2013 Half Year Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ishares FTSE 250 UCITS ETF GBP (Dist)

iShares FTSE 250 UCITS ETF GBP (Dist) MIDD August Factsheet Unless otherwise stated, Performance, Portfolio Breakdowns and Net Assets information as at: 31-Aug-2021 All other data as at 07-Sep-2021 This document is marketing material. For Investors in Switzerland. Investors should read the Key Capital at risk. All financial investments Investor Information Document and Prospectus prior to investing. involve an element of risk. Therefore, the value of your investment and the income from it will The Fund seeks to track the performance of an index composed of 250 mid cap UK companies that vary and your initial investment amount cannot rank below the FTSE 100 Index be guaranteed. KEY FACTS KEY BENEFITS Asset Class Equity Fund Base Currency GBP Exposure to broadly diversified UK companies 1 Share Class Currency GBP 2 Direct investment into 250 UK companies Fund Launch Date 26-Mar-2004 Share Class Launch Date 26-Mar-2004 3 Single country exposure Benchmark FTSE 250 Index Valor 1828018 Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. ISIN IE00B00FV128 Total Expense Ratio 0.40% This means the Fund is more sensitive to any localised economic, market, political or regulatory Distribution Frequency Quarterly events. The value of equities and equity-related securities can be affected by daily stock market Domicile Ireland movements. Other influential factors include political, economic news, company earnings and Methodology Optimised significant corporate events. Counterparty Risk: The insolvency of any institutions providing Product Structure Physical services such as safekeeping of assets or acting as counterparty to derivatives or other Rebalance Frequency Quarterly instruments, may expose the Fund to financial loss. -

Restoring Strength, Building Value

Restoring Strength, Building Value QinetiQ Group plc Annual Report and Accounts 2011 Group overview Revenue by business The Group operates three divisions: US Services, 29% UK Services and Global Products; to ensure efficient 35% leverage of expertise, technology, customer relationships and business development skills. Our services businesses which account for more 36% than 70% of total sales, are focused on providing 2011 2010 expertise and knowledge in national markets. Our £m £m products business provides the platform to bring US Services 588.2 628.0 valuable intellectual property into the commercial UK Services 611.6 693.9 markets on a global basis. Global Products 502.8 303.5 Total 1,702.6 1,625.4 Division Revenue Employees US Services £588.2m 4,500 (2010: £628.0m) (2010: 5,369) Underlying operating profit* £44.3m (2010: £52.6m) Division Revenue Employees UK Services £611.6m 5,045 (2010: £693.9m) (2010: 5,707) Underlying operating profit* £48.7m (2010: £59.1m) Division Revenue Employees Global £502.8m 1,663 Products (2010: £303.5m) (2010: 2,002) Underlying operating profit* £52.4m (2010: £8.6m) * Definitions of underlying measures of performance are in the glossary on page 107. Underlying operang profit* by business Revenue by major customer type Revenue by geography 7% 17% 36% 31% 52% 37% 56% 31% 33% 2011 2010 2011 2010 2011 2010 £m £m £m £m £m £m US Services 44.3 52.6 US Government 894.3 754.1 North America 949.2 825.3 UK Services 48.7 59.1 UK Government 526.5 614.5 United Kingdom 623.7 720.0 Global Products 52.4 8.6 Other 281.8 -

Schroder UK Mid Cap Fund

Schroder UK Mid Ca p Fund plc Half Year Report and Accounts For the six months ended 31 March 2020 Key messages – Portfolio of “high conviction” stocks aiming to provide a total return in excess of the FTSE 250 (ex-Investment Companies) Index and an attractive level of yield. – Dividend has tripled since 2007 as portfolio investments have captured the cash generative nature of investee companies, in a market where income has become an increasingly important part of our investors’ anticipated returns. – Provides exposure to dynamic mid cap companies that have the potential to grow to be included in the FTSE 100 index, which are at an interesting point in their life cycle, and/or which could ultimately prove to be attractive takeover targets. – Proven research driven investment approach based on the Manager’s investment process allied with a strong selling discipline. – Managed by Andy Brough and Jean Roche with a combined 50 years’ investment experience 1, the fund has a consistent, robust and repeatable investment proces s. 1Andy Brough became Lead Manager on 1 April 2016 . Investment objective Schroder UK Mid Cap Fund plc’s (the “Company”) investment objective is to invest in mid cap equities with the aim of providing a total return in excess of the FTSE 250 (ex -Investment Companies) Index. Investment policy The strategy is to invest principally in the investment universe associated with the benchmark index, but with an element of leeway in investment remit to allow for a conviction-driven approach and an emphasis on specific companies and targeted themes. The Company may also invest in other collective investment vehicles where desirable, for example to provide exposure to specialist areas within the universe. -

