Annual Report 2017 Today BHP Is Stronger, Simpler and More Productive

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Of the Environmental Protection Act 1986. EPA

FORM REFERRAL Referral of a Proposal by the Proponent to the Environmental Protection Authority under PROPONENT Section 38(1) of the Environmental Protection Act 1986. EPA PURPOSE OF THIS FORM Section 38(1) of the Environmental Protection Act 1986 (EP Act) provides that where a development proposal is likely to have a significant effect on the environment, a proponent may refer the proposal to the Environmental Protection Authority (EPA) for a decision on whether or not it requires assessment under the EP Act. This form sets out the information requirements for the referral of a proposal by a proponent. Proponents are encouraged to familiarise themselves with the EPA’s General Guide on Referral of Proposals [see Environmental Impact Assessment/Referral of Proposals and Schemes] before completing this form. A referral under section 38(1) of the EP Act by a proponent to the EPA must be made on this form. A request to the EPA for a declaration under section 39B (derived proposal) must be made on this form. This form will be treated as a referral provided all information required by Part A has been included and all information requested by Part B has been provided to the extent that it is pertinent to the proposal being referred. Referral documents are to be submitted in two formats – hard copy and electronic copy. The electronic copy of the referral will be provided for public comment for a period of 7 days, prior to the EPA making its decision on whether or not to assess the proposal. CHECKLIST Before you submit this form, please check that you have: Yes No Completed all the questions in Part A (essential). -

Strategy Delivery Growth

Rio Tinto 2009 Annual report Rio Tinto Financial calendar Strategy 2010 14 January Fourth quarter 2009 operations review 11 February Announcement of results for 2009 24 February Rio Tinto plc and Rio Tinto Limited shares and Rio Tinto plc ADRs quoted “ex-dividend” for 2009 fi nal dividend Delivery 26 February Record date for 2009 fi nal dividend for Rio Tinto plc shares and ADRs 2 March Record date for 2009 fi nal dividend for Rio Tinto Limited shares 11 March Plan notice date for election under the dividend reinvestment plan for the 2009 fi nal dividend 1 April Payment date for 2009 fi nal dividend to holders of Ordinary shares and ADRs Growth 15 April Annual general meeting for Rio Tinto plc 15 April First quarter 2010 operations review 22 April Annual general meeting for Rio Tinto Limited A focused and 14 July Second quarter 2010 operations review 5 August Announcement of half year results for 2010 integrated strategy 11 August Rio Tinto plc and Rio Tinto Limited shares and Rio Tinto plc ADRs quoted “ex-dividend” for 2010 interim dividend 13 August Record date for 2010 interim dividend for Rio Tinto plc shares and ADRs 17 August Record date for 2010 interim dividend for Rio Tinto Limited shares Excellence in 18 August Plan notice date for election under the dividend reinvestment plan for the 2010 interim dividend 9 September Payment date for 2010 interim dividend to holders of Ordinary shares and ADRs operational delivery 14 October Third quarter 2010 operations review 2011 Positioned for growth January Fourth quarter 2010 operations review February Announcement of results for 2010 Useful information and contacts Registered offi ces Investor Centre Rio Tinto Limited Rio Tinto plc To fi nd out more about Investor Centre, go to Computershare Investor Services Pty Limited 2 Eastbourne Terrace www.investorcentre.co.uk/riotinto GPO Box 2975 London Holders of Rio Tinto American Melbourne W2 6LG Depositary Receipts (ADRs) Victoria 3001 Registered in England No. -

