Miguel De Carvalho

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Alberto Abadie

ALBERTO ABADIE Office Address Massachusetts Institute of Technology Department of Economics 50 Memorial Drive Building E52, Room 546 Cambridge, MA 02142 E-mail: [email protected] Academic Positions Massachusetts Institute of Technology Cambridge, MA Professor of Economics, 2016-present IDSS Associate Director, 2016-present Harvard University Cambridge, MA Professor of Public Policy, 2005-2016 Visiting Professor of Economics, 2013-2014 Associate Professor of Public Policy, 2004-2005 Assistant Professor of Public Policy, 1999-2004 University of Chicago Chicago, IL Visiting Assistant Professor of Economics, 2002-2003 National Bureau of Economic Research (NBER) Cambridge, MA Research Associate (Labor Studies), 2009-present Faculty Research Fellow (Labor Studies), 2002-2009 Non-Academic Positions Amazon.com, Inc. Seattle, WA Academic Research Consultant, 2020-present Education Massachusetts Institute of Technology Cambridge, MA Ph.D. in Economics, 1995-1999 Thesis title: \Semiparametric Instrumental Variable Methods for Causal Response Mod- els." Centro de Estudios Monetarios y Financieros (CEMFI) Madrid, Spain M.A. in Economics, 1993-1995 Masters Thesis title: \Changes in Spanish Labor Income Structure during the 1980's: A Quantile Regression Approach." 1 Universidad del Pa´ıs Vasco Bilbao, Spain B.A. in Economics, 1987-1992 Specialization Areas: Mathematical Economics and Econometrics. Honors and Awards Elected Fellow of the Econometric Society, 2016. NSF grant SES-1756692, \A General Synthetic Control Framework of Estimation and Inference," 2018-2021. NSF grant SES-0961707, \A General Theory of Matching Estimation," with G. Imbens, 2010-2012. NSF grant SES-0617810, \The Economic Impact of Terrorism: Lessons from the Real Estate Office Markets of New York and Chicago," with S. Dermisi, 2006-2008. -

Abbreviations of Names of Serials

Abbreviations of Names of Serials This list gives the form of references used in Mathematical Reviews (MR). ∗ not previously listed E available electronically The abbreviation is followed by the complete title, the place of publication § journal reviewed cover-to-cover V videocassette series and other pertinent information. † monographic series ¶ bibliographic journal E 4OR 4OR. Quarterly Journal of the Belgian, French and Italian Operations Research ISSN 1211-4774. Societies. Springer, Berlin. ISSN 1619-4500. §Acta Math. Sci. Ser. A Chin. Ed. Acta Mathematica Scientia. Series A. Shuxue Wuli † 19o Col´oq. Bras. Mat. 19o Col´oquio Brasileiro de Matem´atica. [19th Brazilian Xuebao. Chinese Edition. Kexue Chubanshe (Science Press), Beijing. (See also Acta Mathematics Colloquium] Inst. Mat. Pura Apl. (IMPA), Rio de Janeiro. Math.Sci.Ser.BEngl.Ed.) ISSN 1003-3998. † 24o Col´oq. Bras. Mat. 24o Col´oquio Brasileiro de Matem´atica. [24th Brazilian §ActaMath.Sci.Ser.BEngl.Ed. Acta Mathematica Scientia. Series B. English Edition. Mathematics Colloquium] Inst. Mat. Pura Apl. (IMPA), Rio de Janeiro. Science Press, Beijing. (See also Acta Math. Sci. Ser. A Chin. Ed.) ISSN 0252- † 25o Col´oq. Bras. Mat. 25o Col´oquio Brasileiro de Matem´atica. [25th Brazilian 9602. Mathematics Colloquium] Inst. Nac. Mat. Pura Apl. (IMPA), Rio de Janeiro. § E Acta Math. Sin. (Engl. Ser.) Acta Mathematica Sinica (English Series). Springer, † Aastaraam. Eesti Mat. Selts Aastaraamat. Eesti Matemaatika Selts. [Annual. Estonian Heidelberg. ISSN 1439-8516. Mathematical Society] Eesti Mat. Selts, Tartu. ISSN 1406-4316. § E Acta Math. Sinica (Chin. Ser.) Acta Mathematica Sinica. Chinese Series. Chinese Math. Abh. Braunschw. Wiss. Ges. Abhandlungen der Braunschweigischen Wissenschaftlichen Soc., Acta Math. -

