ACQUISITION RESTRUCTURE and EXPANSION PLAN on INSEL AIR Revised

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

CTA Carriers US DOT Carriers

CTA Carriers The Canadian Transportation Agency (CTA) has defined the application and disclosure of interline baggage rules for travel to or from Canada for tickets issued on or after 1 April 2015. The CTA website offers a list of carriers filing tariffs with the CTA at https://www.otc-cta.gc.ca/eng/carriers-who-file-tariffs-agency. US DOT Carriers The following is a list of carriers that currently file general rule tariffs applicable for travel to/from the United States. This list should be used by subscribers of ATPCO’s Baggage product for determining baggage selection rules for travel to/from the United States. For international journeys to/from the United States, the first marketing carrier’s rules apply. The marketing carrier selected must file general rules tariffs to/from the United States. Systems and data providers should maintain a list based on the carriers listed below to determine whether the first marketing carrier on the journey files tariffs (US DOT carrier). Effective Date: 14AUG17 Code Carrier Code Carrier 2K Aerolineas Galapagos (AeroGal) AA American Airlines 3P Tiara Air Aruba AB Air Berlin 3U Sichuan Airlines AC Air Canada 4C LAN Colombia AD Azul Linhas Aereas Brasileiras 4M LAN Argentina AF Air France 4O ABC Aerolineas S.A. de C.V. AG Aruba Airlines 4V BVI Airways AI Air India 5J Cebu Pacific Air AM Aeromexico 7I Insel Air AR Aerolineas Argentinas 7N Pan American World Airways Dominicana AS Alaska Airlines 7Q Elite Airways LLC AT Royal Air Maroc 8I Inselair Aruba AV Avianca 9V Avoir Airlines AY Finnair 9W Jet Airways AZ Alitalia A3 Aegean Airlines B0 Dreamjet SAS d/b/a La Compagnie Page 1 Revised 31 July 2017 Code Carrier Code Carrier B6 JetBlue Airways GL Air Greenland BA British Airways HA Hawaiian Airlines BE Flybe Group HM Air Seychelles Ltd BG Biman Bangladesh Airlines HU Hainan Airlines BR Eva Airways HX Hong Kong Airlines Limited BT Air Baltic HY Uzbekistan Airways BW Caribbean Airlines IB Iberia CA Air China IG Meridiana CI China Airlines J2 Azerbaijan Airways CM Copa Airlines JD Beijing Capital Airlines Co., Ltd. -

Attachment F – Participants in the Agreement

Revenue Accounting Manual B16 ATTACHMENT F – PARTICIPANTS IN THE AGREEMENT 1. TABULATION OF PARTICIPANTS 0B 475 BLUE AIR AIRLINE MANAGEMENT SOLUTIONS S.R.L. 1A A79 AMADEUS IT GROUP SA 1B A76 SABRE ASIA PACIFIC PTE. LTD. 1G A73 Travelport International Operations Limited 1S A01 SABRE INC. 2D 54 EASTERN AIRLINES, LLC 2I 156 STAR UP S.A. 2I 681 21 AIR LLC 2J 226 AIR BURKINA 2K 547 AEROLINEAS GALAPAGOS S.A. AEROGAL 2T 212 TIMBIS AIR SERVICES 2V 554 AMTRAK 3B 383 Transportes Interilhas de Cabo Verde, Sociedade Unipessoal, SA 3E 122 MULTI-AERO, INC. DBA AIR CHOICE ONE 3J 535 Jubba Airways Limited 3K 375 JETSTAR ASIA AIRWAYS PTE LTD 3L 049 AIR ARABIA ABDU DHABI 3M 449 SILVER AIRWAYS CORP. 3S 875 CAIRE DBA AIR ANTILLES EXPRESS 3U 876 SICHUAN AIRLINES CO. LTD. 3V 756 TNT AIRWAYS S.A. 3X 435 PREMIER TRANS AIRE INC. 4B 184 BOUTIQUE AIR, INC. 4C 035 AEROVIAS DE INTEGRACION REGIONAL 4L 174 LINEAS AEREAS SURAMERICANAS S.A. 4M 469 LAN ARGENTINA S.A. 4N 287 AIR NORTH CHARTER AND TRAINING LTD. 4O 837 ABC AEROLINEAS S.A. DE C.V. 4S 644 SOLAR CARGO, C.A. 4U 051 GERMANWINGS GMBH 4X 805 MERCURY AIR CARGO, INC. 4Z 749 SA AIRLINK 5C 700 C.A.L. CARGO AIRLINES LTD. 5J 203 CEBU PACIFIC AIR 5N 316 JOINT-STOCK COMPANY NORDAVIA - REGIONAL AIRLINES 5O 558 ASL AIRLINES FRANCE 5T 518 CANADIAN NORTH INC. 5U 911 TRANSPORTES AEREOS GUATEMALTECOS S.A. 5X 406 UPS 5Y 369 ATLAS AIR, INC. 50 Standard Agreement For SIS Participation – B16 5Z 225 CEMAIR (PTY) LTD. -

