Main Street Restaurant Group Inc. – MAIN Embarking on a Growth Phase – Initiating Coverage with a BUY

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Hope Center, Inc Orders Due to Tracy by 10:00 Am Monday

Family Order Form Created: 3/15/2019 2:57:17 PM New Hope Center, Inc Orders due to Tracy by 10:00 am Monday. Gift cards will be in by Thursday at 4:00pm. More options available on the website www.shopwithscrip.com. Feel free to add to the form or place your order online. Payments due before order will be placed. Name Customer # Check # Order Date Product % QTY Total Product % QTY Total Product % QTY Total 1-800-Baskets $50.00 12% $ Delta Air Lines $250.00 4% $ Old Navy $100.00 14% $ Ace Hardware $25.00 4% $ Denny's $10.00 7% $ Olive Garden $25.00 8% $ aerie $25.00 10% $ Dick's Sporting Goods 8% $ Outback Steakhouse 8% $ $25.00 $25.00 Aeropostale $25.00 10% $ Disney $25.00 3% $ Panera Bread $10.00 8% $ Amazon.com $25.00 2.25% $ Domino's $10.00 8% $ Panera Bread $25.00 8% $ American Eagle® 10% $ $25.00 Dunkin' Donuts $10.00 3% $ Papa John's Pizza 9% $ $10.00 American Girl $100.00 9% $ Einstein Bros. Bagels 10% $ $10.00 Papa Murphy's Pizza 8% $ American Girl $25.00 9% $ $10.00 Exxon $50.00 1% $ Piggly Wiggly (WI, IL 3% $ Apple iTunes $15.00 5% $ Festival Foods (WI) - 3% $ only) $100.00 Applebee's $25.00 8% $ Skogens $25.00 Piggly Wiggly (WI, IL 3% $ Festival Foods (WI) - 3% $ only) $25.00 Arby's $10.00 8% $ Skogens $50.00 Piggly Wiggly (WI, IL 3% $ only) $50.00 Barnes & Noble $10.00 8% $ Foot Locker $25.00 8% $ Pizza Hut (Not AK or HI) 8% $ Bath & Body Works 12% $ Funset Boulevard 8% $ $10.00 $10.00 $25.00 Pizza Ranch $25.00 8% $ Best Buy $100.00 4% $ GameStop $25.00 3% $ Prime Membership from 8% $ Best Buy $25.00 4% $ Geek Squad & Best Buy -

NEWCASTLE Cushman & Wakefield Global Cities Retail Guide

NEWCASTLE Cushman & Wakefield Global Cities Retail Guide 0 A city once at the heart of the Industrial Revolution, Newcastle has now repositioned itself as a thriving and vibrant capital of the North East. The city offers a blend of culture and heritage, superb shopping, sporting activity and nightlife with the countryside and the coastline at its doorstep. The city is located on the north bank of the River Tyne with an impressive seven bridges along the riverscape. The Gateshead Millennium Bridge is the newest bridge to the city, completed in 2001 - the world’s first and only titling bridge. Newcastle benefits from excellent fast rail links to London with journey times in under three hours. Newcastle Airport is a top ten UK airport and the fastest growing regional airport in the UK, with over 5 million passengers travelling through the airport annually. This is expected to reach 8.5 million by 2030. NEWCASTLE OVERVIEW 1 Cushman & Wakefield | Newcastle | 2019 NEWCASTLE KEY RETAIL STREETS & AREAS NORTHUMBERLAND ST GRAINGER ST & CENTRAL EXCHANGE Newcastle’s traditional prime retail street. Running Grainger Street is located between Newcastle Station and between Haymarket Metro Station to the north and Newcastle’s main retail core. It not only plays host to the Blackett St to the south. It is fully pedestrianised and a key historic Central Exchange Building and Central Arcade footfall route. Home to big brands including H&M, Primark, within, but also Newcastle’s famous Grainger Market. Marks & Spencer, Fenwick among other national multiple Grainger Street is one of Newcastle’s most picturesque retail brands. -

