Draft Red Herring Prospectus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Group Housing

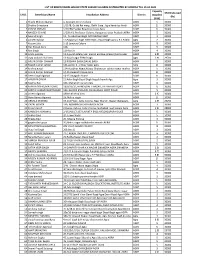

LIST OF ALLOTED PROPERTIES DEPARTMENT NAME- GROUP HOUSING S# RID PROPERTY NO. APPLICANT NAME AREA 1 60244956 29/1013 SEEMA KAPUR 2,000 2 60191186 25/K-056 CAPT VINOD KUMAR, SAROJ KUMAR 128 3 60232381 61/E-12/3008/RG DINESH KUMAR GARG & SEEMA GARG 154 4 60117917 21/B-036 SUDESH SINGH 200 5 60036547 25/G-033 SUBHASH CH CHOPRA & SHWETA CHOPRA 124 6 60234038 33/146/RV GEETA RANI & ASHOK KUMAR GARG 200 7 60006053 37/1608 ATEET IMPEX PVT. LTD. 55 8 39000209 93A/1473 ATS VI MADHU BALA 163 9 60233999 93A/01/1983/ATS NAMRATA KAPOOR 163 10 39000200 93A/0672/ATS ASHOK SOOD SOOD 0 11 39000208 93A/1453 /14/AT AMIT CHIBBA 163 12 39000218 93A/2174/ATS ARUN YADAV YADAV YADAV 163 13 39000229 93A/P-251/P2/AT MAMTA SAHNI 260 14 39000203 93A/0781/ATS SHASHANK SINGH SINGH 139 15 39000210 93A/1622/ATS RAJEEV KUMAR 0 16 39000220 93A/6-GF-2/ATS SUNEEL GALGOTIA GALGOTIA 228 17 60232078 93A/P-381/ATS PURNIMA GANDHI & MS SHAFALI GA 200 18 60233531 93A/001-262/ATS ATUULL METHA 260 19 39000207 93A/0984/ATS GR RAVINDRA KUMAR TYAGI 163 20 39000212 93A/1834/ATS GR VIJAY AGARWAL 0 21 39000213 93A/2012/1 ATS KUNWAR ADITYA PRAKASH SINGH 139 22 39000211 93A/1652/01/ATS J R MALHOTRA, MRS TEJI MALHOTRA, ADITYA 139 MALHOTRA 23 39000214 93A/2051/ATS SHASHI MADAN VARTI MADAN 139 24 39000202 93A/0761/ATS GR PAWAN JOSHI 139 25 39000223 93A/F-104/ATS RAJESH CHATURVEDI 113 26 60237850 93A/1952/03 RAJIV TOMAR 139 27 39000215 93A/2074 ATS UMA JAITLY 163 28 60237921 93A/722/01 DINESH JOSHI 139 29 60237832 93A/1762/01 SURESH RAINA & RUHI RAINA 139 30 39000217 93A/2152/ATS CHANDER KANTA -