Your Guide Directors' Remuneration in FTSE 250 Companies

Your guide Directors’ remuneration in FTSE 250 companies The Deloitte Academy: Promoting excellence in the boardroom October 2018 Contents Overview from Mitul Shah 1 1. Introduction 4 2. Main findings 8 3. The current environment 12 4. Salary 32 5. Annual bonus plans 40 6. Long term incentive plans 52 7. Total compensation 66 8. Malus and clawback 70 9. Pensions 74 10. Exit and recruitment policy 78 11. Shareholding 82 12. Non-executive directors’ fees 88 Appendix 1 – Useful websites 96 Appendix 2 – Sample composition 97 Appendix 3 – Methodology 100 Your guide | Directors’ remuneration in FTSE 250 companies Overview from Mitul Shah It has been a year since the Government announced its intention to implement a package of corporate governance reforms designed to “maintain the UK’s reputation for being a ‘dependable and confident place in which to do business’1, and in recent months we have seen details of how these will be effected. The new UK Corporate Governance Code, to take effect for accounting periods beginning on or after 1 January 2019, includes some far reaching changes, and the year ahead will be a period of review and change for many companies. Remuneration committees must look at how best to adapt to an expanded remit around workforce remuneration, as well as a greater focus on how judgment is used to ensure that pay outcomes are justified and supported by performance. Against this backdrop, 2018 has been a mixed year in the FTSE 250 executive pay environment. In terms of pay outcomes, the picture is relatively stable. Overall pay levels have fallen for FTSE 250 chief executives and we have seen continued momentum in companies adopting executive alignment features such as holding periods, as well as strengthening shareholding guidelines for executives. -

2020 Half Year Report

MidCap_HY_Cover.qxp 25/02/2021 11:25 Page FC1 JPMorgan Mid Cap Investment Trust plc Half Year Report & Financial Statements for the six months ended 31st December 2020 MidCap_HY_Cover.qxp 25/02/2021 11:25 Page IFC2 KEY FEATURES Your Company Objective JPMorgan Mid Cap Investment Trust plc (the ‘Company’) aims to achieve capital growth from investment in medium-sized UK listed companies. The Company specialises in investment in FTSE 250 companies, using long and short term borrowings to increase returns to shareholders. Investment Policies • To focus on FTSE 250 stocks that deliver strong capital growth. • To have significant exposure to the UK economy, with selective exposure to overseas earnings. • To seek out both value stocks and growth stocks, including AIM stocks, to deliver strong performance throughout the market cycle. • To use gearing to increase potential returns to shareholders. • To invest no more than 15% of gross assets in other UK listed investment companies (including investment trusts). The Company’s shares are designed for private investors in the UK, including retail investors, professionally-advised private clients and institutional investors, who seek the potential for capital growth from investment in the UK market and who understand and are willing to accept the risks of exposure to equities. Private investors may wish to consider consulting an independent financial adviser who specialises in advising on the acquisition of shares and other securities before acquiring shares in the Company. Investors should be capable of evaluating the risks and merits of such an investment and should have sufficient resources to bear any loss that may result. -