Corner Bakery Cafe Franchise Disclosure Document 2012.Pdf

85 7th Place East, Suite 500 MINNESOTA St. Paul, Minnesota 55101-2198 DEPARTMENT OF www.commerce.5tate.mn.us COMMERCE 651.296.4026 FAX 651.297.1959 An equal opportunity employer May 22, 2012 MARISA D FAUNCE PLAVE KOCH PLC 12355 SUNRISE VALLEY DRIVE SUITE 230 RESTON, VA 20191 Re: F-5468 CBC RESTAURANT CORPORATION CORNER BAKERY CAFE FRANCHSIE AGREEMENT Dear Ms. Faunce: The Annual Report has been reviewed and is in compliance with Minnesota Statute Chapter 80C and Minnesota Rules Chapter 2860. This means that there continues to be an effective registration statement on file and that the franchisor may offer and sell the above-referenced franchise in Minnesota. The franchisor is not required to escrow franchise fees, post a Franchise Surety Bond or defer receipt of franchise fees during this registration period. As a reminder, the next annual report is due within 120 days after the franchisor's fiscal year end, which is December 31, 2012. Sincerely, MIKE ROTHMAN Commissioner By: Daniel Sexton Commerce Analyst Supervisor Registration Division (651)296-4520 MR:DES:dlw F-5468 STATE OF MINNESOTA DEPARTMENT OF COMMERCE REGISTRATION DIVISION (651) 296-6328 IN THE MATTER OF THE REGISTRATION OF: CORNER BAKERY CAFE FRANCHSIE AGREEMENT By CBC RESTAURANT CORPORATION ORDER AMENDING REGISTRATION WHEREAS, an application to amend the registration and amendment fee have been filed, IT IS HEREBY ORDERED that the registration dated September 29, 2006, is amended as of the date set forth below JL MIKE ROTHMAN Commissioner Department of Commerce 85 7th Place East, Suite 500 St Paul, MN 55101 Date: May 22, 2012 UNIFORM FRANCHISE REGISTRATION APPLICA1\I0N Filei<Jo. -

Regular Meeting of the Azle City Council

AZLE MUNICIPAL DEVELOPMENT DISTRICT REGULAR MEETING CITY COUNCIL CHAMBERS 613 S.E. PARKWAY AZLE, TEXAS 76020 TUESDAY February 11, 2014 AGENDA President Ray Ivey Jack Stevens Vice President Kevin Ingle Justin Berg Secretary Joe McCormick Council Member Paul Crabtree Council Member William Chambers REGULAR SESSION 7:00 p.m. CALL TO ORDER PRESENTATION 1. Presentation of the MDD’s Quarterly Investment Report for Quarter ended December 31, 2013 Executive Director Craig Lemin ACTION ITEMS 2. Consider approving the Minutes of the January 14, 2014 Azle MDD regular meeting Secretary Joe McCormick 3. Discuss upcoming economic development conferences and consider any action on amending the FY2013-2014 budget to allocate funds for travel and training expenses President Ray Ivey DISCUSSION ITEMS 4. Discuss setting goals and priorities of the Strategic Plan for the Azle MDD President Ray Ivey 5. Discussion regarding Azle Municipal Development District plans/procedures/policies President Ray Ivey ADJOURNMENT I, the undersigned authority, do hereby certify the above Agenda was posted at City Hall on February 7, 2014 at the City’s official bulletin board and is readily accessible to the public at all times in accordance with V.T.C.A. Chapter 551, Texas Government Code. ______________________________ Susie Hiles, Assistant to the City Manager Date Agenda Removed from Posting This facility is wheelchair accessible and handicapped parking spaces are available. Auxiliary aids and services are available to a person when necessary to afford an equal opportunity to participate in city functions and activities. Auxiliary aids and services or accommodations should be requested forty-eight hours prior to the scheduled starting time by calling the City Secretary’s Office at 817-444-7101. -

