Educational Institutions GST on Educational Institutions ?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Jaina Doctrine of Karma and the Science of Genetics

i | The Jaina Doctrine of Karma and The Science of Genetics The Jaina Doctrine of Karma and the Science of Genetics ii | The Jaina Doctrine of Karma and The Science of Genetics About the Author D r . Sohan Raj Tater (b.1947) is presently Pro-Vice Chancellor of Singhania University, Pacheri Bari (Jhunjhunu), Rajasthan. Earlier, he served in Public Health Engineering Department, Government of Rajasthan, for 30 years, and took voluntary retirement from the post of Superintending Engineer. Also, he is Honourary Advisor to Jain Vishva Bharati University, Ladnun. A well-known scholar of Jainism, Dr. Tater has to his credit a good number of research papers published in national and international journals of repute. Also, he has participated in various seminars and conferences in India and abroad. iii | The Jaina Doctrine of Karma and The Science of Genetics The Jaina Doctrine of Karma and the Science of Genetics Dr. Sohan Raj Tater Edited by Dr. Narayan Lal Kachhara New Delhi iv | The Jaina Doctrine of Karma and The Science of Genetics This publication is sponsored by Kothari Ashok Kumar Kailash Chand Tater, Jasol (Madurai) and their family members in the memory of their father late Shri Chandanmalji with the inspiration of their mother Mrs. Luni Devi. Copyright © Author All rights reserved. Without limiting the rights under copyright reserved above, no part of this publication may be reproduced, utilized, stored in or introduced into a retrieval system, or transmitted, in any form or by any means (electronic, mechanical, photocopying, recording, or otherwise), without the prior written permission of both the copyright owner and the publisher. -

The Transformations and Challenges of a Jain Religious Aspirant

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by DigitalCommons@Florida International University Florida International University FIU Digital Commons FIU Electronic Theses and Dissertations University Graduate School 3-22-2016 The rT ansformations and Challenges of a Jain Religious Aspirant from Layperson to Ascetic: An Anthropological Study of Shvetambar Terapanthi Female Mumukshus Komal Ashok Kumar [email protected] Follow this and additional works at: http://digitalcommons.fiu.edu/etd Part of the Feminist, Gender, and Sexuality Studies Commons, New Religious Movements Commons, Other Religion Commons, Rhetoric Commons, and the Social and Cultural Anthropology Commons Recommended Citation Ashok Kumar, Komal, "The rT ansformations and Challenges of a Jain Religious Aspirant from Layperson to Ascetic: An Anthropological Study of Shvetambar Terapanthi Female Mumukshus" (2016). FIU Electronic Theses and Dissertations. Paper 2481. http://digitalcommons.fiu.edu/etd/2481 This work is brought to you for free and open access by the University Graduate School at FIU Digital Commons. It has been accepted for inclusion in FIU Electronic Theses and Dissertations by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. FLORIDA INTERNATIONAL UNIVERSITY Miami, Florida THE TRANSFORMATIONS AND CHALLENGES OF A JAIN RELIGIOUS ASPIRANT FROM LAYPERSON TO ASCETIC: AN ANTHROPOLOGICAL STUDY OF SHVETAMBAR TERAPANTHI FEMALE MUMUKSHUS A thesis submitted in partial fulfillment of the requirements for the degree of MASTER OF ARTS in RELIGIOUS STUDIES by Komal Ashok Kumar 2016 To: Dean John F. Stack Steven J. Green School of International and Public Affairs This thesis, written by Komal Ashok Kumar, and entitled The Transformations and Challenges of a Jain Religious Aspirant from Layperson to Ascetic: An Anthropological Study of Shvetambar Terapanthi Female Mumukshus, having been approved in respect to style and intellectual content, is referred to you for judgment. -

