Annual Report and Accounts 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

24 June 2019 (Hong Kong Stock Code: 5) HSBC HOLDINGS PLC

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. 24 June 2019 (Hong Kong Stock Code: 5) HSBC HOLDINGS PLC FIRST INTERIM DIVIDEND FOR 2019 On 3 May 2019, the Directors of HSBC Holdings plc declared the first interim dividend for 2019 of US$0.10 per ordinary share. The dividend is payable on 5 July 2019 to holders of record on 17 May 2019 on the Principal Register in the United Kingdom or the Hong Kong Overseas Branch Register or the Bermuda Overseas Branch Register. The dividend is payable in cash in United States dollars, sterling or Hong Kong dollars, or a combination of these currencies, and with a scrip dividend alternative. Dividends payable in cash in Hong Kong dollars or sterling were converted from United States dollars at the forward exchange rates quoted by HSBC Bank plc in London at or about 11.00 am on 24 June 2019 (US$1=HK$7.812757 and £1=US$1.276039). Accordingly, the cash dividend payable on 5 July 2019 will be: US$0.10 per share; approximately HK$0.781276 per share; or approximately £0.078368 per share. For holders of American Depositary Shares ('ADSs'), each of which represents five ordinary shares, the cash dividend payable will be US$0.50 per ADS. -

Participant Bios

Johan Aalto Senior Partner, Hannes Snellman PRACTICE AND EXPERIENCE Johan Aalto is Hannes Snellman’s Senior Partner. He specializes in mergers and acquisitions, corporate finance and capital markets, with an emphasis on public takeovers. During the last few years, Johan has been involved in some of the largest and most complex transactions in Finland. He also focuses on corporate governance issues and acts as the chairman of general meetings of several listed companies in Finland. Johan has been awarded the honorary title Lagman by the President of the Republic of Finland. MEMBERSHIPS AND POSITIONS OF TRUST • Member of the committee preparing the first Finnish guidelines on takeovers (the Helsinki Takeover Code), 2007 • Board memberships in several companies • Member of the Finnish Bar Association, 1991 EDUCATION AND PROFESSIONAL BACKGROUND • Senior Partner, 2009 • Managing Partner, Hannes Snellman, 2005-2009 • Partner, Hannes Snellman, 1994 • Master of Laws, University of Helsinki, 1987 Nigel Boardman Partner, Slaughter and May Nigel’s broad practice includes domestic and international corporate finance, mergers and acquisitions, joint ventures, IPOs, demergers, private acquisitions and disposals, private equity, public takeovers, issues of compliance and corporate governance, investigations and insolvency, restructurings, investigations and sports law. Nigel has received a number of accolades, including: • The Financial Times’ Special Achievement Award • Chambers Directories Lifetime Achievement award • Lawyer of the Decade award from Financial News (2015) • included in Debrett’s ‘Who’s Who’ • ranked as a “star performer” for Corporate and M&A work by Chambers in its U.K., Europe and Global directories • identified as a “Thought Leader” for M&A and Corporate Governance work in Who’s Who Legal: Thought Leaders 2017 Nigel is a consulting editor of the Oxford University Press’ ‘Annotated Companies Acts’ and is on the Editorial Board of the ‘Journal for Corporate and Commercial Law and Practice’. -

CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) And

HUTCHISON WHAMPOA INTERNATIONAL (03/33) LIMITED (the “Issuer”) US$1,500,000,000 7.45% Guaranteed Notes due 2033 (the “Notes”) (ISIN: US44841SAC35/CUSIP: 44841SAC3/Common Code: 018124572 for Rule 144A Notes) (ISIN: USG4672CAC94/CUSIP: G4672CAC9/Common Code: 018124629 for Regulation S Notes) unconditionally and irrevocably guaranteed by CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) and HUTCHISON WHAMPOA LIMITED In accordance with Regulation (EU) No. 596/2014 on market abuse and the law of 11 January 2008 on transparency requirements, as amended, the Issuer is filing with the Commission de Surveillance du Secteur Financier, storing with the Officially Appointed Mechanism and publishing the attached unaudited results for the six months ended 30 June 2019 of CK Hutchison, a guarantor of the Notes issued by the Issuer. The attached document was also published by CK Hutchison at 4:31 pm and 4:32 pm (Hong Kong time), 1 August 2019 on the websites of Hong Kong Exchanges and Clearing Limited and CK Hutchison, respectively. Hutchison Whampoa International (03/33) Limited Edith Shih Director and Company Secretary 1 August 2019 Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2019 HIGHLIGHTS -

Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD

UOB KAY HIAN (SINGAPORE) PRIVATE LIMITED MARGIN STOCK LIST - HONG KONG MARKET 1 April 2021 Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD. SA HK 2 CLP HOLDINGS LTD. A HK 3 HONG KONG AND CHINA GAS CO. LTD. A HK 4 WHARF (HOLDINGS) LTD. A HK 5 HSBC HOLDINGS PLC SA HK 6 POWER ASSETS HOLDINGS LTD. SA HK 8 PCCW LTD. C HK 10 HANG LUNG GROUP LTD. A HK 11 HANG SENG BANK LTD. SA HK 12 HENDERSON LAND DEVELOPMENT CO. LTD. A HK 14 HYSAN DEVELOPMENT CO. LTD. B HK 16 SUN HUNG KAI PROPERTIES LTD. SA HK 17 NEW WORLD DEVELOPMENT CO. LTD. A HK 19 SWIRE PACIFIC LTD. 'A' A HK 23 BANK OF EAST ASIA, LTD. A HK 27 GALAXY ENTERTAINMENT GROUP LTD. A HK 38 FIRST TRACTOR CO LTD. - H SHARES D HK 41 GREAT EAGLE HOLDINGS LTD. C (Max Net Loan H$10M) HK 45 HONGKONG AND SHANGHAI HOTELS, LTD. B (Max Net Loan H$10M) HK 53 GUOCO GROUP LTD. B (Max Net Loan H$10M) HK 56 ALLIED PROPERTIES (HK) LTD. D HK 62 TRANSPORT INTERNATIONAL HOLDINGS LTD. D (Max Net Loan H$1M) HK 66 MTR CORPORATION LTD. SA HK 69 SHANGRI-LA ASIA LTD. A HK 81 CHINA OVERSEAS GRAND OCEANS GROUP LTD. C HK 83 SINO LAND CO. LTD. A HK 86 SUN HUNG KAI & CO. LTD. D HK 87 SWIRE PACIFIC LTD. 'B' A (Max Net Loan H$10m) HK 101 HANG LUNG PROPERTIES LTD. A HK 107 SICHUAN EXPRESSWAY CO. -

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 128.4 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 69.3 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.3 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 57.5 4 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 37.7 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 32.6 6 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 32.0 7 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.5 8 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 26.5 9 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.4 10 15 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 19.4 11 10 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 18.9 12 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.3 13 13 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 17.9 14 11 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.8 15 14 HK0688002218 6192150 0688.HK 619215 China Overseas Land & Investme CN HKD Y 14.8 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 14.6 17 17 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 13.5 18 19 HK0003000038 6436557 0003.HK 643655 Hong Kong & China Gas Co. -

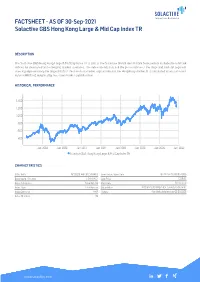

FACTSHEET - AS of 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR

FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR DESCRIPTION The Solactive GBS Hong Kong Large & Mid Cap Index TR is part of the Solactive Global Benchmark Series which includes benchmark indices for developed and emerging market countries. The index intends to track the performance of the large and mid cap segment covering approximately the largest 85% of the free-float market capitalization in the Hong Kong market. It is calculated as a totalreturn index in HKD and weighted by free-float market capitalization. HISTORICAL PERFORMANCE 1,400 1,200 1,000 800 600 400 Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018 Jan-2020 Jan-2022 Solactive GBS Hong Kong Large & Mid Cap Index TR CHARACTERISTICS ISIN / WKN DE000SLA4H36 / SLA4H3 Base Value / Base Date 462.12 Points / 08.05.2006 Bloomberg / Reuters / .SHKLMCT Last Price 1256.93 Index Calculator Solactive AG Dividends Reinvested Index Type Total Return Calculation 8:00 am to 10:30 pm (CET), every 15 seconds Index Currency HKD History Available daily back to 08.05.2006 Index Members 52 FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -6.80% -10.27% -11.73% 9.67% -4.51% 171.99% Performance (p.a.) - - - - - 6.71% Volatility (p.a.) 21.54% 18.63% 16.63% 17.91% 18.51% 20.09% High 1364.34 1419.58 1482.24 1493.61 1493.61 1493.61 Low 1228.29 1228.29 1228.29 1115.51 1228.29 287.41 Sharpe Ratio -2.67 -1.91 -1.34 0.55 -0.32 0.33 Max. -