FOOD SERVICE FACILITY Recent Inspection Log

BUREAU OF ENVIRONMENTAL HEALTH FOOD SERVICE FACILITY Recent Inspection Log The following is a list of all inspections conducted at retail food service facilities in Howard County during the most recent calendar month. Inspection Date: Inspection Type: Facility Name: Facility Type: Risk Priority: 03/01/2017 Comprehensive PAPA JOHNS PIZZA #1725 RESTAURANT High 03/01/2017 Monitoring THE GREENE TURTLE COLUMBIA LLC RESTAURANT High 03/01/2017 Reinspection BOTTOM OF THE BAY RESTAURANT High 03/01/2017 Monitoring HARPER'S CHOICE MIDDLE SCHOOL EXEMPT High 03/01/2017 Comprehensive SUBWAY RESTAURANT High 03/01/2017 Comprehensive VILLA ITALIAN KITCHEN RESTAURANT Moderate 03/01/2017 Monitoring PIZZA BOLI'S RESTAURANT Moderate 03/01/2017 Monitoring SHANNON'S SALOON RESTAURANT High 03/01/2017 Monitoring SAKURA JAPANESE STEAK HOUSE RESTAURANT High 03/01/2017 Monitoring POLLO FELIZ & TAQUERIA RESTAURANT High 03/01/2017 Monitoring COAL FIRE PIZZA, LLC RESTAURANT High 03/01/2017 Monitoring KAHLER HALL EXEMPT High 03/01/2017 Monitoring DUNKIN DONUTS - SNOWDEN DONUTS CAFÉ Moderate 03/01/2017 Monitoring MANJOO BAKERY BAKERY High 03/02/2017 Monitoring LILYS MEXICAN MARKET RESTAURANT High 03/02/2017 Monitoring LU & JOE'S, INC. TAVERN High 03/02/2017 Reinspection MT. HEBRON HIGH SCHOOL EXEMPT High 03/02/2017 Monitoring PATUXENT VALLEY MIDDLE SCHOOL EXEMPT High 03/02/2017 Monitoring DUNKIN DONUTS/BASKIN ROBBINS RESTAURANT Moderate 03/02/2017 Monitoring GIANT FOOD STORE #300 MARKET High 03/02/2017 Monitoring ACE SUSHI @ GIANT STORE #300 SUSHI High Page 1 of 11 Printed on: April 12, 2017 Inspection Date: Inspection Type: Facility Name: Facility Type: Risk Priority: 03/02/2017 Monitoring SUBWAY SANDWICHES RESTAURANT High 03/02/2017 Comprehensive ASEAN BISTRO RESTAURANT High 03/02/2017 Monitoring Myeong Dong RESTAURANT High 03/02/2017 Comprehensive SUBWAY RESTAURANT High 03/02/2017 Monitoring MT. -

Side 2 Merchant Denom

Side 2 Merchant Denom. % Qty Total Merchant Denom. % Qty Total DINING - ON THE GO DINING *Arby's $10 7% *@Applebee's $10/25/50 7% #@Burger King $10 4% Bob Evans $10 9% *@Chipotle $10 9% *Bonefish Grill (use Outback) $25 7% @Cold Stone Creamery $10 7% @Boston Market $10 10% *Crazy Bowls and Wraps $10 / 25 20% Bravo / Brio Tuscan Grill $25 10% *Dairy Queen $10 3% *#@Buffalo Wild Wings $10/25 7% *#@Domino's Pizza*9% til gone** $10 7% *@California Pizza Kitchen $25 7% *Dunkin' Donuts $10 3% *@Cheesecake Factory $25 5% *Einstein Brothers Bagels $10 9% *@Chili's $25/50 9% *Fazoli's $25 7% Chuck E. Cheese $10 7% *Great Harvest Bread Co. $10 6% Cracker Barrel $10/25 8% Hardee's $10 5% @Dave & Buster $25 11% *Imo's Pizza $10 / 25 6% Denny's $10 7% *Jack in the Box $10 4% *Egg & I $25 9.1% Little Ceasars Pizza $20 7% *Fuddrucker's $25 7% Mrs. Field's Cookies $5 9% *Hacienda $25 20% Noodles & Company $10 7% *Houlihan's $25 7% *Panda Express $25 7% *@IHOP $25 7% *@Papa John's Pizza $10 7% *Longhorn Steak Hs(use Red Lobster) $25 8% @Pizza Hut $10 7% *@Maggianno's (use Chili's) $25/50 9% *Qdoba Mexican Grill $25 7% @Morton's/ McCormick & Schmick's $25/100 8% *@St. Louis Bread Co $10 / 25 8% *@O'Charley's $25 11% *#@Starbucks $10 / 25 7% *@Olive Garden (use Red Lobster) $25 8% *Steak & Shake $10 7% *Outback/Flemings/Bonefish Gr $25 7% *#Subway $10 /50 6% *Pasta House $10/15 15% *Taco Bell $10 5% *@P.F. -