Engineering & Mining Journal

Know-How | Performance | Reliability With MineView® and SmartFlow® Becker Mining Systems offers two comprehensive and scalable data management solutions for your Digital Mine. MineView® is a powerful state-of-the-art 3D SCADA system, that analyses incoming data from various mine equipment and visualises it in a 3D mine model. SmartFlow® takes Tagging & Tracking to a new level: collected asset data is centrally processed and smart software analytics allow for process optimization and improved safety. MINEVIEW BECKER MINING SYSTEMS AG We have been at the forefront of technology in Energy Distribution, Automation, Communication, Transportation and Roof Support since 1964. Together with our customers we create and deliver highest quality solutions and services to make operations run more profi tably, reliably and safely. For more information go to www.becker-mining.com/digitalmine Becker Mining is a trademark of Becker Mining Systems AG. © 2018 Becker Mining Systems AG or one of its affi liates. DECEMBER 2018 • VOL 219 • NUMBER 12 FEATURES China’s Miners Promote New Era of Openness and Cooperation Major reforms within the mining sector and the government will foster green mines at home and greater investment abroad ....................................42 Defeating the Deleterious Whether at the head of a circuit or scavenging tailings, today’s flotation innovations address challenges presented by declining grades, rising costs and aging plants ..................................................................................52 Staying on Top of -

Our Company Annual Report 2011 a Disciplined Approach a Proven Strategy We Are BHP Billiton, a Leading Global Resources Company

For personal use only Our Company Annual Report 2011 A disciplined approach A proven strategy We are BHP Billiton, a leading global resources company. Our purpose is to create long-term shareholder value through the discovery, acquisition, development and marketing of natural resources. For personal use only BHP Billiton Limited. ABN 49 004 028 077. Registered in Australia. Registered office: 180 Lonsdale Street, Melbourne, Victoria 3000, Australia. BHP Billiton Plc. Registration number 3196209. Registered in England and Wales. Registered office: Neathouse Place, London SW1V 1BH, UK. Each of BHP Billiton Limited and BHP Billiton Plc are members of the BHP Billiton Group, which is headquartered in Australia. Contents 1 Key information 3 4 Board of Directors and information Key 1 1.1 Our business 3 Group Management Committee 104 1.2 Chairman’s Review 4 4.1 Board of Directors 104 1.3 Chief Executive Offi cer’s Report 5 4.2 Group Management Committee 107 1.4 Selected key measures 6 5 Corporate Governance Statement 108 1.5 Risk factors 7 5.1 Governance at BHP Billiton 108 1.6 Forward looking statements 11 5.2 Shareholder engagement 109 2 Information on the Company 12 5.3 Board of Directors 109 2.1 BHP Billiton locations 12 5.4 Board of Directors – Review, Information on the Company 2 2.2 Business overview 14 re-election and renewal 115 2.2.1 History and development 14 5.5 Board Committees 117 2.2.2 Petroleum Customer Sector Group 14 5.6 Risk management 124 2.2.3 Aluminium Customer Sector Group 21 5.7 Management 125 2.2.4 Base Metals Customer -

BHP: Fine Words, Foul Play 23 September 2020 Introduction

BHP: fine words, foul play 23 September 2020 Introduction BHP presents itself, and is often considered by investors, as the very model of a modern mining company. Not only does it present itself as socially and environmentally responsible but now as indispensable in the efforts to save the world from climate catastrophe. Given the impacts and potential impacts of its Australian operations on Aboriginal sites and the furore over Rio Tinto’s destruction of the Juukan Gorge site earlier this year, perhaps BHP will begin to tread more carefully. It certainly needs to. This briefing summarises concerns around current and planned operations in which BHP is involved in Brazil, Chile, Colombia, Peru and the USA. LMN and our member groups work with communities or partner organisations in these five countries. Concerns include ecological and social impacts, violation of indigenous rights, mining waste disposal and the financing of clean- up. Other matters of current concern are briefly noted. At the end of the briefing are reports on three legacy cases - in Papua New Guinea, Indonesia and Colombia - where BHP pulled out, leaving others to deal with the environmental destruction and social dislocation caused by its operations. LMN exists to work in solidarity with communities harmed by companies linked to London, including BHP, the world’s largest mining corporation. This briefing is intended to encourage those who finance the company to use that finance to force change, and members of the public to join us in support of communities in the frontline of the struggle to defend their rights and the integrity of the planet’s ecosystems. -

