Financial Strength Fact Sheet Financial Strength

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Capital Power Corporation 12Th Floor, EPCOR Tower 1200 – 10423 101 Street Edmonton, AB T5H 0E9

Capital Power Corporation 12th Floor, EPCOR Tower 1200 – 10423 101 Street Edmonton, AB T5H 0E9 For release: February 21, 2017 Capital Power reports fourth quarter and year-end 2016 results EDMONTON, Alberta – Capital Power Corporation (Capital Power, or the Company) (TSX: CPX) today released financial results for the fourth quarter and year ended December 31, 2016. Net income attributable to shareholders in the fourth quarter of 2016 was $28 million and basic earnings per share attributable to common shareholders was $0.21 per share, compared with $35 million, or $0.29 per share, in the comparable period of 2015. Normalized earnings attributable to common shareholders in the fourth quarter of 2016, after adjusting for one-time items and fair value adjustments, were $26 million or $0.27 per share compared with $41 million or $0.42 per share in the fourth quarter of 2015. Net cash flows from operating activities were $69 million in the fourth quarter of 2016 compared with $114 million in the fourth quarter of 2015. Funds from operations (FFO) were $75 million in the fourth quarter of 2016, compared to $125 million in the fourth quarter of 2015. For the year ended December 31, 2016, net income attributable to shareholders was $111 million and basic earnings per share attributable to common shareholders was $0.91 per share compared with $90 million and $0.70 for the year ended December 31, 2015. For the year ended December 31, 2016, normalized earnings attributable to common shareholders were $117 million, or $1.22 per share, compared with $111 million, or $1.15 per share in 2015. -

Investor Presentation Q1 2021 Quarterly Results

Investor Presentation Q1 2021 Quarterly Results May 14th, 2021 Forward looking statements and COVID-19 Forward Looking Statements In the course of today’s meeting, representatives of the Corporation may make, in their remarks or in response to questions, and the accompanying materials may include, statements containing forward-looking information. Certain statements, other than statements of historical fact, are forward-looking statements based on certain assumptions and reflect the Corporation’s current expectations, or with respect to disclosure regarding the Corporation’s public subsidiaries, reflect such subsidiaries’ disclosed current expectations. Forward-looking statements are provided for the purposes of assisting the reader in understanding the Corporation’s financial performance, financial position and cash flows as at and for the periods ended on certain dates and to present information about management’s current expectations and plans relating to the future and the reader is cautioned that such statements may not be appropriate for other purposes. These statements may include, without limitation, statements regarding the operations, business, financial condition, expected financial results, performance, prospects, opportunities, priorities, targets, goals, ongoing objectives, strategies and outlook of the Corporation and its subsidiaries including the fintech strategy, the expected impact of the COVID-19 pandemic on the Corporation and its subsidiaries’ operations, results and dividends, as well as the outlook for North American -

Sun Life Guaranteed Investment Funds (Gifs)

Sun Life Guaranteed Investment Funds (GIFs) ANNUAL FINANCIAL STATEMENTS SUN LIFE ASSURANCE COMPANY OF CANADA December 31, 2015 Life’s brighter under the sun Sun Life Assurance Company of Canada is a member of the Sun Life Financial group of companies. © Sun Life Assurance Company of Canada, 2016. 36D-0092-02-16 Table of Contents Independent Auditors' Report 3 Sun MFS Dividend Income 196 Sun Beutel Goodman Canadian Bond 5 Sun MFS Global Growth 200 Sun BlackRock Canadian Balanced 10 Sun MFS Global Total Return 204 Sun BlackRock Canadian Composite Equity 15 Sun MFS Global Value 209 Sun BlackRock Canadian Equity 20 Sun MFS Global Value Bundle 214 Sun BlackRock Canadian Equity Bundle 25 Sun MFS International Growth 218 Sun BlackRock Cdn Composite Eq Bundle 29 Sun MFS International Growth Bundle 222 Sun BlackRock Cdn Universe Bond 33 Sun MFS International Value 226 Sun Canadian Balanced Bundle 38 Sun MFS International Value Bundle 230 Sun CI Cambridge Canadian Equity 42 Sun MFS Monthly Income 234 Sun CI Cambridge Cdn Asset Allocation 46 Sun MFS US Equity 238 Sun CI Cambridge Global Equity 50 Sun MFS US Equity Bundle 242 Sun CI Cambridge/MFS Canadian Bundle 54 Sun MFS US Growth 246 Sun CI Cambridge/MFS Global Bundle 58 Sun MFS US Value 250 Sun CI Signature Diversified Yield II 62 Sun MFS US Value Bundle 255 Sun CI Signature High Income 66 Sun Money Market 259 Sun CI Signature Income & Growth 70 Sun NWQ Flexible Income 264 Sun Daily Interest 74 Sun PH&N Short Term Bond and Mortgage 268 Sun Dollar Cost Average Daily Interest 78 Sun RBC Global High -