Air Travel Consumer Report

U.S. Department of Transportation Air Travel Consumer Report A Product Of The OFFICE OF AVIATION ENFORCEMENT AND PROCEEDINGS Aviation Consumer Protection Division Issued: November 2016 1 Flight Delays September 2016 1 Mishandled Baggage September 2016 January - September 2016 1 3rd. Oversales Quarter 2016 January - September 2016 2 Consumer Complaints September 2016 (Includes Disability and January - September 2016 Discrimination Complaints) Customer Service Reports to the Dept. of Homeland Security3 September 2016 Airline Animal Incident Reports4 September 2016 1 Data collected by the Bureau of Transportation Statistics. Website: http://www.bts.gov 2 Data compiled by the Aviation Consumer Protection Division. Website: http://www.transportation.gov/airconsumer 3 Data provided by the Department of Homeland Security, Transportation Security Administration 4 Data collected by the Aviation Consumer Protection Division 2 TABLE OF CONTENTS Section Section Page Page Flight Delays (continued) Introduction Table 11 24 2 List of Regularly Scheduled Flights with Tarmac Flight Delays Delays Over 3 Hours, By Carrier Explanation 3 Table 11A 25 Table 1 4 List of Regularly Scheduled International Flights with Overall Percentage of Reported Flight Tarmac Delays Over 4 Hours, By Carrier Operations Arriving On Time, by Carrier Table 12 26 Table 1A 5 Number and Percentage of Regularly Scheduled Flights Overall Percentage of Reported Flight With Tarmac Delays of 2 Hours or More, By Carrier Operations Arriving On Time and Carrier Rank, Footnotes 27 by Month, -

Air Travel Consumer Report

U.S. Department of Transportation Air Travel Consumer Report A Product Of The OFFICE OF AVIATION ENFORCEMENT AND PROCEEDINGS Aviation Consumer Protection Division Issued: August 2017 Flight Delays1 June 2017 Mishandled Baggage1 June 2017 January - June 2017 Oversales1 2nd. Quarter 2017 January - June 2017 Consumer Complaints2 June 2017 (Includes Disability and January - June 2017 Discrimination Complaints) Airline Animal Incident Reports4 June 2017 Customer Service Reports to the Dept. of Homeland Security3 June 2017 1 Data collected by the Bureau of Transportation Statistics. Website: http://www.bts.gov 2 Data compiled by the Aviation Consumer Protection Division. Website: http://www.transportation.gov/airconsumer 3 Data provided by the Department of Homeland Security, Transportation Security Administration 4 Data collected by the Aviation Consumer Protection Division 2 TABLE OF CONTENTS Section Section Page Page Flight Delays (continued) Introduction Table 11 37 2 List of Regularly Scheduled Flights with Tarmac Flight Delays Delays Over 3 Hours, By Carrier Explanation 3 Table 11A 38 Table 1 4 List of Regularly Scheduled International Flights with Overall Percentage of Reported Flight Tarmac Delays Over 4 Hours, By Carrier Operations Arriving On Time, by Carrier Table 12 39 Table 1A 5 Number and Percentage of Regularly Scheduled Flights Overall Percentage of Reported Flight With Tarmac Delays of 2 Hours or More, By Carrier Operations Arriving On Time and Carrier Rank, Footnotes 40 by Month, Quarter, and Data Base to Date Appendix 41 -

