Evidence from Pakistan Banking Industry Syeda Um Ul

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

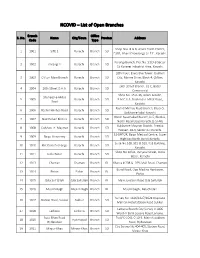

NCOVID – List of Open Branches

NCOVID – List of Open Branches Branch Office S. No. Name City/Town Province Address Code Type Shop Nos. 8 & 9, Anum Trade Center, 1 1001 SITE 1 Karachi Branch SD E31B, Ghani Chowrangi, S.I.T.E., Karachi. Korangi Branch, Plot No. 51/9-B Sector 2 1002 Korangi 1 Karachi Branch SD 15 Korangi Industrial Area, Karachi. 10th Floor, Executive Tower, Dolmen 3 1003 Clifton Main Branch Karachi Branch SD City, Marine Drive, Block-4, Clifton, Karachi. 26th Street Branch, 31-C, Badar 4 1004 26th Street D.H.A. Karachi Branch SD Commercial Shop No. 15 & 16, Adam Arcade, Shaheed-e-Millat 5 1005 Karachi Branch SD B.M.C.H.S. Shaheed-e-Millat Road, Road Karachi. Rashid Minhas Road Branch, Block-5, 6 1006 Rashid Minhas Road Karachi Branch SD Gulshan-e-Iqbal Karachi. North Nazimabad Branch, D-5, Block-L, 7 1007 Nazimabad Block L Karachi Branch SD North Nazimabad Karachi.(5 STAR) Gulshan-e-Maymar Branch, Areeba 8 1008 Gulshan -e- Maymar Karachi Branch SD Heaven, SB-3, Sector X-II Karachi. 51-DHTOR, Baqai Medical Centre, Super 9 1009 Baqai University Karachi Branch SD Highway,North Bond).Karachi. Suite No.518, 519 & 520, KSE Building, 10 1010 Khi Stock Exchange Karachi Branch SD Karachi. Shop No 10/44, Daryalal Street, Jodia 11 1011 Jodia Bazar Karachi Branch SD Bazar, Karachi 12 1013 Chaman Chaman Branch BL Khasra # 208 & 209, Mall Road, Chaman Bund Road, Opp Madina Hardware, 13 1014 Pishin Pishin Branch BL Pishin 14 1015 Qilla Saif Ullah Qila Saifullah Branch BL Main Junction Road Qila Saifullah 15 1016 Muslim Bagh Muslim Bagh Branch BL Muslimbagh , Baluchistan Survey No. -

Allied Bank Is the First Muslim Bank, to Have Been Established on the Territory That Became Pakistan

ALLIED BANK LIMITED MONEY AND BANKING Vision To become a dynamic and efficient bank providing integrated solutions in order to be the first choice bank for the customers. Mission • To provide value-added services to our customers • To provide high-tech innovative solutions to meet customers requirements • To create sustainable value through growth, efficiency and diversity for all stakeholders • To provide a challenging work environment and reward dedicated team members according to their abilities and performance • To play a proactive role in contributing towards the society 1 ALLIED BANK LIMITED MONEY AND BANKING BOARD OF DIRECTORS: Board of Directors (left to right) Mohammad Naeem Mukhtar (Chairman) Mohammad Waseem Mukhtar (Director) Sheikh Jalees Ahmed (Director) Sheikh Mukhtar Ahmed (Director) Abdul Aziz Khan (Director) Mubashir A. Akhtar (Director) Khalid A. Sherwani (Chief Executive Officer) Muhammad Raffat (Company Secretary) 2 ALLIED BANK LIMITED MONEY AND BANKING OVERVIEW OF ALLIED BANK LIMITED: Type Public as "Australasia Bank", 1942 Founded Lahore, Pakistan Headquarters Lahore, Pakistan Industry Finance and Insurance Products Financial Services Revenue Allied Bank is located in Lahore, Punjab, Pakistan. It was established in 1942 before independence, Allied Bank Limited is one of the largest banks in Pakistan with 735 Branches connected to an online network. In August 2004 the Bank was restructured and the ownership was transferred to Ibrahim Group. A Map of Pakistan showing the location of Allied Bank branches in Pakistan 3 ALLIED BANK LIMITED MONEY AND BANKING HISTORY OF ALLIED BANK LIMITED: Allied Bank is the first Muslim bank, to have been established on the territory that became Pakistan. Established in December 1942 as the Australasia Bank at Lahore with a paid-up share capital of Rs. -