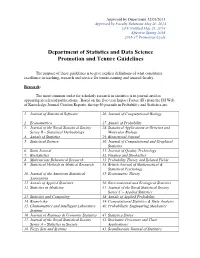

Department of Statistics and Data Science Promotion and Tenure Guidelines

Approved by Department 12/05/2013 Approved by Faculty Relations May 20, 2014 UFF Notified May 21, 2014 Effective Spring 2016 2016-17 Promotion Cycle Department of Statistics and Data Science Promotion and Tenure Guidelines The purpose of these guidelines is to give explicit definitions of what constitutes excellence in teaching, research and service for tenure-earning and tenured faculty. Research: The most common outlet for scholarly research in statistics is in journal articles appearing in refereed publications. Based on the five-year Impact Factor (IF) from the ISI Web of Knowledge Journal Citation Reports, the top 50 journals in Probability and Statistics are: 1. Journal of Statistical Software 26. Journal of Computational Biology 2. Econometrica 27. Annals of Probability 3. Journal of the Royal Statistical Society 28. Statistical Applications in Genetics and Series B – Statistical Methodology Molecular Biology 4. Annals of Statistics 29. Biometrical Journal 5. Statistical Science 30. Journal of Computational and Graphical Statistics 6. Stata Journal 31. Journal of Quality Technology 7. Biostatistics 32. Finance and Stochastics 8. Multivariate Behavioral Research 33. Probability Theory and Related Fields 9. Statistical Methods in Medical Research 34. British Journal of Mathematical & Statistical Psychology 10. Journal of the American Statistical 35. Econometric Theory Association 11. Annals of Applied Statistics 36. Environmental and Ecological Statistics 12. Statistics in Medicine 37. Journal of the Royal Statistical Society Series C – Applied Statistics 13. Statistics and Computing 38. Annals of Applied Probability 14. Biometrika 39. Computational Statistics & Data Analysis 15. Chemometrics and Intelligent Laboratory 40. Probabilistic Engineering Mechanics Systems 16. Journal of Business & Economic Statistics 41. -

Rank Full Journal Title Journal Impact Factor 1 Journal of Statistical

Journal Data Filtered By: Selected JCR Year: 2019 Selected Editions: SCIE Selected Categories: 'STATISTICS & PROBABILITY' Selected Category Scheme: WoS Rank Full Journal Title Journal Impact Eigenfactor Total Cites Factor Score Journal of Statistical Software 1 25,372 13.642 0.053040 Annual Review of Statistics and Its Application 2 515 5.095 0.004250 ECONOMETRICA 3 35,846 3.992 0.040750 JOURNAL OF THE AMERICAN STATISTICAL ASSOCIATION 4 36,843 3.989 0.032370 JOURNAL OF THE ROYAL STATISTICAL SOCIETY SERIES B-STATISTICAL METHODOLOGY 5 25,492 3.965 0.018040 STATISTICAL SCIENCE 6 6,545 3.583 0.007500 R Journal 7 1,811 3.312 0.007320 FUZZY SETS AND SYSTEMS 8 17,605 3.305 0.008740 BIOSTATISTICS 9 4,048 3.098 0.006780 STATISTICS AND COMPUTING 10 4,519 3.035 0.011050 IEEE-ACM Transactions on Computational Biology and Bioinformatics 11 3,542 3.015 0.006930 JOURNAL OF BUSINESS & ECONOMIC STATISTICS 12 5,921 2.935 0.008680 CHEMOMETRICS AND INTELLIGENT LABORATORY SYSTEMS 13 9,421 2.895 0.007790 MULTIVARIATE BEHAVIORAL RESEARCH 14 7,112 2.750 0.007880 INTERNATIONAL STATISTICAL REVIEW 15 1,807 2.740 0.002560 Bayesian Analysis 16 2,000 2.696 0.006600 ANNALS OF STATISTICS 17 21,466 2.650 0.027080 PROBABILISTIC ENGINEERING MECHANICS 18 2,689 2.411 0.002430 BRITISH JOURNAL OF MATHEMATICAL & STATISTICAL PSYCHOLOGY 19 1,965 2.388 0.003480 ANNALS OF PROBABILITY 20 5,892 2.377 0.017230 STOCHASTIC ENVIRONMENTAL RESEARCH AND RISK ASSESSMENT 21 4,272 2.351 0.006810 JOURNAL OF COMPUTATIONAL AND GRAPHICAL STATISTICS 22 4,369 2.319 0.008900 STATISTICAL METHODS IN -

