IMPORTANT: You Must Read the Following Disclaimer Before Continuing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DXE Liquidity Provider Registered Firms

DXE Liquidity Provider Program Registered Securities European Equities TheCboe following Europe Limited list of symbols specifies which firms are registered to supply liquidity for each symbol in 2021-09-28: 1COVd - Covestro AG Citadel Securities GCS (Ireland) Limited (Program Three) DRW Europe B.V. (Program Three) HRTEU Limited (Program Two) Jane Street Financial Limited (Program Three) Jump Trading Europe B.V. (Program Three) Qube Master Fund Limited (Program One) Societe Generale SA (Program Three) 1U1d - 1&1 AG Citadel Securities GCS (Ireland) Limited (Program Three) HRTEU Limited (Program Two) Jane Street Financial Limited (Program Three) 2GBd - 2G Energy AG Citadel Securities GCS (Ireland) Limited (Program Three) Jane Street Financial Limited (Program Three) 3BALm - WisdomTree EURO STOXX Banks 3x Daily Leveraged HRTEU Limited (Program One) 3DELm - WisdomTree DAX 30 3x Daily Leveraged HRTEU Limited (Program One) 3ITLm - WisdomTree FTSE MIB 3x Daily Leveraged HRTEU Limited (Program One) 3ITSm - WisdomTree FTSE MIB 3x Daily Short HRTEU Limited (Program One) 8TRAd - Traton SE Jane Street Financial Limited (Program Three) 8TRAs - Traton SE Jane Street Financial Limited (Program Three) Cboe Europe Limited is a Recognised Investment Exchange regulated by the Financial Conduct Authority. Cboe Europe Limited is an indirect wholly-owned subsidiary of Cboe Global Markets, Inc. and is a company registered in England and Wales with Company Number 6547680 and registered office at 11 Monument Street, London EC3R 8AF. This document has been established for information purposes only. The data contained herein is believed to be reliable but is not guaranteed. None of the information concerning the services or products described in this document constitutes advice or a recommendation of any product or service. -

2020 Governance, Compensation and Financial Report Ements

Governance, Compensation and Financial Report 2020 Governance, Compensation Governance report and Financial Report As part of our reporting suite, this stand-alone document contains the full details of our governance and compensation policies as well as the details of our financial performance. Compensation Compensation report An overview can be found in the Integrated Annual Report. Consolidated Consolidated report financial Statutory report financial Table of contents 3 Governance report 22 Compensation report 38 Consolidated financial report 102 Statutory financial report Appendix 114 Appendix Governance Report In this section 4 Group structure and shareholders 5 Capital structure 7 Board of Directors 16 Executive Committee 19 Compensation, shareholdings and loans 19 Shareholders’ participation 20 Change of control and defence measures 20 Auditors 21 Information policy Givaudan – 2020 Governance, Compensation and Financial Report 4 Corporate governance Governance report Ensuring proper checks and balances 1. Group structure and shareholders The Governance report is aligned with 1.1 Group structure 1.1.1 Description of the issuer’s operational Group structure international standards and has been prepared Givaudan SA, the parent company of the Givaudan Group, with its registered corporate headquarters at 5 Chemin de la Parfumerie, 1214 Vernier, Switzerland (‘the Company’), is a in accordance with the ‘Swiss Code of Obligations’, ‘société anonyme’, pursuant to art. 620 et seq. of the Swiss Code of Obligations. It is listed on Compensation Compensation report the ‘Directive on Information Relating to the SIX Swiss Exchange under security number 1064593, ISIN CH0010645932. Corporate Governance’ issued by the SIX Swiss The Company is a global leader in its industry. Givaudan operates around the world and has two principal businesses: Taste & Wellbeing and Fragrance & Beauty, providing customers Exchange and the ‘Swiss Code of Best Practice for with compounds, ingredients and integrated solutions. -