International Conference on Science and Jain Philosophy

Knowledge may be destructive; Enlightenment is always constructive. InternationalInternational ConferenceConference onon ScienceScience andand JainJain PhilosophyPhilosophy JanuaryJanuary 8-10,8-10, 20162016 || VVenue:enue: IITIIT BombayBombay Register online at www.icsjp.org E-mail: [email protected] Contact +91 96198 21485, +91 98196 04985 Secretariat Noble Mission. Global Vision. BX-01, Woodland, H8, Indian Institute of Technology Bombay, Powai, Mumbai – 400 076. Organized by In collaboration with Follow us on Bhagawan Mahavira International Research Centre, IIT Bombay International Conference on Science and Jain Philosophy Jain Vishva Bharati Institute (Deemed University), Ladnun, Rajasthan, India University of Mumbai Somaiya Vidyavihar @jainphilosophy Knowledge Partner Centre for Philosophy and Foundations of Science, New Delhi Knowledge precedes conduct. Knowledge comes - Mahavira from learning, wisdom comes from awakening. OBJECTIVE In spite of the unprecedented advancements in science and technology, the scientists themselves have accepted their limitations with regards to knowledge of ultimate truths. They also agree that the global problems like violence, global warming, ORGANIZER disparity etc. have intensified as the consequences of wanton use of technology. On the other hand, the ancient wisdom, manifested in Bhagawan Mahavira International Research Centre (BMIRC) the "darshan" (vision) of the sages and seers, especially the Jain Tirthankars, have deeper vision of ultimate reality which includes With a view to integrate science and Jain philosophy and to evolve a Consciousness as well as the physical world. On the basis of this scientific approach to understanding of Jain traditions, BMIRC has kind of intuitive vision, they have prescribed certain spiritual recently been established at Jain Vishva Bharati Institute (Deemed techniques to mitigate the destructive emotions, giving birth to the University), Ladnun, Rajasthan. -

Jainism Chapter 1

Jainism Chapter 1 Rajesh Kumar Jain M M I G , B - 23, Ram Ganga V i h a r , Phase 2, Extn, M o r a d a b a d - 2 4 4 0 0 1 , UP- B h a r a t . (India) Asia 2013 2014 2015 2016 Copyright © Rajesh Kumar Jain, Moradabad-UP-Bharat. 1 From the Desk of Author Dear Readers:- I am happy to publish first chapter of an English version book Jainism, there was a huge demand from south Bharat, USA and UK, so I tried to write and publish the same. My mother tongue is Hindi, so, there are chances of mistakes and hoping that readers will help to rectify the same. Thanks Rajesh Kumar Jain I wrote my first book in 2013, published on wordpress and BlogSpot, book was listed on Pothi and Chinemonteal in 2014, the second edition was published, listed in 2015 and the language was Hindi. Year wise Readers 2013,2014,2015 25000 21600 20000 15000 Series1 10000 6300 5000 1700 0 1 2 3 2 Month Wise Readers of 2013,2014,2015 3500 N o 3000 2500 o f 2000 1500 Series1 R Series2 e 1000 a 500 Series3 d e 0 r s Month Readers were from 72 USA 13550 countries, list of Top Bharat 9509 eighteen countries are Sweden 3901 given with data. France 552 Germany 250 Taiwan 233 UK 195 European 177 Singapore 107 Japan 70 Russia 64 Canada 46 UAE 46 Indonesia 25 Nepal 23 Australia 22 Malaysia 15 Thailand 15 others 800 3 Country wise Readers at a Glance USA Bharat Sweden France Germany Taiwan UK European Singapore Japan Russia Canada UAE Indonesia Nepal Australia Malaysia Thailand others Year Readers % Growth 2013 1700 - 2014 6300 85 2015 21600 242 4 Left to Right: My Wife Smt Alka Jain, Me, My Mother Smt Prem Lata Jain Left to Right: My son Er Varun Jain, Me, My mother Smt Prem Lata Jain 5 Left to Right My son Er Rajat Jain, Me, My daughter in Law Er Vartika Jain 6 Mangalam Bhagavan viro, Mangalam gautamo gani, Mangalam kundakundadya, Jain dharmostu mangalam. -