Mining Area C SRE Invertebrate Fauna Impact Assessment

Mining Area C SRE Invertebrate Fauna Impact Assessment Mining Area C - Life of Project Environmental Management Plan Revision 6 Environmental Impact Assessment of Short-range Endemic Invertebrates BHP Billiton Iron Ore Pty Ltd June 2015 Page | 0 Mining Area C SRE Invertebrate Fauna Impact Assessment Mining Area C Life of Project Environmental Management Plan Revision 6 Environmental Impact Assessment of Short-range Endemic Invertebrates DOCUMENT STATUS Version Review / Approved for Approved for Issue to Author No. Issue Name Date E. Drain (BHP 1 S. Callan, B. Durrant M. O'Connell 08/12/2014 Billiton Iron Ore) 2 S. Callan B. Durrant E. Drain 14/01/2015 3 S. Callan B. Durrant E. Drain 27/01/2015 Final S. Callan B. Durrant E. Drain 26/06/2015 IMPORTANT NOTE Apart from fair dealing for the purposes of private study, research, criticism, or review as permitted under the Copyright Act, no part of this report, its attachments or appendices may be reproduced by any process without the written consent of Biologic Environmental Survey Pty Ltd (“Biologic”). All enquiries should be directed to Biologic. We have prepared this report for the sole purposes of BHP Billiton Iron Ore Pty Ltd (“Client”) for the specific purpose only for which it is supplied. This report is strictly limited to the Purpose and the facts and matters stated in it do not apply directly or indirectly and will not be used for any other application, purpose, use or matter. In preparing this report we have made certain assumptions. We have assumed that all information and documents provided to us by the Client or as a result of a specific request or enquiry were complete, accurate and up-to-date. -

View Annual Report

2010 Annual Report We expect to triple our production base by 2015. A SOLID BASE A POSITION OF STRENGTH GroA ROBUST PROJwECT PIPELINE th A nickel A copper A copper-gold A nickel project under deposit in the One of the The 8th largest operation in a operation with construction in new Copperbelt world’s major copper mine in growing mining over 30 years mining-friendly located in undeveloped the world jurisdiction of mine life Finland NW Zambia copper deposits Kansanshi Guelb Moghrein Ravensthorpe Kevitsa Sentinel Haquira First Quantum Minerals Ltd. is a growing mining and metals First Quantum currently The Company’s current company engaged in mineral produces LME grade “A” copper approved copper projects are exploration, development cathode, copper in concentrate, expected to increase annual and mining. The Company’s gold and sulphuric acid and is production by at least 45% objective is to become a on track to become a significant by 2015. In addition, later-stage globally diversified nickel producer by 2012. The exploration projects have mining company. Company's current operations the potential to add a further are the Kansanshi copper-gold 500,000 tonnes of annual mine in Zambia and the Guelb copper production. Moghrein copper-gold mine in Mauritania. In 2010, First Quantum produced 323,017 tonnes of copper, 191,395 ounces of gold and generated $2.4 billion of revenues. Unless otherwise noted, all amounts in this report are expressed in United States dollars. 2010 Annual Report In 2010, our operations continued to provide a solid base to support our growth strategy. -