SMS Service Is a Way We Use to Keep You Updated in Real Time on Departure Times, Possible Delays Or Cancellations (Starting 7 Days Before Departure)

SMS Service Terms and Conditions What is SMS Service? SMS Service is a way we use to keep you updated in real time on departure times, possible delays or cancellations (starting 7 days before departure). This SMS Service is only for additional information. What do you need to do? The only thing you need to do is enter your mobile phone number when you make a booking, so that we can keep you updated on departure time(s) and the status of your flight(s). * Please note: the SMS service is not available if one or more parts of the journey are being made by train. How does the SMS Service work? • The SMS Service provides you with real-time information about your flight. • You are automatically updated with the flight's status. • The service covers almost all flights worldwide. • We do not charge you for receiving SMS messages. It is possible that your phone service provider may apply charges for each message you receive (to find out more, contact your phone provider). What SMS messages will I receive? • After registering for the SMS Service you receive a welcome text with your flight details. • In the welcome message there is a link to a personalized mobile web-page that can be accessed 24/7 (whenever you have access to the network) which has the following data: • Current flight times, both departure and arrival • Direct link to on-line check-in • Check-in desks • Departure terminal and gate • Arrival terminal and gate • Baggage carousel information • Weather forecast for the next 3 days at your destination • Starting 7 days before departure, we monitor the flight for any potential delays or cancellation. -

(VWP) Carriers

Visa Waiver Program (VWP) Signatory Carriers February 1, 2020 In order to facilitate the arrival of Visa Waiver Program (VWP) passengers, carriers need to be signatory to a current agreement with U.S. Customs and Border Protection (CBP). A carrier is required to be signatory to an agreement in order to transport aliens seeking admission as nonimmigrant visitors under the VWP (Title 8, U.S.C. § 1187(a)(5). The carriers listed below are currently signatory to the VWP and can transport passengers under the program. The date indicates the expiration of the current signed agreement. Agreements are valid for 7 years. If you transport VWP passengers and are not a signatory carrier, fines will be levied. Use the following link to apply to CBP to become a Signatory Carrier: https://www.cbp.gov/travel/international-visitors/business-pleasure/vwp/signatory-status # 21st Century Fox America, Inc. (04/07/2022) 245 Pilot Services Company, Inc. (01/14/2022) 258131 Aviation LLC (09/18/2020) 4770RR, LLC (12/06/2023) 51 CL Corp. (06/23/2024) 51 LJ Corporation (02/01/2023) 650534 Alberta, Inc. d/b/a Latitude Air Ambulance (01/09/2024) 711 CODY, Inc. (02/09/2025) A A&M Global Solutions, Inc. (09/03/2021) A.J. Walter Aviation, Inc. (01/17/2021) A.R. Aviation, Corp. (12/30/2022) Abbott Laboratories Inc. (08/26/2026) AbbVie US LLC (10/15/2026) Abelag Aviation NV d/b/a Luxaviation Belgium (02/27/2026) ABS Jets A.S. (05/07/2025) ACASS Canada Ltd. (02/27/2026) Accent Airways LLC (01/12/2022) Ace Flight Center Inc. -

