Southeast Bend Market Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retailers' Produce and Vegetable Supply Management

Retailers’ Produce and Vegetable Supply Management: A Teaching Case Kurt Christensen Phone: 541-760-6172 [email protected] Zhaohui Wu Phone: 541-737-3514 [email protected] College of Business Oregon State University Corvallis, Oregon 97331 0 Abstract This teaching case compares and contrasts store operations and supply management of produce and vegetable of two very different grocery retailers. It illustrates the purchasing processes, supplier relationship management and merchandise strategies of each store. The objective of this case is to help students understand the competition and current development of produce and vegetable sector and challenge and opportunities in managing perishable food products. Class discussion questions are provided in the end of the case and teaching notes will be provided upon request. Key word: good supply chain, supply management, produce and vegetables, teaching case Background Produce and vegetable retailers face challenges in produce and vegetable purchasing every day. The products they sell are perishable mandating rapid inventory turns. Many items require special handling, storage and frequent inspections to reassess quality and safety. Many customers now expect and demand more choices such as natural and organic produce and vegetable products. In addition, traditional retailers face increasing competition from niche natural food stores such as Whole Foods, local co-ops, Farmer’s Markets and Community Supported Agriculture (CSA) to innovate and meet the demands of changing demographics. The growing demand for social and environmental sustainability creates both opportunities and challenges for retailers. This trend mandates changes in how they manage logistics/inventory, supply relationship, product branding, store management and pricing decisions. -

News Release Fred Meyer and QFC Associates Ratify Agreements with UFCW Local 555

News Release Fred Meyer and QFC Associates Ratify Agreements with UFCW Local 555 PORTLAND, Ore., Feb. 21, 2013 /PRNewswire/ -- The Kroger Co. (NYSE: KR) associates working at Fred Meyer and QFC stores in Portland and throughoutOregon and Southwest Washington have ratified new labor agreements with UFCW Local 555. "We are pleased to reach agreements that are good for our associates and enable us to be competitive in very competitive market areas," said Lynn Gust, Fred Meyer's president. "These agreements provide our associates with additional compensation, affordable health care and pension for retirement." "Our associates will continue to have one of the best total compensation packages in our industry, in our region," said Joe Fey, QFC's president. "I want to thank our associates for their patience, for supporting this agreement, and for the excellent service they provide every day to our customers." The 44 labor agreements cover 6,007 associates working at Fred Meyer and 368 associates at QFC. About Kroger Kroger, one of the world's largest retailers, employs more than 339,000 associates who serve customers in 2,425 supermarkets and multi-department stores in 31 states under two dozen local banner names including Kroger, City Market, Dillons, Jay C, Food 4 Less, Fred Meyer, Fry's, King Soopers, QFC, Ralphs and Smith's. The company also operates 788 convenience stores, 342 fine jewelry stores, 1,124 supermarket fuel centers and 37 food processing plants in the U.S. Recognized by Forbes as the most generous company in America, Kroger supports hunger relief, breast cancer awareness, the military and their families, and more than 30,000 schools and grassroots organizations in the communities it serves. -

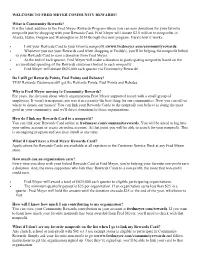

Fred Meyer Community Rewards!

WELCOME TO FRED MEYER COMMUNITY REWARDS! What is Community Rewards? It is the latest addition to the Fred Meyer Rewards Program where you can earn donations for your favorite nonprofit just by shopping with your Rewards Card. Fred Meyer will donate $2.5 million to nonprofits in Alaska, Idaho, Oregon and Washington in 2014 through this new program. Here's how it works: • Link your Rewards Card to your favorite nonprofit atwww.fredmeyer.com/communityrewards. • Whenever you use your Rewards card when shopping at Freddy's, you’ll be helping the nonprofit linked to your Rewards Card to earn a donation from Fred Meyer. • At the end of each quarter, Fred Meyer will make a donation to participating nonprofits based on the accumulated spending of the Rewards customers linked to each nonprofit. • Fred Meyer will donate $625,000 each quarter via Community Rewards! Do I still get Rewards Points, Fuel Points and Rebates? YES! Rewards Customers still get the Rewards Points, Fuel Points and Rebates. Why is Fred Meyer moving to Community Rewards? For years, the decision about which organizations Fred Meyer supported rested with a small group of employees. It wasn't transparent, nor was it necessarily the best thing for our communities. Now you can tell us where to donate our money! You can link your Rewards Cards to the nonprofit you believe is doing the most good in your community, and we'll direct donations to those organizations. How do I link my Rewards Card to a nonprofit? You can link your Rewards Card online at fredmeyer.com/communityrewards. -