Liste Des Actions Concernées Par L'interdiction De Positions Courtes Nettes

Liste des actions concernées par l'interdiction de positions courtes nettes L’interdiction s’applique aux actions listées sur une plate-forme française et relevant de la compétence de l’AMF au titre du règlement 236/2012 (information disponible dans les registres ESMA). Cette liste est fournie à titre informatif. L'AMF n'est pas en mesure de garantir que le contenu disponible est complet, exact ou à jour. Compte tenu des diverses sources de données sous- jacentes, des modifications pourraient être apportées régulièrement. Isin Nom FR0010285965 1000MERCIS FR0013341781 2CRSI FR0010050773 A TOUTE VITESSE FR0000076887 A.S.T. GROUPE FR0010557264 AB SCIENCE FR0004040608 ABC ARBITRAGE FR0013185857 ABEO FR0012616852 ABIONYX PHARMA FR0012333284 ABIVAX FR0000064602 ACANTHE DEV. FR0000120404 ACCOR FR0010493510 ACHETER-LOUER.FR FR0000076861 ACTEOS FR0000076655 ACTIA GROUP FR0011038348 ACTIPLAY (GROUPE) FR0010979377 ACTIVIUM GROUP FR0000053076 ADA BE0974269012 ADC SIIC FR0013284627 ADEUNIS FR0000062978 ADL PARTNER FR0011184241 ADOCIA FR0013247244 ADOMOS FR0010340141 ADP FR0010457531 ADTHINK FR0012821890 ADUX FR0004152874 ADVENIS FR0013296746 ADVICENNE FR0000053043 ADVINI US00774B2088 AERKOMM INC FR0011908045 AG3I ES0105422002 AGARTHA REAL EST FR0013452281 AGRIPOWER FR0010641449 AGROGENERATION CH0008853209 AGTA RECORD FR0000031122 AIR FRANCE -KLM FR0000120073 AIR LIQUIDE FR0013285103 AIR MARINE NL0000235190 AIRBUS FR0004180537 AKKA TECHNOLOGIES FR0000053027 AKWEL FR0000060402 ALBIOMA FR0013258662 ALD FR0000054652 ALES GROUPE FR0000053324 ALPES (COMPAGNIE) -

Robertet Group 177 Management Report

FINANCIAL PERFORMANCE REPORT 2019 FISCAL YEAR ENDING 31 DÉCEMBER 2019 SUMMARY MANAGEMENT REPORT 3 CORPORATE SOCIAL RESPONSIBILITY 16 CONSOLIDATED ACCOUNTS 75 CORPORATE ACCOUNTS 118 CORPORATE GOVERNANCE REPORT 141 CERTIFICATION BY THE PERSON RESPONSIBLE FOR THE ANNUAL FINANCIAL REPORT 2019 162 STATUTARY AUDITORS REPORT 164 ROBERTET GROUP 177 MANAGEMENT REPORT FISCAL YEAR ENDING 31 DECEMBER 2019 MANAGEMENT REPORT 2019 has been a year of intense commercial activity but also one of questioning, allowing us to better envisage future growth and the optimal framework preserving the best interests in the Long Term. Revenues were up to 554.3 million, an increase of 5.6% (3.3% at constant exchange rate) largely in line with initial objectives. Product gross margins improved slightly with partial normalization of supply chemicals for the Fragrance industry, which was in crisis last year. There have been positive developments in the three main divisions, especially in the Raw Materials Division, despite the sharp decline in its Aromatherapy sales. This once again confirms the soundness of Robertet's strategy, making the most of its undeniable expertise in this type of product. This is inherited from its history associated with R&D and a sustainable supply policy that make the Group the undisputed leader in this market. This contributes to the natural differentiation of all Robertet's offers in Fragrances and Flavors. The Health and Beauty Division, which now accounts for more than 3% of Group sales, benefits fully from this accumulated knowledge, combined with successfully targeted acquisitions. The year 2019 was also marked by the Group's acceleration in its range of organic products. -

Corporate Social Responsibility

Corporate Social Responsibility The 2016 Report Contents Introduction ���������������������������������������������������������������� 6 About the Robertet Group 7 Our CSR approach 9 Sourcing materials ������������������������������������������� 12 Supplier evaluation 13 Supporting growers 16 Robertet crops 19 Transforming resources ������������������������� 22 Quality policy 23 Respecting the environment 25 Valuing people ������������������������������������������������������� 29 Sustainable employment 30 Preserving precious know-how 32 Work conditions 34 Equality and human rights 35 Appendixes ����������������������������������������������������������������� 37 Key performance indicators 38 Grenelle II compliance 40 Editorial 2016, a very good year 2016 once again showed the effectiveness of the Robertet model, in terms of strategy as well as corporate social and environmental responsibility� We have reaffirmed our position as a world leader in natural raw materials by opening new sites abroad, particularly in Asia� We have also shown our capacity to innovate and develop new business� In fact, although our history dates back over 150 years, some of our divisions are more recent� This is the case of Robertet Health & Beauty, which uses our expert knowledge of natural ingredients to make women look and feel fabulous� Our 2016 acquisition of Bionov, a top grower of a key natural bioactive ingredient, further strengthens this division, and contributes new synergy and expertise to the Group� Finally, our new approach to materials sourcing -