Abbreviations of Names of Serials

Abbreviations of Names of Serials This list gives the form of references used in Mathematical Reviews (MR). ∗ not previously listed The abbreviation is followed by the complete title, the place of publication x journal indexed cover-to-cover and other pertinent information. y monographic series Update date: January 30, 2018 4OR 4OR. A Quarterly Journal of Operations Research. Springer, Berlin. ISSN xActa Math. Appl. Sin. Engl. Ser. Acta Mathematicae Applicatae Sinica. English 1619-4500. Series. Springer, Heidelberg. ISSN 0168-9673. y 30o Col´oq.Bras. Mat. 30o Col´oquioBrasileiro de Matem´atica. [30th Brazilian xActa Math. Hungar. Acta Mathematica Hungarica. Akad. Kiad´o,Budapest. Mathematics Colloquium] Inst. Nac. Mat. Pura Apl. (IMPA), Rio de Janeiro. ISSN 0236-5294. y Aastaraam. Eesti Mat. Selts Aastaraamat. Eesti Matemaatika Selts. [Annual. xActa Math. Sci. Ser. A Chin. Ed. Acta Mathematica Scientia. Series A. Shuxue Estonian Mathematical Society] Eesti Mat. Selts, Tartu. ISSN 1406-4316. Wuli Xuebao. Chinese Edition. Kexue Chubanshe (Science Press), Beijing. ISSN y Abel Symp. Abel Symposia. Springer, Heidelberg. ISSN 2193-2808. 1003-3998. y Abh. Akad. Wiss. G¨ottingenNeue Folge Abhandlungen der Akademie der xActa Math. Sci. Ser. B Engl. Ed. Acta Mathematica Scientia. Series B. English Wissenschaften zu G¨ottingen.Neue Folge. [Papers of the Academy of Sciences Edition. Sci. Press Beijing, Beijing. ISSN 0252-9602. in G¨ottingen.New Series] De Gruyter/Akademie Forschung, Berlin. ISSN 0930- xActa Math. Sin. (Engl. Ser.) Acta Mathematica Sinica (English Series). 4304. Springer, Berlin. ISSN 1439-8516. y Abh. Akad. Wiss. Hamburg Abhandlungen der Akademie der Wissenschaften xActa Math. Sinica (Chin. Ser.) Acta Mathematica Sinica. -