State Subsidy Distribution List Till 15-02-21.Xlsx

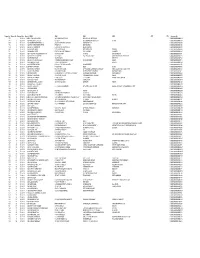

LIST OF BENEFICIARIES WHOSE STATE SUBSIDY HA BEEN DISTRIBUTED BY UPNEDA TILL 15.02.2021 Capacity SFA Disbursed S.NO. Beneficiary Name Installation Address District Installed (Rs) (kW) 1 Shashi Mohan Agarwal 1, Anupam Green Colony AGRA 5 30000 2 Shobha Srivastava 1/114B, Gulab Rai marg , Delhi Gate , Agra kendriya hindi AGRA 22 30000 3 PIYUSH PRASAD 1/192BM Sarkar Road Civil Lines Agra AGRA 10 30000 4 NAVEEN CHAND 1/209 A/1 Professor Colony, Hariparvat Uttar Pradesh AGRA AGRA 5 30000 5 Govind Singh 11, Purshottam Bagh DAYALBAGH AGRA AGRA 2 30000 6 sanjeev talwar 11,Puspanjali Bagh Extenrtion , Dayal Bagh agra C.B.S Public Agra 2 30000 7 Kusum Lata 1-13 Lawyers Colony AGRA 8 30000 8 Gur Prasad Saini 118, AGRA 5 30000 9 Ran Singh 119 Part A AGRA 4 30000 10 amita pandey 12-A,punit estate,near maruti enclave phase 2,bodla near AGRA 5.85 30000 11 vijay prakash malhotra 13 dayal nagar ERROR Agra Agra 1.98 29700 12 ARJUN SINGH CHAHAR 13 ROSHAN BAGH,DAYAL BAGH AGRA 3 30000 13 Rajesh kumar sehgal 131-sector 3 , vibhav nagar agra Agra 10 30000 14 krishna goyal 134-A,subhas Nagar,Mauja Ghatwasan subhas nagar market AGRA 5 30000 15 Anand Kumar Agarwal 14-15 Awagarh house Agra AGRA 10 30000 16 Deen Dayal Agarwal 14-15 Awagrah House AGRA 10 30000 17 ANUPMA SINHA 15 Adan Bagh Dayal Dagh Nagala haweli Agra Agra 3 30000 18 Madhu Rani 163, Maharishi puram Agra AGRA 6 30000 19 MAHENDRA KUMAR GARG 18/A/26/31, HANDICRAFT NAGAR, FATEHABAD ROAD AGRA 10 30000 20 SARITA KUMARI BHATNAGAR 186, ELLORA ENCLAVE, DAYALBAGH 100FT ROAD, AGRA 5 30000 21 Dinesh Agarwal -

Hoả Tiễn Siêu Thanh Brahmos

Nhóm Mạng Việt Nam Văn Hiến www.vietnamvanhien.net/org/info/com Hoả Tiễn Siêu Thanh Brahmos Nam Phong tổng hợp Hoả tiễn siêu thanh Brahmos đã được phối trí trên những vị trí chiến lược tại Ấn Độ tháng 11 năm 2006. Brahmos là tên cuả một công ty hổn hợp giữa hai chánh quyền Nga và Ấn sản xuất hoả tiễn để trang bị trên phi cơ, tàu ngầm, tàu nổi và trên đất liền. Với những đặc điểm như sau: Tầm xa: 300km Trọng lượng: 300kgs Đường kính: 600cm Chiều dài: 8.4m, ngắn hơn nếu trang bị trên phi cơ Tốc độ: 2.08 - 3 mach = 50km/phút Giá tiền: 2.73 triệu đô Mỹ mỗi cái 1 Hoả Tiễn Siêu Thanh Brahmos – Nam Phong tổng hợp www.vietnamvanhien.net Brahmos (ảnh cuả cautionindia.com) Brahmos trên đất (ảnh cuả forum.bahrat.com) Brahmos trên phi cơ (ảnh cuả nosint.com) 2 Hoả Tiễn Siêu Thanh Brahmos – Nam Phong tổng hợp www.vietnamvanhien.net Brahmos trên tàu chiến (ảnh cuả nosint.com) Brahmos trong tàu ngầm (ảnh cuả nosint.com) Chi tiết hơn như dưới đây: BrahMos From Wikipedia, the free encyclopedia . BrahMos 3 Hoả Tiễn Siêu Thanh Brahmos – Nam Phong tổng hợp www.vietnamvanhien.net BrahMos and the launch canister on display at the International Maritime Defence Show, IMDS-2007, St. Petersburg, Russia Type Cruise missile Place of origin India/Russia Service history In service November 2006 Used by Indian Army Indian Navy Indian Airforce (awaiting) Production history Manufacturer Joint venture, Federal State Unitary Enterprise NPO Mashinostroeyenia (Russia) and Defence Research and Development Organization (BrahMos Corp, India) Unit cost US$ 2.73 million 4 Hoả Tiễn Siêu Thanh Brahmos – Nam Phong tổng hợp www.vietnamvanhien.net Specifications Weight 3,000 kg 2,500 kg (air-launched) Length 8.4 m Diameter 0.6 m Warhead 300 kg Conventional semi- armour-piercing Engine Two-stage integrated Rocket/Ramjet Operational 290 km range Speed Mach 2.8-3.0[1] Launch Ship, submarine, aircraft and platform land-based mobile launchers. -