ANNUAL REPORT 2019 Annual Report 2019

ANNUAL REPORT 2019 Annual Report 2019 HabibMetro 1 Modaraba Management First Habib Modaraba ( A n I s l a m i c F i n a n c i a l I n s t i t u t i o n ) 2 HabibMetro Modaraba Management Annual Report 2019 A Progressive Partnership Based on True Sharing and Equality At FHM we believe that to be successful in the long term we must continually reassess our competencies, business strategies and risk management approaches in order to cope up with day to day business challenges. The Relationships that exceed beyond normal business this is how we have acquired the standing we possess today as most progressive Modaraba holding the loyalty and trust of all stakeholders across the country. Our achievements are evidence to the solid business fundamentals and consistent financial management policies practiced across the Modaraba. Our focused business strategy keeps us firmly on path of sustainable growth and profitability. Islamic finance is a financial system operates in accordance with Islamic principle of finance. This system encourages economic activities and proper distribution of wealth which ultimately lead to promote social justice which is the key theory of Islamic economic financial system. Consistency in distribution of dividends among the certificate holders along with increase in certificate holders' equity has made FHM a sound and well performing Modaraba within the sector. By the grace of Allah (SWT), FHM has been maintaining its history of continuous payment of profits to its Certificate Holders and never skipped the same in any single year. Modaraba concept is based on Shirkat. -

Prospectus, Especially the Risk Factors Given at Para 4.11 of This Prospectus Before Making Any Investment Decision

ADVICE FOR INVESTORS INVESTORS ARE STRONGLY ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS PROSPECTUS, ESPECIALLY THE RISK FACTORS GIVEN AT PARA 4.11 OF THIS PROSPECTUS BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FALSE AND FICTITIOUS APPLICATIONS ARE PROHIBITED AND SUCH APPLICATIONS’ MONEY MAY BE FORFEITED UNDER SECTION 87(8) OF THE SECURITIES ACT, 2015. SONERI BANK LIMITED PROSPECTUS THE ISSUE SIZE OF FULLY PAID UP, RATED, LISTED, PERPETUAL, UNSECURED, SUBORDINATED, NON-CUMULATIVE AND CONTINGENT CONVERTIBLE DEBT INSTRUMENTS IN THE NATURE OF TERM FINANCE CERTIFICATES (“TFCS”) IS PKR 4,000 MILLION, OUT OF WHICH TFCS OF PKR 3,600 MILLION (90% OF ISSUE SIZE) ARE ISSUED TO THE PRE-IPO INVESTORS AND PKR 400 MILLION (10% OF ISSUE SIZE) ARE BEING OFFERED TO THE GENERAL PUBLIC BY WAY OF INITIAL PUBLIC OFFER THROUGH THIS PROSPECTUS RATE OF RETURN: PERPETUAL INSTRUMENT @ 6 MONTH KIBOR* (ASK SIDE) PLUS 2.00% P.A INSTRUMENT RATING: A (SINGLE A) BY THE PAKISTAN CREDIT RATING COMPANY LIMITED LONG TERM ENTITY RATING: “AA-” (DOUBLE A MINUS) SHORT TERM ENTITY RATING: “A1+” (A ONE PLUS) BY THE PAKISTAN CREDIT RATING AGENCY LIMITED AS PER PSX’S LISTING OF COMPANIES AND SECURITIES REGULATIONS, THE DRAFT PROSPECTUS WAS PLACED ON PSX’S WEBSITE, FOR SEEKING PUBLIC COMMENTS, FOR SEVEN (7) WORKING DAYS STARTING FROM OCTOBER 18, 2018 TO OCTOBER 26, 2018. NO COMMENTS HAVE BEEN RECEIVED ON THE DRAFT PROSPECTUS. DATE OF PUBLIC SUBSCRIPTION: FROM DECEMBER 5, 2018 TO DECEMBER 6, 2018 (FROM: 9:00 AM TO 5:00 PM) (BOTH DAYS INCLUSIVE) CONSULTANT TO THE ISSUE BANKERS TO THE ISSUE (RETAIL PORTION) Allied Bank Limited Askari Bank Limited Bank Alfalah Limited** Bank Al Habib Limited Faysal Bank Limited Habib Metropolitan Bank Limited JS Bank Limited MCB Bank Limited Silk Bank Limited Soneri Bank Limited United Bank Limited** **In order to facilitate investors, United Bank Limited (“UBL”) and Bank Alfalah Limited (“BAFL”) are providing the facility of electronic submission of application (e‐IPO) to their account holders. -