Operating Divisions MAJOR MARKETS

Operating Divisions Kroger’s operating structure is a balance between our corporate office in Cincinnati, Ohio, and our 21 supermarket operating divisions. This balance keeps merchandising decisions closest to the Customer while achieving synergies in back office operations in order to maximize operating efficiencies and minimize operating costs. In areas that directly affect the Customer, Kroger’s decentralized structure places substantial authority for merchandising and operating decisions in our supermarket divisions. Divisional managers are able to respond quickly to changes in competition and Customer preferences within each local market. For administrative processes that offer economies of scale or are invisible to the Customer (such as procurement, accounting, treasury, operations, etc.), Kroger® leverages its size and centralizes those functions to create value for Customers and better returns for shareholders. Kroger’s 21 supermarket operating divisions are: Division Headquarters # Stores Harris Teeter Charlotte, NC 234 Kroger Southwest* Houston, TX 217 Ralphs Los Angeles, CA 204 Kroger Atlanta Atlanta, GA 186 Roundy’s Milwaukee, WI 151 King Soopers/City Market Denver, CO 148 Smith’s Salt Lake City, UT 138 Kroger Central Indianapolis, IN 136 Fred Meyer Stores Portland, OR 132 Food 4 Less Los Angeles, CA 131 Kroger Michigan Novi, MI 127 Kroger Columbus Columbus, OH 122 Kroger Mid-Atlantic Roanoke, VA 120 Fry’s Food & Drug Phoenix, AZ 119 Kroger Cincinnati Cincinnati, OH 109 Kroger Delta Memphis, TN 104 Kroger Louisville Louisville, KY 97 Kroger Nashville Nashville, TN 92 Dillons Food Stores Hutchinson, KS 81 Jay C/Ruler Seymour, IN 65 Quality Food Centers (QFC) Seattle, WA 65 TOTAL 2,778 *Beginning in 2016, the Southwest Division separated into two separate divisions (Dallas and Houston). -

News Release Kroger Names Lynn Gust President of Fred Meyer Stores

News Release Kroger Names Lynn Gust President of Fred Meyer Stores CINCINNATI, Dec. 14, 2012 /PRNewswire/ -- The Kroger Co. (NYSE: KR) announced today the promotion of Lynn Gust as president of the company's Fred Meyer Stores division. Fred Meyer Stores, based in Portland, Ore., offers one-stop shopping at 133 multi-department stores Alaska, Idaho, Oregon andWashington. Mr. Gust, 59, has been senior vice president of operations since 2011. He started his career with Fred Meyer as a parcel clerk in 1970. Throughout his more than 40 years at the company he has served in a variety of leadership roles, including vice president of the Food Group and senior vice president of the Store Operations Group. In 2006, Mr. Gust was named executive vice president of Corporate Merchandising and Advertising. "Lynn's long history with Fred Meyer and deep knowledge of our business will serve our customers well," said Rodney McMullen, president and chief operating officer of Kroger. "His passion for our employees and customers make him a great fit to carry on the Fred Meyer tradition." Gust was born and raised in Vancouver, Wash. He is a member of the Portland State University Food Industry Leadership Center Advisory Board; on the board of directors of the Western Association of Food Chains; and on the board of directors of the Northwest Grocery Association. He is also a past chair of the Board of Directors of Randall Children's Hospital at Legacy Emanuel Hospital in Portland. He and his wife live in Portland and have four children. Kroger, one of the world's largest retailers, employs more than 339,000 associates who serve customers in 2,422 supermarkets and multi-department stores in 31 states under two dozen local banner names including Kroger, City Market, Dillons, Jay C, Food 4 Less, Fred Meyer, Fry's, King Soopers, QFC, Ralphs and Smith's. -

