REVSTAT No 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BIOGRAPHICAL SKETCH Garrett M. Fitzmaurice Associate Professor Of

Principal Investigator/Program Director (Last, First, Middle): BIOGRAPHICAL SKETCH Provide the following information for the key personnel and other significant contributors in the order listed on Form Page 2. Follow this format for each person. DO NOT EXCEED FOUR PAGES. NAME POSITION TITLE Garrett M. Fitzmaurice Associate Professor of Biostatistics eRA COMMONS USER NAME EDUCATION/TRAINING (Begin with baccalaureate or other initial professional education, such as nursing, and include postdoctoral training.) DEGREE INSTITUTION AND LOCATION YEAR(s) FIELD OF STUDY (if applicable) National University of Ireland BA, MA 1983, 1987 Psychology University of London MSc 1986 Quantitative Methods Harvard University ScD 1993 Biostatistics Professional Experience: 1986-1989 Statistician, Department of Psychology, New York University 1989-1990 Teaching Assistant, Department of Biostatistics, Harvard School of Public Health 1990-1993 Teaching Fellow in Biostatistics, Department of Biostatistics, Harvard SPH 1993-1994 Post-doctoral Research Fellow, Department of Biostatistics, Harvard SPH 1994-1997 Research Fellow, Nuffield College, Oxford University, United Kingdom 1997-1999 Assistant Professor of Biostatistics, Harvard School of Public Health 1999-present Associate Professor of Biostatistics, Harvard School of Public Health 2004-present Associate Professor of Medicine (Biostatistics), Harvard Medical School 2004-present Biostatistician, Division of General Medicine, Brigham and Women’s Hospital, Boston 2006-present Foreign Adjunct Professor of Biostatistics, -

TUTORIAL in BIOSTATISTICS: the Self-Controlled Case Series Method

STATISTICS IN MEDICINE Statist. Med. 2005; 0:1–31 Prepared using simauth.cls [Version: 2002/09/18 v1.11] TUTORIAL IN BIOSTATISTICS: The self-controlled case series method Heather J. Whitaker1, C. Paddy Farrington1, Bart Spiessens2 and Patrick Musonda1 1 Department of Statistics, The Open University, Milton Keynes, MK7 6AA, UK. 2 GlaxoSmithKline Biologicals, Rue de l’Institut 89, B-1330 Rixensart, Belgium. SUMMARY The self-controlled case series method was developed to investigate associations between acute outcomes and transient exposures, using only data on cases, that is, on individuals who have experienced the outcome of interest. Inference is within individuals, and hence fixed covariates effects are implicitly controlled for within a proportional incidence framework. We describe the origins, assumptions, limitations, and uses of the method. The rationale for the model and the derivation of the likelihood are explained in detail using a worked example on vaccine safety. Code for fitting the model in the statistical package STATA is described. Two further vaccine safety data sets are used to illustrate a range of modelling issues and extensions of the basic model. Some brief pointers on the design of case series studies are provided. The data sets, STATA code, and further implementation details in SAS, GENSTAT and GLIM are available from an associated website. key words: case series; conditional likelihood; control; epidemiology; modelling; proportional incidence Copyright c 2005 John Wiley & Sons, Ltd. 1. Introduction The self-controlled case series method, or case series method for short, provides an alternative to more established cohort or case-control methods for investigating the association between a time-varying exposure and an outcome event. -

