Mvw 2020-1 Llc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Premier Tier List 2019

INTERVAL INTERNATIONAL® 2019 RESORT RECOGNITION PROGRAM Interval International Premier Resorts provide an outstanding vacation experience, with state-of-the-art conveniences and modern features and appointments. 2019 2019 Florida, Miami South Carolina, Myrtle Beach Area Vermont Eastern U.S.A. Marriott’s Villas at Doral |VD M Dunes Village Resort | TDU & DVL Trapp Family Lodge Guest Houses | TFL & TF2 Owners Quarters at Crescent Shores |CX T CENTRAL FLORIDA Florida, Miami Beach Sheraton Broadway Plantation |W ST Florida, Orlando Marriott Vacation Club Pulse®, South Beach |B MQ Western U.S.A. CLC Encantada |TD E Tennessee, Gatlinburg Grand Beach | EGE & EG2 Florida, Naples and Marco Island Bent Creek Golf Village |NT B MIDWEST Lighthouse Key Resort & Spa | LKE Charter Club Resort of Naples Bay | CHN & CH1 Michigan Marriott’s Harbour Lake |Z MH Eagle’s Nest on Marco Beach |L EG Virginia, Virginia Beach The Inn at Bay Harbor | INB & LKQ Marriott’s Imperial Palms | MIP The Surf Club of Marco |M SC Boardwalk Resort and Villas |W TR Vacation Club 1 | VPN Marriott’s Royal Palms |P MR Ocean Beach Club and Oceanaire at Marriott’s Sabal Palms | MSP Florida, The Palm Beaches Ocean Beach Club | OCB & OCI Minnesota Mystic Dunes Resort & Golf Club |CC P Marriott’s Ocean Pointe |PB M Turtle Cay Resort |TL T The Village at Izatys | VIZ Parkway International Resort | PKY, PK1 & PK2 Sheraton Vistana Resort | VIT & VIO Virginia, Williamsburg Missouri, Branson Star Island Resort |BR V Florida, Panhandle The Colonies at Williamsburg |WQ C The Falls Village -

Marriott Bonvoy

B:24.5” T:24” S:23.5” ELITE ELITE-LEVEL BENEFITS AT A GLANCE PARTICIPATING BENEFIT DESCRIPTION BRANDS MARRIOTT BONVOY™ GOLD ELITE 25 Nights/Year MARRIOTT BONVOY™ SILVER ELITE 10 Nights/Year MARRIOTT BONVOY™ PLATINUM ELITE 50 Nights/Year MARRIOTT BONVOY™ TITANIUM ELITE 75 Nights/Year MARRIOTT BONVOY™ AMBASSADOR ELITE 100 NIights + $20K Rev/Year A member is matched with a personal Ambassador (above property), who is the member’s point person for every stay. Ambassador Service is the highest level of service All brands Ambassador Service l for members. All brands except Marriott Vacation Club® Flexibility to check in and out of the room outside of normal arrival and departure times. For example, check in at 9 p.m. and check out at 9 p.m. Requests for Your24 and participating Vistana™ properties Your24™ l are communicated through Ambassadors. and Design Hotels™ All brands except resorts, 48-Hour Guarantee Marriott Vacation Club, and participating l l Guaranteed room availability for reservations booked 48 hours prior to arrival (at Residence Inn and TownePlace Suites, benefit applies to studio room only). Vistana properties and Design Hotels™ • JW Marriott® Access to lounge for member plus one guest. This benefit only applies to the one guest room in which the Platinum Elite/Titanium Elite/Ambassador Elite member is staying. • Marriott Hotels® • Delta Hotels® Brand Lounge Offer Guest Compensation2 • Autograph Collection® Hotels US$100 if no breakfast • Renaissance® Hotels US/CAN: If lounge is closed or hotel does not have a lounge, offer -