RBI's 1St Ever CFO & Other Influential Women in Banking & Business

RBI's 1st Ever CFO & Other Influential Women in Banking & Business Sector! In the advanced era, women are taking charge of almost every sector from creating new business, acquiring companies and representing some of the top banks and financial institutions in the country. Where Ms. Sudha Balakrishnan has been appointed as the Chief Financial Officer (CFO) of the Reserve Bank of India; Indra Nooyi, CEO of PepsiCo is the common resident of Forbes List of Most Powerful Women & Influential Businesswomen in the World. There are many such exceptional professionals who are taking decisions that affect future of millions of people across the country and the globe. Here's the list of Most influential Indian Women in Banking & Business sector. If you are preparing for SSC, Banking or other Government Exams, it is very important that you know about these women, their career trajectory and importance of their business and work as you are bound to have questions based on this list in the General Awareness section of these exams. Most Influential Women in Banking and Business Sector The following list encompasses the most Powerful Women in Banking and Business Sector. All of them have found places in the Top 100 or Top 50 in surveys conducted by international firms like Forbes and Fortune. Let’s have a look at some top notch influential women, which are important from the exam point of view. 1 | P a g e 1. SUDHA BALAKRISHNAN • Former Executive of National Securities Depository Limited, Sudha Balakrishnan has been appointed as the first Women Chief Financial Officer of Reserve Bank of India (RBI) adding another feather to her cap. -

Chryscapital Wins VCC Circle Fund Manager of the Year

4/1/2019 Morgan Stanley buys majority stake in warehouse developer KSH Infra HOME (HTTPS://WWW.VCCIRCLE.COM/) / FINANCE (HTTPS://WWW.VCCIRCLE.COM/INDUSTRY/FINANCE) FINANCE (HTTPS://WWW.VCCIRCLE.COM/INDUSTRY/FINANCE) Mankind Pharma, IIFL Wealth, Byju's, ChrysCap, KKR among winners of VCCircle Awards By Debjyoti Roy (https://www.vccircle.com/author/debjyoti-roy) 14 February, 2019 Winners of VCCircle Awards 2019 Drugmaker Mankind Pharma Ltd, ed-tech venture Byju's, homegrown private equity rm ChrysCapital and global alternative asset manager KKR are among the winners of the VCCircle Awards 2019. The annual awards, now in their eighth year, felicitate PE- and venture capital-backed companies in key sectors as well as investment funds, law rms and investment bankers. The winners were awarded on Thursday as part of the VCCircle India Limited Partners Summit 2019, held at ITC Grand Central in Mumbai. The winners were chosen based on the recommendation of an eminent ve-member jury. The jury comprised Keki Mistry, CEO at Housing Development Finance Corporation; Gopal Srinivasan, chairman and managing director at TVS Capital Funds Ltd; Michael Liu, senior vice president at Portfolio Advisors; Sameer Garde, president (India and SAARC), Cisco; and Anjali Bansal, founder of Avaana Capital. Plastic products maker Supreme Industries Ltd; IIFL Wealth Management Ltd, a unit of nancial services company IIFL Holdings; Mahindra & Mahindra Ltd, part of the diversied Mahindra Group; HL Agro Products, one of the country’s top exporters of sesame seeds and corn products; and Bangalore International Airport Ltd bagged the portfolio company awards in their respective sectors. The awards also recognised top PE and VC fundraisers, as also the exit of the year based on annualised return, or the internal rate of return (IRR). -

Speaker Biographies

Speaker Biographies Ope Adebanjo ’20, Student, Harvard Law School Ope Adebanjo is a second year JD Candidate at Harvard Law School. She graduated from Harvard College in 2015 and majored in Comparative Literature and African Studies, with a minor in Sociology and a citation in Yoruba. Ope worked as an operations supervisor at McMaster-Carr Supply Company in Atlanta GA, managing teams of e-commerce and sales representatives and managing warehouse projects and operations during her time before law school. She also has her Masters in International Business from J. Mack Robinson College of Business at Georgia State University. As a HLS student, Ope is interested in intellectual property law and international business law with a focus on the intersection of policy and technology. Kendra Albert ’16, Clinical Instructional Fellow, Cyberlaw Clinic, Harvard Law School Kendra is a clinical instructional fellow at the Cyberlaw Clinic at Harvard Law School, where they teach students how to practice law by working with pro bono clients. Previously, they were an associate at Zeitgeist Law PC, a boutique technology law firm in San Francisco, and a research associate at the Berkman Klein Center for Internet and Society. Kendra’s scholarship and academic work touches on diverse issues, from online harassment to linkrot to video game preservation. They hold a JD cum laude from Harvard Law School and a bachelor’s degree in lighting design and history from Carnegie Mellon University. Julie Anna Alvarez ’88, Director of Alumni and International Career Services, Columbia Law School Julie Anna Alvarez is the Director of Alumni and International Career Services at Columbia Law School’s Office of Career Services and Professional Development. -

Hsbc Appoints David Liao and Surendra Rosha As Co-Chief Executives for Asia Pacific

