FTSE/JSE Africa Index Series V5.3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of the Recognized Foreign Exchanges Relative to the Reporting Requirement (3Rd December 2007)

List of the recognized foreign exchanges relative to the reporting requirement (3rd December 2007) Art. 15 para. 2 SESTA determines that securities dealers must report all the infor- mation necessary to ensure a transparent market (reporting requirement). In Art. 2 following SESTO-SFBC the appropriate implementing regulations are determined. Exceptions of the reporting requirement are recorded in Art. 4 SESTO-SFBC. Art. 4 letter a SESTO-SFBC determines that the securities dealer shall not be obliged to report transactions abroad in foreign securities admitted for trading on a Swiss stock exchange, provided that they are conducted on a foreign stock exchange recognized by Switzerland. According to established practice relative to the release of the reporting require- ment, recognized exchanges are the exchanges that are united in the World Fed- eration of Exchanges and/or the Federation of European Stock Exchanges (FESE). All foreign exchanges that are authorized by the Swiss Federal Banking Commis- sion in accordance with Art. 14 SESTO are also recognized exchanges concerning this matter, even they are neither member of the World Federation of Exchanges nor of the FESE. As an exception to this rule, besides the Deutsche Börse AG (member of World Federation of Exchanges) also the remaining German (regional) exchanges are recognized in this context. Name Location AMERICAN STOCK EXCHANGE New York, USA AMMAN STOCK EXCHANGE Amman, JORDAN ATHENS EXCHANGE Athens, GREECE AUSTRALIAN STOCK EXCHANGE Sydney, AUSTRALIA BAYERISCHE BÖRSE Munich, GERMANY BERMUDA STOCK EXCHANGE Hamilton, BERMUDA BOLSA DE COMERCIO DE BUENOS AIRES Buenos Aires, ARGENTINA BOLSA DE COMERCIO DE SANTIAGO Santiago, CHILE BOLSA DE VALORES DE COLOMBIA Bogota, COLOMBIA BOLSA DE VALORES DE LIMA Lima, PERU BOLSA DE VALORES DO SAO PAULO Sao Paulo, BRAZIL Name Location BOLSA MEXICANA DE VALORES Mexico, MEXICO BOLSAS Y MERCADOS ESPANOLES Barcelona, Bilbao, Madrid, Valencia, SPAIN BOMBAY STOCK EXCHANGE LTD. -

South Africa and Namibia

SOUTH AFRICA AND NAMIBIA SOUTH AFRICA $881.61 Bn $200.29 Bn Equity Market Debt Market 372 125 136% 260% 59% Capitalization Capitalization Number of Number of Domestic Total Equity Debt Market listed issuers Equity Market Market Cap/ Cap/GDP companies (bonds) Cap/GDP GDP 91,716,796,484 $2,127.21 Bn Equity Market Share Volume Traded Debt Market Total Nominal Traded NAMIBIA $138.37 Bn* $2.72 Bn 17% 953%* 19% Equity Market Debt Market 44* 10 Domestic Total Equity Domestic Capitalization Capitalization Number of Number of Equity Market Market Cap/ Debt Market listed issuers Cap/GDP GDP Cap/GDP companies (bonds) 193,100,874 41,296,398 Equity Market Share Volume Traded Debt Market Instrument Volume Traded *Includes dual-listings and ETFs. CFA Institute Research Foundation | 1 SOUTH AFRICA AND NAMIBIA • 1881: Kimberley Royal 1880s Stock Exchange established • 1886: Gold discovered on the reef • 1895: Durban Roodepoort • 1887: Johannesburg Stock 1890s Deep listed on the JSE Exchange (JSE) established • 1897: South African Breweries (SAB) listed on the JSE • 1901: Cape Town stock exchange established 1900s • 1904: Namibian Stock Exchange (NSX) founded 1910s • 1910: NSX closed • 1947: Stock Exchanges 1940s Control Act was passed in SA • 1963: JSE joins World 1960s Federation of Exchanges • 1990: Namibian independence from South Africa • 1992: NSX established (second time); First • 2000: JSE moves to corporate bond (SAB) issued 1990s Sandton; First ETF listed on in South Africa the JSE • 1996: Open outcry trading • 2001: FTSE agreement with ceases -

