Related Companies: Guidance for Higher Education Institutions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View Annual Report

Pressure Technologies Annual Report & Accounts 2007 The Board of Directors of Pressure Technologies plc (Left to right) Nigel Luckett, Non-executive Director; John Hayward, Chief Executive; Richard Shacklady, Non-executive Chairman. The Operational Board of Directors of Chesterfield Special Cylinders Limited (Standing – left to right) John Brown, John Hayward (Managing Director), Philip Redfern. (Seated – left to right) Philip Catton, Alan Harding. Pressure Technologies plc Contents of the Annual Report Page Company information 2 Chairman’s statement 3 Chief Executive’s statement 4 Directors’ report 6 Independent auditors’ report to the shareholders 12 Consolidated profit and loss account 13 Consolidated statement of total recognised gains and losses 13 Consolidated balance sheet 14 Company balance sheet 15 Consolidated cash flow statement 16 Notes to the financial statements 17 1 Pressure Technologies plc Company information Directors R.L.Shacklady – non-executive Chairman J.T.S.Hayward – Chief Executive N.F.Luckett – non-executive Secretary T.J.Lister Registered office Meadowhall Road Sheffield S9 1BT Registered number 06135104 Website www.pressuretechnologies.com Nominated advisor Brewin Dolphin Securities 34 Lisbon Street Leeds LS1 4LX Auditors Grant Thornton UK LLP Chartered Accountants Centre City Tower 7 Hill Street Birmingham B5 4UU Solicitors Hlw Commercial Lawyers LLP Commercial House Commercial Street Sheffield S1 2AT Bankers Bank of Scotland 7 Leopold Street Sheffield S1 2FF Registrars Capita Registrars Northern House Woodsome Park Fenay Bridge Huddersfield HD8 0LA 2 Pressure Technologies plc Chairman’s statement Following our successful listing on AIM in June 2007, it gives me great pleasure to present our first Annual Report as a public company. -

Guardian Public Article Promotional Leaflet.Pmd

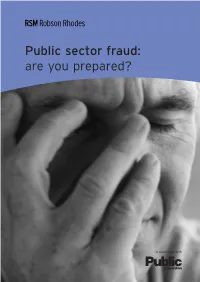

Public sector fraud: are you prepared? in association with Introduction Fraud can take different forms and can Our in-depth survey of UK companies RSM Robson Rhodes is pleased to be impact on organisations in many ways. last year, backed by the Home Office, associated with the Guardian Public It includes embezzlement, bribery, Fraud Advisory Panel and CBI, estimated initiative to raise awareness and cheque and credit card fraud, corruption, the annual total losses due to corporate research public sector fraud. This leaflet computer crime, identity theft, fraud at £32bn with a further £8bn spent features the output from a roundtable procurement fraud, benefit, revenue on prevention. discussion of experts convened by the and VAT fraud. Guardian and RSM Robson Rhodes in The Public Sector does not escape May 2005 which provided the impetus Recent research and trends indicate fraudulent activity and particularly as for a new survey into the issue. that fraud is a growing, global, issue public spending increases so does the and affects organisations of all types opportunity to defraud the system. You are encouraged to participate in this and sizes. Money laundering of the survey; its findings are likely to inform Public sector fraud can involve members proceeds of crime is also growing. public sector policy in combating fraud. of the public, employers in and suppliers to the public sector alike. This unique roundtable event Whilst everyone at the meeting had brought together a broad range a slightly different perspective and, of expertise from across the public possibly, a slightly different agenda sector — resulting in a compelling there was broad agreement in many discussion on fraud. -

VINCI PLC Annual Report 2004 Contents

VINCI PLC Annual Report 2004 Contents Company Information Consolidated Profit and Loss Account 01 18 Chief Executive’s Report Consolidated Balance Sheet 03 19 Directors’ Report Company Balance Sheet 14 20 Independent Auditors’ Report Consolidated Cash Flow Statement 16 21 Notes to the Cash Flow Statement 22 Accounting Policies 23 Notes to the Accounts 26 Principal Subsidiary Undertakings 48 Principal Offices 49 Cover: Vauxhall Cross Interchange, London. This Page: The Butterfly House, Surrey. Company Information Directors (Chairman & Chief Executive) J O M Stanion A M Comba D A L Joyce E M M Zeller (Non-Executive) J C Banon (Non-Executive) P J G Billon (Non-Executive) Q Davies MP (Non-Executive) X M P Huillard (Non-Executive) P J W Ratynski (Non-Executive) A Zacharias Secretary D W Bowler Registered Office Astral House Imperial Way Watford Hertfordshire WD24 4WW Registered Number 737204 Auditors RSM Robson Rhodes LLP Colwyn Chambers 19 York Street Manchester M2 3BA Bankers National Westminster Bank Plc P O Box 2DG 208 Piccadilly London W1A 2DG 01 Tower Place, London. 02 “The Group entered 2005 with a record level of work in hand” Chief Executive’s Report VINCI PLC made solid progress in 2004 with a 37% increase in profit to £11.5 million before tax compared with £8.4 million the previous year. The significant cost increases incurred in 2003, of which pension contributions were the principal cause, were fully absorbed in 2004 with a strong recovery in net margins at the operating level. The pre tax margin on sales increased to 2.3%. The Group entered 2005 with a record level of work in hand and the order book has since grown to over £500 million. -