Alberto Abadie

ALBERTO ABADIE Office Address Massachusetts Institute of Technology Department of Economics 50 Memorial Drive Building E52, Room 546 Cambridge, MA 02142 E-mail: [email protected] Academic Positions Massachusetts Institute of Technology Cambridge, MA Professor of Economics, 2016-present IDSS Associate Director, 2016-present Harvard University Cambridge, MA Professor of Public Policy, 2005-2016 Visiting Professor of Economics, 2013-2014 Associate Professor of Public Policy, 2004-2005 Assistant Professor of Public Policy, 1999-2004 University of Chicago Chicago, IL Visiting Assistant Professor of Economics, 2002-2003 National Bureau of Economic Research (NBER) Cambridge, MA Research Associate (Labor Studies), 2009-present Faculty Research Fellow (Labor Studies), 2002-2009 Non-Academic Positions Amazon.com, Inc. Seattle, WA Academic Research Consultant, 2020-present Education Massachusetts Institute of Technology Cambridge, MA Ph.D. in Economics, 1995-1999 Thesis title: \Semiparametric Instrumental Variable Methods for Causal Response Mod- els." Centro de Estudios Monetarios y Financieros (CEMFI) Madrid, Spain M.A. in Economics, 1993-1995 Masters Thesis title: \Changes in Spanish Labor Income Structure during the 1980's: A Quantile Regression Approach." 1 Universidad del Pa´ıs Vasco Bilbao, Spain B.A. in Economics, 1987-1992 Specialization Areas: Mathematical Economics and Econometrics. Honors and Awards Elected Fellow of the Econometric Society, 2016. NSF grant SES-1756692, \A General Synthetic Control Framework of Estimation and Inference," 2018-2021. NSF grant SES-0961707, \A General Theory of Matching Estimation," with G. Imbens, 2010-2012. NSF grant SES-0617810, \The Economic Impact of Terrorism: Lessons from the Real Estate Office Markets of New York and Chicago," with S. Dermisi, 2006-2008. -

Miguel De Carvalho

School of Mathematics Miguel de Carvalho Contact M. de Carvalho T: +44 (0) 0131 650 5054 Information The University of Edinburgh B: [email protected] School of Mathematics : mb.carvalho Edinburgh EH9 3FD, UK +: www.maths.ed.ac.uk/ mdecarv Personal Born September 20, 1980 in Montijo, Lisbon. Details Portuguese and EU citizenship. Interests Applied Statistics, Biostatistics, Econometrics, Risk Analysis, Statistics of Extremes. Education Universidade de Lisboa, Portugal Habilitation in Probability and Statistics, 2019 Thesis: Statistical Modeling of Extremes Universidade Nova de Lisboa, Portugal PhD in Mathematics with emphasis on Statistics, 2009 Thesis: Extremum Estimators and Stochastic Optimization Advisors: Manuel Esqu´ıvel and Tiago Mexia Advisors of Advisors: Jean-Pierre Kahane and Tiago de Oliveira. Nova School of Business and Economics (Triple Accreditation), Portugal MSc in Economics, 2009 Thesis: Mean Regression for Censored Length-Biased Data Advisors: Jos´eA. F. Machado and Pedro Portugal Advisors of Advisors: Roger Koenker and John Addison. Universidade Nova de Lisboa, Portugal `Licenciatura'y in Mathematics, 2004 Professional Probation Period: Statistics Portugal (Instituto Nacional de Estat´ıstica). Awards & ISBA (International Society for Bayesian Analysis) Honours Lindley Award, 2019. TWAS (Academy of Sciences for the Developing World) Young Scientist Prize, 2015. International Statistical Institute Elected Member, 2014. American Statistical Association Young Researcher Award, Section on Risk Analysis, 2011. National Institute of Statistical Sciences j American Statistical Association Honorary Mention as a Finalist NISS/ASA Best y-BIS Paper Award, 2010. Portuguese Statistical Society (Sociedade Portuguesa de Estat´ıstica) Young Researcher Award, 2009. International Association for Statistical Computing ERS IASC Young Researcher Award, 2008. 1 of 13 p l e t t si a o e igulctoson Applied Statistical ModelingPublications 1. -

Biometrics & Biostatistics

Hanley and Moodie, J Biomet Biostat 2011, 2:5 Biometrics & Biostatistics http://dx.doi.org/10.4172/2155-6180.1000124 Research Article Article OpenOpen Access Access Sample Size, Precision and Power Calculations: A Unified Approach James A Hanley* and Erica EM Moodie Department of Epidemiology, Biostatistics, and Occupational Health, McGill University, Canada Abstract The sample size formulae given in elementary biostatistics textbooks deal only with simple situations: estimation of one, or a comparison of at most two, mean(s) or proportion(s). While many specialized textbooks give sample formulae/tables for analyses involving odds and rate ratios, few deal explicitly with statistical considera tions for slopes (regression coefficients), for analyses involving confounding variables or with the fact that most analyses rely on some type of generalized linear model. Thus, the investigator is typically forced to use “black-box” computer programs or tables, or to borrow from tables in the social sciences, where the emphasis is on cor- relation coefficients. The concern in the – usually very separate – modules or stand alone software programs is more with user friendly input and output. The emphasis on numerical exactness is particularly unfortunate, given the rough, prospective, and thus uncertain, nature of the exercise, and that different textbooks and software may give different sample sizes for the same design. In addition, some programs focus on required numbers per group, others on an overall number. We present users with a single universal (though sometimes approximate) formula that explicitly isolates the impacts of the various factors one from another, and gives some insight into the determinants for each factor. -