ALLAHABAD BANK PERSONNEL ADMINISTRATION DEPARTMENT Head Office: 2 N

ALLAHABAD BANK PERSONNEL ADMINISTRATION DEPARTMENT Head Office: 2 N. S. Road, Kolkata – 700 001 Instruction Circular No. 17302/HO/PA/2019-20/125 Date: 31/03/2020 To All Offices & Branches C I R C U L A R Allotment of new SR number The central government has come out with a scheme called “The Amalgamation of Allahabad Bank into Indian Bank Scheme, 2000” vide notification No. G.S.R. 156 (E) dated 04.03.2020 published in the Gazette of India Extraordinary No.133 dated 04.03.2020, whereby Allahabad Bank is to be amalgamated into Indian Bank w.e.f. 01st April, 2020. In view of the above, all the employees of Allahabad Bank in active service as also those who have retired from Allahabad Bank as on 01.04.2020 have been allotted with NEW SR NUMBER replacing existing Employee No/PF No w.e.f. 01.04.2020. The list of new SR numbers is enclosed in annexure I & II. Annexure-I : SR Number of the employees in active service. Annexure-II : SR Number of the retired employees However, the existing employee No./ PF No. will remain functional till further instruction. All concerned are requested to take a careful note of their respective SR Number as per the Annexure. Hindi version of the circular will follow. (S.K. Suri) General Manager (HR) Annexure-II: SR Number of the retired employees SNO PF_No Pensioner_name New SR No 1 24 P K DASGUPTA 400024 2 46 GANESH PRASAD TANDON 400046 3 57 SHAYAMAL KUMAR SANYAL 400057 4 61 RAM MURAT MISHRA 400061 5 68 RAMESH CHANDRA SRIVASTAVA 400068 6 69 SRI PRAKASH MISHRA 400069 7 71 SUDARSHAN KUMAR KHANNA 400071 8 84 SARAN KUMAR 400084 9 89 CHITTA RANJAN BASU 400089 10 92 DEB KUMAR BANERJEE 400092 11 93 GOPI NATH SETH 400093 12 96 NEMAI CHANDRA DEY 400096 13 100 P N.S. -

Unpaid Warrants 2015-16 Ocps

Cheque No Warrant No Warrant Date Amount NAME ADD1 ADD2 ADD3 CITY PIN Reference No 575 1 7/21/2016 30.00 N VARALAKSHMI DEVI W/O RAMACHANDRA RAO VELIVENNU VIA NIDADAVOL 0 0000000000000N006232 576 2 7/21/2016 6.00 NIMAL CHANDRA SETT G R E/B 3 PO CHANDRAPURA DTGIRIDHA BIHAR0 0 0000000000000N005084 577 3 7/21/2016 6.00 KRISHNAMURTHY INAVOLU S/O RANGAIAH SATULUR POST GUNTUR DIST A P 0 0000000000000K006049 578 4 7/21/2016 6.00 BIPIN NAROTTAMBHAI PATEL PATEL FALIA GOTRI BARODA 0 0000000000000B006209 579 5 7/21/2016 6.00 GOPAL RAMAKUMAR E 29 BHARATHI DASAN SALAI BLOCK 9 NEYVELI 0 0000000000000G001287 580 6 7/21/2016 6.00 KAPOOR CHAND V P D HAYAT NAGAR DIST GURDASPUR PUNJAB0 0 0000000000000K006687 581 7 7/21/2016 6.00 BHAVNA V PATEL PLOT NO .931/2 SECTOR NO.2/C GANDHINAGAR GUJARAT0 0 0000000000000B006325 582 8 7/21/2016 6.00 JYOTSANA KAMLESHKUMAR SHAH AT & POST-SAMNI TA-AMOD DIST-BHARUCH0 0 0000000000000J001291 585 11 7/21/2016 6.00 KANHAIYA LAL SOMANI DEEP PUJAB PLOT NO 60 SECTOR 4 GANDHINAGARCHITTARGARH RAJ 0 0000000000000K007518 586 12 7/21/2016 6.00 KRISHNA KUMARI 1024 BKS MARG NEW DELHI 0 0000000000000K007520 587 13 7/21/2016 6.00 LALIT JANKINATH SAHANI 12 PRERNA BUILDING MANIK NAGAR GANGAPUR ROAD NASIK0 0 0000000000000L000515 588 14 7/21/2016 6.00 NAGINA DEVI JAIN 37 TEJA NAGAR COLONY RATLAM 0 0000000000000N007538 590 16 7/21/2016 6.00 LOVEKESH SHARMA H NO 242 K RALIWAY COLONEY JALANDHARPUR 0 0000000000000L001156 591 17 7/21/2016 132.00 PRANAV KAPOOR P O BOX 5593 DUBAI U A E0 0 0000000000000P000001 592 18 7/21/2016 6.00 SHIVHALA CHANDAK GAURAV -