It's Your Big Day, Be Swept Away

IT’S YOUR BIG DAY, BE SWEPT AWAY. Courtyard by Marriott SpringHill Suites Charlotte University Research Park Charlotte University Research Park 333 West W.T. Harris Blvd. 8700 Research Drive Charlotte, NC 28262 Charlotte, NC 28262 CourtyardCharlotteUniversity.com SpringHillSuitesCharlotteUniversity.com +1-704-549-4888 +1-704-503-4800 With so many details to keep track of, why not give us a few? CUSTOMIZE YOUR EXPERIENCE BY CHOOSING 3 PERKS: • One bottle of champagne and gourmet chocolates • One suite for up to 3 nights • Enjoy 50% off Sunday night stays • Welcome gift for each guest • Distribution of your gift bags to all guests • Customized welcome letter given to guests with directions to and from ceremony and reception venues • Breakfast for all guests staying at the hotel • Use of the meeting room during your stay (limited availability) • Turn-down service • Double Marriott Rewards® Points for guests who are Marriott Rewards Members • 2 p.m. Late check-out for all guests • 1-night stay for the couple on their 1 year anniversary For rates and information, contact Alexandra Dean at 704-281-5218 or [email protected] 10 or more room nights required. Offer cannot be combined with any other promotions. Blackout dates may apply. Other restrictions apply. REWARDING EVENTSSM L-R: Warner Center Marriott® Woodland Hills, CA; JW Marriott® Hotel Pune, India; JW Marriott Phuket Resort & Spa, Thailand; Renaissance® Austin Hotel, TX REWARDING EVENTS REWARDS YOU We know that successful meetings and events don’t just happen on their own. It all starts with a plan—and a planner. That’s why we’ve created a way to help you make the most of your choices. -

Download the Interval Sales Pages, Search the Tool Kit App to Access the Publication, Zoom in and N Mailing Address Magazine

APRIL – JUNE 201 5 A PUBLICATION OF INTERVAL LEISURE GROUP PROFILES ANANTARA VACATION CLUB | BRECKENRIDGE GRAND VACATIONS | DIVI RESORTS GROUP HOTEL DE L’EAU VIVE | PALACE RESORTS | SIMPSON BAY RESORT & MARINA | WELK RESORTS GROWING GLOBAL REACH The Interval Presence in the Americas, Asia, and Beyond The Allure of the Has Industry Lending New Trends in Urban Vacation Turned the Corner? Kitchen Design APRIL – JUNE 2015 vacation industry review RESORTDEVELOPER.COM CONTENTS page 38 S E L I F O R W P E I V Divi Resorts Group Y E Branching out in New Directions 30 R R E Palace Resorts E N I 30 Years and Growing 34 V U E LOS CABOS S Anantara Vacation Club S N I Rapid Rebound After Odile 8 Ready for Asia’s Middle-Class Boom 38 I TIMESHARE TALK Hotel de L’Eau Vive VIEWPOINT Industry Lending Turns the Corner 14 Struggle and Triumph in New Orleans 4 2 Living in Interesting Times 4 TRENDS Welk Resorts The Allure of Urban Vacations 18 Five Decades of Focus on the Guest 4 4 INSIDER Benefits, News, FROM THE GROUND UP Breckenridge Grand Vacations Updates, and More 6 New Trends in Kitchen Design 22 Best Address for Year-Round Fun 46 PULSE AFFILIATIONS Simpson Bay Resort & Marina People and Global Expansion for Interval 27 A Caribbean Jewel Restored 5 0 Industry News 59 executive editor creative director photo editor advertising y s c Torey Marcus Ailis M. Cabrera Kimberly DeWees Nicole Meck n US$1 €0.89, £0.65 n Interval International o i editor-in-chief senior graphics assistant vice president e s 949.470.8324 r r Betsy Sheldon manager graphics and production r £1 US$1.54, 1.38 e € John Cavaliere Janet L. -