The Food Industry Scorecard

THE FOOD INDUSTRY SCORECARD An evaluation of food companies’ progress making—and keeping— animal welfare promises humanesociety.org/scorecard Executive summary Most of the largest U.S. food companies have publicly pledged to eliminate certain animal abuses from their supply chains. But as countless consumers have asked: are they keeping their promises? For context, the vast majority of animals in our food system live Here’s the good news: that kind of radical view is out of in dismal conditions. Mother pigs are locked in gestation crates step with traditional American values. Agribusiness may see ani- so small they can’t turn around. Egg-laying hens are crammed mals as mere machines, but consumers don’t. into cages so tightly they can’t even spread their wings. And chickens in the poultry industry are bred to grow so large, so ɠ As the American Farm Bureau reports, nearly all consumers (95%) believe farm animals should be fast they suffer from agonizing leg disorders. treated well. It wasn’t always this way. Throughout history, animals hav- en’t been forced to endure such miserable lives. (And today, ɠ The Food Marketing Institute found that animal welfare is shoppers’ second most important social issue. there are certainly farmers who don’t use these abusive prac- tices.) But as agri-culture developed into agri-business, the ɠ The food industry analytics firm Technomic concluded industry’s relationship to animals became more severe. that for American restaurant patrons, concerns about animal cruelty outweigh those regarding the “Forget the pig is an animal,” urged Hog Farm Management environment, fair trade, local sourcing and other issues. -

Starbucks Åpner Sin Andre Kaffebar I Bergen

Starbucks åpner sin andre kaffebar i Bergen Oslo, 19. august – Starbucks har inngått avtale om å åpne nok en kaffebar i Bergen sentrum. Fra før er der kjent at Starbucks kommer i Kjøttbasaren, med forventet åpning i november. Nå er det klart at Starbucks i februar 2014 åpner en kaffebar i Neumannsgate 25. Lokalene benyttes i dag av restaurant Sumo, som vil flytte til lokalene ved siden av (se egen pressemelding). Starbucks har med dette sikret seg to gode beliggenheter i Bergen, og fortsetter jakten etter flere med uforminsket styrke. Den nye Starbucks kaffebaren vil ha ca. 50 sitteplasser og prosessen med å ansette flere baristaer er i gang. Umoe Restaurants fikk de geografiske rettighetene til Starbucks for Norge og Sverige i september i fjor, og arbeider målrettet med å ekspandere det amerikanske kaffekonseptet i de største byene i Norge og Sverige. - Vi er veldig glade for å ha sikret oss to gode lokaliteter for Starbucks i Bergen, sier direktør for Starbucks Skandinavia, Joannis Vendrig. Vi ser fram til å tilby kvalitetskaffe og den gode Starbucks- opplevelsen til byens innbyggere og besøkende. Umoe Restaurants har i løpet av det siste halve året samarbeidet med Starbucks i London for å trene opp nye Starbucks-partnere (alle ansatte i Starbucks kalles partnere) for å sikre at alle kunder får en suveren og unik kaffeopplevelse, ”The Starbucks Experience”. Partnerne trenes opp i alt fra baristakunst til kaffekjedens historie. Samtidig kommer det erfarne Starbucks-partnere over fra andre land for å bistå de nye butikkene i åpningsfasen. ### Om Umoe Restaurants Umoe Restaurants er et ledende restaurant-selskap i Skandinavia med 320 restauranter og kafeer. -