2016-2017 Annual Report with Results Reporting

FOOD FOR LANE COUNTY ANNUAL REPORT 2016-2017 INDIVIDUAL DONORS Our MissiOn Founding Trustees Hunger in Lane County To alleviate hunger by creating access to food Scott and Kathy Kitchel John and Chrissy Murphy Our viSiOn Marion Sweeney, Kate Laue and Cama Evans More Than One in Three Lane County Residents Experience Food Insecurity To eliminate hunger in Lane County Rick Wright, Market of Choice Plantinum Circle ($10,000+) Anonymous (6) Food insecurity is a lack of access, at times, to Why do people experience food insecurity? Beverly Avidan FOOD FOr Lane COunty PrOGraMS Philip and Florence Barnhart Mark and Mary Ann Beauchamp enough food for an healthy lifestyle. Too often • Fixed income • Minimal or no benefits Cereal FOR YOUTH Meals ON WHeels Glenn and Renee Buchanan this means a difficult trade-off between important Provides nutritious, organic cereal to Friendly volunteers deliver a freshly Dee Carlson and Mike Balm • Underemployment • Chronic illness children and teens prepared, nutritiously balanced, meal to seniors living in Eugene with time for a brief basic needs such as medical care, housing, or • Lack of affordable housing • Student loan debt CHIldreN’S WEEKEND SNACK PACK visit and safety check Distributes snack kits for elementary school- • Cost of childcare • Medical bills transportation, and nutritiously adequate foods. aged children to take home on weekends MUltICUltUral OUTREACH and vacations Employs a Multicultural Outreach Coordinator to work with community EXTRA HelpING partners cultivating dignity, respect and Provides -

Levi V. the Kroger Company Et

Case: 1:21-cv-00042-TSB Doc #: 1 Filed: 01/19/21 Page: 1 of 14 PAGEID #: 1 IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF OHIO CHRISTOPHER LEVI, individually and on CIVIL ACTION behalf of all others similarly situated, Plaintiff, Case No. v. THE KROGER COMPANY; and FRED MEYER STORES, INC. d/b/a FRED JURY TRIAL DEMANDED MEYER, Defendants. COLLECTIVE ACTION COMPLAINT Plaintiff, Christopher Levi (“Levi” or “Plaintiff”), files this Collective Action Complaint against Defendants, The Kroger Company (“Kroger”) and Fred Meyer Stores, Inc. d/b/a Fred Meyer (“Fred Meyer”) (collectively, “Defendants”), seeking all available relief under the Fair Labor Standards Act, 29 U.S.C. § 201 et seq. (“FLSA”), on behalf of himself and all current and former Assistant Store Managers (“ASMs”), however variously titled, who work (or worked) at any “Fred Meyer” store in the United States during the relevant time period. The following allegations are based on personal knowledge as to Plaintiff’s own conduct and are made on information and belief as to the acts of others. NATURE OF THE ACTION 1. Plaintiff brings this action on behalf of himself and similarly situated current and former ASMs to recover unpaid overtime pursuant to the FLSA. Defendants violated the FLSA by failing to pay their ASMs, including Plaintiff, overtime compensation for the hours they Case: 1:21-cv-00042-TSB Doc #: 1 Filed: 01/19/21 Page: 2 of 14 PAGEID #: 2 worked over forty (40) in one or more workweeks because Defendants classify them as exempt from overtime. 2. Defendants employ ASMs in over 130 Fred Meyer stores in Alaska, Idaho, Oregon, and Washington. -