FTSE 350 Climate Change Report 2013

01 Are UK companies prepared for the international impacts of climate change? FTSE 350 Climate Change Report 2013 9 October 2013 Report writer and global advisor 02 03 The evolution of CDP Contents With great pleasure, CDP announced an exciting change this year. CEO Foreword 4 Executive Summary 6 Over ten years ago CDP pioneered the only global disclosure system for companies to report their environmental impacts and strategies to investors. In that time, 2013 Climate Performance and Disclosure Leaders 8 and with your support, CDP has accelerated climate change and natural resource 2013 Leadership Criteria 10 issues to the boardroom and has moved beyond the corporate world to engage Investor insight - the “Aiming for A” coalition 11 with cities and governments. FTSE 350 companies have a global footprint 12 The CDP platform has evolved significantly, supporting multinational purchasers Companies’ focus on climate change risks and opportunities needs broadening 12 to build more sustainable supply chains. It enables cities around the world to exchange information, take best practice action and build climate resilience. We Scientific Insight - Professor Sir Brian Hoskins 17 assess the climate performance of companies and drive improvements through Companies’ understanding of their value chain is limited 20 shareholder engagement. Corporate insight - Reckitt Benckiser 22 Our offering to the global marketplace has expanded to cover a wider spectrum of FTSE 100 companies have a more sophisticated response the earth’s natural capital, specifically water and forests, alongside carbon, energy to climate change than FTSE 250 companies 23 and climate. Preparing for climate change: Comparing FTSE 100 and FTSE 250 companies 26 For these reasons, we have outgrown our former name of the Carbon Disclosure PwC commentary – Celine Herweijer 28 Project and rebranded to CDP. -

Close Brothers Group Plc Annual Report 2013 Close Brothers Makes Loans, Trades Securities and Provides Financial Advice and Investment Management Services

Annual Report 2013 Close Brothers Group plc Close Brothers Close Brothers Group plc Annual Report 2013 Close Brothers makes loans, trades securities and provides financial advice and investment management services. Corporate Overview 1 Financial Highlights 2 Our Business 4 Chairman’s and Chief Executive’s Statement 8 Business Model 10 Strategy and Key Performance Indicators Business Review 12 Financial Overview 18 Banking 20 Securities 22 Asset Management 24 Principal Risks and Uncertainties Governance 28 Board of Directors 30 Executive Committee 31 Report of the Directors 33 Corporate Governance 44 Corporate Responsibility 47 Report of the Board on Directors’ Remuneration Financial Statements 61 Report of the Auditor 62 Consolidated Income Statement 63 Consolidated Statement of Comprehensive Income 64 Consolidated Balance Sheet 65 Consolidated Statement of Changes in Equity 66 Consolidated Cash Flow Statement 67 Company Balance Sheet 68 The Notes 112 Investor Relations 112 Cautionary Statement Close Brothers Group plc 1 Annual Report 2013 Corporate Overview Financial Highlights for the year ended 31 July 2013 Adjusted operating profit £166.5m 8 3.1p £ million (2012: £134.2m) (2012: 67.3 p) 200 166.5 1 2 160 Adjusted operating profit Adjusted basic earnings 131.2 134.2 113.7 116.5 per share 120 80 40 0 £16 3.1m 81.6p 2009 2010 2011 2012 2013 (2012: £134.9m) (2012: 68.6p) Adjusted basic earnings per Operating profit before tax Basic earnings per share share pence 90 83.1 67.3 60.5 64.8 £119.4m 44.5p 60 58.2 30 (2012: £99.7m) (2012: 41.5p) 0 Profit attributable to shareholders Ordinary dividend per share3 2009 2010 2011 2012 2013 Ordinary dividend per share 1 Stated before exceptional items and amortisation of intangible assets on acquisition. -

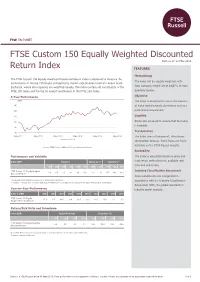

FTSE FACTSHEET FTSE Custom 150 Equally Weighted Discounted Data As At: 31 May 2016