FINAL DISTRIBUTION.Xlsx

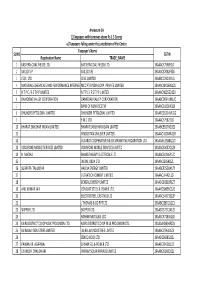

Annexure-1A 1)Taxpayers with turnover above Rs 1.5 Crores a) Taxpayers falling under the jurisdiction of the Centre Taxpayer's Name SL NO GSTIN Registration Name TRADE_NAME 1 EASTERN COAL FIELDS LTD. EASTERN COAL FIELDS LTD. 19AAACE7590E1ZI 2 SAIL (D.S.P) SAIL (D.S.P) 19AAACS7062F6Z6 3 CESC LTD. CESC LIMITED 19AABCC2903N1ZL 4 MATERIALS CHEMICALS AND PERFORMANCE INTERMEDIARIESMCC PTA PRIVATE INDIA CORP.LIMITED PRIVATE LIMITED 19AAACM9169K1ZU 5 N T P C / F S T P P LIMITED N T P C / F S T P P LIMITED 19AAACN0255D1ZV 6 DAMODAR VALLEY CORPORATION DAMODAR VALLEY CORPORATION 19AABCD0541M1ZO 7 BANK OF NOVA SCOTIA 19AAACB1536H1ZX 8 DHUNSERI PETGLOBAL LIMITED DHUNSERI PETGLOBAL LIMITED 19AAFCD5214M1ZG 9 E M C LTD 19AAACE7582J1Z7 10 BHARAT SANCHAR NIGAM LIMITED BHARAT SANCHAR NIGAM LIMITED 19AABCB5576G3ZG 11 HINDUSTAN UNILEVER LIMITED 19AAACH1004N1ZR 12 GUJARAT COOPERATIVE MILKS MARKETING FEDARATION LTD 19AAAAG5588Q1ZT 13 VODAFONE MOBILE SERVICES LIMITED VODAFONE MOBILE SERVICES LIMITED 19AAACS4457Q1ZN 14 N MADHU BHARAT HEAVY ELECTRICALS LTD 19AAACB4146P1ZC 15 JINDAL INDIA LTD 19AAACJ2054J1ZL 16 SUBRATA TALUKDAR HALDIA ENERGY LIMITED 19AABCR2530A1ZY 17 ULTRATECH CEMENT LIMITED 19AAACL6442L1Z7 18 BENGAL ENERGY LIMITED 19AADCB1581F1ZT 19 ANIL KUMAR JAIN CONCAST STEEL & POWER LTD.. 19AAHCS8656C1Z0 20 ELECTROSTEEL CASTINGS LTD 19AAACE4975B1ZP 21 J THOMAS & CO PVT LTD 19AABCJ2851Q1Z1 22 SKIPPER LTD. SKIPPER LTD. 19AADCS7272A1ZE 23 RASHMI METALIKS LTD 19AACCR7183E1Z6 24 KAIRA DISTRICT CO-OP MILK PRO.UNION LTD. KAIRA DISTRICT CO-OP MILK PRO.UNION LTD. 19AAAAK8694F2Z6 25 JAI BALAJI INDUSTRIES LIMITED JAI BALAJI INDUSTRIES LIMITED 19AAACJ7961J1Z3 26 SENCO GOLD LTD. 19AADCS6985J1ZL 27 PAWAN KR. AGARWAL SHYAM SEL & POWER LTD. 19AAECS9421J1ZZ 28 GYANESH CHAUDHARY VIKRAM SOLAR PRIVATE LIMITED 19AABCI5168D1ZL 29 KARUNA MANAGEMENT SERVICES LIMITED 19AABCK1666L1Z7 30 SHIVANANDAN TOSHNIWAL AMBUJA CEMENTS LIMITED 19AAACG0569P1Z4 31 SHALIMAR HATCHERIES LIMITED SHALIMAR HATCHERIES LTD 19AADCS6537J1ZX 32 FIDDLE IRON & STEEL PVT. -

