Branchless Banking: Do Branches Still Matter?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

158877363.Pdf

Company Name NASSCOM Contact Salutation NASSCOM Contact First Name 3D PLM Software Solutions Ltd Mr. Sudarshan 3Five8 Technologies Pvt Ltd Ms. Sangeeta 3Forz Innovations Software Pvt Ltd Mr. Janakiram 3i Infotech Ltd Mr. Prathmesh 4C-Learning Solutions Pvt Ltd Mr. Vivek 4i Apps Solutions Pvt Ltd Mr. Kathiresh Kumar 7Seas Entertainment Ltd Mr. Maruti Sanker A G Technologies Pvt Ltd Mr. Anup A N Buildwell Pvt Ltd Mr. Rohit A T Kearney Ltd Ms. Shilpi A1 Future Technologies Mr. Srish Kumar Aabasoft Mr. Sujas AABSyS Information Technology Pvt Ltd Mr. Ravi Aaric Technologies Pvt Ltd Mr. Vipin Aarupadai Veedu Institute of Technology (VinayakaMr. Missions University) C Thara Abiba Systems Pvt Ltd Mr. Senthil ABM Knowledgeware Ltd Mr. Govind Abra Technologies Pvt Ltd Mr. Yogeshnath AbsolutData Research & Analytics SolutionsMr. Pvt Ltd Suhale Accel Frontline Ltd Mr. Ravi Sankar AccelTree Software Pvt Ltd Mr. Sasikumar Accelya Kale Solutions Ltd Mr. Mitul Accenture Services Pvt Ltd Mr. Rajesh Acclaris Business Solutions Pvt Ltd Mr. Subrata Accretive Health Pvt Ltd Mr. Shailendra Pratap Acidaes Solutions Pvt Ltd Mr. Rahul Ackcezione Technologies Pvt Ltd Mr. Kishore ACL Mobile Ltd Ms. Gunjan Acliv Technologies Pvt Ltd Mr. Achutha ACN Infotech (India) Pvt Ltd Mr. Chaman Acteva Solutions Management Pvt Ltd Ms. Sreeparna ActWitty Software Systems Pvt Ltd Mr. Samarth Adaptive Processes Consulting Pvt Ltd Ms. Ananya ADCC Infocad Pvt Ltd Mr. Amit Add Technologies (India) Ltd Mr. William Adhi Software Pvt Ltd Mr. K Aditya Birla Minacs Worldwide Ltd Ms. Pooja Adobe Systems India Pvt Ltd Mr. Naresh Chand ADP India Ltd Mr. S ADP Pvt Ltd Mr. -

Digital Roadmaps of Financial Institutions 13

Table of contents Incredible Intellect 2 About Intellect Design Arena Limited 3 Numbers That Matter 4 Letter to Shareholders 6 A Culture of Design Thinking 11 Deep Asset Rich Company to accelerate the Digital Roadmaps of Financial Institutions 13 Contextual Banking for the Information Age 17 The Context of Contextual Banking 19 Infusing Progility in Software Implementation with iTurmeric FinCloud 22 Driving Growth through the Levers of Monetisation 24 The Last Mile in Delivering Customer Delight – D-3 OTIF Implementation 26 Brand Beacons 27 Intellect Executive Council 29 Board of Directors 30 Global Oces 31 Chapter 1 Incredible Intellect We live in a world of personalisation. A world where designing products that work in a way that they you can stream video content on platforms that know understand their end customers’ real needs. An what your favourite box sets are and sends you asset-rich organisation with unparalleled expertise in suggestions about what to watch next. A world the financial technologies domain, driven by our belief where you can personalise those new sneakers that in Contextual Banking - this is perhaps why our have just launched in your favourite colours. customers also call us ‘Incredible Intellect’. This is all made possible from having an in-depth The fact that IBS Intelligence Annual Sales League knowledge of the customer. What context they Table 2020 also ranked Intellect’s Revolutionary operate in and what their circumstances are. This is Contextual Banking Technology as #1 in Retail and at the heart of FinTechs too. Transaction Banking, vindicates our pioneering use of Contextual Banking, based on the Design Thinking Welcome to the world of Contextual Banking, where principles. -