Commons at Willowbrook NEC Highway 249 & FM 1960, Houston, Texas 77070

SHOPPING CENTER FOR LEASE Commons At Willowbrook NEC Highway 249 & FM 1960, Houston, Texas 77070 Edge Realty Partners Kathy King | Vice President Debbie Adams | Principal 5444 Westheimer Rd, Suite 1650, Houston, Texas 77056 [email protected] | 713.900.3030 [email protected] | 713.900.3006 713.900.3000 | edge-re.com 336 CONROE COMMONS AT WILLOWBROOK | PROPERTY INFORMATION CLEVELAND MOSS HILL 45 59 LOCATION THE WOODLANDS NEC Highway 249 & FM 1960 Houston, Texas 77070 TOMBALL HEMPSTEAD 290 SPRING DAYTON SIZE LIBERTY 90 249 GEORGE BUSH 99 448,812 sf INTERCONTINENTAL HUMBLE CYPRESS AIRPORT AVAILABLE SPACE 8 69 See site plan for availability 8 Anchor, junior anchor & small shop space available TOLL 10 SEALY 10 KATY RANAUAC A T E 99 6 610 HOUSTON BAYTOWN 225 Please call for pricing PASADENA WILLIAM P. SUGAR LAND HOBBY AIRPORT TRAFFIC COUNTS 8 ROSENBERG 90 TOLL 161,956 CPD 66,690 CPD Highway 249 FM 1960 PEARLAND ELLINGTON FIELD AIRPORT 59 2019 DEMOGRAPHIC SNAPSHOT 6 MAJOR45 TENANTS PROPERTY INFORMATION NEEDVILLE ALVIN 1 Mile 3 Mile 5 Mile Academy, Conn’s, Ross, Michaels, Marshalls, • Super regional intersection of Highway 249 and FM 1960 288 TEXAS CITY 36 HomeGoods, The Tile Shop, Total Wine, DSW, • Across from Willowbrook Mall featuring tenants such as Nordstrom TOTAL POPULATION 13,069 93,653 306,346 Rack, Macy's , Dillard's, JCPenney, Forever 21 and H&M Ulta, Men’s Wearhouse, Bath & Body Works, DAYTIME POPULATION 19,344 103,437 247,764 GALVESTON • Great tenant line up with excellent visiblity & signage TGI Fridays, Chipotle, McAlister’s Deli, -

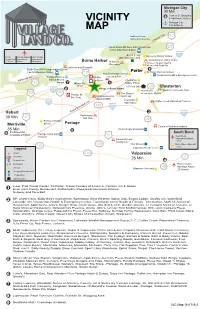

VLC Map 11X17v5-2

Michigan City 30 Min 8 Franklin St. Shopping & Lighthouse Outlets 20 VICINITY Michigan City MAP Port AuthorityCalumet Trail Indiana Dunes 12 National Lakeshore Calumet Trail 94 South Shore RR Dune Park (Chesterton) 20 1:35 to Millennium Station Seven Peaks Discovery Charter School 94 O’Hare Chicago Midway Gary Chicago Waterpark Duneland 421 International International International Indiana Dunes Visitor Center 1:10 Hour 1 Hour 25 Minutes Burns Harbor Marquette Fairhaven Baptist Church, Greenway College, and Academy Lakefront and Riverwalk South Shore RR Portage/Ogden Dunes 2 1:26 to Millennium Station Porter St Patrick Catholic School 12 Yost Elementary School Chesterton Health & Emergency Center Portage Public & BH Fire Lakeland Park Marquette Trail Marina Shores BH Police Chesterton 12 Marina 7 Bass Pro 1 Middle School Shops US Post Office 49 Chesterton 6 Village in Burns Harbor 94 Westchester Sand Creek Country Club 20 The Brassie Intermediate School 20 Portage #2 Imagination Glen Golf Club Fire Dept. Outdoor BMX Chesterton Coffee Creek Watershed Preserve 90 High School 149 65 90 Hobart Prairie-Duneland Trail 3 Robbinhurst 90 30 Min 6 Golf Club 49 Portage Christian School Portage Merriville Courts of Northwest Indiana 35 Min 5 Porter Regional Hospital Southlake Mall South Bend 9 Crossings at Hobart Portage Community Hospital 6 South Bend 6 Sunset Hill Farm International Airport 1 Hour County Park 149 49’er Drive-in Notre Dame University 130 1 Hour 2 Legand Valparaiso Health Center 421 Airport 130 Valparaiso Fire/Police 25 Min 2 Medical -

A Publix Prime Commercial Property Is Available for Sale Or Lease!