COMPARATIVE ANALYSIS of FINANCIAL PERFORMANCE and GROWTH of CONVENTIONAL and ISLAMIC BANKS of PAKISTAN Ishtiaq Khan, Sarhad University of Science & IT, Peshawar

COMPARATIVE ANALYSIS OF FINANCIAL PERFORMANCE AND GROWTH OF CONVENTIONAL AND ISLAMIC BANKS OF PAKISTAN Ishtiaq Khan, Sarhad University of Science & IT, Peshawar. Email: [email protected] Wali Rahman, Associate Professor, Sarhad University of Science & IT, Peshawar. Email: [email protected] Saeedullah Jan, Khushal Khan Khattak University, Karak. Email: [email protected] Mustaq Khan, Abasyn University of Science & IT, Peshawar Email: [email protected] Abstract. Various types of the banking system are operating in the world. The most commons are conventional and Islamic. Customers evaluate these systems before they decide in invest. The prime aim of this study is to assess and compare the financial performance and growth of conventional and Islamic banks operating in Pakistan. Banks offer different types of products and services for the satisfaction of customers for their financial needs. Conventional banking is based on interest while Islamic banking offers interest-free banking. To compare their respective performance financial ratios are applied. In Pakistan, Habib Bank Limited and Allied Bank Limited are typical examples of the conventional banking whereas Dubai Islamic Bank Limited and Meezan Bank Limited are operating as Islamic banking. Three (03) years data were obtained from the “Financial Statement Analysis of Financial Sector of Pakistan 2009-2011” State Bank of Pakistan publication. The analyses reflect that the liquidity ratio of Islamic banks appeared higher as compared to conventional banks, whereas the profitability and solvency ratios of conventional banks were comparatively higher than Islamic banks. Debt to asset ratio of Islamic banks seemed better than conventional banks due to low debt financing. Also, with regard to expansion, the growth rate of Islamic banks in Pakistan is comparatively higher than conventional banks. -

Snapshot of Results of Banks in Pakistan Snapshot of Results of Banks in Pakistan Six Months Period Ended 30 June 2016

KPMG Taseer Hadi & Co. Chartered Accountants Snapshot of results of Banks in Pakistan Snapshot of results of banks in Pakistan Six months period ended 30 June 2016 This snapshot has been prepared by KPMG Taseer Hadi & Co. and summarizes the performance of selected banks in Pakistan for the 6 months period ended 30 June 2016. The information contained in this snapshot has been obtained from the published consolidated financial statements of the banks and where consolidated financial statements were not available, standalone financials have been used. Reference should be made to the published financial statements of the banks to enhance the understanding of ratios and analysis of performance of a particular bank. We have tried to provide relevant financial analysis of the banks which we thought would be useful for benchmarking and comparison. However, we welcome any comments, which would facilitate in improving the contents of this document. The comments may be sent on [email protected] Dated: 23 September 2016 Karachi © 2016 KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistan and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2 Document Classification: KPMG Public HBL NBP UBL MCB ABL BAF 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 Ranking By total assets 1 1 2 2 3 3 4 4 5 5 6 6 By net assets 1 1 2 2 3 3 4 4 5 5 7 7 By profit before tax 1 1 4 4 2 3 3 2 5 5 7 8 Profit before tax * 28,298 -