FTSE Factsheet

FTSE Russell Factsheet FTSE LATIBEX Index Series Data as at: 29 December 2017 bmkTitle1 FTSE Group and Bolsas y Mercados Españoles (BME) have joined forces to create three indices, FEATURES the FTSE LATIBEX All-Share Index, FTSE LATIBEX TOP Index and the FTSE LATIBEX Brazil Index. These provide investors with real-time access, in one single point, to the performance of Coverage Latin American stocks listed on LATIBEX and denominated in Euros. The indexes measure the performance of Latin American stocks listed on LATIBEX The benchmark FTSE LATIBEX All-Share Index has been designed to represent the performance of the LATIBEX market in real-time. The index comprises all securities that are listed on the Objective market, covering eight countries: Argentina, Brazil, Mexico and Peru. LATIBEX offers international investors a gateway to Latin American equity markets. The FTSE LATIBEX TOP Index is a tradable index for derivatives, designed to represent the LATIBEX is a market segment for Latin performance of the largest and most liquid securities trading on LATIBEX. The index comprises American securities based in Madrid (Spain). the fifteen largest listed securities, who have specialist liquidity providers. The free-float weight Investment products such as warrants and is capped at 10% to ensure that it meets fund regulatory requirements worldwide to avoid over- certificates are already issued on FTSE concentration in any one stock. LATIBEX TOP and listed on the Spanish The FTSE LATIBEX BRAZIL Index is a Euro-denominated tradable index covering Brazilian Exchange, Deutsche Börse, Euronext and stocks, and ranks the most liquid listed on LATIBEX by free float adjusted market cap. -

FTSE Factsheet

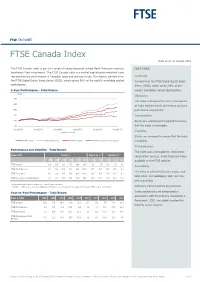

FTSE FACTSHEET FTSE Canada Index Data as at: 31 August 2015 bmkTitle1 The FTSE Canada Index is part of a range of indices designed to help North American investors FEATURES benchmark their investments. The FTSE Canada index is a market-capitalisation weighted index representing the performance of Canadian large and mid cap stocks. The index is derived from Coverage the FTSE Global Equity Index Series (GEIS), which covers 98% of the world’s investable market Derived from the FTSE Global Equity Index capitalization. Series (GEIS), which covers 98% of the 5-Year Performance - Total Return world’s investable market capitalisation. (CAD) Objective 300 The index is designed for use in the creation 250 of index tracking funds, derivatives and as a 200 performance benchmark. 150 Investability 100 Stocks are selected and weighted to ensure 50 that the index is investable. Aug-2010 Aug-2011 Aug-2012 Aug-2013 Aug-2014 Aug-2015 Liquidity Data as at month end Stocks are screened to ensure that the index FTSE Canada FTSE North America FTSE Developed FTSE Developed ex North America is tradable. Transparency Performance and Volatility - Total Return The index uses a transparent, rules-based Index (CAD) Return % Return pa %* Volatility %** construction process. Index Rules are freely 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR available on the FTSE website. FTSE Canada -6.5 -7.4 -3.1 -7.1 29.8 33.3 9.1 5.9 13.3 11.9 9.6 Availability FTSE North America -0.2 0.4 10.9 21.0 96.4 149.1 25.2 20.0 14.9 11.6 8.4 The index is calculated based on price and FTSE Developed -1.0 0.3 12.5 17.8 86.2 114.6 23.0 16.5 12.4 11.0 9.1 total return methodologies, both real time FTSE Developed ex North America -2.3 0.1 14.9 13.5 72.8 78.1 20.0 12.2 12.3 12.3 11.4 and end-of-day. -