ETO Listing Dates As at 11 March 2009

LISTING DATES OF CLASSES 03 February 1976 BHP Limited (Calls only) CSR Limited (Calls only) Western Mining Corporation (Calls only) 16 February 1976 Woodside Petroleum Limited (Delisted 29/5/85) (Calls only) 22 November 1976 Bougainville Copper Limited (Delisted 30/8/90) (Calls only) 23 January 1978 Bank N.S.W. (Westpac Banking Corp) (Calls only) Woolworths Limited (Delisted 23/03/79) (Calls only) 21 December 1978 C.R.A. Limited (Calls only) 26 September 1980 MIM Holdings Limited (Calls only) (Terminated on 24/06/03) 24 April 1981 Energy Resources of Aust Ltd (Delisted 27/11/86) (Calls only) 26 June 1981 Santos Limited (Calls only) 29 January 1982 Australia and New Zealand Banking Group Limited (Calls only) 09 September 1982 BHP Limited (Puts only) 20 September 1982 Woodside Petroleum Limited (Delisted 29/5/85) (Puts only) 13 October 1982 Bougainville Copper Limited (Delisted 30/8/90) (Puts only) 22 October 1982 C.S.R. Limited (Puts only) 29 October 1982 MIM Holdings Limited (Puts only) Australia & New Zealand Banking Group Limited (Puts only) 05 November 1982 C.R.A. Limited (Puts only) 12 November 1982 Western Mining Corporation (Puts only) T:\REPORTSL\ETOLISTINGDATES Page 1. Westpac Banking Corporation (Puts only) 26 November 1982 Santos Limited (Puts only) Energy Resources of Aust Limited (Delisted 27/11/86) (Puts only) 17 December 1984 Elders IXL Limited (Changed name - Foster's Brewing Group Limited 6/12/90) 27 September 1985 Queensland Coal Trust (Changed name to QCT Resources Limited 21/6/89) 01 November 1985 National Australia -

To Be Renamed Ausmex Mining Group Limited

Eumeralla Resources Limited ACN 148 860 299 to be renamed Ausmex Mining Group Limited PROSPECTUS For the offer of up to 75 million shares at an issue price of $0.08 each to raise up to $6,000,000 (before costs) (public offer). The public offer is subject to a minimum subscription requirement of $4,000,000. The public offer is not underwritten. This prospectus is a re-compliance prospectus for the purposes of satisfying chapters 1 and 2 of the listing rules and to satisfy ASX requirements for reinstatement of the company’s securities to trading following a change in the nature and scale of the company’s activities. The offers made under this prospectus and the issue of securities pursuant to this prospectus are subject to and conditional on satisfaction of the offer conditions. If the offer conditions are not satisfied, no securities will be issued pursuant to this prospectus and the company will repay all money received from applicants without interest. Lead manager Solicitors to the Offers CPS Capital Group Pty Ltd Blackwall Legal LLP Level 45, 108 St Georges Terrace Level 6, 105 St Georges Terrace Perth WA 6000 Perth WA 6000 This document is important and should be read in its entirety. If after reading this prospectus you have any questions about the securities being offered under this prospectus or any other matter, then you should consult your stockbroker, accountant or other For personal use only professional advisor. The shares offered by this prospectus should be considered as highly speculative. CONTENTS 1. CORPORATE DIRECTORY ............................................................................................. 3 2. -

Attachment 13

Appendix 13 Executive Summary ‘The modern world is built on steel which has become essential to economic growth. In developing and developed nations alike, steel is an indispensable part of life … The future growth in demand for steel will be driven mainly by the needs of the developing world.’1 Note: 87% of all world metals consumed are iron and steel. Australia is rich in natural resources. Among the key resources in abundance are iron ore and thermal and coking coal; the key feedstock for steel. Queensland has an abundance of coal, while Western Australia has an abundance of iron ore. Australia has a small population with limited steel production, so these resources are shipped internationally to be used as inputs to steel production. Strong growth in raw steel production and consumption, driven by the rapid industrialisation of China and India in particular, is expected to continue. This will necessitate substantial investment in new global steelmaking capacity. Australia plays a significant leading role in the export steelmaking supply-chain as it has an estimated 40% of the world’s high grade seaborne iron ore and 65% of the world’s seaborne coking coal. Project Iron Boomerang was developed by East West Line Parks Pty Ltd (“EWLP”) to explore the economic feasibility of establishing first-stage steel mill semi-finished steel production in Australia, close to the major raw materials inputs. This Pre-Feasibility Study provides strong evidence that the construction of first-stage smelter precincts offers many cost effective consolidation and efficiency savings, and that a dedicated railroad with all supporting infrastructure is feasible and economically favourable for steelmakers. -