FTSE FACTSHEET FTSE Custom 150 Equally Weighted Discounted Data as at: 31 May 2016 Return Index FEATURES bmkTitle1 Methodology The FTSE Custom 150 Equally Weighted Discounted Return Index is designed to measure the The index will be equally weighted, with performance of the top 150 largest companies by market capitalization listed on London Stock each company weight set at 0.667% at each Exchange, where all companies are weighted equally. The index contains all constituents of the quarterly review. FTSE 100 Index and the top 50 largest constituents of the FTSE 250 Index. Objective 5-Year Performance (GBP) The index is designed for use in the creation 130 of index tracking funds, derivatives and as a 120 performance benchmark. 110 Liquidity 100 Stocks are screened to ensure that the index is tradable. 90 Transparency 80 May-2011 May-2012 May-2013 May-2014 May-2015 May-2016 The index uses a transparent, rules-based Data as at month end construction process. Index Rules are freely available on the FTSE Russell website. FTSE Custom 150 Equally Weighted Discounted Return Availability Performance and Volatility The index is calculated based on price and Index (GBP) Return % Return pa %* Volatility %** total return methodologies, available real- time and end-of-day. 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR FTSE Custom 150 Equally Weighted Industry Classification Benchmark 2.9 -1.7 -0.5 -8.2 6.1 17.1 2.0 3.2 17.7 14.6 11.9 Discounted Return Index constituents are categorized in * Compound annual returns measured over 3 and 5 years respectively accordance with the Industry Classification ** Volatility – 1YR based on 12 months daily data. -

Fund Manager Commentary Royal London Equities May 2017

ASSET MANAGEMENT FUND MANAGER COMMENTARY ROYAL LONDON EQUITIES MAY 2017 For professional investors only, not suitable for retail investors TABLE OF CONTENTS RLAM EQUITY PERFORMANCE 3 ROYAL LONDON UK EQUITY INCOME FUND 4 ROYAL LONDON UK GROWTH FUND 5 ROYAL LONDON UK MID CAP GROWTH FUND 6 ROYAL LONDON UK OPPORTUNITIES FUND 7 ROYAL LONDON UK SMALLER COMPANIES FUND 8 CONTACT DETAILS 9 2 | PAGE RLAM EQUITY PERFORMANCE 1 month (%) Rolling 12 months (%) RL UK Equity Income M Inc 4.47 23.82 IA UK Equity Income Sector 3.58 21.59 FTSE All Share Index 4.36 24.52 RL UK Growth Fund M Acc 3.48 25.06 IA UK All Companies Sector 3.58 21.59 FTSE All Share Index 4.36 24.52 RL UK Mid Cap Growth Fund M Acc 3.26 18.66 IA UK All Companies Sector 3.58 21.59 FTSE 250 Index 2.15 19.48 RL UK Opportunities Fund M Acc 2.75 15.15 IA UK All Companies Sector 3.58 21.59 FTSE All Share Index 4.36 24.52 RL UK Smaller Companies Fund M Acc 4.29 22.61 IA UK Smaller Companies Sector 3.54 27.56 FTSE Small Cap ex IT Index 1.78 23.99 Source: RLAM and FE. Returns quoted are net of fees. Past performance is not a guide to future performance. The value of investments and the income from them is not guaranteed and may go down as well as up and investors may not get back the amount originally invested. -

Ishares FTSE 250 UCITS ETF

iShares FTSE 250 UCITS ETF GBP (Dist) MIDD August Factsheet Performance, Portfolio Breakdowns and Net Assets information as at: 31/08/ 2021 All other data as at 07/09/2021 For Investors in Luxembourg. Investors should read the Key Investor Information Document and Capital at risk. All financial investments Prospectus prior to investing. involve an element of risk. Therefore, the value of your investment and the income from it will The Fund seeks to track the performance of an index composed of 250 mid cap UK companies that vary and your initial investment amount cannot rank below the FTSE 100 Index be guaranteed. KEY FACTS KEY BENEFITS Asset Class Equity Fund Base Currency GBP Exposure to broadly diversified UK companies 1 Share Class Currency GBP 2 Direct investment into 250 UK companies Fund Launch Date 26/03/2004 Share Class Launch Date 26/03/2004 3 Single country exposure Benchmark FTSE 250 Index ISIN IE00B00FV128 Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. Total Expense Ratio 0,40% Distribution Type Quarterly This means the Fund is more sensitive to any localised economic, market, political or regulatory Domicile Ireland events. The value of equities and equity-related securities can be affected by daily stock market Methodology Optimised movements. Other influential factors include political, economic news, company earnings and Product Structure Physical significant corporate events. Counterparty Risk: The insolvency of any institutions providing Rebalance Frequency Quarterly services such as safekeeping of assets or acting as counterparty to derivatives or other UCITS Yes instruments, may expose the Fund to financial loss. -