Ten Things We Should Know About Time Series

KIER DISCUSSION PAPER SERIES KYOTO INSTITUTE OF ECONOMIC RESEARCH Discussion Paper No.714 “Great Expectatrics: Great Papers, Great Journals, Great Econometrics” Michael McAleer August 2010 KYOTO UNIVERSITY KYOTO, JAPAN Great Expectatrics: Great Papers, Great Journals, Great Econometrics* Chia-Lin Chang Department of Applied Economics National Chung Hsing University Taichung, Taiwan Michael McAleer Econometric Institute Erasmus School of Economics Erasmus University Rotterdam and Tinbergen Institute The Netherlands and Institute of Economic Research Kyoto University Japan Les Oxley Department of Economics and Finance University of Canterbury New Zealand Rervised: August 2010 * The authors wish to thank Dennis Fok, Philip Hans Franses and Jan Magnus for helpful discussions. For financial support, the first author acknowledges the National Science Council, Taiwan; the second author acknowledges the Australian Research Council, National Science Council, Taiwan, and the Japan Society for the Promotion of Science; and the third author acknowledges the Royal Society of New Zealand, Marsden Fund. 1 Abstract The paper discusses alternative Research Assessment Measures (RAM), with an emphasis on the Thomson Reuters ISI Web of Science database (hereafter ISI). The various ISI RAM that are calculated annually or updated daily are defined and analysed, including the classic 2-year impact factor (2YIF), 5-year impact factor (5YIF), Immediacy (or zero-year impact factor (0YIF)), Eigenfactor score, Article Influence, C3PO (Citation Performance Per Paper Online), h-index, Zinfluence, and PI-BETA (Papers Ignored - By Even The Authors). The ISI RAM data are analysed for 8 leading econometrics journals and 4 leading statistics journals. The application to econometrics can be used as a template for other areas in economics, for other scientific disciplines, and as a benchmark for newer journals in a range of disciplines. -

HHS Public Access Author Manuscript

HHS Public Access Author manuscript Author Manuscript Author ManuscriptBiometrika Author Manuscript. Author manuscript; Author Manuscript available in PMC 2016 June 01. Published in final edited form as: Biometrika. 2015 June ; 102(2): 281–294. doi:10.1093/biomet/asv011. On random-effects meta-analysis D. ZENG and D. Y. LIN Department of Biostatistics, CB #7420, University of North Carolina, Chapel Hill, North Carolina 27599, U.S.A D. ZENG: [email protected]; D. Y. LIN: [email protected] Summary Meta-analysis is widely used to compare and combine the results of multiple independent studies. To account for between-study heterogeneity, investigators often employ random-effects models, under which the effect sizes of interest are assumed to follow a normal distribution. It is common to estimate the mean effect size by a weighted linear combination of study-specific estimators, with the weight for each study being inversely proportional to the sum of the variance of the effect-size estimator and the estimated variance component of the random-effects distribution. Because the estimator of the variance component involved in the weights is random and correlated with study-specific effect-size estimators, the commonly adopted asymptotic normal approximation to the meta-analysis estimator is grossly inaccurate unless the number of studies is large. When individual participant data are available, one can also estimate the mean effect size by maximizing the joint likelihood. We establish the asymptotic properties of the meta-analysis estimator and the joint maximum likelihood estimator when the number of studies is either fixed or increases at a slower rate than the study sizes and we discover a surprising result: the former estimator is always at least as efficient as the latter. -

Professor Robert Kohn

Professor Robert Kohn Curriculum Vitae Education Ph.D. Econometrics, Australian National University. Master of Economics, Australian National University. Academic Experience 2003 to present. Professor,Australian School of Business. Joint appointment between School of Economics and School of Banking and Finance. 1987 to 2003 Professor, Australian Graduate School of Management, University of New South Wales 1985-1987 Associate Professor, Australian Graduate School of Management, University of NSW 1982-1986 Associate Professor of Statistics, Graduate School of Business, University of Chicago 1979 -1982 Assistant Professor in Statistics, Graduate School of Business, University of Chicago Related Academic Experience 1991-2002 Head, Statistics and Operations Group, Australian Graduate School of Management, University New South Wales 1995-January 2002. Director, PhD Program Australian Graduate School of Management 1996-1998 Director of Research, Australian Graduate School of Management 1998- 2002 Associate Dean for Research, Australian Graduate School of Management 1998 to 2002 1 Member of the Committee on Research, University of New South Wales 1992 to 2002 Member, Higher Degree Committee, Australian Graduate School of Management 1991 to 2002 Member, Executive Committee, Australian Graduate School of Management. Awards Fellow of the Journal of Econometrics 2000 Fellow of the Institute of Mathematical Statistics 2002 Fellow of the American Statistical Association 2005 Scientia Professor, University of New South Wales, 2007-2012 Fellow Academy Social Sciences of Australia 2007 Associate Editor. 1996- Australia and New Zealand Journal of Statistics Associate Editor 1999-2001. Journal of the American Statistical Association. Associate Editor 2004- Bayesian Analysis Journal Associate Editor 2006 -2007 Sankhya Professional Affiliations Member of American Statistical Association, Econometric Society, Institute of Mathematical Statistics, Royal Statistical Society and Australian Statistical Society. -