Consciousness in Modern Science and Jain Philosophy

PROGRAM Second International Conference on Science and Jain Philosophy (ICSJP) Virtual Conference | March 19-22, 2021 CONSCIOUSNESS IN MODERN SCIENCE AND JAIN PHILOSOPHY Second International Conference on Science and Jain Philosophy (ICSJP) Virtual Conference | March 19-22, 2021 Organizers: FIU Jain Studies Program Steven J. Green School of International & Public Affairs Jain Education and Research Foundation (JERF) 1 Organizers: FIU Jain Studies Program Steven J. Green School of International & Public Affairs Jain Education and Research Foundation (JERF) Co-sponsors: Mohini Jain Presidential Chair in Jain Studies University of California, Davis Jain Vishva Bharati Centers Orlando, New Jersey, Houston, London Vardhamana Charitable Foundation Federation of Jain Associations in North America (JAINA) Jain Center of South Florida Knowledge Partners: Spiritual Technology Research Foundation (Mumbai) Jain Academy of Scholars (Ahmedabad) World Jain Confederation (Mumbai) ORGANIZERS CO-SPONSORS KNOWLEDGE PARTNERS Second International Conference on Science and Jain Philosophy (ICSJP) Virtual Conference | March 19-22, 2021 PROGRAM AGENDA FRIDAY, MARCH 19, 2021 7:30 AM to 7:40 AM EDT | 4:30 AM to 4:40 AM PDT | 5:00 PM to 5:10 PM IST Welcome Address Founding Dean John F. Stack, Jr. Florida International University Conference Overview Iqbal Akhtar Florida International University 7:40 AM to 9:15 AM EDT | 4:40 AM to 6:15 AM PDT | 5:10 PM to 6:45 PM IST Theme: Soul and Consciousness in Jain Philosophy Samani Chaitanya Pragya (Moderator) Florida International -

To Read JVB London Newsletter

NEWSLETTER JAIN WORLD PEACE CENTRE (JWPC LONDON) June 2020 || Volume 4 || Issue 01 INSPIRATION BOARD Inside this issue: I first came to know about priority to take our children Respected Samani Ji’s about to Respected Samani Ji’s 20 years ago when I first every Sunday for Gyanshala. Western Philosophy & Jainism 1 learnt that Jain nuns are in They were fortunate to the UK, not for a short learn the Bhaktamara Stotra Achrya Mahapragya’s life 2 duration but on a and other Jain prayers from Acharya Mahapragya Birth 5 continuous basis. I was them. For me it was ecstatic at the thought of receiving spiritual nectar JVB Global Quiz Program 7 having Jain saints in our every week and revitalising Mindfulness 10 midst and getting their myself with their blessings. constant guidance & In 2010 I was fortunate to Marathon Yatra in February 11 blessings. The ancient embark on a two year JVB Gyanshala London 14 Indian tradition of receiving distant learning Masters blessings from Gurus and course in Jainology & Mr Rajeev Shah Mahavir Jayanti Celebration 15 saints for all phases of life Comparative Religions from became a reality in the Jain Vishva Bharati Covid-19 Workshop 16 Western world. What a University, Ladnun. With not only Talk the Talk, but Learning Bhaktambar Stotra 17 foresight of Acharya Tulsi the constant support and also Walk the Talk by and Acharya Mahapragya to encouragement from Father’s Day Card Making 17 create a new Jain order of Respected Samani Ji’s, I was adhering to the stringent Jain principles. I feel Special Family Birthday 18 Samani Ji’s who adhere to blessed to get a Gold medal Celebration with Samani Ji all the vows of Jain monks and rank first in the course. -

Download Book

AHIMSA TIMES - JULY 2008 ISSUE - www.jainsamaj.org Page 1 of 15 Vol. No. 97 Print "Ahimsa Times " July, 2008 www.jainsamaj.org Board of Trustees Circulation + 80000 Copies( Jains Only ) Email: Ahimsa Foundation [email protected] New Matrimonial New Members Business Directory "Nonviolence is not inaction. It is not discussion. It is not for the timid or weak... Non-violence is hard work. It is the willingness to sacrifice. It is the patience to win." TEMPLES PARASNATH HILLS FACE THREAT DUE TO MINING Giridih, Mining, legal or otherwise, is no longer just a geological problem at the Parasnath hills. Frequent tree-felling and soil erosion have given the issue a religious angle. Geologists and environmentalists warn that if no concrete steps are taken to stop misuse of the mountain within 50 years, there would be a significant threat to the 4,431 ft Parasnath hill. Parasnath hills hold special significance for Jains as most of the Jain Tirthankars including Parsva or Parsvanath, attained nirvana on the hill. Environmentalist U.C. Mehta said the life of the mountain is decreasing fast thanks to the way trees are being cut down frequently. One of the problems is the construction of the Grand Trunk Road, which passes beside the hill. The road has been under construction for four years, and stones and soil from the hill are being used for the construction. President of Jain Swetamber Society, Kamal Singh Rampuria says he will ask the government for a survey to get exact data of the hill’s height and also to take necessary steps to maintain the condition of the hill. -