2020 Annual Information Form

2020 Annual Information Form March 23, 2021 POWER CORPORATION OF CANADA > 2020 ANNUAL INFORMATION FORM 2 TABLE OF CONTENTS Item 1 General Information 3 Item 1.1 Defined terms 3 Item 1.2 Information regarding Power Financial 4 Item 2 Documents Incorporated by Reference 5 Item 3 Forward-Looking Information 6 Item 4 Corporate Structure 8 Item 4.1 Incorporation 8 Item 4.2 Intercorporate relationships 9 Item 5 General Development of the Business 11 Item 5.1 Business of Power 11 Item 5.2 Development of the business over the last three years 11 Item 6 Narrative Description of the Business 16 Item 6.1 Publicly traded operating companies 16 Item 6.2 Alternative asset investment platforms 20 Item 6.3 China AMC 22 Item 7 Risk Factors 23 Item 8 Description of the Share Capital 25 Item 8.1 Power 25 Item 8.2 Power Financial 27 Item 9 Ratings 32 Item 10 Dividends 35 Item 10.1 Power 35 Item 10.2 Power Financial 35 Item 11 Market for Securities 37 Item 11.1 Power 37 Item 11.2 Power Financial 38 Item 12 Directors and Officers 41 Item 12.1 Directors 41 Item 12.2 Executive and other officers 42 Item 13 Voting Securities 44 Item 14 Committees 45 Item 14.1 Audit Committee 45 Item 15 Interest of Management and Others in Material Transactions 48 Item 16 Transfer Agent 49 Item 17 Experts 49 Item 18 Environmental, Social and Governance Factors 50 Item 19 Additional Information 51 Appendix A Power Corporation of Canada Audit Committee Charter 52 POWER CORPORATION OF CANADA > 2020 ANNUAL INFORMATION FORM 3 ITEM 1 GENERAL INFORMATION Item 1 Item 1.1 Defined terms – General Information General The following abbreviations have been used throughout this Annual Information Form: Name in full Abbreviation adidas AG adidas Annual Information Form of Great-West Lifeco Inc., Lifeco’s Annual Information Form dated February 10, 2021 Annual Information Form of IGM Financial Inc., IGM Financial’s Annual Information Form dated March 18, 2021 The Canada Life Assurance Company Canada Life China Asset Management Co., Ltd. -

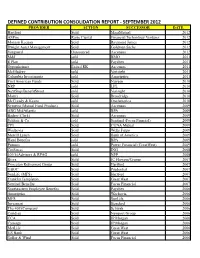

Defined Contribution Consolidation Report

DEFINED CONTRIBUTION CONSOLIDATION REPORT - SEPTEMBER 2012 PROVIDER ACTION SUCCESSOR DATE Hartford Sold MassMutual 2012 ASPire Raise Capital Financial Technology Ventures 2012 Morgan Keegan Sold Raymond James 2012 Dwight Asset Management Sold Goldman Sachs 2012 Vanguard Outsourced Ascensus 2012 M&I sold BMO 2011 E Plan sold Paychex 2011 Oppenheimer Exited RK Ascensus 2011 McGladrey sold Verisight 2011 Columbia Investments sold Ameriprise 2011 First American Funds Sold Nuveen 2010 NRP sold LPL 2010 NextStep/BenefitStreet sold Verisight 2010 Matrix Sold Broadridge 2010 McCready & Keene sold OneAmerica 2010 Symetra (Mutual Fund Product) Sold Ascensus 2009 ABG MidAtlantic sold BPA 2009 Baden (Clark) Sold Ascensus 2009 Schloss & Co. sold Sentinal (Focus Finncial) 2009 CPI Sold CUNA Mutual 2009 Wachovia Sold Wells Fargo 2009 Merrill Lynch Sold Bank of America 2009 Hand Benefits sold BPA 2009 Putnam sold Power Financial (GreatWest) 2009 CitiStreet Sold ING 2008 401(k)Advisors & RPAG sold NFP 2008 Bisys Sold JC Flowers/Crump 2007 Princeton Retirement Group Sold Hartford 2007 UBOC Sold Prudential 2007 SunLife (MFS) Sold Hartford 2007 Franklin Templeton Sold Great West 2007 Sentinel Benefits Sold Focus Financial 2007 Southeastern Employee Benefits Sold Paychex 2006 Ameriprise Sold Wachovia 2006 MFS Sold SunLife 2006 Invesmart Sold Standard 2006 The 401kCompany Sold Schwab 2006 Ceridian Sold Newport Group 2006 CCA Sold JP Morgan 2006 Cynergy Sold JP Morgan 2006 MetLife Sold Great West 2006 US Bank Sold Great West 2006 Geller & Wind Sold Focus Financial -