Market Analysis for Grocery Retail Space in Forest Grove, Oregon

MARKET ANALYSIS FOR GROCERY RETAIL SPACE IN FOREST GROVE, OREGON PREPARED FOR THE CITY OF FOREST GROVE, FEBRUARY 2018 TABLE OF CONTENTS I. INTRODUCTION ............................................................................................................................................. 2 II. EXECUTIVE SUMMARY .................................................................................................................................. 2 III. TRADE AREA DEFINITION .............................................................................................................................. 4 IV. GROCERY MARKET OVERVIEW ...................................................................................................................... 5 THE PORTLAND METRO MARKET .............................................................................................................................. 5 METRO LOCATION PATTERNS ................................................................................................................................... 8 FOREST GROVE-CORNELIUS ................................................................................................................................... 15 V. SOCIO-ECONOMIC CONDITIONS .................................................................................................................. 19 POPULATION & HOUSEHOLDS ................................................................................................................................ 19 EMPLOYMENT & COMMUTING .............................................................................................................................. -

Feature Advertising by U.S. Supermarkets Meat and Poultry

United States Department of Agriculture Agricultural Feature Advertising by U.S. Supermarkets Marketing Service Meat and Poultry Livestock, Poultry and Seed Program Independence Day 2017 Agricultural Analytics Division Advertised Prices effective through July 04, 2017 Feature Advertising by U.S. Supermarkets During Key Seasonal Marketing Events This report provides a detailed breakdown of supermarket featuring of popular meat and poultry products for the Independence Day marketing period. The Independence Day weekend marks the high watershed of the summer outdoor cooking season and is a significant demand period for a variety of meat cuts for outdoor grilling and entertaining. Advertised sale prices are shown by region, state, and supermarket banner and include brand names, prices, and any special conditions. Contents: Chicken - Regular and value packs of boneless/skinless (b/s) breasts; b/s thighs; split, bone-in breasts; wings; bone-in thighs and drumsticks; tray and bagged leg quarters; IQF breast and tenders; 8-piece fried chicken. Northeast .................................................................................................................................................................. 03 Southeast ................................................................................................................................................................. 21 Midwest ................................................................................................................................................................... -

A COMPARISON of MODELS MEASURING the SPATIAL ACCESSIBILITY of SUPERMARKETS in PORTLAND, OREGON by ANDREA

MEASURING FOOD DESERTS: A COMPARISON OF MODELS MEASURING THE SPATIAL ACCESSIBILITY OF SUPERMARKETS IN PORTLAND, OREGON by ANDREA LEIGH SPARKS A THESIS Presented to the Department of Planning, Public Policy and Management and the Graduate School of the University of Oregon in partial fulfillment of the requirements for the degree of Master of Community and Regional Planning June 2008 ii "Measuring Food Deserts: A Comparison ofModels Measuring the Spatial Accessibility of Supermarkets in Portland, Oregon," a thesis prepared by Andrea Leigh Sparks in partial fulfillment of the requirements for the Master of Community and Regional Planning degree in the Department of Planning, Public Policy and Management. This thesis has been approved and accepted by: Dr. Neil Bania, Chair of the Examining Committee .:r \J.....Je. 3 2. 00 g' Date Committee in Charge: Dr. Neil Bania, Chair Dr. Laura Leete Dr. Marc Schlossberg Accepted by: Dean of the Graduate School . iii © 2008 Andrea Leigh Sparks IV An Abstract ofthe Thesis of Andrea Leigh Sparks for the degree of Master ofCommunity and Regional Planning in the Department ofPlanning, Public Policy and Management to be taken June 2008 Title: MEASURING FOOD DESERTS: A COMPARISON OF MODELS MEASURING THE SPATIAL ACCESSIBILITY OF SUPERMARKETS IN PORTLAND, OREGON "I - , i) Approve,d: _~~~--,-i _ Dr. Neil Bania Food deserts are low-income, urban areas that have poor spatial access to supermarkets. To date, researchers have developed theories about the food desert phenomenon's public health and fiscal implications in the form of diet-related health problems and its impact on the efficiency ofgovernment transfer payments, like food stamps. -