Appendix D to Tradition SEF Rulebook Equities Product Listing

Appendix D to Tradition SEF Rulebook Equities Product Listing Broad-Market Equity Index Swap Product Listing Tradition SEF, Inc. I. Discussion of contracts; not readily susceptible to manipulation • Index Selection: Tradition SEF limits the indexes underlying its equity index swap offerings to well-established, publicly available third-party equity index market benchmarks. Tradition SEF believes that the size and liquidity of the cash market that underlies these indexes creates in each case a deliverable supply of underlying securities and volume of trading that would not make them easily susceptible to manipulation. Furthermore, Tradition SEF believes that the large number of participants in each market, and the calculation of each index being based on actual transaction data from major stock markets further limit the susceptibility of manipulation of these indexes. The broad-based equity indexes underlying swaps on Tradition SEF are the timeliest, recognized and reliable benchmarks for equity prices in their respective markets. The index levels are readily available and commercially acceptable as benchmarks for investors, portfolio managers and public policy makers. Tradition SEF believes that such benchmark indexes, which also underlie liquid index futures contracts on major Designated Contract Markets, and equity index exchange traded funds on stock exchanges, due to the large number of index members, ubiquity, and broad-market nature are not readily susceptible to manipulation. Furthermore, the associated index futures contracts and exchange traded funds offer a deep liquidity pool to hedge and risk-manage swaps based on such indexes’ index. Swap Contract Specifications: A discussion of Variance and Volatility Swaps: Equity Index Variance and volatility swaps pay out on the degree of stock price fluctuation, not the absolute level or direction of the underlying index. -

Esg Disclosure in Comparative Perspective: Optimizing Private Ordering in Public Reporting

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Penn Law: Legal Scholarship Repository ESG DISCLOSURE IN COMPARATIVE PERSPECTIVE: OPTIMIZING PRIVATE ORDERING IN PUBLIC REPORTING VIRGINIA HARPER HO* & STEPHEN KIM PARK** ABSTRACT Demand for corporate non-financial “environmental, social, and governance” (ESG) information from investors and governments is on the rise globally, and leading securities regulators and stock exchanges worldwide now encourage or mandate its disclosure by large firms. However, rising demand has been matched by growing dissatisfaction with ESG informational gaps in financial reports, on the one hand, and the dearth of investment-grade information in corporate sustainability reports and other public sources, on the other. These developments raise questions about whether the Securities and Exchange Commission (SEC) and its counterparts in other jurisdictions should continue to defer primarily to private market-based approaches to ESG disclosure, reform the disclosure framework to expressly address non-financial information, or seek to combine elements of both public disclosure regulation and private ordering in new ways. This Article anticipates these policy choices by assessing the range of approaches to ESG disclosure that have been adopted in the United States and six other influential jurisdictions: South Africa, Brazil, the European Union, the United Kingdom, Hong Kong, and * Professor of Law and Associate Dean for International & Comparative Law, University of Kansas School of Law. ** Associate Professor of Business Law and Satell Fellow in Corporate Social Responsibility, University of Connecticut. Prior versions of this Article were presented at the National Business Law Scholars Conference, the American Society of Comparative Law Workshop on Comparative Business and Financial Law at Fordham Law School, and the Notre Dame Law School Faculty Colloquium. -

FTSE TWSE Taiwan Technology Index

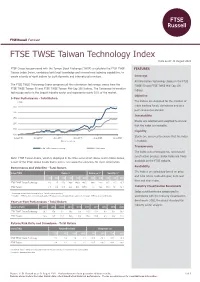

FTSE Russell Factsheet FTSE TWSE Taiwan Technology Index Data as at: 31 August 2021 bmkTitle1 FTSE Group has partnered with the Taiwan Stock Exchange (TWSE) to calculate the FTSE TWSE FEATURES Taiwan Index Series, combining both local knowledge and international indexing capabilities, to create a family of eight indices for both domestic and international investors. Coverage All information technology stocks in the FTSE The FTSE TWSE Technology Index comprises all the information technology stocks from the TWSE 50 and FTSE TWSE Mid Cap 100 FTSE TWSE Taiwan 50 and FTSE TWSE Taiwan Mid-Cap 100 Indices. The Taiwanese information indices. technology sector is the largest industry sector and represents nearly 30% of the market. Objective 5-Year Performance - Total Return (TWD) The indices are designed for the creation of 350 index tracking funds, derivatives and as a performance benchmark. 300 Investability 250 Stocks are selected and weighted to ensure 200 that the index is investable. 150 Liquidity 100 Stocks are screened to ensure that the index Aug-2016 Aug-2017 Aug-2018 Aug-2019 Aug-2020 Aug-2021 Data as at month end is tradable. Transparency FTSE TWSE Taiwan Technology FTSE Taiwan The index uses a transparent, rules-based bmkTitle3 construction process. Index Rules are freely Note: FTSE Taiwan Index, which is displayed in the time-series chart above and in tables below, available on the FTSE website. is part of the FTSE Global Equity Index Series. See www.ftse.com/geis for more information. Availability Performance and Volatility - Total Return The indices are calculated based on price Index (TWD) Return % Return pa %* Volatility %** and total return methodologies, both real 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR time and end-of-day. -

