2009 Cooper Carry All rights reserved. Design: Cooper Carry 2 Historic Erie Canal AQUedUct & Broad Street Corridor Master Plan HISTORIC ERIE CANAL AQUEDUCT & BROAD STREET CORRIDOR 1.0 MASTER PLAN TABLE OF CONTENTS 5 1.1 EXECUTIVE SUMMARY 23 1.2 INTRODUCTION 27 1.3 PARTICIPANTS 33 2.1 SITE ANALYSIS/ RESEARCH 53 2.2 DESIGN PROCESS 57 2.3 HISTORIC PRECEDENT 59 2.4 MARKET CONDITIONS 67 2.5 DESIGN ALTERNATIVES 75 2.6 RECOMMENDATIONS 93 2.7 PHASING 101 2.8 INFRASTRUCTURE & UTILITIES 113 3.1 RESOURCES 115 3.2 ACKNOWLEDGEMENTS Historic Erie Canal AQUedUct & Broad Street Corridor Master Plan 3 A city... is the pulsating product of the human hand and mind, reflecting man’s history, his struggle for freedom, creativity and genius. - Charles Abrams VISION STATEMENT: “Celebrating the Genesee River and Erie Canal, create a vibrant, walkable mixed-use neighborhood as an international destination grounded in Rochester history connecting to greater city assets and neighborhoods and promoting flexible mass transit alternatives.” 4 Historic Erie Canal AQUedUct & Broad Street Corridor Master Plan 1.1 EXECUTIVE SUMMARY CREATING A NEW CANAL DISTRICT Recognizing the unrealized potential of the area, the City of the historic experience with open space and streetscape initiatives Rochester undertook a planning process to develop a master plan which coordinate with the milestones of the trail. for the Historic Erie Canal Aqueduct and adjoining Broad Street Corridor. The resulting Master Plan for the Historic Erie Canal Following the pathway of the original canal, this linear water Aqueduct and Broad Street Corridor represents a strategic new amenity creates a signature urban place drawing visitors, residents, beginning for this underutilized quarter of downtown Rochester. -

Anaheim.Qxp Layout 1 4/26/19 11:09 AM Page 45

City_of_Anaheim.qxp_Layout 1 4/26/19 11:09 AM Page 45 CUSTOM CONTENT • April 29, 2019 Presented By City_of_Anaheim.qxp_Layout 1 4/26/19 11:10 AM Page 46 C-46 ORANGE COUNTY BUSINESS JOURNAL CITY OF ANAHEIM APRIL 29, 2019 City_of_Anaheim.qxp_Layout 1 4/26/19 11:10 AM Page 47 APRIL 29, 2019 CITY OF ANAHEIM ORANGE COUNTY BUSINESS JOURNAL C-47 City_of_Anaheim.qxp_Layout 1 4/26/19 11:10 AM Page 48 C-48 ORANGE COUNTY BUSINESS JOURNAL CITY OF ANAHEIM APRIL 29, 2019 City_of_Anaheim.qxp_Layout 1 4/26/19 11:11 AM Page 49 City_of_Anaheim.qxp_Layout 1 4/26/19 11:11 AM Page 50 C-50 ORANGE COUNTY BUSINESS JOURNAL CITY OF ANAHEIM APRIL 29, 2019 Anaheim Based Firm Wincome USA Rebrands Its Management Division as Wincome Hospitality Wincome USA, a privately owned real-estate investment, development and but now under Marriott’s portfolio). Attributed with multiple awards, including Marriott’s management firm, based in Anaheim, California, announces this week their intent to Franchise Hotel of the Year Award for Distinctive Properties in both 2017 and 2018 for launch Wincome Hospitality, their new hospitality division. With nearly 40 years in the Avenue of the Arts Costa Mesa Hotel, Wincome was able to take another forgotten industry successfully managing multiple hotels and restaurants, Wincome has property and turn it into a market leader. elevated every project and establishment to greater levels of quality and profitability. Their new hospitality division plans to do more of that. In 2016, Wincome purchased an office building at 888 Disneyland Drive—leasing the building to tenants as well as setting up their corporate headquarters. -

NORDSTROM, INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended January 29, 2011 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from____________ to ____________ Commission file number 001-15059 NORDSTROM, INC. (Exact name of registrant as specified in its charter) Washington 91-0515058 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 1617 Sixth Avenue, Seattle, Washington 98101 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code 206-628-2111 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common stock, without par value New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES NO Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES NO Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Cfd 05-8 2018

NEW ISSUE NOT RATED In the opinion of Stradling Yocca Carlson & Rauth, a Professional Corporation, Newport Beach, California (“Bond Counsel”), under existing statutes, regulations, rulings and judicial decisions, and assuming the accuracy of certain representations and compliance with certain covenants and requirements described herein, interest (and original issue discount) on the 2018 Bonds is excluded from gross income for federal income tax purposes and is not an item of tax preference for purposes of calculating the federal alternative minimum tax imposed on individuals. In the further opinion of Bond Counsel, interest (and original issue discount) on the 2018 Bonds is exempt from State of California personal income tax. See the caption “LEGAL MATTERS — Tax Matters” with respect to tax consequences concerning the 2018 Bonds. $5,120,000 COMMUNITY FACILITIES DISTRICT NO. 05-8 (SCOTT ROAD) OF THE COUNTY OF RIVERSIDE SPECIAL TAX BONDS, SERIES 2018 Dated: Date of Delivery Due: September 1, as shown on the inside cover page The Community Facilities District No. 05-8 (Scott Road) of the County of Riverside Special Tax Bonds, Series 2018 (the “2018 Bonds”) are being issued and delivered by Community Facilities District No. 05-8 (Scott Road) of the County of Riverside (the “District”) to (i) provide additional financing for certain public infrastructure improvements along a section of Scott Road, (ii) increase the balance in the reserve fund to equal the Reserve Requirement as of the date of issuance of the 2018 Bonds and (iii) pay the costs of issuance with respect to the 2018 Bonds. See “SOURCES AND USES OF FUNDS” herein.