Consciousness in Modern Science and Jain Philosophy

PROGRAM Second International Conference on Science and Jain Philosophy (ICSJP) Virtual Conference | March 19-22, 2021 CONSCIOUSNESS IN MODERN SCIENCE AND JAIN PHILOSOPHY Second International Conference on Science and Jain Philosophy (ICSJP) Virtual Conference | March 19-22, 2021 Organizers: Jain Studies Program Steven J. Green School of International & Public Affairs Florida International University Jain Education and Research Foundation (JERF) 1 Organizers: FIU Jain Studies Program Steven J. Green School of International & Public Affairs Jain Education and Research Foundation (JERF) Co-sponsors: Mohini Jain Presidential Chair in Jain Studies University of California, Davis Jain Vishva Bharati Centers Orlando, New Jersey, Houston, London Vardhamana Charitable Foundation Federation of Jain Associations in North America (JAINA) Jain Center of South Florida Knowledge Partners: Spiritual Technology Research Foundation (Mumbai) Jain Academy of Scholars (Ahmedabad) World Jain Confederation (Mumbai) ORGANIZERS CO-SPONSORS KNOWLEDGE PARTNERS Second International Conference on Science and Jain Philosophy (ICSJP) Virtual Conference | March 19-22, 2021 PROGRAM AGENDA FRIDAY, MARCH 19, 2021 7:30 AM to 7:40 AM EDT | 4:30 AM to 4:40 AM PDT | 5:00 PM to 5:10 PM IST Welcome Address Founding Dean John F. Stack, Jr. Florida International University Conference Overview Iqbal Akhtar Florida International University 7:40 AM to 9:15 AM EDT | 4:40 AM to 6:15 AM PDT | 5:10 PM to 6:45 PM IST Theme: Soul and Consciousness in Jain Philosophy Samani Chaitanya Pragya -

Bhaktamar Stotra the Divine Intervention

Bhaktamar Stotra The Divine Intervention Acharya Mahapragya Jain Vishva Bharati, Ladnun Inside_PAP.indd 1 14-01-2019 15:04:09 Bhaktamar Stotra Publisher Jain Vishva Bharati Ladnun - 341306 Nagaur District (Raj) India Ph : +91 - 1581 - 226080/224671 E-mail: [email protected] ISBN : 978-81-939051-0-4 All right reserved Jain Vishva Bharati, Ladnun No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without the prior permission of the publishers. Jain Vishva Bharati, Ladnun First Edition : September 2018 Price : Rs.250/- Printed at : Pragati Offset Pvt Ltd Bhaktamar Stotra By Acharya Mahapragya Inside_PAP.indd 2 14-01-2019 15:04:09 Content Preface ................................................................. I Foreword ............................................................... III 1. Foundation for Bhaktamar Stotra ..................... 01 2. Resolutions - Making and Keeping .................... 15 3. Reunion of Intellect and Emotions ................... 25 4. Stuti – Its Value ................................................... 33 5. Realizing the Value of Stuti ................................ 41 6. Seeking Inner Beauty .......................................... 53 7. King of Three Realms Owns Nothing ............... 63 8. The Omniscient Light ......................................... 73 9. Adinath: Beyond the Sun & the Moon .............. 81 10. Illumination of Knowledge ............................... -

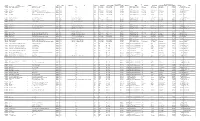

ITI Code ITI Name ITI Category Address State District Phone Number Email Name of FLC Name of Bank Name of FLC Manager Mobile No