PCC Q2 2021 Investor Presentation

Investor Presentation Q2 2021 Quarterly Results August 9th, 2021 Forward looking statements and COVID-19 Forward Looking Statements In the course of today’s meeting, representatives of the Corporation may make, in their remarks or in response to questions, and the accompanying materials may include, statements containing forward-looking information. Certain statements, other than statements of historical fact, are forward-looking statements based on certain assumptions and reflect the Corporation’s current expectations, or with respect to disclosure regarding the Corporation’s public subsidiaries, reflect such subsidiaries’ current expectations as disclosed in their respective Management’s Discussion and Analysis (“MD&A”). Forward-looking statements are provided for the purposes of assisting the listener/reader in understanding the Corporation’s financial performance, financial position and cash flows as at and for the periods ended on certain dates and to present information about management’s current expectations and plans relating to the future and the listener/reader is cautioned that such statements may not be appropriate for other purposes. These statements may include, without limitation, statements regarding the operations, business, financial condition, expected financial results, performance, prospects, opportunities, priorities, targets, goals, ongoing objectives, strategies and outlook of the Corporation and its subsidiaries including the fintech strategy, the expected impact of the COVID-19 pandemic on the Corporation and -

Todd E. Freed

Todd E. Freed Partner, New York Mergers and Acquisitions; Financial Institutions Todd Freed focuses on mergers and acquisitions, corporate finance and private equity, primarily in the financial services industry. Mr. Freed is co-head of the firm’s Financial Insti- tutions Group and leads the firm’s pre-eminent insurance M&A practice, which recently was named Insurance Practice Group of the Year by Law360. He also was named as a Law360 MVP for Insurance M&A. Mr. Freed is a trusted adviser and go-to dealmaker with significant experience representing public and private acquirers and target companies, private equity firms, and investment banks in a variety of U.S. and international mergers and acquisitions, capital-raising transactions, SPACs, joint ventures, restructurings, and other corporate matters. Mr. Freed is a leading practitioner in M&A, contested transactions, activist situations, and corporate governance and regulatory matters. In addition, he advises clients with respect to takeover preparedness, T: 212.735.3714 SEC reporting obligations and cybersecurity matters. F: 917.777.3714 [email protected] Repeatedly, Mr. Freed has been selected for inclusion in Chambers USA: America’s Leading Lawyers for Business; recognized for his leading experience in the insurance industry, includ- ing in The Best Lawyers in America; named as a leading lawyer in the mergers and acquisitions Education category in the IFLR1000; and recognized in Lawdragon 500 Leading Lawyers in America. In J.D., Ohio State University College addition, he was named a 2020 Insurance MVP by Law360 and has consistently been named of Law, 1997 (summa cum laude; a Client Service All-Star by The BTI Consulting Group, recognizing how clients highly value Associate Editor, Ohio State Law and trust Mr. -

