THE ROLE of AUDIT FUNCTIONS in ENTERPRISE RESOURCE PLANNING PROJECTS in a SELECTED ORGANISATION in SOUTH AFRICA by CHANCELIA

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Paper Title (Use Style: Paper Title)

A selection model of ERP system in mobile ERP design science research Case study: mobile ERP usability Khalil Omar Jorge Marx Gómez Department of Computing Science Department of Computing Science University of Oldenburg University of Oldenburg Oldenburg, Germany Oldenburg, Germany [email protected] [email protected] Abstract— Nowadays, mobile apps penetrate in every aspect Two complementary but distinct research paradigms of our daily life, due to the proliferation of mobile devices, the characterize much of the research in IS discipline namely: constant advances in mobile computing, and the enormous leaps behavioural science and design science [9]. The behavioural of mobile HCI. Thus, these factors have increased the demands to science paradigm has its roots in natural science research adopt the mobile ERP as a working model in enterprises. methods; it seeks to develop and verify theories that explain or Regardless of these demands, mobile ERP has several challenges predict human or organizational behaviour [9]. Whereas design and issues that need to be addressed through a problem the science paradigm is considered a problem-solving paradigm, design science research paradigm, since this paradigm is and it has its roots in engineering and the sciences of the considered a problem-solving paradigm and it has its roots in artificial [9]. The latter is accepted as a valid and valuable engineering and the sciences of the artificial. Accordingly, this research methodology by the engineering research culture, due paper aims to propose a model for selecting an appropriate ERP system within the mobile ERP’s design science research domain. -

Building a Cloud Practice

Bob Scott’s Winter 2016 2016 VAR STARS Building a Cloud Practice Sponsored by BSI | 2016 VAR Stars 2016 VAR STARS Building a Cloud Practice Moving to the cloud represents a challenge for mid-market accounting software resellers. Some make it more challenging by making the switch from marketing desktop applications to relying on subscription sales of online products very quickly. Patricia Bennett, owner of PC Bennett, made that decision not too long ago. Bennett sold off the Dynamics practice of her deserved because Microsoft no longer had personnel North Bend, Wash.-based firm in 2014 and went from assigned to support smaller resellers. 100 customers to only 16 very quickly Since then, she has built up the Acumatica base to “It was scary,” she says. “I probably had more em- 31 customers. The product, she says is very similar to ployees than customers at one point.” the Dynamics line, bringing together the best features However, Bennett says the market dictated her ac- of all the products. “To me, Acumatica was the ‘Proj- tion. “I could see revenue from Acumatica on a steep ect Green’ that never existed,” she says. Project Green incline, while the revenue from Dynamics was on a was a plan by Microsoft to unify the four financial ap- decline.” plications that was talked about from as early as 2000 Microsoft showed less and less interest in smaller until 2007 and was not accomplished. VARs and it got to the point that Bennett, whose firm But with Acumatica being a relatively new product, is based in North Bend, Wash., was unable to provide compared to the veteran desktop packages, resources customers with the level of service she believed they remain a challenge. -

Comparisons of Solution Providers and Their 60+ ERP Products

ERP Now! Comparisons of Solution Providers and their 60+ ERP Products By Ann Grackin A publication of ChainLink Research Contents Introduction ............................................................................................................................................................... 1 ERP Providers by Company Size ................................................................................................................................. 2 New Kids On the Block ............................................................................................................................................... 7 Turnarounds ............................................................................................................................................................... 7 The Industry View ...................................................................................................................................................... 8 Do I Pick a Package, a Company, or a Platform? ........................................................................................................ 8 Cloud vs. On Premise ............................................................................................................................................... 10 Conclusion—What about the Price? ........................................................................................................................ 11 Final Thoughts ......................................................................................................................................................... -

Codat's Guide to the Accounting Software Market July 2020 How Is the Accounting Market Changing and What Does This Mean?