CAVAL Bma Sustainable Development Report

SuStainable Development Covering health, safety, environmental and community performance for the year ended 30 June 2008 www.bmacoal.com Cover: Lexie Frankham, Goonyella Riverside Mine contents This page: Stuart Davison, South Walker Creek Mine note from marcelo bastos.............. 1 introduction ..................................... 2 Health & Safety................................ 3 Supporting our communities .......... 5 environment ..................................... 9 indigenous Relations ..................... 14 economic ....................................... 16 01 note from marcelo bastos Welcome to BHP Billiton Mitsubishi During FY08, climate change was Alliance’s (BMA) 2008 Sustainable a key focus area for BMA. Our new Development Report. growth projects have enabled us to take a ‘best practice’ approach This report details the progress we to reducing and mitigating our have made over the past year, our greenhouse gas emissions through current sustainable development a number of avenues including priorities and objectives, and how energy efficiency. we work to manage and govern our sustainability activities. Our Energy Excellence program, which aims at ensuring behavioural We were greatly encouraged by the change, innovation and technological feedback from our 2007 report. We are progress, is a key element of our proud of the progress we have made, overarching climate change approach. but we also acknowledge many areas for further improvement. Needless to say, the biggest environmental and social impact Our commitment to the health and during FY08 was the devastating safety of our people is absolute, and Central Queensland floods, affecting our impacts on the environment all our mine sites. and community also must not be As detailed further in this report, our compromised. employees not only supported our The nature of our business means it communities, but showed enormous takes a strong team effort to realise commitment and team work in these commitments, and I greatly managing the release of water and value the support of all our operations. -

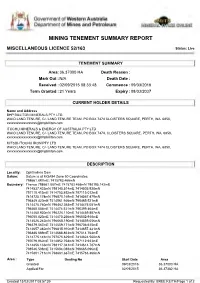

Mining Tenement Summary Report

Government of Western Australia Department of Mines and Petroleum MINING TENEMENT SUMMARY REPORT MISCELLANEOUS LICENCE 52/163 Status: Live TENEMENT SUMMARY Area: 36.37000 HA Death Reason : Mark Out : N/A Death Date : Received : 02/09/2015 08:33:48 Commence : 09/03/2016 Term Granted : 21 Years Expiry : 08/03/2037 CURRENT HOLDER DETAILS Name and Address BHP BILLITON MINERALS PTY LTD WAIO LAND TENURE, C/- LAND TENURE TEAM, PO BOX 7474 CLOISTERS SQUARE, PERTH, WA, 6850, [email protected] ITOCHU MINERALS & ENERGY OF AUSTRALIA PTY LTD WAIO LAND TENURE, C/- LAND TENURE TEAM, PO BOX 7474, CLOISTERS SQUARE, PERTH, WA, 6850, [email protected] MITSUI-ITOCHU IRON PTY LTD WAIO LAND TENURE, C/- LAND TENURE TEAM, PO BOX 7474 CLOISTERS SQUARE, PERTH, WA, 6850, [email protected] DESCRIPTION Locality: Ophthalmia Dam Datum: Datum is at MGA94 Zone 50 Coordinates. 798661.887mE; 7415783.466mN Boundary: Thence 798661.887mE 7415783.466mN 798195.142mE 7414537.433mN 798145.514mE 7414505.938mN 797110.415mE 7414753.892mN 797115.012mE 7414725.174mN 796870.169mE 7414567.479mN 796849.420mE 7414561.946mN 796465.521mE 7414475.760mN 796462.363mE 7414475.051mN 796460.004mE 7414474.521mN 796399.464mE 7414460.930mN 796226.110mE 7414459.887mN 796050.820mE 7414470.256mN 796032.918mE 7414526.242mN 796068.190mE 7414559.056mN 796379.567mE 7414559.171mN 796736.615mE 7414657.382mN 796815.910mE 7414657.431mN 796886.689mE 7414688.863mN 797014.764mE 7414775.141mN 797075.629mE 7414824.500mN 797079.962mE 7414852.758mN 797112.933mE 7414856.133mN