Zone Wise List of NASI Fellows

The National Academy of Sciences, India (The Oldest Science Academy of India) Zone wise list of Fellows & Honorary Fellows (2021) 5, Lajpatrai Road, Prayagraj – 211002, UP, India 1 The list has been divided into six zones; and each zone is further having the list of scientists of Physical Sciences and Biological Sciences, separately. 2 The National Academy of Sciences, India 5, Lajpatrai Road, Prayagraj – 211002, UP, India Zone wise list of Fellows Zone 1 (Bihar, Jharkhand, Odisha, West Bengal, Meghalaya, Assam, Mizoram, Nagaland, Arunachal Pradesh, Tripura, Manipur and Sikkim) (Section A – Physical Sciences) ACHARYA, Damodar, Chairman, Advisory Board, SOA Deemed to be University, Khandagiri Squre, Bhubanesware - 751030; ACHARYYA, Subhrangsu Kanta, Emeritus Scientist (CSIR), 15, Dr. Sarat Banerjee Road, Kolkata - 700029; ADHIKARI, Satrajit, Sr. Professor of Theoretical Chemistry, School of Chemical Sciences, Indian Association for the Cultivation of Science, 2A & 2B Raja SC Mullick Road, Jadavpur, Kolkata - 700032; ADHIKARI, Sukumar Das, Formerly Professor I, HRI,Ald; Professor & Head, Department of Mathematics, Ramakrishna Mission Vivekananda University, Belur Math, Dist Howrah - 711202; BAISNAB, Abhoy Pada, Formerly Professor of Mathematics, Burdwan Univ.; K-3/6, Karunamayee Estate, Salt Lake, Sector II, Kolkata - 700091; BANDYOPADHYAY, Sanghamitra, Professor & Director, Indian Statistical Institute, 203, BT Road, Kolkata - 700108; BANERJEA, Debabrata, Formerly Sir Rashbehary Ghose Professor of Chemistry,CU; Flat A-4/6,Iswar Chandra Nibas 68/1, Bagmari Road, Kolkata - 700054; BANERJEE, Rabin, Emeritus Professor, SN Bose National Centre for Basic Sciences, Block - JD, Sector - III, Salt Lake, Kolkata - 700098; BANERJEE, Soumitro, Professor, Department of Physical Sciences, Indian Institute of Science Education & Research, Mohanpur Campus, WB 741246; BANERJI, Krishna Dulal, Formerly Professor & Head, Chemistry Department, Flat No.C-2,Ramoni Apartments, A/6, P.G. -