Power Financial Corporation

FIRST REPORT QUARTER 2020 POWER FINANCIAL CORPORATION FINANCIAL POWER 1 First Quarter Report For the period ended March 31, 2020 POWER FINANCIAL CORPORATION TABLE OF CONTENTS CORPORATION FINANCIAL POWER PART A This document contains management’s discussion and analysis of the financial condition, financial performance and cash flows of Power Financial Corporation (the Corporation) for the three months ended March 31, 2020 and the unaudited interim condensed consolidated financial statements of the Corporation as at and for the three months ended March 31, 2020. This document has been fi led with the securities regulatory authorities in each of the provinces and territories of Canada and mailed to requesting shareholders of the Corporation in accordance with applicable securities laws. GREAT-WEST LIFECO INC. LIFECO GREAT-WEST PART B PART B POWER FINANCIAL CORPORATION PART A GREAT-WEST LIFECO INC. PART B IGM FINANCIAL INC. PART C PARGESA HOLDING SA PART D IGM FINANCIAL INC. FINANCIAL IGM PART C PART C PARGESA HOLDING SA HOLDING PARGESA PART D PART D POWER FINANCIAL CORPORATION—FIRST QUARTER REPORT 2020 1 PPFC_2020_QUAT1_ENG01_PFC.inddFC_2020_QUAT1_ENG01_PFC.indd 1 22020-05-14020-05-14 55:59:59 PMPM The trademarks contained in this report are owned by Power Financial Corporation or by a Member of the Power Corporation Group of Companies®. Trademarks that are not owned by Power Financial are used with permission. 2 POWER FINANCIAL CORPORATION—FIRST QUARTER REPORT 2020 PPFC_2020_QUAT1_ENG01_PFC.inddFC_2020_QUAT1_ENG01_PFC.indd 2 22020-05-14020-05-14 55:59:59 PMPM POWER FINANCIAL CORPORATION FINANCIAL POWER POWER FINANCIAL CORPORATION PART A PART A MANAGEMENT’S DISCUSSION AND ANALYSIS PAGE A 2 FINANCIAL STATEMENTS AND NOTES PAGE A 44 POWER FINANCIAL CORPORATION—FIRST QUARTER REPORT 2020 A 1 PPFC_2020_QUAT1_ENG01_PFC.inddFC_2020_QUAT1_ENG01_PFC.indd B1B1 22020-05-14020-05-14 55:59:59 PMPM POWER FINANCIAL CORPORATION Management’s Discussion and Analysis MAY 14, 2020 ALL TABULAR AMOUNTS ARE IN MILLIONS OF CANADIAN DOLLARS, UNLESS OTHERWISE NOTED. -

Amundi Index Solutions

AMUNDI INDEX SOLUTIONS SICAV with sub-funds under Luxembourg law Annual report, including Audited Financial Statements for the period from 09/06/16 (date of incorporation) to 30/09/17 AMUNDI INDEX SOLUTIONS Audited annual report R.C.S. Luxembourg B 206.810 For the period from 09/06/16 (date of incorporation) to 30/09/17 Subscriptions are only valid if made on the basis of the current prospectus accompanied by the key investor information document, the latest annual report and the latest semi-annual report if published after the annual report. Table of contents Page Organisation 4 Director’s Report 6 Securities Portfolio as at 30/09/17 AMUNDI INDEX EQUITY EUROPE LOW CARBON 11 AMUNDI INDEX EQUITY GLOBAL LOW CARBON 15 AMUNDI INDEX EQUITY GLOBAL MULTI SMART ALLOCATION SCIENTIFIC BETA 27 AMUNDI INDEX FTSE EPRA NAREIT GLOBAL 39 AMUNDI INDEX MSCI EMERGING MARKETS 43 AMUNDI INDEX MSCI EMU 52 AMUNDI INDEX MSCI EUROPE 55 AMUNDI INDEX MSCI JAPAN 60 AMUNDI INDEX MSCI NORTH AMERICA 63 AMUNDI INDEX MSCI PACIFIC EX JAPAN 70 AMUNDI INDEX MSCI WORLD 72 AMUNDI INDEX S&P 500 87 AMUNDI FTSE 100 92 AMUNDI GLOBAL INFRASTRUCTURE 93 AMUNDI MSCI BRAZIL 94 AMUNDI MSCI USA MINIMUM VOLATILITY FACTOR 95 AMUNDI USA EQUITY MULTI SMART ALLOCATION SCIENTIFIC BETA 96 AMUNDI INDEX BARCLAYS EURO AGG CORPORATE 97 AMUNDI INDEX BARCLAYS EURO CORP BBB 1-5 105 AMUNDI INDEX BARCLAYS GLOBAL AGG 500M 109 AMUNDI INDEX BARCLAYS US CORP BBB 1-5 127 AMUNDI INDEX BARCLAYS US GOV INFLATION - LINKED BOND 132 AMUNDI INDEX J.P. MORGAN EMU GOVIES IG 133 AMUNDI INDEX J.P. -