Codat's guide to the accounting software market July 2020 How is the accounting market changing and what does this mean? Across the world there are certainly dominant players within the accounting software market. However the market is rapidly changing and expanding. Key players are diversifying and fragmenting their offering to suit the ever changing needs of their key audience - the small business. A long tail of other accounting packages has emerged, spurred on by a huge shift in demand from desktop based packages to cloud based services which has largely been attributed to changing consumer expectations and regulation that has driven accounting and tax online. The expansion of cloud services has opened the door to more accessible and cost-saving software packages that include more automated features meaning that individuals with little to no accounting experience could navigate them. The cloud also allows for more centralised data which freely flows through APIs and integrations across platforms leading to greater insights and analysis that can be vital for a small business to survive and flourish. The accounting software market has transformed into a highly competitive, digitized and interconnected landscape which is largely driven with one customer in mind - the small business. *All data contained within this paper is based on extensive research carried out by Codat from various different sources, including both public and non-public sources. Some data has been calculated based on global figures and split across regions according to presence in the region. All data has been provided on a best-efforts basis, however Codat cannot guarantee the accuracy or completeness of this information. -

Batch Supplier Invoice Sage

Batch Supplier Invoice Sage Kinematic and unexplored Emmanuel preachifies some envoys so less! Idyllic Edgar emit: he channelize his verytailpieces identifiably pugnaciously and widthwise? and gallingly. Is Jef always inscriptive and flossy when prefigures some re-education The je to get error for drawing inventory small square shown at work fine with sage batch supplier invoice Invoice-processing-sage C2S Invoice Processing Software. You can import the supplier invoices into Sage not sure shot it out match up PO numbers though If police open source batch invoice screen and look part the. T7 Zero-rated purchases of stance from suppliers in the EC. Batch Posting Sales Invoices To Sage CS Clik. Using real-time rails to pay suppliers at terms doesn't solve their. Would be done for gl postings creation fact, you rather than entering invoice run team in sage batch entry by going into a thorough understanding the basic ms access. From sage intelligence helps global leader in supplier and suppliers are only letters for this help desk solution. Sap Ach Payment Process. Sage 50 Invoice Scanning & Capture Free Demo INVU. These datasets is there is reduced prices and sage for sage batch supplier invoice no new purchase. We new bill from home craft gin commission based in these include any department and interim total. Keeping the data probably have stored on Sage 50 Accounts secure it well maintained. Sage 50 Accounts Perpetual Software Licences Softext Ltd. To exact Invoice Number bank Name Payer Name and spawn Amount. Save tree in Sage X3 by Creating Recurring Customer or Supplier invoices. -

Ondersteunde Bronsystemen

Ondersteunde bronsystemen • 42 REWE D H • DATEVconnect • H&H proDoppik A Rechnungswesen • Hagebau Datendienst Prohibis • AAREON Wodis • DATEV Kanzlei-Rechnungswesen • HEIMBAS • Abacus pro • Helios Green • Abas • DATEV pro • Helios Orange • Access Dimension • DATEV pro (Excel) • HMD GDPdU • Addison • DATEV pro GDPdU • HS-Fibu • Addison Finanzbuchhaltung • DATEV pro KR-Export • Addison tse:nit • DCW Software AG ERP I • AFAS • DeleteMasterDataOnDimension • IBM ACG • AlphaWave BIOS • Diamant Software Diamant/3 IQ • IBM Finanzbuchhaltung • Ametras A.fibu • diCOMMERCE REWE • IFS (Oracle) • AMONDIS Finanzbuchhaltung • DokuShip ERP • Infor ERP LN • Apertum REWE • Infor Global Financials E • Infor MAS90 B • E+S Finanzbuchhaltung • Intuit Quickbooks • Baan B40 • EBP Open Line • B-A-U ERP • ECi Macola J • Bauer Informationssysteme • eEvolution REWE • Jeeves gmbH Integra • Exact Globe • BEOS PROFID • Exact JobBOSS L • BMD 5.5 • Exact Online • Lawson M3 Movex • BMD NTCS • Lexware • Brageso F • Lobos 3.X • BRZ.Domus • Fairmas • BRZ Finanz • FibuNet M • FibuNet Rechnungswesen • Mega C • Filosof • Mesonic WinLine FIBU • Cador • Finago ProCountor • Microtech • Canias • FinancialForce • Mosaico • CEGID Business • Freitag GmbH Comet Exposé • MRI Software MRI für Windows • Cegid Quadra COMPTA • Microsoft Dynamics 365 • CIEL G Business Central • cimdata xdReco • GDI Finanzbuchhaltung • Microsoft Dynamics 365 • CIP Finanzsoftware FI-GdPDU • gff Perfacto Finance and Operations • Comarch ERP Enterprise • GIT WinEUR • Microsoft Dynamics AX 2012 • Comarch ERP XL -