CURRICULUM VITAE YAAKOV MALINOVSKY May 3, 2020

CURRICULUM VITAE YAAKOV MALINOVSKY May 3, 2020 University of Maryland, Baltimore County Email: [email protected] Department of Mathematics and Statistics Homepage: http://www.math.umbc.edu/ yaakovm 1000 Hilltop Circle Cell. No.: 240-535-1622 Baltimore, MD 21250 Education: Ph.D. 2009 The Hebrew University of Jerusalem, Israel Statistics M.A. 2002 The Hebrew University of Jerusalem, Israel Statistics with Operation Research B.A. 1999 The Hebrew University of Jerusalem, Israel Statistics (Summa Cum Laude) Experience in Higher Education: From July 1, 2017 , University of Maryland, Baltimore County, Associate Professor, Mathematics and Statistics. Fall 2011 { 2017, University of Maryland, Baltimore County, Assistant Professor, Mathematics and Statistics. September 2009 { August 2011, NICHD, Visiting Fellow. Spring 2003 { Spring 2007, The Hebrew University in Jerusalem, Instructor, Statistics. 2000{2004, The Open University, Israel, Instructor, Mathematics and Computer Science. Scholarships & Awards: 2014 IMS Meeting of New Researchers Travel award 2010 IMS Meeting of New Researchers Travel award 2003 Hebrew University Yochi Wax prize for PhD student 2001 Hebrew University Rector fellowship 1996 Hebrew University Dean's award 1995 Hebrew University Dean's list Academic visiting: Biostatistics Research Branch NIAID (June-August 2015), La Sapienza Rome Department of Mathematics (January 2018), Alfr´edR´enyi Institute of Mathematics Budapest (June 2018), Biostatistics Branch NCI (August 2017, August 2018, August 2019), Haifa University Department -

Academic Standards and Conventions2002

Partial Academic Standards and Conventions Department of Statistics Florida State University June 27, 2002 I. Important Journals in Statistics by Subdiscipline A. Mathematical Statistics and Probability 1. Top Tier Journals Annals of Applied Probability Annals of Probability Annals of Statistics Biometrika Journal of the American Statistical Association 2. Second Tier Journals Advances in Applied Probability Annals of Inst. H. Poincaré Bernoulli Canadian Journal of Statistics Journal of Applied Probability Journal of Multivariate Analysis Journal of Nonparametric Statistics Journal of the Royal Statistical Society, Series B Journal of Statistical Planning and Inference Journal of Time Series Analysis Lifetime Data Analysis Probability Theory and Related Fields Sankhya 1 Scandinavian Journal of Statistics Statistica Sinica Statistical Inference for Stochastic Processes Statistics Statistics and Decisions Statistics and Probability Letters Stochastic Processes and their Applications There are many other reputable journals, not listed, which are of lesser prestige. B. Applied and Computational Statistics 1. Top Tier Journals Biometrics Biometrika IEEE Transactions on Information Theory IEEE Transactions on Pattern Analysis and Machine Intelligence Journal of the American Statistical Association Technometrics 2. Second Tier Journals American Statistician Applied Statistics Biostatistics Computational Statistics and Data Analysis IEEE Transactions on Signal Processing Journal of Agricultural, Biological and Environmental Statistics Journal of Computational Statistics 2 Journal of Computational and Graphical Statistics Journal of Quality Technology Lifetime Data Analysis SIAM Journals Statistics in Medicine There are many other reputable journals, not listed, which are of lesser prestige. C. Top Tier Review Journals International Statistical Institute Review Statistical Science II. Important Publishers Academic Press Cambridge University Press Chapman & Hall John Wiley Marcell Dekker Oxford University Press Springer-Verlag III. -