Annual Report 2018-19

ANNUAL REPORT 2018-19 SAVIC TECHNOLOGIES PRIVATE LIMITED Email: [email protected] Website: www.savictech.com 3 LETTER TO THE SHAREHOLDER Senthilkumar S Chairman and Managing Director Dear Shareholders, In line with the dividend paying To conclude, I would like to thank On behalf of Board of Directors of tradition, Board of directors are you, shareholders, for your your company, I warmly welcome pleased to recommend dividend unstinted support and confidence you to the 3rd Annual General of 10% on equity shares. in the company. My gratitude Meeting. Thank you for your extends to our stakeholders - presence here today, your Our core business is SAP and we customers, government bodies, continued support and goodwill is will continue to strengthen our channel partners and associates fuelling the success of your foot print with SAP. This year we for their support and, to all the company. have established our alliances employees of the company for with Microsoft, UIPath and TATA their contributions. I thank the We are a modest company, Communications. These alliances Board of Directors for their continuously improving to earn will help us to build a resilient collaboration and support. I wish the trust of our customers. We are business model to improve our the team SAVIC the very best to also a hungry company, unafraid revenue this year. put in a strong growth to embrace bold dreams for big performance in FY 2019-20 and in opportunities ahead. It is critical to align ourselves in the years ahead. SAP’s intelligent enterprise digital FY 18-19 was a difficult year. -

Maveric Systems DATA BU Brochure 09 Copy

BROCHURE ACCURATE DATA FOR PRECISE DECISIONS ACCELERATE YOUR NEXT IN DATA TRANSFORMATION THROUGH PRECISE DECISIONS USING ON DEMAND DATA ENGINEERED FOR ACCURACY OVERVIEW Backed by domain, driven by technology, validated at each step, Maveric DataTech is committed to accelerate your business through precise decisions using on demand data, engineered for accuracy. Maveric’s Domain Data Model (DDM) offers a deep context to a bank’s business. Reinforced by real time integration, it helps gain critical time savings and process efficiencies. A 3-layer accuracy assertion guarantees high level quality by validating every bit of data flowing through the data pipelines. Banking Domain Model On Demand Data Real time Data Integration 3 Layered Accuracy Assertion PRECISE DECISIONS Engineered for Ready to use domain led Accuracy decision models Transformation, Interpretation and Monetization of Data Ready to use data pipelines and data quality solutions OUR STORY SO FAR Partnering with Data Academy building best-in-class Competency across solution providers Domain & Technology Continuous Working with 3 of Innovation by Top 20 World DataTech Labs banks On-Demand Accurate Data, Anytime, Everytime DATA PRECISE DECISIONS OUR DIFFERENTIATORS 2 decades of BFSI experience with a large in-house pool of domain experts Transformation specialists who can deliver tangible results under tough conditions LED BY DOMAIN Wide ranging knowledge across core financial & banking products and their data life cycles 10,000+ person-years of technology transformation experience -

Federal Register/Vol. 80, No. 39/Friday, February 27, 2015/Notices

Federal Register / Vol. 80, No. 39 / Friday, February 27, 2015 / Notices 10715 Dated: February 23, 2015. Register pursuant to Section 6(b) of the Co.LTD, Bangkok, THAILAND, has been Jerri Murray, Act on December 2, 2014 (79 FR 71447). added as parties to this venture. Department Clearance Officer for PRA, U.S. The following members have changed Patricia A. Brink, their names: Elion Ettevo˜tted AS to AS Department of Justice. Director of Civil Enforcement, Antitrust [FR Doc. 2015–04122 Filed 2–26–15; 8:45 am] Eesti Telekom, Tallinn, ESTONIA; Division. LeanMeanBusinessMachine to BILLING CODE 4410–02–P [FR Doc. 2015–04099 Filed 2–26–15; 8:45 am] BumpConductor B.V., Driehuis, BILLING CODE P NETHERLANDS; and Nextel del Peru´ SA to Entel Peru SA, Lima, PERU. DEPARTMENT OF JUSTICE The following members have DEPARTMENT OF JUSTICE Antitrust Division withdrawn as parties to this venture: Antitrust Division 6fusion USA, Inc., Raleigh, NC; Notice Pursuant to the National ArenaCore Pty Ltd., Melbourne, Cooperative Research and Production Notice Pursuant to the National AUSTRALIA; Ariston Global, Pittsford, Act of 1993—Members of SGIP 2.0, Inc. Cooperative Research and Production NY; Aspivia Ltd., Illovo, SOUTH Act of 1993—Telemanagement Forum AFRICA; Atoll Solution Ltd., Urom, Notice is hereby given that, on HUNGARY; BEISIS, Ceroux Mousty, Notice is hereby given that, on BELGIUM; Cloudscaling© (The January 14, 2015, pursuant to Section January 16, 2015, pursuant to Section 6(a) of the National Cooperative Cloudscaling Group, Inc.), San 6(a) of the National Cooperative Francisco, CA; Competitiveness Cluster Research and Production Act of 1993, Research and Production Act of 1993, 15 U.S.C. -