Canadian Preferred Shares Report

Canadian Preferred Shares Report July 21, 2021 Fixed Income Group The evaporating Preferred market For the first half of 2021, there were only a handful of new issues in the Canadian Performance preferred market and redemptions galore; it was like a kettle filled to the top that keeps boiling over. The S&P/TSX Preferred Share Index continued its upward trend for the 2nd quarter of 2021, through a robust appetite from individual yield seekers, Inside this Report managed products and the continued redemption of outstanding issues. This forced Market Performance ..................... 2 investors to buy less attractive issues and invest more money into ETFs and mutual fund preferred issues. Several factors contributed to this including but not limited Redemptions announced in Q3 2021 ............................................ 2 to: Fund Flows .................................. 2 Negative supply – There has been approx. $5 billion in net redemptions (book value) in 2021. Most issuers redeemed preferred shares (prefs) when it was Market Updates ............................ 2 advantageous to do so. Issuers have not been issuing new paper in exchange, but New Issues in Q2 2021 ................. 3 have been using different venues for financing. The first and second quarters saw Credit Rating Changes ................. 3 very few new issues; so there was a dwindling supply of prefs for a second quarter in a row. Canadian Yield Curve Portfolio Positioning and Where to Look for Opportunities .................. 3 ETF and Fund inflows – With issues being called away and no alternative new issues Highlighted: Preferred Shares…....4 in sight, investors have been pouring money into preferred share ETFs and mutual funds. Approximately $743 million of new money has gone into these two Most Actively Traded………………6 instruments since the beginning of the year. -

Amundi Index Solutions

SEMI- ANNUAL REPORT March 2018 Amundi Index Solutions SICAV with sub-funds under Luxembourg law Management Company Amundi Luxembourg S.A Administrative agent CACEIS Bank, Luxembourg Branch Depositary CACEIS Bank, Luxembourg Branch AMUNDI INDEX SOLUTIONS Unaudited semi-annual report R.C.S. Luxembourg B 206.810 For the period from 01/10/17 31/03/18 Subscriptions are only valid if made on the basis of the current prospectus accompanied by the key investor information document, the latest annual report and the latest semi-annual report if published after the annual report. Table of contents Page Organisation 5 Securities Portfolio as at 31/03/18 AMUNDI INDEX EQUITY EUROPE LOW CARBON 7 AMUNDI INDEX EQUITY GLOBAL LOW CARBON 11 AMUNDI INDEX EQUITY GLOBAL MULTI SMART ALLOCATION SCIENTIFIC BETA 23 AMUNDI INDEX FTSE EPRA NAREIT GLOBAL 36 AMUNDI INDEX MSCI EMERGING MARKETS 40 AMUNDI INDEX MSCI EMU 49 AMUNDI INDEX MSCI EUROPE 52 AMUNDI INDEX MSCI JAPAN 57 AMUNDI INDEX MSCI NORTH AMERICA 60 AMUNDI INDEX MSCI PACIFIC EX JAPAN 67 AMUNDI INDEX MSCI WORLD 69 AMUNDI INDEX S&P 500 84 AMUNDI CAC 40 89 AMUNDI EURO STOXX 50 90 AMUNDI EUROPE EQUITY MULTI SMART ALLOCATION SCIENTIFIC BETA 91 AMUNDI FTSE 100 92 AMUNDI FTSE EPRA EUROPE REAL ESTATE 93 AMUNDI FTSE MIB 94 AMUNDI GLOBAL INFRASTRUCTURE 95 AMUNDI JPX-NIKKEI 400 96 AMUNDI MSCI BRAZIL 98 AMUNDI MSCI EM ASIA 99 AMUNDI MSCI EM LATIN AMERICA 101 AMUNDI MSCI EUROPE 102 AMUNDI MSCI EUROPE EX SWITZERLAND 104 AMUNDI MSCI EUROPE EX UK 105 AMUNDI MSCI EUROPE GROWTH 106 AMUNDI MSCI EUROPE HIGH DIVIDEND FACTOR 107 -

Canadian Investment Grade Preferred Share Fund

CANADIAN INVESTMENT GRADE PREFERRED SHARE FUND INTERIM MANAGEMENT REPORT OF FUND PERFORMANCE For the financial period ended June 30, 2021 CANADIAN INVESTMENT GRADE PREFERRED SHARE FUND CAUTION REGARDING FORWARD-LOOKING TABLE OF CONTENTS STATEMENTS Interim management report of fund performance 1 This report may contain forward-looking statements about the Fund, including Financial highlights 2 its strategy, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer Summary of investment portfolio 3 to future events or conditions, or that include words such as “expects,” Corporate information Back cover “anticipates,” “intends,” “plans,” “believes,” “estimates,” or negative versions thereof and similar expressions. In addition, any statement that may be made concerning future performance, strategies or prospects, and possible future action, is also a forward-looking statement. Forward-looking statements are based on current expectations and projections about future events and are inherently subject to, among other things, risks, uncertainties, and assumptions about the Fund and economic factors. Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made by the Fund. Any number of important factors could contribute to these digressions, including, but not limited to, general economic, political and market factors, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. We stress that the abovementioned list of important factors is not exhaustive. We encourage you to consider these and other factors carefully before making any investment decisions, and urge you to avoid placing undue reliance on forward-looking statements.