IBFT Guideline

MCB Bank Limited IBFT- Guidelines 1. Al Baraka Bank (Pakistan) Limited Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Format Example: AAAAAAAAAAAAA Note: A = Account Number 2. Allied Bank Limited Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA Note: B = Branch Code, A = Account Number 3. APNA Microfinance Bank Please enter APNA Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA Note: B = Branch Code, A = Account Number 4. Askari Bank Limited Please enter Askari Bank Account Number by following the layout below: For Branch Banking: Total Digits of Bank Account Number: 14 Digits Format Example: BBBBAAAAAAAAAA Note: B = Branch Code, A = Account Number For Branchless Banking: Total Digits of Bank Account Number: 11 Digits Format Example: 03XXXXXXXXX 5. Bank Al-Habib Limited Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digits Format Example: BBBBTTTTBBBBBBRRC Note: B = Branch Code, A = Account Number, T = Account Type, BBBB= Base Number, RR = Digit Running Number, C = Check Digit 111 000 622 mcb.com.pk /MCBBankPk Over 1350 Branches & ATMs 6. Bank Al-Falah Limited Please enter Bank Al-Falah Account Number by following the layout below: For Conventional Banking: Total Digits of Account Number: 14 Digits Format Example: BBBBAAAAAAAAAA Note: B = Branch Code, A = Account Number For Islamic Banking: Total Digits of Account Number: 18 Digits Format Example: BBBBAAAAAAAAAAAAAA Note: B = Branch Code, A = Account Number For Branchless Banking: Total Digits of Account Number: 11 Digits Format Example: 03XXXXXXXXX 7. -

Downloading the Said Form Is Wp-Content/Uploads/2014/10/ABL-Request-Letter.Pdf

CONTENTS 02 Vision Unconsolidated Financial Statements 02 Mission 02 Core Values of Allied Bank Limited 63 Auditors’ Report to the Members 03 Company Information 64 Statement of Financial Position 03 Board of Directors 65 Profit and Loss Account 04 Profile of the Directors 66 Statement of Other Comprehensive 06 Board Committees Income 08 Chairman’s Message 67 Statement of Cash Flow 10 Directors’ Report 68 Statement of Changes in Equity 15 Calendar of Major Events 70 Notes to the Financial Statements 16 Corporate Structure 144 Annexure I 17 Management & Committees 147 Annexure II 18 Chief Executive Officer’s Review 148 Annexure III 26 Group’s Review 152 Annexure IV 34 Performance Highlights 38 Horizontal Analysis 40 Vertical Analysis Consolidated Financial Statements 42 Statement of Value Addition of Allied Bank Limited and its 43 Cash Flow - Direct Method Subsidiary 44 Concentration & Maturity Profile 158 Directors’ Report on Consolidated 45 Quarterly Comparison of Financial Results Financial Statements 46 Product & Services 159 Auditors’ Report to the Members 48 Corporate Sustainability 160 Statement of Financial Position 51 Notice of 68th Annual General Meeting 161 Profit and Loss Account 53 Statement of Compliance with Code of 162 Statement of Other Comprehensive Corporate Governance (CCG) Income 55 Auditors’ Review Report to the Members on 163 Statement of Cash Flow Statement of Compliance with CCG 164 Statement of Changes in Equity 56 Statement of Ethics and Business Practices 166 Notes to the Financial Statements 58 Statement of Internal Controls 239 Annexure I 59 Whistle Blowing Policy 240 Pattern of Shareholding 247 Glossary of Financial & Banking Terms 251 Form of Proxy Annual Report of Allied Bank Limited for the year 2014 PERFORMANCE 2014 DEPOSITS UP BY10% Rs. -