Airline Contact Information

AIRLINE CONTACT INFORMATION AIR FRANCE Website: https://www.airfrance.us Phone: 1-800-237-2747 ALASKA AIR Website: https://www.alaskaair.com Phone: 1-800-252-7522 AMERICAN AIRLINES, INC. Website: http://www.aa.com Travel Alert Website: https://www.aa.com/i18n/travel-info/travel-alerts.jsp Phone: 800-433-7300 (ENG) / 800-633-3711 (SPA) AVIANCA Website: http://www.avianca.com/us/en Phone: Puerto Rico: (1 800) 284-2622 / Dominican Republic: (809) 200-8662 / Aruba: (00297) 588-0059 / Curacao: (5999) 844-2020 BRITISH AIRWAYS Website: https://www.britishairways.com Phone: 1 (800) 247-9297 CAPE AIR Website: http://www.capeair.com Travel Alert Website: https://www.capeair.com/scripts/alert.php?id=1370 Phone: 800-Cape-Air (227-3247) or 508-771-6944 CARIBBEAN AIRLINES LIMITED Website: https://www.caribbean-airlines.com/#/main Travel Alert Website: https://www.caribbean-airlines.com/#/caribbean-experience/media- releases/24 Email: [email protected] Phone: From US: + 1 800 744 2225, From Caribbean: + 1 800 744 2225 or +1 868 625 7200 CAYMAN AIRWAYS LIMITED Website: https://www.caymanairways.com Email: [email protected] Phone: 345-949-2311 / 1-800-422-9626 DELTA AIR LINES, INC. Website: https://www.delta.com Travel Alert Website: https://www.delta.com/content/www/en_US/traveling-with- us/advisories/hurricane-irma.html Phone: 1-888-750-3284 INSEL AIR Website: https://www.fly-inselair.com/en/ Travel Alert Website: https://www.fly-inselair.com/en/news/travel-alert-for-passengers- traveling-to-and-from-sint-maarten/ Email: [email protected] Phone: From US: + 1 855 493 6004 / From St. -

Informe Estadístico Sobre El Transporte Aéreo En República Dominicana 2017

Informe Estadístico sobre el Transporte Aéreo en República Dominicana 2017 Febrero 2018 Santo Domingo, R.D. Elaborado por: Carlos E. Santana C. Sabrina Pichardo Paola Massiel Mendoza C. Revisado por: Francisco E. Guerrero S. Jesenia Ortiz Himilce Tejada Francisco Figuereo Copyright 2018 Todos los derechos reservados Santo Domingo, Rep. Dom. CONTENIDO GLOSARIO DE TÉRMINOS ........................................................................................... I GLOSARIO DE SIGLAS ............................................................................................... III PALABRAS DEL PRESIDENTE DE LA JUNTA DE AVIACIÓN CIVIL .................. V RESUMEN EJECUTIVO .............................................................................................. VI MOVIMIENTO GENERAL DE PASAJEROS ............................................................... 1 Entrada y salida de pasajeros 2017 ............................................................................... 1 Flujo de pasajeros por tipo de vuelo 2017 .................................................................... 1 Crecimiento en el tráfico de pasajeros 2010 - 2017 ...................................................... 2 MOVIMIENTO DE PASAJEROS POR AEROPUERTOS DOMINICANOS. .............. 2 Tráfico de pasajeros por aeropuertos 2017 ................................................................... 2 Variación en el movimiento de pasajeros por aeropuertos 2010 - 2017 ....................... 3 Principales líneas aéreas por aeropuertos .................................................................... -

ALTA Press Release

ALTA’s Aviation Law Americas Conference Taking Place September 6 – 8, 2017 in Bogota, Colombia Registration now open at ALTA Aviation Law Americas Miami, Florida (April 25, 2017) – ALTA’s (Latin American and Caribbean Air Transport Association) 11th annual Aviation Law Americas Conference is taking place September 6 – 8, 2017 in Bogota, Colombia. ALTA’s Aviation Law Americas is the region's premier legal conference focused specifically on the aviation industry. Attended by top law firms, aviation industry experts and airlines from throughout the Americas, the two-day conference brings together legal decision makers for meetings in one location to focus on exchanging views, ideas, and best practices on legal, finance and aero-political issues and challenges that the industry is currently facing in the region. ALTA’s Legal and Aeropolitical Committee meeting together with the IATA-ALTA Aeropolitical Forum is also held at this conference to discuss emerging challenges and to coordinate actions before civil aviation authorities, governmental agencies, airport administrations, and international and multilateral organizations. “ALTA’s Aviation Law Americas provides the ideal venue for aviation legal and finance executives to meet in one place for face-to-face discussions on current and upcoming topics of key importance for the air transport industry,” said Gonzalo Yelpo, ALTA’s Chief Legal Counsel and Chair of the Aviation Law Americas Conference. Past conferences have focused on topics such as the economic outlook, aviation in a competitive environment, the environment, recent case studies in litigation and liability, passenger rights, aircraft financing, and more. For complete details and to register, visit Aviation Law Americas. -