Unpaid Warrants 31.10.2016

Cheque No Warrant No Warrant Date Folio No Amount Beneficiary Name 575 1 21‐Jul‐2016 0000000000000N006232 30.00 N VARALAKSHMI DEVI W O RAMACHANDRA RAO VELIVENNU VIA NIDADA 576 2 21‐Jul‐2016 0000000000000N005084 6.00 NIMAL CHANDRA SETT G R E B 3 PO CHANDRAPURA DTGIRIDHA BIHA 577 3 21‐Jul‐2016 0000000000000K006049 6.00 KRISHNAMURTHY INAVOLU S O RANGAIAH SATULUR POST GUNTUR DIST A 578 4 21‐Jul‐2016 0000000000000B006209 6.00 BIPIN NAROTTAMBHAI PATEL PATEL FALIA GOTRI BARODA 0 0 0 579 5 21‐Jul‐2016 0000000000000G001287 6.00 GOPAL RAMAKUMAR E 29 BHARATHI DASAN SALAI BLOCK 9 NEYVEL 580 6 21‐Jul‐2016 0000000000000K006687 6.00 KAPOOR CHAND V P D HAYAT NAGAR DIST GURDASPUR PUNJAB 581 7 21‐Jul‐2016 0000000000000B006325 6.00 BHAVNA V PATEL PLOT NO 931 2 SECTOR NO 2 C GANDHINAGAR 582 8 21‐Jul‐2016 0000000000000J001291 6.00 JYOTSANA KAMLESHKUMAR SHAH AT AND POST SAMNI TA AMOD DIST BHARUCH 0 0 585 11 21‐Jul‐2016 0000000000000K007518 6.00 KANHAIYA LAL SOMANI DEEP PUJAB PLOT NO 60 SECTOR 4 GANDHINAG 586 12 21‐Jul‐2016 0000000000000K007520 6.00 KRISHNA KUMARI 1024 BKS MARG NEW DELHI 0 0 587 13 21‐Jul‐2016 0000000000000L000515 6.00 LALIT JANKINATH SAHANI 12 PRERNA BUILDING MANIK NAGAR GANGAPUR 588 14 21‐Jul‐2016 0000000000000N007538 6.00 NAGINA DEVI JAIN 37 TEJA NAGAR COLONY RATLAM 0 0 590 16 21‐Jul‐2016 0000000000000L001156 6.00 LOVEKESH SHARMA H NO 242 K RALIWAY COLONEY JALANDHARPUR 591 17 21‐Jul‐2016 0000000000000P000001 132.00 PRANAV KAPOOR P O BOX 5593 DUBAI U A E 0 0 592 18 21‐Jul‐2016 0000000000000S005012 6.00 SHIVHALA CHANDAK GAURAV FARM HOUSE OPP -

Inactive Accounts.Pdf

Sr.No Customer Name Address Operator 1 DAV College, Kanpur 1 ts0,u0 f}osnh 6@36 jktkckx] iqjkuk dkuiqj 2 vkj0ih0 vfXugks=h Mh0,0oh0 b.Vj dkyst dkuiqj 3 ,l0ih0 flag rksej Mh0,0oh0 b.Vj dkyst dkuiqj 4 lqcks/k dqekj 'kqDyk Vkmu ,fj;k f'kojktiqj dkuiqj 5 t;ohj flag 11 vkn'kZ uxj dkyksuh 'kkgtgkiqj 6 fizfUliy vUuiqjh gk;j lsds.Mªh Ldwy lcyiqj iksLV eaxyiqj dkuiqj n;k 'kadj 7 ,ou IyfEcfjax odZ 77@80 dqyh cktkj dkuiqj vrhd vgen 8 us'kuy ckyhcky ,lksfl,'ku 111,@364 v'kksd uxj dkuiqj ds0Mh0 cktisbZ] ,u0Mh0 'kekZ 9 f'kYih phjkdyh laLFkku 128@332] ,p&2 Cykd fdnobZ uxj dkuiqj czts'k dfV;kj] jked`".k xkSM xaxkyh dULVªD'ku 11@309 'kwVjxat dkuiqj Mh0ih0 mRre 10 f'koe~ dkULVªD'ku U;w jk;xat f'kijh cktkj >kWalh jktho oekZ 11 dwij ,syu deZpkjh miHkksDrk lgdkjh lfefr;kWa dwij ,yuxat dkuiqj vks0ih0 jLrksxh 12 efgyk dksvkijsfVo lkbu lkslkbVh VS¶dks dEikm.M dkuiqj pUnz dkUrk pkSjfl;k 1 dksnkbZ yky ehukiqj dkuiqj 2 n;kuUn fo|ky; flfoy ykbUl dkuiqj 3 Mh0,0oh0 dkyst gkLVy 15@64 flfoy ykbUl dkuiqj 4 jktsUnz Lo#i 15@96 flfoy ykbUl dkuiqj 5 izksQslj bUpktZ Mh0,0oh0 dkyst dkuiqj 6 ohjsUnz dqekj vLFkkuk dkuiqj fo'o fo|ky; 7 xzkeks|ksx VªLV iq[kjk;kWa iq[kjk;kWa] dkuiqj 8 jke izlkn 'kekZ Mh0,.0oh0 b.Vj dkyst] dkuiqj 9 jhrk lgk; 111@98 g"kZ uxj dkuiqj 10 loksZn; uxj e.My dkuiqj loksZn; uxj] dkuiqj 11 ch0 izlkn 14@5 flfoy ykbUl dkuiqj 12 fo|kdkUr fodkl uxj dkuiqj 13 y{eh JhokLro ,e0th0 dkyst gkLVy dkuiqj 14 yhfyek eSF;w 112@205 Lo#i uxj dkuiqj 15 Nch ,oa jke pUnz 15@76 ckck?kkV] dkuiqj 16 xksiky 'kadj 15@96 flfoy ykbUl dkuiqj 17 gjh'k pUnz ,oa chuk 72@8 lqrj[kkuk dkuiqj -