SOCIAL Responsibility

THE 2015 REPORT CORPORATE SOCIAL Responsibility ROBERTET GROUP CONTENTS INTRODUCTION About the Robertet Group - page 5 Our CSR approach - page 8 SOURCING MATERIALS Supplier evaluation- page 12 Supporting producers - page 16 Subsidiaries and joint ventures- page 18 Partnerships - page 19 TRANSFORMING RESOURCES Quality policy- page 22 Respecting the environment - page 24 VALUING PEOPLE Sustainable employment - page 30 Preserving precious know-how - page 31 Work conditions - page 32 Equality and human rights - page 33 APPENDIXES Key performance indicators- page 37 Grenelle II compliance - page 40 GROWING obertet is a family business, founded in Grasse, France, Rin 1850. The company has developed over the years, led by five generations with the same passions: excellence and nature. Today, the Robertet Group is the world leader in natural raw materials, and employs nearly 2,000 people. The Group continues to be faithful to its founding values: long-term vision, innovation and creativity, respecting people, preserving biodiversity, contribu- ting to the community (especially Grasse), and sharing know- how. These fundamental principles enable us to grow and meet market demands. Today, customers expect more than quality and product safety. The scope of corporate leadership is expanding beyond economic considerations to include social and environ- mental factors. This change implies important responsibilities with regard to stakeholders in our natural raw materials supply chains. It also means offering customers healthier products and develo- ping cleaner production processes. Our ambition is also to further explore the potential of raw materials and develop the co-products of the plants from which we extract our flavors and fragrances. This mission, which draws on our natural product expertise, is the role of Robertet’s new Health & Beauty division. -

International Smallcap Separate Account As of July 31, 2017

International SmallCap Separate Account As of July 31, 2017 SCHEDULE OF INVESTMENTS MARKET % OF SECURITY SHARES VALUE ASSETS AUSTRALIA INVESTA OFFICE FUND 2,473,742 $ 8,969,266 0.47% DOWNER EDI LTD 1,537,965 $ 7,812,219 0.41% ALUMINA LTD 4,980,762 $ 7,549,549 0.39% BLUESCOPE STEEL LTD 677,708 $ 7,124,620 0.37% SEVEN GROUP HOLDINGS LTD 681,258 $ 6,506,423 0.34% NORTHERN STAR RESOURCES LTD 995,867 $ 3,520,779 0.18% DOWNER EDI LTD 119,088 $ 604,917 0.03% TABCORP HOLDINGS LTD 162,980 $ 543,462 0.03% CENTAMIN EGYPT LTD 240,680 $ 527,481 0.03% ORORA LTD 234,345 $ 516,380 0.03% ANSELL LTD 28,800 $ 504,978 0.03% ILUKA RESOURCES LTD 67,000 $ 482,693 0.03% NIB HOLDINGS LTD 99,941 $ 458,176 0.02% JB HI-FI LTD 21,914 $ 454,940 0.02% SPARK INFRASTRUCTURE GROUP 214,049 $ 427,642 0.02% SIMS METAL MANAGEMENT LTD 33,123 $ 410,590 0.02% DULUXGROUP LTD 77,229 $ 406,376 0.02% PRIMARY HEALTH CARE LTD 148,843 $ 402,474 0.02% METCASH LTD 191,136 $ 399,917 0.02% IOOF HOLDINGS LTD 48,732 $ 390,666 0.02% OZ MINERALS LTD 57,242 $ 381,763 0.02% WORLEYPARSON LTD 39,819 $ 375,028 0.02% LINK ADMINISTRATION HOLDINGS 60,870 $ 374,480 0.02% CARSALES.COM AU LTD 37,481 $ 369,611 0.02% ADELAIDE BRIGHTON LTD 80,460 $ 361,322 0.02% IRESS LIMITED 33,454 $ 344,683 0.02% QUBE HOLDINGS LTD 152,619 $ 323,777 0.02% GRAINCORP LTD 45,577 $ 317,565 0.02% Not FDIC or NCUA Insured PQ 1041 May Lose Value, Not a Deposit, No Bank or Credit Union Guarantee 07-17 Not Insured by any Federal Government Agency Informational data only. -