Ites (Including Hardware) Others

3.0 8.0% 2.2 92.0% 2008 2013 IT & ITeS (including hardware) Others • The Indian IT & ITeS sector is pivotal for the Indian economy • The sector’s GDP contribution has increased from 1.2 percent in 1998 to 6.4 percent in 2008 to ~8.0 percent in 2013 driven by significant exports to western countries • The sector has provided new job opportunities and at present employs about 3 million directly and 9.5 million indirectly • The Cabinet in August 2014 has approved the ambitious 'Digital India' programme, which aims to connect all gram panchayats by broadband Internet, promote e-governance and transform India into a connected knowledge economy. Significant talent pool . High ranking on the English . National e-governance proficiency index . Indian firms are plan expanding globally . National Mission on Talent . Business processes Education through ICT support are maturing . Automation of the Public . Increasing customer Distribution System Aspiring Government focus driving ITeS . National Knowledge Indian investments services Network enterprises . Digital India programme Key drivers for IT & ITeS adoption . Managed services . Focus on India as a . BOOT model Aggressive primary market New focus by . Outcome-based business . India-specific R&D service models projects providers . Low-cost, customized . Mobility, cloud and products for the Indian Huge social networking market population technologies base ii . The Indian IT & ITeS sector primarily operates through six major states, including Karnataka, Andhra Pradesh, Maharashtra, Tamil Nadu, Haryana and Uttar Pradesh — major centers of top IT & ITeS firms such as TCS, Infosys, HCL, Tech Mahindra, Cognizant and Capgemini are based in these states. Also, a majority of these centers are based in tier 1 cities of these states, such as Bengaluru, Chennai, Hyderabad, Gurgaon and Noida . -

Data for Digital

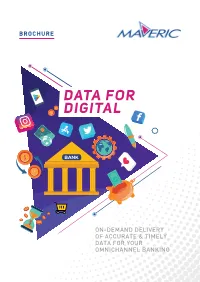

BROCHURE DATA FOR DIGITAL ON-DEMAND DELIVERY OF ACCURATE & TIMELY DATA FOR YOUR OMNICHANNEL BANKING OVERVIEW Extremely delightful customer experiences Customers Preference for Omni-channels Going Digital Anytime, Anywhere is no longer banking (24*7 availability) a choice Evolution of digital first financial products Necessity to compete and collaborate with FinTechs SUCCESS OF DIGITAL BANKING IS DEPENDENT ON ITS FLEXIBLE DATA FABRIC Banks often stumble when it comes to Connecting Balancing Governance Decentralized Systems and Self-Service Inaccurate Data & Enabling Near Maintaining Data Incompatible Architectures Real-Time Data Flows Security & Compliance OUR SOLUTION Data for Digital eliminates the chokepoints that typically plague digital adoption. It is specially designed to ensure accuracy and instant availability, when and where required. When you adopt Data for Digital, you’re choosing a zero error, zero disruption solution. Your enduring banking success will be powered by three critical indicators Real-Time Validate on the Go Govern as you Integration protocol, modelled Consume processes, 01 of multiple 02 from deep domain 03 that address governance sources of data expertise and self-service Data Governance GUI Data Data STORAGE User SOURCES Integration Hub SYSTEMS Core Data APIs/Micro Banking Data Quality and Warehouse services Validation Layer CRM DATA INTEGRATION AGENTS DATA INTEGRATION AGENTS Dashboards RDBMS METADATA Clickstream REPOSITORY ML/AI NoSQL engines Domain Model 3rd party Datasets Portals systems OUR PROMISE Versatile -