JEROME P. REITER Department of Statistical Science, Duke University Box 90251, Durham, NC 27708 Phone: 919 668 5227

JEROME P. REITER Department of Statistical Science, Duke University Box 90251, Durham, NC 27708 phone: 919 668 5227. email: [email protected]. September 26, 2021 EDUCATION Ph.D. in Statistics, Harvard University, 1999. A.M. in Statistics, Harvard University, 1996. B.S. in Mathematics, Duke University, 1992. DISSERTATION \Estimation in the Presence of Constraints that Prohibit Explicit Data Pooling." Advisor: Donald B. Rubin. POSITIONS Academic Appointments Professor of Statistical Science and Bass Fellow, Duke University, 2015 - present. Mrs. Alexander Hehmeyer Professor of Statistical Science, Duke University, 2013 - 2015. Mrs. Alexander Hehmeyer Associate Professor of Statistical Science, Duke University, 2010 - 2013. Associate Professor of Statistical Science, Duke University, 2009 - 2010. Assistant Professor of Statistical Science, Duke University, 2006 - 2008. Assistant Professor of the Practice of Statistics and Decision Sciences, Duke University, 2002 - 2006. Lecturer in Statistics, University of California at Santa Barbara, 2001 - 2002. Assistant Professor of Statistics, Williams College, 1999 - 2001. Other Appointments Chair, Department of Statistical Science, Duke University, 2019 - present. Associate Chair, Department of Statistical Science, Duke University, 2016 - 2019. Mathematical Statistician (part-time), U. S. Bureau of the Census, 2015 - present. Associate/Deputy Director of Information Initiative at Duke, Duke University, 2013 - 2019. Social Sciences Research Institute Data Services Core Director, Duke University, 2010 - 2013. Interim Director, Triangle Research Data Center, 2006. Senior Fellow, National Institute of Statistical Sciences, 2002 - 2005. 1 ACADEMIC HONORS Keynote talk, 11th Official Statistics and Methodology Symposium (Statistics Korea), 2021. Fellow of the Institute of Mathematical Statistics, 2020. Clifford C. Clogg Memorial Lecture, Pennsylvania State University, 2020 (postponed due to covid-19). -

The American Statistician

This article was downloaded by: [T&F Internal Users], [Rob Calver] On: 01 September 2015, At: 02:24 Publisher: Taylor & Francis Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: 5 Howick Place, London, SW1P 1WG The American Statistician Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/utas20 Reviews of Books and Teaching Materials Published online: 27 Aug 2015. Click for updates To cite this article: (2015) Reviews of Books and Teaching Materials, The American Statistician, 69:3, 244-252, DOI: 10.1080/00031305.2015.1068616 To link to this article: http://dx.doi.org/10.1080/00031305.2015.1068616 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of information. Taylor and Francis shall not be liable for any losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoever or howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use of the Content. This article may be used for research, teaching, and private study purposes. -