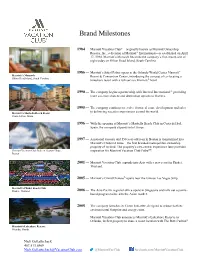

Brand Milestones

Brand Milestones 1984 — Marriott Vacation Club®—originally known as Marriott Ownership Resorts, Inc., a division of Marriott® International—is established on April 17, 1984. Marriott’s Monarch becomes the company’s first resort, one of eight today on Hilton Head Island, South Carolina. 1986 — Marriott’s Sabal Palms opens at the Orlando World Center Marriott® Marriott’s Monarch Resort & Convention Center, introducing the concept of co-locating a Hilton Head Island, South Carolina timeshare resort with a full-service Marriott® hotel. 1990 — The company begins a partnership with Interval International®, providing more vacation choices and destination options to Owners. 1995 — The company continues to evolve from real estate development and sales Marriott’s Marbella Beach Resort to delivering vacation experiences around the world. Costa del Sol, Spain 1996 — With the opening of Marriott’s Marbella Beach Club in Costa del Sol, Spain, the company expands into Europe. 1997 — A national treasure and 150-year-old icon in Boston is transformed into Marriott’s Custom House—the first branded metropolitan ownership property of its kind. The property’s city-centric experience later provides Marriott Vacation Club Pulse at Custom House, inspiration for Marriott Vacation Club PulseSM. Boston 2001 — Marriott Vacation Club expands into Asia with a new resort in Phuket, Thailand. 2005 — Marriott’s Grand Chateau® opens near the famous Las Vegas Strip. Marriott’s Phuket Beach Club Phuket, Thailand 2006 — The Asia-Pacific regional office opens in Singapore and rolls out a points- based program tailored to the Asian market. 2008 — The company launches its Green Initiative, designed to reduce both its environmental footprint and energy costs. -

Marriott International Is Getting Slimed! and That's a Good Thing!

Marriott International is Getting Slimed! And That's a Good Thing! Nickelodeon and Marriott International Enter into Global Partnership to Create New Branded Hotel Experience 20 New Resorts Around the World Expected by 2020; First Hotel Expected to Open in San Diego in 2010 NEW YORK, May 31, 2007 (BUSINESS WIRE) -- Marriott International, Inc. (NYSE: MAR), Nickelodeon, a unit of Viacom International, Inc.'s (NYSE: VIA B), MTV Networks, and Miller Global Properties, LLC, an international real estate investment and development company, today announced an agreement to co-develop a breakthrough new lodging resort brand and concept for travelers seeking fun and adventure, "Nickelodeon Resorts by Marriott," with 20 potential hotels expected to be under construction by 2020. The new upscale, self-contained destination resorts will be developed through a collaboration among Nickelodeon, the world's number-one entertainment brand for kids, with 35 channels reaching approximately more than 200 million households in 135 countries; Marriott International, which has nearly 2,900 hotels in 68 countries; and Miller Global Properties. Miller Global will have certain exclusive rights to develop and own the resorts in specified geographic areas, and plans to seed an investment fund that is expected to initially provide $300 million of dedicated development equity capital. All "Nickelodeon Resorts by Marriott" properties will be managed by Marriott. The first "Nickelodeon Resorts by Marriott" property is expected to be a 650-room resort at Liberty Station in San Diego, which will incorporate a 100,000 square-foot water park and activity deck complex featuring a variety of pools and interactive attractions. -

The Changing Face of Timeshare in Europe

Hospitality Directions Europe Edition* Issue 12 September 2005 The changing face of timeshare in Europe Timeshare was originally a European idea but has proved to be a concept that has developed fastest in the USA. Indeed, predictions of explosive growth for timeshare in Europe have not been borne out, despite the fact that there are now around 1.3 million timeshare owners in Europe compared with 460,000 in 1990. Why then should European timeshare appear less dynamic than in the USA? What are the prospects for the sector in Europe from the investor/developer’s point of view? This study looks at timeshare and its derivatives in Europe – such as fractional ownership, Private Residence Clubs and points clubs. The evidence suggests that timeshare from the developer’s standpoint has the potential to earn above-average rates of return, but that its long-term future in Europe depends on a number of key factors. Chief among these is the extent to which the current legislative and regulatory environment, which has been built by national legislatures around the framework of the European Union’s 1997 Timeshare Directive, can be more closely harmonised across Europe and a better balance achieved between the interests of the consumer and those of the developer. The second key influence is the extent of the involvement of some of the major branded hotel companies in the timeshare sector. In the USA, major companies such as Hilton, Marriott, Disney and Starwood have entered the industry, raising the profile and credibility of timeshare as a consequence. In Europe, branded hotel companies are now entering and/or expanding their activities in timeshare, helping to counteract some of the negative images that have dogged the sector in the past. -