MUMBAI 400058 Amount for Unclaimed and Unpaid Dividend 1200.00 06-Nov-2022 2 ROLT0000000000274911 a ARUN 3/24 PETER's RD

ROLTA INDIA LIMITED Statement showing Unpaid/Unclaimed Dividend as on 27th AGM held on 23-09-2017 for the FY ended 2014-15 DUE DATE FOR SR . NO. FOLIO NO DP-ID/CL-ID FIRST NAME MIDDLE NAME LAST NAME ADDRESS PINCODE INVESTMENT TYPE AMOUNT DUE (Rs.) TRANSFER TO IEPF 1 ROLT0000000000062344 A A PARNANDIWAR CHEMOPLAST D-516 CRYSTAL PLAZA NEW LINK ROAD OSHIWARA,ANDHERI (W) MUMBAI 400058 Amount for unclaimed and unpaid dividend 1200.00 06-Nov-2022 2 ROLT0000000000274911 A ARUN 3/24 PETER'S RD. COLONY ROYA PETTAH MADRAS 600014 Amount for unclaimed and unpaid dividend 600.00 06-Nov-2022 3 ROLT0000000000352514 A CHANDRAMOLI CHIEF GENERAL MANAGAR (OPERATIONS) THE TRAVANCORE RAYONS LTD RAYONPURAM,KERALA STATE 683543 Amount for unclaimed and unpaid dividend 300.00 06-Nov-2022 4 ROLT0000000000238384 A CHARLES JOSEPH NO 13 MALIGAI SHOP SOUTH STREET KARAIKUDI PASUMPON DIST TAMIL NADU 623001 Amount for unclaimed and unpaid dividend 600.00 06-Nov-2022 5 ROLT0000000000330869 A D KODILKAR 58 R NO 1861 NEHRUNAGAR KURLA (EAST) MUMBAI 400024 Amount for unclaimed and unpaid dividend 1800.00 06-Nov-2022 6 IN300159-10005475-0000 A D SPATHY 29 WAHAB STREET CHOOLAIMEDU CHENNAI. 600094 Amount for unclaimed and unpaid dividend 540.00 06-Nov-2022 7 ROLT0000000000055096 A GOPINATH KURUP 318 / 01 AMBALAMEDU P.O. KOCHI 682303 Amount for unclaimed and unpaid dividend 600.00 06-Nov-2022 8 ROLT0000000000067397 A H VSSUDHAKAR THE FEDERAL BANK LTD HOTEL DWARAKA COMPLEX LAKDIKA POOL HYDERABAD 500004 Amount for unclaimed and unpaid dividend 300.00 06-Nov-2022 9 IN300610-10103975-0000 A JAIRAM GUPTA 'ANNAPURNESWARI NILAYA' GANDHI NAGAR NEAR MUNICIPAL PARK, CHELLAKERE CHITRADURGA DIST. -