Presentation Title

Abstract Application quality assurance is an essential step in the SDLC before going live with the software. In an attempt to shorten the time to market, the size of the test cycles get bigger with increased scope and with participation of larger Test Management – business & IT teams. The monitoring & control of the progress becomes essential as any slippage can spiral Execution Monitoring & out of control quickly. Small things having a larger impact are generally not Control Tool identified quickly enough creating a knock on impact & delay. By Illampooranan This paper deals with a debottlenecking report tool based on HP ALM that generates reports with This paper is useful for great precision based on user demands. PMO/Test Managers/Business Managers involved in Large/Complex Testing programs . Organizations that use HP ALM for Test Management www.maveric-systems.com How does this help ▸ Micro understand without Micro managing: E.g., one can identify that a specific tester is unable to execute a test case for 2 days due to a defect unresolved by developer ▸ Find out the needle in Haystack – pin point a single defect/test case/tester that stops/impacts progress and focus action on the same ▸ Prioritize – One can pick up top 5 issues that hold up significant progress and act with focus, obtain big results with optimum effort ▸ Reusable: Tool is based on HP ALM, can be built in organizations that use HP ALM ▸ Can generate ‘Live’ data – many detailed reports can be produced real time & and any desired frequency, below are list of the few reports » List of all pending/failed/blocked test cases & linked defects » Top ‘n’ defects holding maximum test cases » Business teams behind the plan in execution » Defects vs. -

The Promise of Model-Based Testing

T17 Concurrent Session Thursday 05/08/2008 3:00 PM The Promise of Model-Based Testing Presented by: Mahesh Velliyur Maveric Testing Solutions Presented at: STAREAST Software Testing Analysis & Review May 5-9, 2008; Orlando, FL, USA 330 Corporate Way, Suite 300, Orange Park, FL 32043 888-268-8770 904-278-0524 [email protected] www.sqe.com Mahesh Velliyur Executive Director and Co-Founder, Maveric Systems Ltd. Mahesh Velliyur is an Executive Director and co-founder of Maveric Systems. He has over 20 years of experience in the IT industry in the area of IT Strategy, architecture, design and implementation of IT solutions to the private and government sector. After serving premier consulting and technology organizations, Mahesh started his first entrepreneurial venture in 1992. He has wide ranging experience in delivering complex development and testing solutions to clients in Europe and US through innovative models of delivery. At Maveric, apart from being the architect of Maveric's proprietary testing frameworks and methodologies, Mahesh heads delivery operations of Maveric across the various delivery centers. He takes accountability for all offshore delivery in Maveric. With Maveric rapidly becoming multi-locational in its delivery, Mahesh’s primary challenge is ensuring that clients perceive the same level of responsiveness and capability in Maveric teams across various delivery locations. Mahesh and his team also ensure that we are constantly innovating and improving our testing methods and processes to significantly enhance the quality of our client’s applications. Mahesh holds the belief that test automation will be the one area in testing where we will see the most rapid and radical changes in the coming years. -

Building Inspired Leaders with Character, Competence and Enthusiasm

Building Inspired Leaders with Character, Competence and Enthusiasm Student Placement Dossier 2016-17 2 SOIL was co-created by a team of thoughtful business leaders and 32 companies with the aim to build Leaders with character, competence and enthusiasm. We believe that businesses, in course of their routine operations can create social good, ecological balance, holistic development and healthy international relations if they choose to act in inspired ways. Our learning methodology can inculcate inspired thinking and consequently inspired actions in the business leaders of the future who will contribute to the triple bottom line of social wellbeing, ecological sustainability and shareholder value as a deviation from current excessive focus on shareholder value. SOIL was created to fulfill this vision and hence is a “game changer”. Format: Full Time Profile: Graduates Length: 12 months of any discipline with minimum 2 years of work experience Intake: April Language: English Campus: Gurgaon, Services Capital of India and a booming start-up hub Exchange International Dedicated Career Programs: With Faculty: Leading Services: 100% prestigious and names from placements within internationally academia and 3 months of recognized industry across the graduation business schools globe invited as abroad visiting faculty. 3 Letter from Founder & Dean I am glad to present the eighth batch of SOIL students – the batch of 2017, who call themselves the 'Self-Starters'. Inspiration is about being cognizant of one's own strengths and achieving success by focusing on these. At SOIL, the students systematically develop their self-awareness and learn about their strengths. This prepares them to be leaders who This year the School of Inspired Leadership (SOIL) are compassionate, adapt well to changes, believe student body is initiating a 'Dialogue Across in ethics over personal gains and sustain in Differences'. -