Download Investment Profile

Vanguard® Vanguard® FTSE Social Index Fund Product Summary Vanguard Style View : Large Growth Seeks to track the performance of the FTSE4Good US Select Index. Index of large- and mid-capitalization U.S. companies screened for certain social criteria. Market cap weighted index composed of large- and Investment style mid-capitalization stocks. Value Blend Growth Screened for certain environmental, social, and corporate Large governance (ESG) criteria. Specifically excludes stocks of certain companies in the following Mid industries: adult entertainment, alcohol, tobacco, weapons, fossil Small fuels, gambling, and nuclear power.* Market capitalization Excludes stocks of certain companies that do not meet standards Central tendency of U.N. global compact principles and companies that do not meet Expected range of fund holdings certain diversity criteria.* Employs a passively managed, full-replication approach. Quarterly Commentary People and Process The human toll of COVID-19 further mounted during the second Vanguard FTSE Social Index Fund seeks to track the performance quarter of 2021 amid fresh outbreaks of the virus and new of the FTSE4Good US Select Index, a market cap weighted index variants. The global economy nevertheless continued to rebound composed of large- and mid-capitalization stocks that is screened sharply if unevenly. Countries that have better succeeded in for certain environmental, social, and corporate governance (ESG) containing the virus—whether through vaccinations, lockdowns, or criteria by the Index sponsor, which is independent of Vanguard. both—tended to fare the best. With the reopening of economies Specifically, the Index excludes stocks of certain companies in the and pent-up demand boosting corporate profits, global stocks following industries: adult entertainment, alcohol, tobacco, finished the quarter significantly higher. -

Xtrackers FTSE All-World Ex UK UCITS ETF Supplement to The

Xtrackers FTSE All-World ex UK UCITS ETF Supplement to the Prospectus This Supplement contains information in relation to Xtrackers FTSE All-World ex UK UCITS ETF (the “Fund”), a sub-fund of Xtrackers (IE) plc (the “Company”) an umbrella type open-ended investment company with segregated liability between sub-funds and with variable capital governed by the laws of Ireland and authorised by the Central Bank of Ireland (the “Central Bank”). This Supplement forms part of, may not be distributed unless accompanied by (other than to prior recipients of the prospectus of the Company dated 26 February 2021 (the “Prospectus”)), and must be read in conjunction with, the Prospectus. An investment in the Fund should not constitute a substantial proportion of an investment portfolio and may not be appropriate for all investors. Xtrackers (IE) plc Dated 26 February 2021 M-19981595-71 ________________________________________________________________________________________ IMPORTANT INFORMATION The Fund is an ETF. The Shares of this Fund are fully transferable to investors and will be listed for trading on one or more stock exchanges. 2 M-19981595-71 ________________________________________________________________________________________ TERMS OF THE SHARES REPRESENTING INTERESTS IN THE FUND ________________________________________________________________________________________ Investment Objective The investment objective of the Fund is to track the performance before fees and expenses of the Underlying Asset, which is the FTSE All-World ex UK Index (the “Reference Index”). The Reference Index is designed to reflect the performance of shares of companies from developed countries and emerging markets worldwide excluding the UK. Further information on the Reference Index is contained under "General Description of the Underlying Asset". Investment Policy In order to seek to achieve the investment objective, the Fund will adopt a Direct Investment Policy. -