A Publix prime commercial property is available for Sale or Lease! The property is ideal for a National Franchise (Pizza Hut, KFC, TGI Fridays etc.) It is located at the corner of a major lighted intersection (Ridge Road and DeCubellis Road New Port Richey, Florida) This area is expected to increase in value as there are plans for an extension from Ridge RD/Moon Lake to connect to the Veterans Highway (SR 589), which will cut down the commute time to Tampa. This extension will increase traffic count on Ridge RD dramatically. For more information: Owner: Lazaros Terzidis Tel: 727 493 2020 Email: [email protected] Private Website: www.grrealty.com Property information: Size 34, 905 SF .8± acres Real estate taxes for 2018 $4,333 Parcel ID 32-25-17-0000-00400-0090 Sale Price $1,290,000 Rental Rate: $2.25 /SF/Yr $6,500/month (5-20 Years, 10% increase every five years ) Owner Financing! The property is free and clear of any debt Address Ridge Road & Decubellis Road, New Port Richey, 34654 Pasco County, Florida Location The subject is located on the south west side of the Ridge road and Decubellis Road intersection in the Publix Shopping Center, Pasco County, FL. Site Size .8± acres 34,905 SF Existing Land Use C2 Contiguous North C2 - East C2 - West Res - South C2 Property uses Flood Zone A, X Utilities & Services Water - Sanitary Sewer - Storm Water - Electric - Fire (Available at site) Property Tax Data Parcel ID# 32 25 17 0000 00400 0090 R.E. Taxes $4,333 (2018) Ownership Lazaros Terzidis Legal Description COM AT MOST SLY COR OF THE OAKS -

A Passion for Quality. a Promise of Value. Handcrafted Dishes, 100% BEEF BURGERS, ALL-NATURAL CHICKEN, Hand-Cut Vegetables, and OVEN-BAKED Buns

A PASSION FOR QUALITY. A PROMISE OF VALUE. HANDCRAFTED DISHES, 100% BEEF BURGERS, ALL-NATURAL CHICKEN, HAND-CUT VEGETABLES, AND OVEN-BAKED BUNS. WE DO ALL THIS BECAUSE QUALITY IS THE ONLY waY TO DELIVER VALUE. AND YOU DESERVE BOTH. Dear Guests, under EU regulation, at your request please ask to speek to the duty manager who can provide you with information which of our menu items contain allergens. & WINE GLASS BOTTLE GLASS BOTTLE RED 150ml 750 ml WH ITE 150ml 750 ml NEBLINA NEBLINA COCKTAILS NON-ALCOHOLIC Cabernet Sauvignon 18 ZŁ 79 ZŁ Sauvignon Blanc 18 ZŁ 79 ZŁ Chile Chile NewULTIMATE SALTY DIRTY DOG 30 ZŁ STRAWBERRY BANANA SMOOTHIE 17 ZŁ Premium vodka, Jägermeister, fresh lemon Fresh banana, strawberry purée, cream of NEBLINA ANTERRA and lime juices, grapefruit syrup. coconut, pineapple juice, grenadine. Merlot 18 ZŁ 79 ZŁ DELLE VENEZIE I.G.T. Chile Pinot Grigio 19 ZŁ 87 ZŁ BLACKBERRY LONG ISLAND ICED TEA 27 ZŁ NOVEMBER SEABREEZE 13 ZŁ Italy Premium vodka, premium white rum, Cranberry and apple juices, fresh lime and JINDA – LEE premium gin, Chambord Liqueur, Triple Sec, lemon juices, club soda. Shiraz - 90 ZŁ CARMEN blackberries, fresh lime and lemon juices, Australia PREMIER 1850RESERVA fresh lemon, 7 Up. TRIPLE BERRY SMOOTHIE 21 ZŁ CASABLANCA VALLEY D.O. Strawberry purée, blackberries, raspberries, ’14/15 CHIANTI Chardonnay - 139 ZŁ ULTIMATE LONG ISLAND ICED TEA 35 ZŁ agave nectar, lime and lemon juices, TENUTE GUICCIARDINI STROZZI Chile Premium vodka, premium white rum, cranberry juice, cream of coconut. D.O.C.G. premium gin, Triple Sec, brandy, sweet & sour Sangiovese - 110 ZŁ mix, fresh lemon, Pepsi.