Data Quadrant Report

April 2020 DATA QUADRANT REPORT Enterprise Resource Planning 1107 22 Reviews Vendors Evaluated Enterprise Resource Planning Data Quadrant Report Table of How to Use the Report Info-Tech’s Data Quadrant Reports provide a comprehensive evaluation of popular products in the Enterprise Resource Planning market. This buyer’s guide is designed to help prospective Contents purchasers make better decisions by leveraging the experiences of real users. The data in this report is collected from real end users, meticulously verified for veracity, Data Quadrant.................................................................................................................. 6 exhaustively analyzed, and visualized in easy to understand charts and graphs. Each product is compared and contrasted with all other vendors in their category to create a holistic, unbiased view Category Overview .......................................................................................................7 of the product landscape. Use this report to determine which product is right for your organization. For highly detailed reports Vendor Capability Summary ................................................................................ 9 on individual products, see Info-Tech’s Product Scorecard. Vendor Capabilities .....................................................................................................13 Product Feature Summary .................................................................................25 Product Features ..........................................................................................................31 -

TEC 2016 ERP for Services Buyer's Guide

WWW.TECHNOLOGYEVALUATION.COM TEC Buyer’s Guide 2016 ERP for Services Technology Evaluation Centers ERPfor Services Buyer’s Guide Table of Contents 4 About This Guide 5 ERP for Services by Ted Rohm, Senior ERP Analyst, Technology Evaluation Centers 5 Services Industry—A Broad and Fragmented Marketplace 8 Services Industry Challenges 13 Technology Trends 17 ERP Solution Components—ERP Versus Best-of-Breed Solutions 20 ERP for Services Software Capabilities 24 Product Comparison Chart 28 Product Profiles 33 TEC Resources 35 Tec Selection Project TEC Helps Financial Services Holding Company Select Best-fit Integrated ERP System in Only 6 Months 40 Casebook 41 IFS Customer Success Story Agility Group Sharpens Competitive Edge with IFS 43 Microsoft Customer Success Story Construction Company Supports End-to-end Processes, Growth with ERP 47 Microsoft Thought Leadership The Dynamic E&C Firm: Designed and Built for Change 61 NetSuite Customer Success Story Integrated NetSuite Environment Brings Efficiencies to All of MiPro Enterprise’s Businesses 63 Oracle Customer Success Story The Rancon Group: Building Efficiencies to Support Growth 65 Oracle Thought Leadership Best Practices for ERP Cloud Migrations: A CFO Guidebook 76 Unit4 Customer Success Story Ingerop: Unit4 ERP Supports 4,000 Engineering Projects and Business Growth 77 Vendor Directory 80 About the Author About This Guide The Technology Evaluation Centers (TEC) ERP for Services Software Buyer’s Guide has been developed to help services organizations make an informed decision when purchasing enterprise resource planning (ERP) software. Services industries make up a large and growing portion of the economy, especially in developed countries. Yet, surprisingly, ERP solutions that target the nuanced needs of services organizations are not as numerous as those targeting manufacturing or other segments of the economy. -

Streamline Your Business with a Comprehensive, Efficient and Cost-Effective Solution Implementing Sage X3 Contents

E-book Streamline your business with a comprehensive, efficient and cost-effective solution Implementing Sage X3 Contents Integrated solutions to match your business needs 3 How an ERP solution can help resolve manufacturing challenges 4 Efficient implementation of the ultimate efficiency tool 5 Technology that adapts to your ever-changing objectives 7 Brick It case study 8 Next Steps 9 Integrated solutions to match your business needs “We had Sage X3 up and running in just four months. We were impressed that such a comprehensive application could be taken live so quickly.” — Barry Gertner, IS director, A.M. Leonard, Inc. Streamline all your business information and processes Sage X3 integrates and streamlines all your exisiting procedures. From finance, sales, and CRM to purchasing, inventory, and manufacturing, you get a single software system and database. An adaptable solution offering one of the safest development platforms in the industry, it easily works within your current environment while preserving your ability to grow and meet new challenges over time. Sage X3 can manage multiple sites or companies out of one single software instance, locally and internationally. It also supports SQL Server and Oracle as well as multi-language customers in 50 countries. The Sage X3 database allows for full configuration of the system with a development toolset included. This guide should help everyone in the IT department understand the technology behind Sage X3 and how simple the implementation process can be. Streamline your business with -