Norwest Holst Group PLC Report and Accounts 2000 1234

Norwest Holst Group PLC Report and Accounts 2000 1234 Cover Pictures - 1 Vasco da Gama Bridge, Lisbon. 2 Cambridge Business Park. 3 Bute Avenue, Cardiff. 4 ProLogis Park, Hounslow. Norwest Holst Group PLC Contents page Company Information 1 Financial Highlights 3 Chief Executive’s Report 4 Directors’ Report 14 Auditors’ Report 17 Consolidated Profit and Loss Account 19 Consolidated Statement of Total Recognised Gains and Losses 20 Consolidated Balance Sheet 21 Company Balance Sheet 22 Consolidated Cash Flow Statement 23 Notes to the Cash Flow Statement 24 Accounting Policies 26 Notes to the Accounts 29 Principal Subsidiary Undertakings 44 Principal Offices 45 Norwest Holst Group PLC Synopsis 46 Cambridge Business Park Cambridge Business Park ProLogis Park, Hounslow Six contracts have been successfully negotiated to build office accommodation at A high specification warehouse and office development in Hounslow forms part of an Cambridge Business Park. ongoing construction programme across the country for ProLogis Developments Limited. Norwest Holst Group PLC Company Information DIRECTORS J O M Stanion (Chairman & Chief Executive) A M Comba E M M Zeller J C Banon (Non-executive) P J G Billon (Non-executive) X M P Huillard (Non-executive) A Zacharias (Non-executive) SECRETARY D W Bowler REGISTERED OFFICE Astral House Imperial Way Watford Hertfordshire WD24 4WW REGISTERED NUMBER 737204 AUDITORS RSM Robson Rhodes Colwyn Chambers 19 York Street Manchester M2 3BA BANKERS National Westminster Bank Plc 1 Bute Avenue, Cardiff - A £120 million privately -

IPA Students up to the Mark

autumn 2005 student bulletin IPAIPA Students up to the Mark In this edition CPI and Early Entry Commenting on the 23% increase in students sitting this year’s Certificate Examinations June 2005 of Proficiency in Insolvency Examination, IPA President Louise Verrill said: Results “It is hugely encouraging for the future of the profession that more people than ever before are taking the CPI to acquire a now well recognised and CPI Examiner’s Report valued insolvency qualification.” There was also an increase in the pass rate – 69% compared with 61% in 2004. JIE: The Price of Success – A Season without Spurs Jonathan Birch, Chairman of the Examinations & “More sat the EEE Training Committee, said that the CPI represented a good test of all round practical Accounting paper in June E&T Student Issues insolvency knowledge, and it was evident that Sub-Group students had worked hard to build on their desk 2005 than in the previous work and deliver some excellent results. He particularly congratulated the prize winners – year’s two sittings, with a Kiri Jimmieson, Begbies Traynor (first); Mark Patterson, BDO Stoy Hayward, and pass rate of 81% and 13 of Amanda Jones, Begbies Traynor (joint second); Please pass this on and Brendan Hogan, Unity (third) – and the the 21 pass students achieving nine students who had achieved distinctions. If you know someone in your firm The full CPI June 2005 results are on the back distinctions or merits.” who might be thinking about, or page of this edition. could be encouraged to think There were also increases in the numbers about, studying for an insolvency sitting the Early Entry Examinations as a Antoinette Thorpe, McCambridge Duffy & Co; qualification, why not pass this preliminary step towards the Joint Insolvency and Ivy Yeap, K S Tan & Co. -