The Marriot Hotel Group Collection and Earning Structure

THE MARRIOT HOTEL GROUP COLLECTION AND EARNING STRUCTURE Brand Brand Description Logo Earning Structure Conversion Structure Contact Information JW Marriott® At Marriott's most elegant and luxurious 2 miles per US$ spent on brand, little touches add up to all qualifying charges exceptional experiences. JW Marriott luxury hotels and resorts provide business and leisure travelers with simple elegance, an inviting atmosphere, and a deluxe level of comfort and personal service on their terms. Autograph The Autograph Collection is an evolving 2 miles per US$ spent on ensemble of strikingly independent all qualifying charges Collection® hotels. Each destination has been selected for its bold originality, rich Hotels character and uncommon details. From near to far, iconic to historic, the result is an array of properties that is nothing less than unique, nothing short of collectively exceptional. Renaissance Travel should be inspiring. At 2 miles per US$ spent on Renaissance Hotels worldwide, you'll all qualifying charges Hotels® find inspiration at every location. Rewards Points Choose from one of our historic icons, 1,500 Miles = 10,000pts chic boutiques or luxurious resorts. Each offers its own personality, local 3,500 Miles = 20,000pts flavor, distinctive style and charm. All 7,000 Miles = 30,000pts See Table on Page 5 will stimulate your appetite for 17,500 Miles = 70,000pts discovery. 35,000 Miles = 140,000pts Our Flagship brand of quality-tier, full- Marriott 2 miles per US$ spent on service hotels & resorts provides all qualifying charges Hotels® consistent, dependable, and genuinely caring experiences to guests on their terms. Features include fully equipped fitness centers, gift shops, swimming pools, Concierge levels, business centers, and meeting facilities. -

Public Offering Statement for a State of Washington Timeshare Registration

PUBLIC OFFERING STATEMENT FOR A STATE OF WASHINGTON TIMESHARE REGISTRATION Name of Promoter: Vacation Ownership Sales, Inc. Name of Timeshare Plan: Vacation Internationale Program PURCHASER CANCELLATION RIGHTS RCW 64.36.150 As a prospective purchaser, you may, for seven days following execution of an agreement to purchase a timeshare, cancel the agreement and receive a refund of any consideration paid by providing written notice of the cancellation to the promoter or the promoter’s agent. If you did not receive the disclosure document, the agreement is voidable by the purchaser until the purchaser receives the document and for seven days thereafter. You may cancel your contract without any cancellation fee or other penalty, or stated reason for doing so, by mailing or by hand delivering a notice of cancellation to: Vacation Ownership Sales, Inc., 1417 – 116th Avenue NE, Bellevue, WA 98004; Attn: Contracts Administration. EACH PROSPECTIVE PURCHASER SHALL BE PROVIDED A PUBLIC OFFERING STATEMENT PRIOR TO THE EXECUTION OF ANY AGREEMENT FOR THE PURCHASE OF A TIMESHARE Purchasers who believe that conditions are not as stated in the Public Offering Statement are requested to contact the Department of Licensing, Business and Professions Division, Timeshare Section, P.O. Box 9021, Olympia, Washington 98507-9021. WA POS (FY 2020-21) Page 1 of 27 PUBLIC OFFERING STATEMENT FOR A STATE OF WASHINGTON TIMESHARE REGISTRATION TABLE OF CONTENTS NAME AND ADDRESS OF PROMOTER, AND ITS DIRECTORS AND OFFICERS ..................... 4 LOCATION AND GENERAL DESCRIPTION OF TIMESHARE PROPERTY ................................ 4 A. Type of Plan and Time Share Interest Received ....................................................................... 4 (1) Right to Use Plan; How Title is Held Generally ...................................................................... -

For Immediate Release Marriott Vacation Club Appoints New General Manager at Marriott's Canyon Villas at Desert Ridge

FOR IMMEDIATE RELEASE MARRIOTT VACATION CLUB APPOINTS NEW GENERAL MANAGER AT MARRIOTT’S CANYON VILLAS AT DESERT RIDGE ORLANDO, Fla., - October 1, 2008 – Marriott Vacation Club International – the vacation ownership division of Marriott International, Inc. (NYSE:MAR) – has appointed Sue Tan-Graf to general manager at Marriott’s Canyon Villas at Desert Ridge in Phoenix, Ariz. A 14-year Marriott veteran, Tan-Graf comes to Marriott’s Canyon Villas at Desert Ridge with extensive experience in the industry. Tan-Graf began her career with Marriott as a front desk associate at the Overland Park Marriott in Kansas. From there she was promoted to assistant housekeeping manager and later to director of services at the Santa Clara Marriott in California. In 2000, Tan-Graf joined MVCI where she held many leadership roles including assistant front office manager and director of services at Marriott’s Desert Springs Villas in Palm Desert, Calif., director of facilities at Marriott’s MountainSide in Park City, Utah and director of customer experience at Marriott’s Shadow Ridge in Palm Desert. Then in 2006, she was promoted to director of customer experience for the Marriott Vacation Club West region. “Throughout her career, Sue has demonstrated a strong work ethic and a great passion for service,” said Jane Berg, regional vice president of customer experience for the West region. “I am confident her versatile experience and leadership skills will carry through to her new role at Marriott’s Canyon Villas, where Sue will be a tremendous asset.” In her most recent role, Tan-Graf served as general manager of Marriott’s Custom House in Boston where she and her associates won Marriott Vacation Club International’s World-Class Resort Award and received the highest scores in “owner satisfaction” for the division in 2007. -