Visualizing Research Collaboration in Statistical Science: a Scientometric

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Library Philosophy and Practice (e-journal) Libraries at University of Nebraska-Lincoln 9-13-2019 Visualizing Research Collaboration in Statistical Science: A Scientometric Perspective Prabir Kumar Das Library, Documentation & Information Science Division, Indian Statistical Institute, 203 B T Road, Kolkata - 700108, [email protected] Follow this and additional works at: https://digitalcommons.unl.edu/libphilprac Part of the Library and Information Science Commons Das, Prabir Kumar, "Visualizing Research Collaboration in Statistical Science: A Scientometric Perspective" (2019). Library Philosophy and Practice (e-journal). 3039. https://digitalcommons.unl.edu/libphilprac/3039 Viisualliiziing Research Collllaborattiion iin Sttattiisttiicall Sciience:: A Sciienttomettriic Perspecttiive Prrabiirr Kumarr Das Sciienttiiffiic Assssiissttantt – A Liibrrarry,, Documenttattiion & IInfforrmattiion Sciience Diiviisiion,, IIndiian Sttattiisttiicall IInsttiittutte,, 203,, B.. T.. Road,, Kollkatta – 700108,, IIndiia,, Emaiill:: [email protected] Abstract Using Sankhyā – The Indian Journal of Statistics as a case, present study aims to identify scholarly collaboration pattern of statistical science based on research articles appeared during 2008 to 2017. This is an attempt to visualize and quantify statistical science research collaboration in multiple dimensions by exploring the co-authorship data. It investigates chronological variations of collaboration pattern, nodes and links established among the affiliated institutions and countries of all contributing authors. The study also examines the impact of research collaboration on citation scores. Findings reveal steady influx of statistical publications with clear tendency towards collaborative ventures, of which double-authored publications dominate. Small team of 2 to 3 authors is responsible for production of majority of collaborative research, whereas mega-authored communications are quite low. -

Abbreviations of Names of Serials

Abbreviations of Names of Serials This list gives the form of references used in Mathematical Reviews (MR). ∗ not previously listed E available electronically The abbreviation is followed by the complete title, the place of publication § journal reviewed cover-to-cover V videocassette series and other pertinent information. † monographic series ¶ bibliographic journal E 4OR 4OR. Quarterly Journal of the Belgian, French and Italian Operations Research ISSN 1211-4774. Societies. Springer, Berlin. ISSN 1619-4500. §Acta Math. Sci. Ser. A Chin. Ed. Acta Mathematica Scientia. Series A. Shuxue Wuli † 19o Col´oq. Bras. Mat. 19o Col´oquio Brasileiro de Matem´atica. [19th Brazilian Xuebao. Chinese Edition. Kexue Chubanshe (Science Press), Beijing. (See also Acta Mathematics Colloquium] Inst. Mat. Pura Apl. (IMPA), Rio de Janeiro. Math.Sci.Ser.BEngl.Ed.) ISSN 1003-3998. † 24o Col´oq. Bras. Mat. 24o Col´oquio Brasileiro de Matem´atica. [24th Brazilian §ActaMath.Sci.Ser.BEngl.Ed. Acta Mathematica Scientia. Series B. English Edition. Mathematics Colloquium] Inst. Mat. Pura Apl. (IMPA), Rio de Janeiro. Science Press, Beijing. (See also Acta Math. Sci. Ser. A Chin. Ed.) ISSN 0252- † 25o Col´oq. Bras. Mat. 25o Col´oquio Brasileiro de Matem´atica. [25th Brazilian 9602. Mathematics Colloquium] Inst. Nac. Mat. Pura Apl. (IMPA), Rio de Janeiro. § E Acta Math. Sin. (Engl. Ser.) Acta Mathematica Sinica (English Series). Springer, † Aastaraam. Eesti Mat. Selts Aastaraamat. Eesti Matemaatika Selts. [Annual. Estonian Heidelberg. ISSN 1439-8516. Mathematical Society] Eesti Mat. Selts, Tartu. ISSN 1406-4316. § E Acta Math. Sinica (Chin. Ser.) Acta Mathematica Sinica. Chinese Series. Chinese Math. Abh. Braunschw. Wiss. Ges. Abhandlungen der Braunschweigischen Wissenschaftlichen Soc., Acta Math. -