University of Huddersfield Repository

CORE Metadata, citation and similar papers at core.ac.uk Provided by University of Huddersfield Repository University of Huddersfield Repository Filatotchev, Igor, Jackson, Gregory, Gospel, Howard and Allcock, Deborah Key drivers of 'good' corporate governance and the appropriateness of UK policy responses : final report Original Citation Filatotchev, Igor, Jackson, Gregory, Gospel, Howard and Allcock, Deborah (2007) Key drivers of 'good' corporate governance and the appropriateness of UK policy responses : final report. Project Report. The Department of Trade and Industry and King's College London, London, UK. This version is available at http://eprints.hud.ac.uk/473/ The University Repository is a digital collection of the research output of the University, available on Open Access. Copyright and Moral Rights for the items on this site are retained by the individual author and/or other copyright owners. Users may access full items free of charge; copies of full text items generally can be reproduced, displayed or performed and given to third parties in any format or medium for personal research or study, educational or not-for-profit purposes without prior permission or charge, provided: • The authors, title and full bibliographic details is credited in any copy; • A hyperlink and/or URL is included for the original metadata page; and • The content is not changed in any way. For more information, including our policy and submission procedure, please contact the Repository Team at: [email protected]. http://eprints.hud.ac.uk/ KEY DRIVERS OF ‘GOOD’ CORPORATE GOVERNANCE AND THE APPROPRIATENESS OF UK POLICY RESPONSES Final Report Igor Filatotchev, Gregory Jackson, Howard Gospel, Deborah Allcock King’s College London, University of London JANUARY 2007 About this publication The project manager for this report was Sheetal Radia, Economic Adviser, Corporate Law and Governance Directorate, Department of Trade and Industry Published in January 2007 by the Department of Trade and Industry. -

Annual Report 2018 2 FOREWORD

Grant Thornton UK LLP Annual report for year ending 30 June 2018 REGISTERED NO. OC307742 Contents Foreword 2 Our markets 6 Business Review – Our culture 18 Business Review – Quality 21 Business Review – Our financial performance 24 Members’ Report 27 Independent Auditor’s Report 30 Consolidated statement of comprehensive income 37 Consolidated statement of financial position 39 Consolidated statement of changes in equity 41 Consolidated statement of cash flows 42 Operating activities notes and accounting policies 44 Investing activities notes and accounting policies 59 Financing activities notes and accounting policies 70 Extended notes and accounting policies 82 Statement of financial position for the parent entity 101 Statement of changes in equity for the parent entity 102 Notes to the parent entity financial statements 103 Independent Auditor’s Report to the members of the parent entity 112 Index 115 FOREWORD This is my first Annual Report as Grant Thornton’s CEO and I am delighted to have been given the privilege to lead this firm at an important stage of its “I am confident that with a relentless focus on our evolution. three markets and a purpose which is underpinned There is no escaping the fact that it has been a tough year for Grant Thornton. by a strong culture, we will add value to clients, The decision by an individual to disclose confidential and private information about the firm, and about our former CEO Sacha Romanovitch, was create opportunities for our people, deliver high unprofessional and disappointing. I want to make it clear that Grant Thornton quality work and achieve sustainable growth” UK condemns such actions and take the opportunity to apologise to Sacha and thank her for her leadership. -

Annual Report 2005/06 L I C N U

6 0 / 5 0 0 2 T R O P E INANCIAL EPORTING OUNCIL R F R C L A U N N A ANNUAL REPORT 2005/06 L I C N U O MAY 2006 C G N I T R O P E R L A I C N A N I F FINANCIAL REPORTING COUNCIL ANNUAL REPORT 2005/06 MAY 2006 Financial Reporting Council Annual Report 2005/06 Introduction to the FRC The FRC's aim is to promote confidence in corporate reporting and governance. The regulatory role of the FRC is to define high standards in corporate reporting, auditing, actuarial practice and corporate governance and, where appropriate, to oversee the application of those standards. We see this role as vital to the healthy functioning of business and markets and thus as making a significant contribution to the economy overall and the UK's competitiveness in international markets. We know that no system of regulation can eliminate the possibility of corporate reporting or governance failures. But we are certain that proper definition and promotion of good practice will substantially reduce risk and improve performance. We believe in the value of thorough consultation and research as the best way to secure the application of high standards in practice. We, therefore, pay close and continuous attention to the views of practitioners, particularly investors, businesses and the professions. We recognise the central role of the professions in formulating and applying accounting, auditing and actuarial standards. Judgement by practitioners in the light of particular circumstances is fundamental to good reporting and governance. -

84109 Ofwat SC

Annual report 2002–03 >> of the Director General of Water Services Our vision << A water industry that delivers a world-class service, representing best value to customers now and in the future. Our mission << To regulate in a way that provides incentives and encourages the companies to achieve a world-class service in terms of quality and value for customers in England and Wales. How we do it << By: >> Setting price limits at levels which: – enable well-managed companies to finance the delivery of services in line with relevant standards and requirements; – provide incentives for companies to improve efficiency and service delivery; – share the benefits between customers and investors. >> Ensuring that we are aware of stakeholders’ views and priorities by consulting with customer groups, the industry and others, and undertaking customer surveys. >> Facilitating the development of competition to promote further efficiency gains and, where practicable, further choice for customers. >> Working with the quality regulators to make sure that Ministers have the information they need to set the quality improvement programme within a long-term framework. >> Ensuring that customers’ tariffs are fair and do not unduly discriminate or show preference to any class of customer. >> Handling disputes and complaints involving the companies economically, effectively and fairly. >> Monitoring the companies’ performance and taking action, where necessary, to protect the interests of customers and other stakeholders. >> Openly and transparently publishing information, which allows customers and other stakeholders to have their say in regulatory decisions. >> Making sure that Ofwat delivers best value in its regulatory role and by valuing and encouraging the development of its entire staff. -