News Release 7 June 2021 HSBC APPOINTS DAVID LIAO AND SURENDRA ROSHA AS CO-CHIEF EXECUTIVES FOR ASIA PACIFIC Peter Wong retires as Asia Pacific CEO and becomes non-executive Chairman of The Hongkong and Shanghai Banking Corporation (HBAP) HSBC today announces that David Liao and Surendra Rosha have been appointed Co-Chief Executives of HSBC Asia Pacific, taking over from Peter Wong with immediate effect. David, formerly Head of Global Banking Asia Pacific, and Surendra (known widely by his last name, Rosha), formerly CEO of HSBC India, will share pan- regional leadership responsibilities that include jointly leading regional businesses and functions, embedding purpose, values and culture, developing leadership and talent and overseeing risk, capital and liquidity levels. David and Rosha will be promoted to Group Managing Director and will join the HBAP Board as Executive Directors. They will be based in Hong Kong, reporting directly to Noel Quinn, Group Chief Executive and will join the Group Executive Committee. The region will continue to be run as a single entity, jointly managed. David and Rosha will share the reporting lines for the markets in Asia Pacific between them. Peter will step into the role of non-executive Chairman of HBAP, replacing Laura Cha, who has also stepped down as non-executive Director of HSBC Holdings. He will also serve as an adviser to Group Chairman Mark Tucker and Group CEO Noel Quinn. “I am very excited to have David and Rosha join the Group Executive Committee. Their collective experience of our markets across Asia Pacific, together with their combined knowledge of the bank and our customers mean they are ideally placed to grow the business. -

You Haven't Seen Anything

(220000 ( BEST UNDER A BILLION PRICE RS. 100. AUGUST 17, 2012 INDIA YOU HAVEN’T SEEN ANYTHING Ratan Tata’s corporate innings was spectacular. Now, he’s ready to take YET the Tata trusts to the next level. www.forbesindia.com Letter From The Editor Goodbye Tata, Hello World! very year, after we publish before perspective on how the trusts the much-awaited Forbes list have evolved—but also why they’re E of the 100 Richest Indians, shortly set for a radical rethink. I invariably get letters from readers On December 28 this year, when Ratan enquiring why Ratan Naval Tata’s Tata turns 75, it will bring the curtains name is missing from our list. I’ve down on one of the most impactful even had a few foreign journalists tenures in India Inc. However, if you’re EVEN THOUGH THEIR based in India and abroad call me to expecting Tata to hang up his boots and WORK HAS TOUCHED enquire whether the unique ownership settle into a quiet life of retirement inside SEVERAL MILLION model—where a set of trusts own 66 his newly built sea-facing mansion in INDIANS OVER MANY percent of Tata Sons—was for real. Colaba in the southern tip of Mumbai, DECADES, THERE HAS For decades, the workings of the trusts you could be in for a surprise. SELDOM BEEN ANY have remained shrouded in secrecy. Unknown to the world, Tata has ATTEMPT TO CLAIM Despite several attempts in the past, been actively preparing for a plunge CREDIT OR SEEK no media publication has succeeded into the world of philanthropy. -

Board Appointment the Hong Kong and Shanghai Banking Corporation

News Release 23 November 2020 BOARD APPOINTMENT THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED The Hongkong and Shanghai Banking Corporation Limited has appointed Cheng Chi Man (Sonia Cheng) as an Independent Non-executive Director of the Bank. Ms Cheng is currently the Chief Executive Officer of Rosewood Hotel Group. She is an executive director of New World Development Company Limited and a non-executive director of Chow Tai Fook Jewellery Group Limited, both listed on The Stock Exchange of Hong Kong Limited. She is also a director of New World China Land Limited. Laura Cha, Chairman of the Board of The Hongkong and Shanghai Banking Corporation, commented: “Sonia’s wealth of experience in our key markets of Hong Kong and mainland China will be a great fit to the Board of The Hongkong and Shanghai Banking Corporation, the flagship Asian entity of the HSBC Group. Her proven expertise in spearheading global expansion of her hotel brands will also bring value to our internationally focused business.” Ms Cheng will also be a member of The Hongkong and Shanghai Banking Corporation Limited’s Risk Committee. ends/more This news release is issued by Registered Office and Head Office: The Hongkong and Shanghai Banking 1 Queen’s Road Central, Hong Kong SAR Web: www.hsbc.com.hk Corporation Limited Incorporated in the Hong Kong SAR with limited liability Note to editors: Photo Caption Sonia Cheng has been appointed Independent Non-executive Director of The Hongkong and Shanghai Banking Corporation Limited. The Hongkong and Shanghai Banking Corporation Limited The Hongkong and Shanghai Banking Corporation Limited is the founding member of the HSBC Group.