FTSE/JSE Top 40 Index

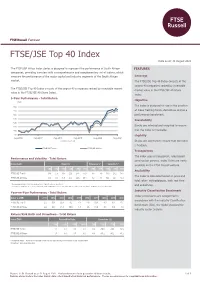

FTSE Russell Factsheet FTSE/JSE Top 40 Index Data as at: 31 August 2021 bmkTitle1 The FTSE/JSE Africa Index Series is designed to represent the performance of South African FEATURES companies, providing investors with a comprehensive and complementary set of indices, which measure the performance of the major capital and industry segments of the South African Coverage market. The FTSE/JSE Top 40 Index consists of the largest 40 companies ranked by investable The FTSE/JSE Top 40 Index consists of the largest 40 companies ranked by investable market market value in the FTSE/JSE All-Share value in the FTSE/JSE All-Share Index. Index. 5-Year Performance - Total Return Objective The index is designed for use in the creation of index tracking funds, derivatives and as a performance benchmark. Investability Stocks are selected and weighted to ensure that the index is investable. Liquidity Stocks are screened to ensure that the index is tradable. Transparency The index uses a transparent, rules-based Performance and Volatility - Total Return construction process. Index Rules are freely Index (ZAR) Return % Return pa %* Volatility %** available on the FTSE Russell website. 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR Availability FTSE/JSE Top 40 -0.6 2.5 14.5 22.6 27.8 53.0 8.5 8.9 17.3 23.2 15.5 The index is calculated based on price and FTSE/JSE All Share -0.1 4.0 15.9 25.2 26.6 49.1 8.2 8.3 16.4 22.5 15.2 total return methodologies, both real time * Compound annual returns measured over 3 and 5 years respectively and end-of-day. -

Purple-Group-Annual-Report-2016

2Awards and Highlights 1 Purple Philosophy 2 Chairman’s Letter 4 Chief Executive Officer’s Letter 5 Chief Financial Officer’s Report 6 12Ethical Leadership 38Directors’ Responsibility 86 Notice of Annual General Meeting 86 and Corporate Citizenship 12 for Financial Reporting 38 Shareholder Rights 90 Summary Governance Results 19 Group Secretary’s Report 39 Brief Curriculum Vitae of Our People 20 Directors’ Report 40 Directors Standing for Re-election 90 Our Leadership Report of the Audit Committee 42 Form of Proxy 91 Executive Team Management Team 22 Report of the Independent Auditor 43 Notes to the Form of Proxy 92 Board Members 24 Consolidated Statement Corporate Information 93 of Profit or Loss 44 Your Thoughts Our Team 26 Consolidated Statement of 94 Other Comprehensive Income 45 Consolidated Statement of Financial Position 46 Consolidated Statement of Changes in Equity 47 Consolidated Statement 28 of Cash Flows 48 Navigate the Markets 28 Notes to the Consolidated Annual Our Brands – Emperor 30 Financial Statements 49 Our Brands – EasyEquities 32 Shareholder Analysis 85 Our Brands – GT247.com 34 Our Brands – GT Private Broking 36 INVESTING AND TRADING SOLUTIONS FOR EVERYONE First World Trader (FWT) t/a Emperor Asset Management Proprietary First World Trader Nominees Proprietary GT247.com Limited (EAM) Limited (FWTN) Non-discretionary Category I FAIS licence, Discretionary Category II FAIS licence, which Approved by the FSB to operate and hold which provides FWT the ability to conduct provides EAM the ability to conduct an clients’ assets in the name of the nominee. an intermediary and advisory service on intermediary investment management service STRATE approval to hold equity securities on derivatives, shares, money market, retail on derivatives, shares, money market and behalf of clients. -

Wealth Management | Global After the Storm Covid 19 Has Permanently Changed the Way Wealth Managers Deliver Advice and Serve Their Clients

M BLUEPAPER Wealth Management | Global After the Storm Covid 19 has permanently changed the way Wealth Managers deliver advice and serve their clients. To drive outperformance over the next 5+ years, firms should double down on technology investments, strategically cut costs, build differentiated product offerings and consider inorganic opportunities. Oliver Wyman is a global leader in management consulting. For more information, visit www.oliverwyman.com. Oliver Wyman is not authorized or regulated by the PRA or the FCA and is not providing investment advice. Oliver Wyman authors are not research analysts and are neither FCA nor FINRA registered. Oliver Wyman authors have only contributed their expertise on business strategy within the report. Oliver Wyman’s views are clearly delineated. The securities and valuation sections of this report are the work of Morgan Stanley only and not Oliver Wyman. For disclosures specifically pertaining to Oliver Wyman, please see the Disclosure Section located at the end of this report. Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. M BLUEPAPER Authors MORGAN STANLEY OLIVER WYMAN Betsy L. Graseck, CFA1 Kai Upadek EQUITY ANALYST PARTNER +1 212 761 8473 +44 20 7852 7657 [email protected] [email protected] Magdalena L Stoklosa, CFA2 Christian Edelmann EQUITY ANALYST PARTNER +44 20 7425 3933 +44 20 7852 7557 [email protected] [email protected] Nick Lord3 Bradley Kellum EQUITY ANALYST PARTNER +65 6834 6746 +1 646 364 8425 [email protected] [email protected] Michael J.