Timeshare As a Strategy in Tourism Investment: the Case of Croatia Rick Lagiewski

Rochester Institute of Technology RIT Scholar Works Presentations and other scholarship Faculty & Staff choS larship 2005 Timeshare as a strategy in tourism investment: the case of Croatia Rick Lagiewski Damon Revelas Follow this and additional works at: https://scholarworks.rit.edu/other Recommended Citation Damon A. Revelas and Richard “Rick” M. Lagiewski. “Timeshare as a strategy in tourism investment: the case of Croatia." This Conference Paper is brought to you for free and open access by the Faculty & Staff choS larship at RIT Scholar Works. It has been accepted for inclusion in Presentations and other scholarship by an authorized administrator of RIT Scholar Works. For more information, please contact [email protected]. TIMESHARE AS A STRATEGY IN TOURISM INVESTMENT: THE CASE OF CROATIA Damon A. Revelas Roger A. Saunders School of Hotel & Restaurant Management Boston, Massachusetts Richard “Rick” M. Lagiewski Rochester Institute of Technology Rochester, New York ABSTRACT The purpose of this paper is to examine how timeshare strategy can assist tourism investment in the lodging sector within a transitional economy. Specifically, the study describes initial timeshare operations in Croatia, an example of a transitional country, steeped in tourism tradition. Moreover, the discussion identifies benefits and challenges to timeshare implementation for hotel companies, when applied to broader tertiary perspectives. By using the case study approach, a record of events that lead to establishing timeshare operations should serve as a collaborative example to other developers, investors, hotel companies and legal entities that may attempt similar projects in other transitional tourism countries. Key words: Timeshare, transitional economy, tourism, hotel investment, and strategy INTRODUCTION The former Yugoslavia was a multi-ethnic state in southeast Europe divided administratively between six republics: Bosnia-Herzegovina, Croatia, Macedonia, Montenegro, Serbia, and Slovenia. -

Enjoying Your Vacation Options

Enjoying Your Vacation Options Marriott Vacation Club® has created the most flexible and exciting vacation ownership program available—the Marriott Vacation Club Destinations™ program. This guide will help you understand and maximize your options. As a Marriott Vacation Club Destinations Owner and through the Marriott Vacation Club Destinations Exchange Program, you can use Vacation Club Points for a variety of experiences within four flexible collections of vacation options: Marriott Vacation Club® Resorts – Enjoy a vacation at any of more than 50 Marriott Vacation Club resorts in the U.S., the Caribbean, Europe and Asia. Marriott Rewards® – Redeem your Vacation Club Points for Marriott Rewards points and stay at more than 3,800 Marriott® hotels worldwide. Explorer Collection – Discover unique travel opportunities and adventures, including cruises, safaris, rafting, mountain biking and guided tours. Exchange Partner Resorts – Vacation at hundreds of resorts in dozens of locations through our external exchange partner, Interval International®. With all this flexibility, you have virtually limitless possibilities! OPTION 1: MARRIOTT VACATION CLUB RESORTS Choose a spacious vacation villa for your next getaway. When you plan a vacation within Marriott Vacation Club Resorts, you will have access to more than 50 magnificent resorts offering spacious accommodations, from deluxe studios to 1- and 2-bedroom villas and even 3-bedroom villas and townhouses, depending on the location. Stretch out and enjoy all the comforts of home with amenities such as a fully equipped kitchen, washer and dryer, a balcony or patio, and separate living and dining areas.1 Vacationing at a Marriott Vacation Club resort is perfect for extended vacations or family reunions.