Causality: Readings in Statistics and Econometrics Hedibert F

Causality: Readings in Statistics and Econometrics Hedibert F. Lopes, INSPER http://www.hedibert.org/current-teaching/#tab-causality Annotated Bibliography 1 Articles 1. Angrist and Imbens (1995) Two-Stage Least Squares Estimation of Average Causal Effects in Models With Variable Treatment Intensity. JASA, 90, 431-442. 2. Angrist and Krueger (1991) Does compulsory school attendance affect earnings? Quarterly Journal of Economic, 106, 979-1019. 3. Angrist, Imbens and Rubin (1996) Identification of causal effects using instrumental variables (with discussion). JASA, 91, 444-472. 4. Athey and Imbens (2015) Machine Learning Methods for Estimating Heterogeneous Causal Effects. 5. Balke and Pearl (1995). Counterfactuals and policy analysis in structural models. In Besnard and Hanks, Eds., Uncertainty in Artificial Intelligence, Proceedings of the Eleventh Conference. Morgan Kaufmann, San Francisco, 11-18. 6. Bareinboim and Pearl (2015) Causal inference from big data: Theoretical foundations and the data-fusion problem. Proceedings of the National Academy of Sciences. 7. Bollen and Pearl (2013) Eight myths about causality and structural equation models. In Morgan (Ed.) Handbook of Causal Analysis for Social Research, Chapter 15, 301-328. Springer. 8. Bound, Jaeger, and Baker (1995) Problems with Instrumental Variables Estimation when the Correlation Be- tween the Instruments and the Endogenous Regressors is Weak. JASA, 90, 443-450. 9. Brito and Pearl (2002) Generalized instrumental variables. In Darwiche and Friedman, Eds. Uncertainty in Artificial Intelligence, Proceedings of the Eighteenth Conference. Morgan Kaufmann, San Francisco, 85-93. 10. Brzeski, Taddy and raper (2015) Causal Inference in Repeated Observational Studies: A Case Study of eBay Product Releases. arXiv:1509.03940v1. 11. Chambaz, Drouet and Thalabard (2014) Causality, a Trialogue. -

Can P-Values Be Meaningfully Interpreted Without Random Sampling?

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Hirschauer, Norbert; Grüner, Sven; Mußhoff, Oliver; Becker, Claudia; Jantsch, Antje Article — Published Version Can p-values be meaningfully interpreted without random sampling? Statistics Surveys Provided in Cooperation with: Leibniz Institute of Agricultural Development in Transition Economies (IAMO), Halle (Saale) Suggested Citation: Hirschauer, Norbert; Grüner, Sven; Mußhoff, Oliver; Becker, Claudia; Jantsch, Antje (2020) : Can p-values be meaningfully interpreted without random sampling?, Statistics Surveys, ISSN 1935-7516, Cornell University Library, Ithaca, NY, Vol. 14, pp. 71-91, http://dx.doi.org/10.1214/20-SS129 , https://projecteuclid.org/euclid.ssu/1585274548 This Version is available at: http://hdl.handle.net/10419/215709 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

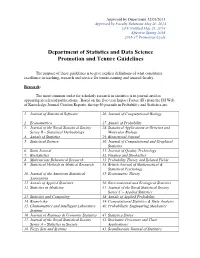

Department of Statistics and Data Science Promotion and Tenure Guidelines

Approved by Department 12/05/2013 Approved by Faculty Relations May 20, 2014 UFF Notified May 21, 2014 Effective Spring 2016 2016-17 Promotion Cycle Department of Statistics and Data Science Promotion and Tenure Guidelines The purpose of these guidelines is to give explicit definitions of what constitutes excellence in teaching, research and service for tenure-earning and tenured faculty. Research: The most common outlet for scholarly research in statistics is in journal articles appearing in refereed publications. Based on the five-year Impact Factor (IF) from the ISI Web of Knowledge Journal Citation Reports, the top 50 journals in Probability and Statistics are: 1. Journal of Statistical Software 26. Journal of Computational Biology 2. Econometrica 27. Annals of Probability 3. Journal of the Royal Statistical Society 28. Statistical Applications in Genetics and Series B – Statistical Methodology Molecular Biology 4. Annals of Statistics 29. Biometrical Journal 5. Statistical Science 30. Journal of Computational and Graphical Statistics 6. Stata Journal 31. Journal of Quality Technology 7. Biostatistics 32. Finance and Stochastics 8. Multivariate Behavioral Research 33. Probability Theory and Related Fields 9. Statistical Methods in Medical Research 34. British Journal of Mathematical & Statistical Psychology 10. Journal of the American Statistical 35. Econometric Theory Association 11. Annals of Applied Statistics 36. Environmental and Ecological Statistics 12. Statistics in Medicine 37. Journal of the Royal Statistical Society Series C – Applied Statistics 13. Statistics and Computing 38. Annals of Applied Probability 14. Biometrika 39. Computational Statistics & Data Analysis 15. Chemometrics and Intelligent Laboratory 40. Probabilistic Engineering Mechanics Systems 16. Journal of Business & Economic Statistics 41.