Three Essays on Audit Regulation, Audit Market Structure, and the Quality of Financial Statements

Three Essays on Audit Regulation, Audit Market Structure, and the Quality of Financial Statements Dissertation zur Erlangung des akademischen Grades Doktor der Wirtschaftswissenschaften (Dr. rer. pol) am Fachbereich Wirtschaftswissenschaften der Universität Konstanz Vorgelegt von: Benjamin Heß Tag der mündlichen Prüfung: 09. Juli 2014 1. Referentin: Prof. Dr. Ulrike Stefani 2. Referent: Prof. Dr. Jens Jackwerth Contents Summary ..................................................................................................................... 1 Zusammenfassung .......................................................................................................... 5 Chapter 1: Audit Market Regulation and Supplier Concentration around the World: Empirical Evidence .................................................................... 10 1.1 Motivation ........................................................................................................ 11 1.2 The Regulatory Environment of Statutory Audits and its possible Effects on the Market Structure ............................................................................................... 14 1.3 Supplier Concentration and Competition in the National Audit Markets ........ 27 1.3.1 Sampling .................................................................................................... 27 1.3.2 Measures for Audit Market Concentration and Competition .................... 30 1.3.3 Variables for Audit Regulation and Country-Specific Characteristics ..... 37 1.4 Regression Analysis -

The Suppliers of Statutory Audit Services to Large Companies

STATUTORY AUDIT SERVICES MARKET INVESTIGATION The suppliers of statutory audit services to large companies Introduction 1. This paper provides an overview of the suppliers of statutory audit services in the UK and the history of their consolidation (paragraphs 2 to 21). It then provides a brief portrait of each of nine large firms which have provided statutory audit services to large listed companies in the UK in turn: Baker Tilly, BDO, Deloitte, Ernst and Young (EY), Grant Thornton, KPMG, Mazars, PKF, and PwC. Overview and the history of consolidation The structure of the UK firms and their international networks 2. The four largest UK firms (Deloitte, EY, KPMG and PwC) are members of international networks of broadly similar scale. Each operating in approximately 150 territories and employing between 145,000 and 182,000 partners and staff in total. The members firms of the networks share a name, brand, a commitment to audit quality standards and common methodologies but member firms remain legally separate, and are typically independently owned and controlled. Member firms are brought together by common membership of a central network body or entity. The EY network differs through the greater level of ‘global integration’ and this is discussed below. 3. Most of the other large firms (Baker Tilly, BDO, Grant Thornton and PKF) are also members of networks (Mazars by contrast has adopted a global ‘integrated partnership’).1 The legal structure of these networks is broadly similar to the four largest networks and are differentiated primarily by the combined size of their member firms. Geographic coverage (measured by the number of countries in which 1 Mazars is included in the comparisons of networks. -

Related Companies: Guidance for Higher Education Institutions

December 2005/48 Higher education institutions set up related companies for a variety of reasons to help them Good practice manage their activities efficiently and flexibly. Guidance for governors and senior This guide outlines the issues and risks managers associated with assurance, compliance and accountability that are faced by institutions when using related companies. The guidance is not prescriptive, but a tool for institutions to use as they think fit. Related companies: guidance for higher education institutions Produced for the UK funding bodies by RSM Robson Rhodes © HEFCE 2005 Contents Section Page 1 Executive summary 2 2 Introduction 5 3 Risk assessment guidance 10 4 Activities and entities for related company activity 30 5 Checklists 36 Acknowledgements 53 Glossary of terms 55 Appendices (separate file on the web at www.hefce.ac.uk under Publications) Appendix I – Duties of the Nominated Officer 58 Appendix II – Nominated Officer’s report 59 Appendix III – Duties of companies’ officers 66 Appendix IV – Contents of key documents 69 Appendix V – Specimen memorandum of understanding 74 Appendix VI – Outline business plan 78 Appendix VII – Protection and exploitation of technology and intellectual 97 property rights 1 1 Executive summary Introduction 1. Institutions set up related companies for a variety of reasons: for example to carry out commercial activities, to provide a focus for commercial enterprise in a culture different from that of the institution itself, or to protect the institution's charitable status and/or provide advantageous tax or estate planning. Increasingly, related companies are also being used to commercially exploit intellectual property. 2. Related companies provide institutions with opportunities to manage their business efficiently and with a degree of flexibility and varying involvement.