MGT 7 FY 2017-18 Attachment-4

Dp/client_ID NAME_OF_HOLDER FH_NAME ADDRESS CITY STATE PINCODE TY HOLD FV 000182 SHARMILA JAIN H L JAIN C/O KANWARLAL PUKHRAJ MUKIMMUK 1 165 0010 000766 PRERNA H HIRANANDANI HARESH B-3 SHANTI KUNJOPP G P OPUNE 1 50 0010 A01826 AJAI KUMAR BHANSALI MAGHRAJ BHANSALI KUSHAL DEEP16/553, CHOPASNI HO 1 150 0010 A13727 ASHOK GUPTA JAGDISH GUPTA C/O DEEP BUILDING MATERIAL STO 1 247 0010 A14224 ASHOK SHAMRAO JADHAV SHAMRAO JADHAV C/O M/S NEW INDIA MOTORS1036 ' 1 15 0010 B00075 BHAGIRATHI GOPE JAGANNATH GOPE C/O SMT SUMITRA GOPE34 KHASMAH 1 50 0010 B02039 BASUDHARA MAJUMDER ANJAN KUMAR MAJUMDER 5261 123RD AVENUE SEBELLEUEWA 1 50 0010 C01805 CHENCHERI ARUMUGHAN CHENCHERI SANKARAN LOAD CONTROLLERFLIGHT OPERETIO 1 150 0010 C01931 CONSTANTINA F A DMELLO TREVOR DMELLO 4294 SUGARBUSH ROADMISSISSAUGA 1 25 0010 D00054 DHARAMVIR DALAL BUDH RAM DALAL C/O M/S BHARAT PETROLEUM CORP. 1 150 0010 D13647 DINESH K KUNVARJIBHAI DISPUTE CASE 1 200 0010 D13693 DUSHYANT VYAS SHANTUKUMAR VYAS SHANTI NIKETANA/29 VIHAR KUNJ 1 100 0010 F01836 FAUZIA SAMI KIDWAI ZAHIN UDDIN KIDWAI C/O MR Z D KIDWAIMINISTRY OF E 1 150 0010 G12996 G PARAMESHWARA REDDY G ESWARA REDDY H NO 365SOUTH END PARKL B NAGA 1 247 0010 G13002 G PARAMESHWARA REDDY G ESWARA REDDY H NO 365SOUTH END PARKL B NAGA 1 247 0010 H12522 H C NAGARAJA H CHANDRASHEKHARAPPA D NO 2440/3 CHANDRA SADANA(NEA 1 247 0010 J01815 JANARDANAN KYLA VALAPPIL NIL KYLA VALAPPIL HOUSENEAR OLADAT 1 150 0010 J02061 JITENDRA R GHIA RAICHAND T GHIA 1570 LABURNUM ROADHOFFMAN ESTA 1 147 0010 K01813 KOSHY KURIEN NIL CHAVADIYIL HOUSEKADAMANKULAM -