Bankislami Half Yearly Report June 2018

HALF YEARLY REPORT JUNE 02 Corporate Information 04 Directors’ Report 08 Auditors‘ Report 09 Statement of Financial Position 10 Profit and Loss Account 11 Statement of Comprehensive Income 12 Cash Flow Statement 13 Statement of Changes in Equity 14 Notes to and forming part of the financial statements 34 Consolidated Directors’ Report 36 Consolidated Financial Statements Halfyearly Report 2018 Corporate Information Board of Directors Legal Adviser Mr. Ali Hussain Chairman 1- Haidermota & Co. Mr. Fawad Anwar Vice Chairman Barrister at Law Mr. Ali Mohamad Hussain Ali Mohamad Alshamali Dr. Amjad Waheed 2- Mohsin Tayebaly & Co. Mr. Hasan A.Bilgrami Chief Executive Officer Corporate Legal Consultants / Barristers & Advocates Mr. Muhammad Nadeem Farooq High Courts & Supreme Court Mr. Noman Yakoob Mr. Siraj Ahmed Dadabhoy Management (in alphabetical order) Ahmad Mobeen Malik Head, Distribution - North Sharia'h Supervisory Board Bilal Zuberi Head, Distribution - South Mufti Irshad Ahmad Aijaz Chairman Fakhir Ahmad Head, Human Resources Mufti Muhammad Husain Member Farooq Anwar Head, Operations Mufti Javed Ahmed Member Hasan A. Bilgrami Chief Executive Officer Kashif Nisar Head, Shariah Advisory & Structuring Audit Committee Khawaja Ehrar ul Hassan Company Secretary & Head of Legal Dr. Amjad Waheed Chairman Mahmood Rashid Head, Government Relations & Security Mr. Noman Yakoob Member Masood Muhammad Khan Head, Compliance Mr. Ali Mohamad Hussain Ali Mohamad Alshamali Member Muhammad Asadullah Chaudhry Head, Service Quality & Phone Banking Saad Ahmed Madani Head, Corporate Banking Risk Management Committee Sadaruddin Pyar Ali Head, Administration & General Services Mr. Fawad Anwar Chairman Sohail Sikandar Chief Financial Officer Mr. Siraj Ahmed Dadabhoy Member Syed Abdul Razzaq Head, Risk Management Mr. Hasan A. -

Bank Islami 2011

04 06 12 14 20 21 23 24 27 29 30 31 32 33 34 76 135 137 138 142 Corporate Information Board of Directors Chief Justice (Retd.) Mahboob Ahmed Chairman Mr. Ahmed Goolam Mahomed Randeree Mr. Ali Raza Siddiqui Mr. Ali Hussain Mr. Hasan A. Bilgrami Chief Executive Officer Mr. Hicham Hammoud Mr. Shabir Ahmed Randeree Sharia'h Supervisory Board Mr. Justice (Retd.) Muhammad Taqi Usmani Chairman Professor Dr. Fazlur Rahman Member Mufti Irshad Ahmad Aijaz Member & Sharia'h Adviser Audit Committee Mr. Hicham Hammoud Chairman Mr. Ali Raza Siddiqui Member Mr. Shabir Ahmed Randeree Member Executive Committee Chief Justice (Retd.) Mahboob Ahmed Chairman Mr. Ahmed Goolam Mahomed Randeree Member Mr. Hasan A. Bilgrami Member Mr. Hicham Hammoud Member Risk Management Committee Mr. Ahmed Goolam Mahomed Randeree Chairman Mr. Hasan A Bilgrami Member Human Resource & Compensation Committee Mr. Ali Raza Siddiqui Chairman Mr. Ahmed Goolam Mahomed Randeree Member Mr. Hicham Hammoud Member Mr. Hasan A. Bilgrami Member Company Secretary Syed Shah Sajid Hussain Auditors A. F. Ferguson & Co. Chartered Accountants Legal Adviser Haidermota & Co. Barrister at Law 04 Management (in alphabetical order) Mr. Ahmed Mustafa Head, Branch Operations Mr. Arsalan Vohra Head, Risk Policy & Analytics Mr. Arshad Wahab Zuberi Head, Administration and General Service Mr. Asad Alim Head, Information Systems Mr. Farooq Anwar Head, Operations Mr. Hasan A. Bilgrami Chief Executive Officer Mr. Khawaja Ehrar ul Hassan Head, Compliance and Legal Mr. Muhammad Faisal Shaikh Head, Product Development Mr. Muhammad Furqan Head, Credit Administration Mr. Muhammad Imran Head, Consumer & Retail Banking Mr. Muhammad Shoaib Khan Head, Treasury & Financial Institutions Mr. -