Close Brothers Group Stakeholder Pension Plan – Extended Fund Range

Close Brothers Group Stakeholder Pension Plan – Extended Fund Range Choosing your own investments When you're considering making your own investment choice, there are some things you need to think about before you select your own funds. This guide gives detailed information about the funds available to you and what you need to be aware of before making your choice. This guide was produced inApril 2021. Contents Should I make a different investment choice? page 3 Understanding investment programmes page 4 Your investment programme options page 6 Choosing your own investment funds page 15 Working out your attitude to investment risk page 18 Fund risk warnings page 20 Charges page 22 The funds you can choose from page 23 More information and help page 35 Important documents This guide should be read alongside the ‘How contributions are invested’ guide which explains where your contributions are invested when you join the scheme. You should also read it with the Key features document for an understanding of the plan aims and risks. If you do not have any of these documents, please call 0800 068 1431 2 Should I make a different investment choice? We understand that some people may find the default If, after reading the ‘How contributions are invested’ guide, you investment solution does not match their attitude to decide the default investment solution isn’t appropriate, or investment risk or invests in areas that they wouldn’t choose you would like to choose your own investments, this guide for themselves. provides you with information about the options available. It’s important to ensure that your investments are right for you Once you’ve decided where to invest contributions, you can and are in line with the amount of investment risk you are update your plan using Membersite, www.aviva.co.uk prepared to take. -

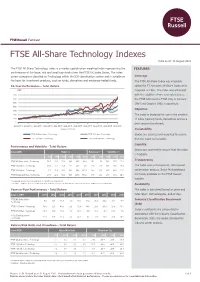

FTSE All-Share Technology Indexes

FTSE Russell Factsheet FTSE All-Share Technology Indexes Data as at: 31 August 2021 bmkTitle1 The FTSE All-Share Technology Index is a market-capitalization weighted index representing the FEATURES performance of the large, mid and small cap stocks from the FTSE UK Index Series. The index covers companies classified as Technology within the ICB classification system and is suitable as Coverage the basis for investment products, such as funds, derivatives and exchange-traded funds. The FTSE All-Share Index was originally 10-Year Performance - Total Return called the FT Actuaries All-Share Index at its (GBP) inception in 1962. The index was enhanced 700 with the addition of two new sub-indexes, 600 the FTSE 100 and the FTSE 250, in January 500 1984 and October 1992, respectively. 400 Objective 300 200 The index is designed for use in the creation 100 of index tracking funds, derivatives and as a 0 performance benchmark. Aug-2011 Aug-2012 Aug-2013 Aug-2014 Aug-2015 Aug-2016 Aug-2017 Aug-2018 Aug-2019 Aug-2020 Aug-2021 Data as at month end Investability FTSE All-Share Index - Technology FTSE 100 Index - Technology Stocks are selected and weighted to ensure FTSE 250 Index - Technology FTSE SmallCap Index - Technology that the index is investable. Liquidity Performance and Volatility - Total Return Stocks are screened to ensure that the index Index (GBP) Return % Return pa %* Volatility %** is tradable. 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR Transparency FTSE All-Share Index - Technology 14.1 29.0 27.8 18.6 48.5 44.4 14.1 7.6 16.5 25.7 21.8 FTSE 100 Index - Technology 17.4 30.1 26.9 5.1 40.2 4.8 11.9 0.9 20.5 25.5 29.3 The index uses a transparent, rules-based FTSE 250 Index - Technology 7.7 25.9 24.0 33.1 58.6 151.9 16.6 20.3 19.5 34.4 21.5 construction process.