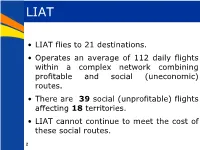

• LIAT Flies to 21 Destinations. • Operates an Average of 112 Daily Flights Within a Complex Network Combining Profitable and Social (Uneconomic) Routes

LIAT • LIAT flies to 21 destinations. • Operates an average of 112 daily flights within a complex network combining profitable and social (uneconomic) routes. • There are 39 social (unprofitable) flights affecting 18 territories. • LIAT cannot continue to meet the cost of these social routes. 2 Current Market LIAT Population Target Market Direct Market Social Media Destinations (Sept. 2012 Est.) (Age: 15 - 64) Reach Reach Anguilla 15,423 10,282 6,940 6,100 Antigua & Barbuda 89,018 59,191 70,968 29,020 Barbados 287,733 204,305 191,878 114,240 British Virgin Islands 31,148 18,805 14,620 9,720 Curacao 145,834 98,894 92,500 95,420 Dominica 73,126 48,737 32,151 22,800 Dominican Republic 10,088,598 6,617,959 4,120,801 2,233,360 Grenada 109,011 71,214 34,961 29,640 Guadeloupe 405,500 262,385 155,740 125,860 Guyana 741,908 352,220 190,000 NA Martinique 397,166 256,966 170,000 125,680 Puerto Rico 3,690,923 2,636,974 1,698,301 1,486,340 St. Kitts & Nevis 50,726 35,037 22,340 22,140 Saint Lucia 162,178 109,032 142,900 48,300 St. Maarten 39,088 27,312 St. Vincent & Grenadines 103,537 70,027 76,000 40,000 Trinidad 1,226,383 885,138 650,611 435,240 US Virgin Islands 105,275 71,490 30,000 8,340 TOTAL CARIBBEAN 17,762,575 11,835,968 7,700,711 4,832,200 3 Demand in the Region Purpose of Travel LIAT Customer Service Survey 2007: • In 2007 a Customer Service Survey was implemented. -

Airlines List in Outside

Partner Airline List (Ticketprinter outside BSP) 23 March, 2012 The following list provides an overview of Hahn Air Partner Airlines available in your market. Hahn Air offers 243 airlines for single and multi airline ticketing and 2 airlines for multi airline ticketing only (marked in orange colour). Please always use Quick Check on www.hahnair.com prior to ticketing. 1X Branson AirExpress CU Cubana de Aviacion LG Luxair SP SATA Air Acores 2I Star Perú CX CATHAY PACIFIC Airways LI Liat SS Corsairfly 2J Air Burkina CY Cyprus Airways LO LOT Polish Airlines SV Saudi Arabian Airlines 2K AeroGal Aerolineas Galapagos CZ China Southern Airlines LP Lan Peru SW Air Namibia 2L Helvetic Airways D2 Severstal Aircompany LR Lacsa SX SkyWork Airlines 2M Moldavian Airlines D6 Interair South Africa LW Pacific Wings Airlines SY Sun Country Airlines 2N Nextjet DC Golden Air LY EL AL Israel Airlines T4 TRIP Linhas Aéreas 2W Welcome Air DG South East Asian Airlines M7 Marsland Aviation TA TACA 3B Job Air - Central Connect DN Senegal Airlines M9 Motor Sich Airlines JSC TB Jetairfly.com 3E Air Choice One DV JSC Air Company Scat MD Air Madagascar TF Malmö Aviation 3L InterSky EI Aer Lingus ME Middle East Airlines TK Turkish Airlines 3P Tiara Air N.V. EK Emirates MF Xiamen Airlines TM LAM - Linhas Aereas 4J Somon Air ET Ethiopian Airlines MH Malaysia Airlines TN Air Tahiti Nui 4M Lan Argentina EY Etihad Airways MI SilkAir TU Tunis Air 4Q Safi Airways F7 Darwin Airline SA MK Air Mauritius U6 Ural Airlines 5C Nature Air F9 Frontier Airlines MU China Eastern Airlines