IFMP Quarterly

QUARTERLY JUNE 2021 ARTICLE ON MESSAGE FROM THE CEO THE FUTURE OF BANCAS- SURANCE SECTOR IN INTRODUCTION TO THE INSTITUTE PAKISTAN IFMP ACTIVITIES INDUSTRY PROFESSIONALS’ INTERVIEW ARTICLE TERMS OF THE MONTH BUSINESS AND ECONOMIC NEWSFLASH URDU GLOSSARYTERMS OF THE MONTH FEEDBACKS BUSINESS AND ECONOMIC NEWSFLASH MARKETS IN REVIEW URDU GLOSSARY Your Gateway to Careers in Financial Markets QUOTES AND JOKES Institute of FinancialMARKETS Markets IN REVIEW of Pakistan Address: Building 9-A, 2nd Floor, P.E.C.H.S Block No. 6, Shahrah-e-Faisal Karachi. Tel: +92 (21) 34540843-44 00 CONTENT Message from the CEO Page: 1 Introduction to the Institute Page: 2 IFMP Activities Page: 3 Industry Professionals’ Interview Page: 4 Featured Article Page: 6 Article from IFMP Member Page: 18 Terms of the Quarter Page: 22 Business and Economic Newsflash (Local) Page: 23 Business and Economic Newsflash (International) Page: 34 Regulatory Updates Page: 47 Urdu Glossary Page: 52 Investment Quotes Page: 53 Feedbacks Page: 54 Markets in Review Page: 55 www.ifmp.org.pk 92 (21) 34540843-44 [email protected] Message from the Chief Executive Officer 01 he last few years have seen a rapid growth in size, quality and sophistication of finan- T cial markets, because of changes in the policy and regulatory environment, the entre- preneurial initiatives of individuals and institutions, and the availability of trained man- power. The continuing growth of financial markets is further adding to the demand for well-trained professionals. Institute of Financial Markets of Pakistan is dedicated to the professional development of financial markets and research on financial markets as well as the well being of financial markets by educating the professionals about the norms and ethics being practiced in the markets. -

Annual Audited Financial Statements 2013-14

Jubilee Spinning & Weaving Mills Ltd. Annual Report 2014 Annual Report 2014 Contents 1. Company information .......................................3 2. Notice of Annual General Meeting .......................................4 3. Director's Report to the Shareholders ..........................................5 4. Key Operating & Financial Ratios..............................................................................................8 5. Vision Statement & Mission Statement .........................................09 6. Statement of compliance with the Code of Corporate Governance ......................................10 7. Review Report of the Members on Statement of Compliance with the best practices of Code of Corporate Governance ...................................................................................12 8. Auditors Report to the Members ..........................................13 9. Balance Sheet ............................................14 10. Profit & Loss Account ..........................................16 11. Statement of Comprehensive Income .......................................................................................17 12. Cash Flow Statement ...........................................18 13. Statement of Changes in Equity ......................................19 14. Notes to the Accounts ............................................20 15. Pattern of Shareholding ............................................55 16. Form of Proxy .................................enclosed 1 Annual Report 2014 Company Information