France Alpha 7.1% Beta 0.6 Download

CIM algo Draft version R30 France Calculation Date: 2020-01-20 The CIMalgo R30 France is Cimalgo's Robust investment model applied to France. The Robust model is an algorithmic portfolio construction procedure which seeks to provide strong risk-adjusted performance and low beta in any market worldwide by aiming at high-liquidity stocks and combining high diversification with propriatary portfolio optimization techniques. The performance is achieved through optimization for low volatility and limited drawdowns. Combined with a simple equal-weighting rule ex- ploiting long-term mean reversal properties of equity prices results in stable long-term risk-adjusted performance independent of both domestic and global market business cycles. All performance below is based on total return. Backtest Performance Model Characteristics Backtested performance is compared to MSCI France Gross Total Return USD Index. Region France 2000−01−10 / 2020−01−20 Universe All Trading Constituents 30 600 R30 MSCI Weighting Equal 500 Rebalancing Quarterly 400 Currency USD Liquidity Requirement Min 0.2M USD ADTV 300 Annual Performance (%) 200 Year Return % Volatility % Sharpe Ratio 100 R30 MSCI R30 MSCI R30 MSCI 2000 21.1 0.4 21.6 24.5 1.0 0.0 Jan 10 Jan 01 Jan 01 Jan 02 Jan 01 Jan 01 Jan 02 Jan 01 Jan 01 Jan 01 Jan 01 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2001 -15.6 -22.1 17.2 25.0 -0.9 -0.9 2002 5.1 -20.8 13.9 32.0 0.4 -0.7 2003 41.6 41.0 10.2 22.2 4.1 1.9 Drawdown Comparison (%) 2004 36.8 19.2 12.0 15.0 3.1 1.3 2005 13.7 10.6 10.9 12.4 1.3 0.9 Drawdown is compared to MSCI France Gross Total Return USD Index. -

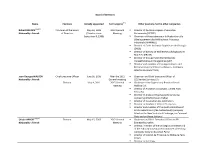

Board of Directors Name Positions Initially Appointed Term Expires

Board of Directors Name Positions Initially appointed Term expires(**) Other positions held in other companies Robert BRUNCK(2)(4)(*) Chairman of the Board May 20, 1999 2012 General . Director of Centre Européen d’Education Nationality : French of Directors (Director since Meeting Permanente (CEDEP) September 9, 1998) . Chairman of Association pour la Recherche et le Développement des Méthodes et Processus industriels (ARMINES) . Director of Ecole Nationale Supérieure de Géologie (ENSG) . Director of Bureau de Recherches Géologiques et Minières (BRGM) . Director of Groupement des Entreprises Parapétrolières et Paragazières (GEP) . Director and member of the Appointment and Remuneration Committee of Nexans (company listed on Euronext Paris) Jean-Georges MALCOR Chief Executive Officer June 30, 2010 After the 2012 . Chairman and Chief Executive Officer of Nationality : French General meeting CGGVeritas Services S.A. Director May 4, 2011 2015 General . Chairman of the Supervisory Board of Sercel meeting Holding S.A. Director of Ardiseis FZCO (Dubaï, United Arab Emirates) . Director of Arabian Geophysical & Surveying Company (ARGAS) (Saudi Arabia) . Director of Association des Centraliens . Director of Fondation Villette Entreprises . Director and member of the Audit committee of STMicroelectronics (the Netherlands) (company listed on the New York stock Exchange, on Euronext Paris and on Borsa Italiana) Olivier APPERT(2)(3)(*) Director May 15, 2003 2012 General . Chairman and Chief Executive Officer of IFP Nationality : French Meeting Energies Nouvelles . Director, member of the Strategic Committee and of the Ethics & Governance Committee of Technip (company listed on Euronext Paris) . Director of Institut de Physique du Globe de Paris (IPGP) . Director of Storengy Loren CARROLL(1) Director January 12, 2007 2013 General . -

Euro Stoxx® Total Market Small Index

EURO STOXX® TOTAL MARKET SMALL INDEX Components1 Company Supersector Country Weight (%) BE SEMICONDUCTOR Technology Netherlands 1.34 DIALOG SEMICON Technology Germany 1.32 Valmet Industrial Goods & Services Finland 1.19 EVOTEC Health Care Germany 1.18 BANK OF IRELAND GROUP Banks Ireland 1.11 SOITEC Technology France 1.09 BANCO BPM Banks Italy 1.07 TAG IMMOBILIEN AG Real Estate Germany 1.07 WIENERBERGER Construction & Materials Austria 1.03 INTERPUMP GRP Industrial Goods & Services Italy 1.03 COFINIMMO Real Estate Belgium 0.97 AEDIFICA Real Estate Belgium 0.92 SHOP APOTHEKE EUROPE Personal Care, Drug & Grocery Stores Germany 0.85 ALTEN Technology France 0.83 SPIE Construction & Materials France 0.77 BCO SABADELL Banks Spain 0.77 ITALGAS Utilities Italy 0.76 FREENET Telecommunications Germany 0.75 MORPHOSYS Health Care Germany 0.74 ALSTRIA OFFICE REIT Real Estate Germany 0.74 SOLVAC Chemicals Belgium 0.71 ARCADIS Construction & Materials Netherlands 0.70 GERRESHEIMER Health Care Germany 0.69 KONECRANES Industrial Goods & Services Finland 0.69 TIETOEVRY Technology Finland 0.68 GRAND CITY PROPERTIES Real Estate Germany 0.67 SOPRA STERIA GROUP Technology France 0.65 VARTA AG Industrial Goods & Services Germany 0.64 DE LONGHI Consumer Products & Services Italy 0.64 CORBION Food, Beverage & Tobacco Netherlands 0.64 VIDRALA Industrial Goods & Services Spain 0.64 CA IMMOBILIEN ANLAGEN Real Estate Austria 0.63 BUZZI UNICEM Construction & Materials Italy 0.63 VISCOFAN Food, Beverage & Tobacco Spain 0.62 AZIMUT HLDG Financial Services Italy 0.62 -