SEC/SE/120/18-19 Chennai, August 02, 2018 Corporate Relationship Department Bombay Stock Exchange Limited PJ Towers, Dalal Stree

SEC/SE/120/18-19 Chennai, August 02, 2018 Corporate Relationship Department Bombay Stock Exchange Limited PJ Towers, Dalal Street Mumbai – 400001 Sub: Submission of Annual Report for the Financial Year 2017-18 Ref: Company Symbol: SQSBFSI Dear Sir/Madam, Pursuant to Regulation 34 (1) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, please find attached the Annual Report of the Company for the financial year 2017-18. You are requested to take the above on record and oblige. Thanking you, Yours faithfully, For SQS India BFSI Limited S. Sampath Kumar Company Secretary and Compliance Officer FCS No.3838 SQS India BFSI Limited sqs-bfsi.com 6A, Sixth Floor, Prince InfoFity II, SQS India BFSI Limited sqs-bfsi.com No. 283/3 & 283/4, Rajiv Gandhi Salai (OMR), Kandanchavadi, Chennai – 600 096, India, Annual Report FY 201 - 201 Phone: +91 44 4392 3200 sqs-bfsi.com SQS India BFSI Business Locations Other SQS Group Business Locations Printed by Chennai Micro Print (P) Ltd. - 77 Transforming the World Through Quality SQS India BFSI Limited Corporate information BOARD OF DIRECTORS Diederik Vos Chairman & Director Aarti Arvind Managing Director & Chief Executive Offi cer K. Ramaseshan Executive Director & Chief Financial Offi cer Prof. K Kumar Independent Director Lilian Jessie Paul Independent Director Prof. S Rajagopalan Independent Director Rajiv Kuchhal Independent Director René Gawron Non-Executive Director Ulrich Bäumer Independent Director COMPANY SECRETARY & S Sampath Kumar COMPLIANCE OFFICER AUDITORS Kalyaniwalla & Mistry LLP Chartered Accountants Esplanade House, 29, Hazarimal Somani Marg, Fort, Mumbai – 400 001. INTERNAL AUDITORS A. Murali & Associates, Chartered Accountants New No.2, T4, 3rd Floor, Majestic Square, Sherfudeen Street, Choolaimedu, Chennai-600 094 BANKERS The Lakshmi Vilas Bank Limited Cathedral Road, Chennai-600 086 ICICI Bank Limited Bazullah Road, T. -

20 Leading Software Testing Providers 2014

20 LEADING SOFTWARE TESTING PROVIDERS 2014 TCS A: 4th Floor, 33 Grosvenor Place, London, SW1X 7HY, UK T: +44 (0) 207 245 1800 E: [email protected]; [email protected] W: www.tcs.com TCS in UK and EUROPE… with a 38-year old successful track record Since 1975, Tata Consultancy Services (TCS) has been helping UK and European businesses become more effective. TCS UK and Europe service over 350 customers across UK and the continent, including 44 of the FT Europe Top 100 companies. TCS is a major UK and Europe employer with over 50,000 people across 50 locations. The TCS facility in Peterborough is home to the FCA-regulated subsidiary, Diligenta, one of the UK‟s largest pension policy administrators. It also hosts a TCS Innovation Centre, part of TCS‟ global innovation network. In Liverpool, TCS has invested in a state of the art delivery centre dedicated to the public sector. About TCS worldwide TCS is an IT services, consulting and business solutions organisation that delivers real results to global business, ensuring a level of certainty no other firm can match. TCS is a part of the Tata Group, one of the largest and most innovative industrial conglomerates with 100 companies. Building on more than 40 years of experience, TCS adds real value to global organisations through domain expertise, proven solutions and world-class service. TCS has 300,000 plus employees, representing 118 nationalities. TCS partners with clients across 44 countries. Repeat customers contribute to 99% of TCS‟s revenue. Awards and recognitions • Ranked No.1 for customer satisfaction in UK IT Services – Whitelane research, 2014 and 2013.