Distributions You Can Count on . . . but What's the Point? †

econometrics Article Distributions You Can Count On . But What’s the Point? † Brendan P. M. McCabe 1 and Christopher L. Skeels 2,* 1 School of Management, University of Liverpoo, Liverpool L69 7ZH, UK; [email protected] 2 Department of Economics, The University of Melbourne, Carlton VIC 3053, Australia * Correspondence: [email protected] † An early version of this paper was originally prepared for the Fest in Celebration of the 65th Birthday of Professor Maxwell King, hosted by Monash University. It was started while Skeels was visiting the Department of Economics at the University of Bristol. He would like to thank them for their hospitality and, in particular, Ken Binmore for a very helpful discussion. We would also like to thank David Dickson and David Harris for useful comments along the way. Received: 2 September 2019; Accepted: 25 February 2020; Published: 4 March 2020 Abstract: The Poisson regression model remains an important tool in the econometric analysis of count data. In a pioneering contribution to the econometric analysis of such models, Lung-Fei Lee presented a specification test for a Poisson model against a broad class of discrete distributions sometimes called the Katz family. Two members of this alternative class are the binomial and negative binomial distributions, which are commonly used with count data to allow for under- and over-dispersion, respectively. In this paper we explore the structure of other distributions within the class and their suitability as alternatives to the Poisson model. Potential difficulties with the Katz likelihood leads us to investigate a class of point optimal tests of the Poisson assumption against the alternative of over-dispersion in both the regression and intercept only cases. -

Daniel S. Cooley Education Academic and Professional Experience

Daniel S. Cooley Professor and Graduate Director Department of Statistics, Colorado State University, Fort Collins, CO 80523-1877 [email protected] www.stat.colostate.edu/∼cooleyd August 4, 2020 Education Ph.D. Applied Mathematics, University of Colorado at Boulder, 2005 M.S. Applied Mathematics, University of Colorado at Boulder, 2002 B.A. Mathematics, University of Colorado at Boulder, 1994 Academic and Professional Experience 2020-Present: Graduate Director; Department of Statistics, Colorado State University. 2018-Present: Professor; Department of Statistics, Colorado State University. 2017-2020: Associate Chair; Department of Statistics, Colorado State University. 2015-Present: Faculty Member; School of Environmental Sustainability, Colorado State University. 2012-2018: Associate Professor; Department of Statistics, Colorado State University. 2007-2012: Assistant Professor; Department of Statistics, Colorado State University. 2005-2007: Postdoctoral Researcher; Department of Statistics, Colorado State University (joint ap- pointment). 2005-2007: Postdoctoral Researcher; Geophysical Statistics Project, National Center for Atmo- spheric Research, (joint appointment). Visiting Appointments Fall 2014: Visiting Scholar; Department of Statistics, University of Washington, Seattle WA. Fall 2011: Research Fellow, Program on Uncertainty Quantification; SAMSI, Research Triangle Park, NC. June 2008: Invited Visitor; Institut de Recherche Math´ematiqueAvanc´ee,Universit´eLouis Pasteur Strasbourg, France. Research Interests Extreme value theory, modeling multivariate extremes, heavy tailed phenomena, spatial statistics, applications in atmospheric science and environmental science. Honors/Awards College of Natural Sciences, Professor Laureate, 2017-2019. ASA Section on Statistics and the Environment Young Researcher Award, 2012. ASA Section on Statistics and the Environment (ENVR) JSM Presentation Award for the paper \Spatial Prediction of Extreme Value Return Levels", August 2005. 1 Publications Research Articles, Refereed 1.