RESPONSABILITÉ SOCIÉTALE Des Entreprises

RAPPORT 2015 RESPONSABILITÉ SOCIÉTALE des Entreprises GROUPE ROBERTET SOMMAIRE INTRODUCTION Notre identité - page 5 La RSE chez Robertet - page 8 SOURCER LES MATIERES L’évaluation des fournisseurs - page 12 L’accompagnement des producteurs - page 16 Les filiales et joint ventures - page 18 Les partenariats - page 19 TRANSFORMER LES RESSOURCES La politique qualité - page 22 Le respect de l’environnement - page 24 VALORISER LES HOMMES La pérennité de l’emploi - page 30 La transmission du savoir faire - page 31 Les conditions de travail - page 32 L’égalité et les droits humains - page 33 ANNEXES Tableau des indicateurs - page 37 Tableau de correspondance avec l’article 225 - page 40 GROWING obertet est une société familiale fondée en 1850 à RGrasse et qui s’est développée au fil du temps, et à travers cinq générations animées d’une même passion : le goût de l’excellence et la passion du naturel. Aujourd’hui leader mondial des matières premières naturelles et un Groupe de près de 2000 collabora- teurs, l’entreprise maintient ses valeurs d’origines et ses principes fondamentaux : la vision à long terme, le respect de l’humain, la préservation de la biodiversité, la contribution aux territoires et en particulier à celui de Grasse, la transmission du savoir faire, l’innovation et la créativité… C’est avec ces forces que le Groupe doit évoluer avec son marché et s’adapter à ses exigences, car les attentes de nos clients et des consommateurs vont désormais au delà de la qualité et de la sécurité des produits. Le dirigeant d’entreprise voit son champ de responsabilité s’élargir, et se doit d’intégrer des considérations non seulement économiques mais aussi sociales et environnementales. -

Board of Directors Name Position Initially Appointed Term

Board of Directors Name Position Initially appointed Term expires(**) Other positions held in other companies Robert BRUNCK(2)(4) Chairman of the Board May 20, 1999 2016 General . Director of Centre Européen d’Education Nationality : French of Directors (Director since Meeting Permanente (CEDEP) September 9, 1998) . Chairman of Association pour la Recherche et le Développement des Méthodes et Processus industriels (ARMINES) . Director of Ecole Nationale Supérieure de Géologie (ENSG) . Director of Bureau de Recherches Géologiques et Minières (BRGM) . Director of Groupement des Entreprises Parapétrolières et Paragazières – Association Française des Techniciens du Pétrole (GEP-AFTP) . Director and member of the Appointment and Remuneration Committee of Nexans (company listed on Euronext Paris) Jean-Georges MALCOR Chief Executive Officer May 4, 2011 2015 General . Chairman of the Board of Directors of Sercel Nationality : French and Director meeting Holding S.A. Director of Ardiseis FZCO (Dubaï, United Arab Emirates) . Director of Arabian Geophysical & Surveying Company (ARGAS) (Saudi Arabia) . Chairman of Fonds de Dotation Universcience Partenaires . Director of Seabed Geosolutions B.V. Director and member of the Audit committee of STMicroelectronics (The Netherlands) (company listed on the New York stock Exchange, on Euronext Paris and on Borsa Italiana) Olivier APPERT(2)(3) Director May 15, 2003 2016 General . Chairman and Chief Executive Officer of IFP Nationality : French Meeting Energies Nouvelles . Director, member of the Strategic Committee and of the Ethics & Governance Committee of Technip (company listed on Euronext Paris) . Director of Institut de Physique du Globe de Paris (IPGP) . Director and member of the Audit committee of Storengy Name Position Initially appointed Term expires(**) Other positions held in other companies Loren CARROLL(1)(*) Director January 12, 2007 2013 General .