State Subsidy Distribution List Till Date

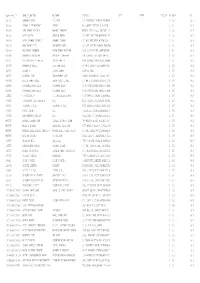

LIST OF BENEFICIARIES WHOSE STATE SUBSIDY HA BEEN DISTRIBUTED BY UPNEDA TILL DATE Capacity Plant SFA Disbursed S.NO. Application ID Beneficiary Name Installation Address District Mobile no. Firm Name Installed Commissioni (Rs) 1 15439956271752 Gur Prasad Saini 118, AGRA 9997431806 5 23/01/19 Shiva Bio Gas Agency 30000 2 1535461559757 Madhu Rani 163, Maharishi puram Agra AGRA 8958106666 6 26/11/18 Arna Energies Pvt Ltd 30000 3 15378570211041 Naredla Hazur saran 21,Radha Nagar, Dayal bagh AGRA 8909662229 2 23/01/19 Shiva Bio Gas Agency 30000 4 1532970935245 AMRISH PRAKASH GAUR 22 TULSI VIHAR DAYAL BAGH AGRA 7599259882 2 22/01/19 Shiva Bio Gas Agency 30000 5 1535622455779 Rekha Yadav 28, Tagore Nagar, Dayal Bagh Agra AGRA 9837121787 5 18/05/18 Arna Energies Pvt Ltd 30000 6 153242945546 Vandana Maheshwari 32,Shanta kunj dayal bagh Agra AGRA 9407050015 5 21/08/18 Arna Energies Pvt Ltd 30000 7 15378627941042 Trilok Kumar Gupta 45, Laxmi Nagar, Sikandra Agra AGRA 9599699155 5 03/07/18 Arna Energies Pvt Ltd 30000 8 1536739019899 Praveendra kumar yadav 506 Kaveri Gold Khandari Agra AGRA 7983025129 7 04/10/18 Arna Energies Pvt Ltd 30000 9 153243079648 Girish Narain Gupta E-203 Kamla Nagar AGRA 7500202200 10 03/12/18 Sunshade Energy Pvt. 30000 10 1532780194207 Rohit Nayyar E-25 New Agra New Agra AGRA AGRA 8077429207 10 18/05/18 Arna Energies Pvt Ltd 30000 11 15437286181677 SANGITA SAINI ELLORA ENCLAVE AGRA 9897289879 5 23/01/19 Shiva Bio Gas Agency 30000 12 15445188851847 ALPNA MATHUR FF-3,Plot no. -

(1954-2014) Year-Wise List 1954

MINISTRY OF HOME AFFAIRS (Public Section) Padma Awards Directory (1954-2014) Year-Wise List Sl. Prefix First Name Last Name Award State Field 1954 1 Dr. Sarvapalli Radhakrishnan BR TN Public Affairs 2 Shri Chakravarti Rajagopalachari BR TN Public Affairs 3 Shri Chandrasekhara Raman BR TN Science & Venkata 4 Dr. Satyendra Nath Bose PV WB Litt. & Edu. 5 Shri Nandlal Bose PV WB Art 6 Dr. Zakir Husain PV AP Public Affairs 7 Shri Bal Gangadhar Kher PV MAH Public Affairs 8 Shri V.K. Krishna Menon PV KER Public Affairs 9 Shri Jigme Dorji Wangchuk PV BHU Public Affairs 10 Dr. Homi Jehangir Bhabha PB MAH Science & 11 Dr. Shanti Swarup Bhatnagar PB UP Science & 12 Shri Mahadeva Iyer Ganapati PB OR Civil Service 13 Dr. Jnan Chandra Ghosh PB WB Science & 14 Shri Radha Krishna Gupta PB DEL Civil Service 15 Shri Maithilisharan Gupta PB UP Litt. & Edu. 16 Shri R.R. Handa PB PUN Civil Service 17 Shri Amarnath Jha PB UP Litt. & Edu. 21 May 2014 Page 1 of 193 Sl. Prefix First Name Last Name Award State Field 18 Shri Ajudhia Nath Khosla PB DEL Science & 19 Dr. K.S. Krishnan PB TN Science & 20 Shri Moulana Hussain Madni PB PUN Litt. & Edu. Ahmad 21 Shri Josh Malihabadi PB DEL Litt. & Edu. 22 Shri V.L. Mehta PB GUJ Public Affairs 23 Shri Vallathol Narayan Menon PB KER Litt. & Edu. 24 Dr. Arcot Mudaliar PB TN Litt. & Edu. Lakshamanaswami 25 Lt. (Col) Maharaj Kr. Palden T Namgyal PB PUN Public Affairs 26 Shri V. Narahari Raooo PB KAR Civil Service 27 Shri Pandyala Rau PB AP Civil Service Satyanarayana 28 Shri Jamini Roy PB WB Art 29 Shri Sukumar Sen PB WB Civil Service 30 Shri Satya Narayana Shastri PB UP Medicine 31 Late Smt.