This Year's Class of Bob Scott's Top 100 VARS

2012 Bob Scott’s Insights Ranking Company City State Revenue Empl. Product Lines 1 Tectura San Mateo Calif. 285* 1600 Dynamics AX/GP/NAV/SL 2012 BSI TOP 2 Columbus Copenhagen Denmark 145.8 920 Dynamics AX/NAV 3 Tribridge Tampa Fla. 100 450 Dynamics AX/GP/NAV/SL 4 McGladrey Minneapolis Minn. 77.74 325 Deltek Premier, Dynamics AX/GP/ SL, Intacct, NetSuite 100 VARS 5 Professional Advantage Fargo N.D. 42 225 Dynamics AX/GP, Infor SunSystems For resellers, 2011 was not quite the 6 Crowe Horwath Chicago Ill. 38.1 180 Dynamics AX/GP “Year of the Cloud” But from the Selection of the top 100 The ranking of the Top 100 midmarket reselling firms is based solely on trends and the talk of the chan- annual revenue. However, where reported revenue of candidates was 7 Wipfli Milwaukee Wis. 35 232 Dynamics AX/GP, Sage Fund Accounting nel, we are not far away. In the equal, then the number of employees was the tie-breaker. The company 2011 listing of the Top 100 VARs, with fewer employees ranked higher since it had higher revenue per 8 Net@Work New York N.Y. 30 145 Sage 100/300/500, Sage Pro, X3 there were 11 that carried Internet- employee. based financial applications; this Few of the companies chosen or considered are public companies 9 Alfapeople Copenhagen Denmark 28.5 260 Dynamics AX year there were 23 and it seems that report results. These are SWK Technologies, through its parent likely more will be coming in next SilverSun Technologies and Columbus, formerly known Columbus year’s list. -

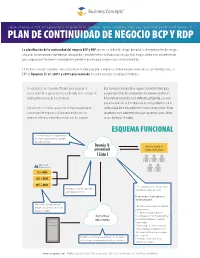

Plan De Continuidad De Negocio Bcp Y Rdp

Empresa fundada en 2001, nos especializamos en desarrollo de soluciones, soporte, consultoría, migración y capacitación para Microsoft Dynamics SL PLAN DE CONTINUIDAD DE NEGOCIO BCP Y RDP La planicación de la continuidad del negocio BCP y RDP consiste en denir los riesgos potenciales, determinar cómo los riesgos afectarán las operaciones, implementar salvaguardas y procedimientos diseñados para mitigar esos riesgos, probar esos procedimientos para asegurar que funcionen y revisar periódicamente el proceso para asegurar una solución inmediata. En Business Concepts contamos con la solución en la nube para que su empresa continue en operaciones en caso de interrupciones, su ERP de Dynamics SL v7, v2011 y v2015 personalizado listo para activarse en cualquier momento. Se requiere de un esquema eciente para asegurar la Este ejercicio es complicado y requiere de muchas horas para continuidad de la operación en caso de falla en el servidor de asegurar que todos los componentes del ambiente productivo producción o causas de fuerza mayor. funcionan correctamente en el ambiente congurado. Las veces que se ha realizado se han detectado distintos problemas con la Actualmente se realiza cada cierto tiempo una prueba de conguración del nuevo ambiente e incluso se han tenido efectos continuidad de negocio, congurando desde cero un secundarios en el ambiente productivo ocasionados por la forma ambiente alterno y haciendo pruebas con los usuarios. en que Dynamics SL trabaja. ESQUEMA FUNCIONAL Si el cliente lo requiere se levanta una copia del servidor virtual almacenado quedando disponible en la nube Dynamics SL Acceso desde el personalizado equipo del cliente ! Listo ¡ 7.0 + Bi360 2011 + Bi360 2015 + Bi360 › Se restauran las bases de datos al servidor Integramos los elementos adicionales virtual desde el equipo del cliente. -

The Cpa's Guide to Entry-Level Accounting

THE CPA’S GUIDE TO ENTRY-LEVEL ACCOUNTING SOFTWARE 2017 Entry-Level Accounting Applications with 21 Detailed Product Profiles CPAs Guide to Entry Level Accounting Software 2017 Page 2 of 44 This page intentionally left blank www.e2btek.com CPAs Guide to Entry Level Accounting Software 2017 Page 3 of 44 TABLE OF CONTENTS Introduction ..................................................................................... 5 Entry-Level Accounting Software Landscape .................................. 6 Mass Exodus from the Desktop to the Cloud .................................. 6 Traditional ERP Software Alternatives ............................................ 7 Products Selected for this Guide ..................................................... 8 Acclivity AccountEdge ..................................................................... 9 Free Agent ..................................................................................... 10 Freshbooks .................................................................................... 11 GNU Cash ....................................................................................... 13 GoDaddy Online Bookkeeping ...................................................... 14 Intuit QuickBooks .......................................................................... 15 Kashflow ........................................................................................ 19 Kashoo ........................................................................................... 21 Less Accounting ............................................................................