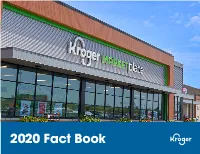

2020 Fact Book Kroger at a Glance KROGER FACT BOOK 2020 2 Pick up and Delivery Available to 97% of Custom- Ers

2020 Fact Book Kroger At A Glance KROGER FACT BOOK 2020 2 Pick up and Delivery available to 97% of Custom- ers PICK UP AND DELIVERY 2,255 AVAILABLE TO PHARMACIES $132.5B AND ALMOST TOTAL 2020 SALES 271 MILLION 98% PRESCRIPTIONS FILLED HOUSEHOLDS 31 OF NEARLY WE COVER 45 500,000 640 ASSOCIATES MILLION DISTRIBUTION COMPANY-WIDE CENTERS MEALS 34 DONATED THROUGH 100 FEEDING AMERICA FOOD FOOD BANK PARTNERS PRODUCTION PLANTS ARE 35 STATES ACHIEVED 2,223 ZERO WASTE & THE DISTRICT PICK UP 81% 1,596 LOCATIONS WASTE OF COLUMBIA SUPERMARKET DIVERSION FUEL CENTERS FROM LANDFILLS COMPANY WIDE 90 MILLION POUNDS OF FOOD 2,742 RESCUED SUPERMARKETS & 2.3 MULTI-DEPARTMENT STORES BILLION kWh ONE OF AMERICA’S 9MCUSTOMERS $213M AVOIDED SINCE MOST RESPONSIBLE TO END HUNGER 2000 DAILY IN OUR COMMUNITIES COMPANIES OF 2021 AS RECOGNIZED BY NEWSWEEK KROGER FACT BOOK 2020 Table of Contents About 1 Overview 2 Letter to Shareholders 4 Restock Kroger and Our Priorities 10 Redefine Customer Expereince 11 Partner for Customer Value 26 Develop Talent 34 Live Our Purpose 39 Create Shareholder Value 42 Appendix 51 KROGER FACT BOOK 2020 ABOUT THE KROGER FACT BOOK This Fact Book provides certain financial and adjusted free cash flow goals may be affected changes in inflation or deflation in product and operating information about The Kroger Co. by: COVID-19 pandemic related factors, risks operating costs; stock repurchases; Kroger’s (Kroger®) and its consolidated subsidiaries. It is and challenges, including among others, the ability to retain pharmacy sales from third party intended to provide general information about length of time that the pandemic continues, payors; consolidation in the healthcare industry, Kroger and therefore does not include the new variants of the virus, the effect of the including pharmacy benefit managers; Kroger’s Company’s consolidated financial statements easing of restrictions, lack of access to vaccines ability to negotiate modifications to multi- and notes. -

Hunger in Lane County More Than One in Three Lane County Residents Experience Food Insecurity

FOOD FOR LANE COUNTY ANNUAL REPORT 2015-2016 Hunger in Lane County More Than One in Three Lane County Residents Experience Food Insecurity Food insecurity is a lack of access, at times, to Why do people experience food insecurity? enough food for an healthy lifestyle. Too often • Fixed income • Minimal or no benefits this means a difficult trade-off between important • Underemployment • Chronic illness basic needs such as medical care, housing, or • Lack of affordable housing • Student loan debt transportation, and nutritiously adequate foods. • Cost of childcare • Medical bills OREGON’S FOOD INSECURITY AMONG NATION’S HIGHEST 43% OF LANE COUNTY HOUSEHOLDS STRUGGLE TO MEET BASIC NEEDS FOOD INSECURITY RANK: 6TH WORST IN LANE COUNTY SCHOOLS, 53% OF CHILDREN WERE ELIGIBLE FOR FREE AND REDUCED LUNCHES IN 2017 Source: Oregon Center for Public Policy analysis of USDA data Source: United Way of Lane County, Jan., 2016 2 OUR MISSION: ALLEVIATE HUNGER BY CREATING ACCESS TO FOOD We are a private, nonprofit 501(c)3 food bank and accomplish our mission by soliciting, collecting, rescuing, growing, preparing and packing food for distribution through a network of more than 150 partner agencies and distribution sites. FOOD for Lane County carries the operational expense of food banking and processing with no fees to community partner agencies. We have built our success on the ability to be agile and responsive to the community’s need since we were founded in 1984. As the second largest food bank in Oregon, we are a partner of both the Oregon Food Bank network and Feeding America, the national food bank collaborative.