Mapped FLC Details Mapped Bank Branch Details ITI Code ITI Name ITI Category Address State District Phone Number Email Name of FLC Name of Bank Name of FLC Manager Mobile No. Of FLC Manager Landline of FLC Address Name of Bank Name of Branch Name of Branch Manager Mobile No. of Manager Landline No. Address PR08000005 T.P Pareek I.T.C Vidyanagar Ganeshpura Road Beawar P 9-Vidyanagar Ganeshpura Beawar Rajasthan Ajmer NULL Ajmer Bank Of Baroda A K Bos ( Since Resign) 9414007977 BOB Rly Camp St Road Ajmer HDFC HDFC,Beawar HARSH BAMBA 9828049697 01462-512010 Beawar PR08000121 Raghukul Industrial Training Center P Balupura road, Adarsh nagar Rajasthan Ajmer NULL Ajmer Bank Of Baroda A K Bos ( Since Resign) 9414007977 BOB Rly Camp St Road Ajmer Bank of Baroda BOB Adhersh Nager Rakesh Bhargva 8094015498 0145 3299898 Adresh nager Ajmer PR08000438 Raj Industrial Training Centre Sirfvikisan Chatavas P Sirvisan Chatravas Ganeshpura Road Beawar Rajasthan Ajmer NULL Ajmer Bank Of Baroda A K Bos ( Since Resign) 9414007977 BOB Rly Camp St Road Ajmer HDFC HDFC,Beawar HARSH BAMBA 9828049697 01462-512010 Beawar PR08000454 Shri Baba Ramdev Pvt. Industrial Training Institute, P Arjunpura (Jagir), Via Mangliwas Rajasthan Ajmer NULL Ajmer BRKGB S K Mittal 9461016730 BRKGB,Adresh Nager Ajmer UBI UBI Manlgliyawas Sh.Gulab Singh 9783301076 0145-2785226 Mangliyawas PR08000471 Shri Balaji ITC P V & P Bandanwara, P.S Bhinay Rajasthan Ajmer NULL Ajmer BRKGB S K Mittal 9461016730 BRKGB,Adresh Nager Ajmer BRKGB BRKGB,Bandenwara Mr S K Jain 7726854671 01466-272020 Bandenwara -

Dāna and Dhyāna in Jaina Yoga: a Case Study of Prekṣādhyāna and the Terāpanth

i Dāna and Dhyāna in Jaina Yoga: A Case Study of Prekṣādhyāna and the Terāpanth by Smita Kothari A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Department for the Study of Religion Collaborative Program in South Asian Studies and Environmental Studies University of Toronto © Copyright by Smita Kothari 2013 ii Dāna and Dhyāna in Jaina Yoga: A Case Study of Prekṣādhyāna and the Terāpanth Smita Kothari Doctor of Philosophy Department for the Study of Religion Collaborative Program in South Asian Studies and Environmental Studies University of Toronto 2013 Abstract This dissertation examines the role one aspect of the Jaina tradition plays in a globalized world in the 21st century vis-à-vis an economically viable, socially just, and ecologically sustainable society. I address this by means of an in-depth study of dāna (giving, gifting, charity) and dhyāna (meditation) conducting a case study of prekṣādhyāna, a form of meditation developed by the Terāpanth, a Śvetāmbara Jaina sect, in 1975 and their stance on dāna. These practices, the Terāpanth claim, are transformative on an individual and societal level. I argue that while prekṣādhyāna’s spiritually transformative influence remains narrowly circumscribed to the individual level, nevertheless it allows the Terāpanth to participate in the booming economy of the transnational yoga market. Yet, as my analyses of their historically controversial position on dāna vis-à-vis the Jaina position on dāna and the recent change in this position within the Terāpanth reveal, their ability to transform the world is limited to their own community. I explore, through participation/observation, how prekṣādhyāna as a performative ritual brings an individual closer to spiritual liberation, and attempt to demonstrate how the Terāpanth construct this practice as a form of modern yoga by using authoritative discourses of science and scripture.