Financial Report for 2019/20

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

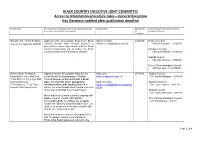

BLACK COUNTRY EXECUTIVE JOINT COMMITTEE Access to Information Procedure Rules – General Exception Key Decisions Notified After Publication Deadline

BLACK COUNTRY EXECUTIVE JOINT COMMITTEE Access to Information procedure rules – General Exception Key Decisions notified after publication deadline Project Name Key Decision to be considered (to provide adequate details for Contact Officer Date Item to Chair of relevant Overview and Scrutiny those both in and outside of the Council) be Committee informed considered Growth Hub - Grant Funding Approval for the Accountable Body for the Black Simon Neilson 24/06/20 Dudley Council Agreement Approval 2020/21 Country Growth Hub (Walsall Council) to [email protected] - Cllr Ray Burston – 11/06/20 proceed to a Grant Agreement, with the Black Country Consortium Ltd, to deliver the Black Sandwell Council Country Growth Hub Funding for 2020/21. - Cllr Laura Rollins – 15/06/20 Walsall Council - Cllr John Murray – 15/06/20 City of Wolverhampton Council - Cllr Paul Sweet – 10/06/20 Hub to Home Transport Approval for the Accountable Body for the Alan Lunt 25/09/19 Dudley Council Innovation Centre and Test Local Growth Deal programme (Walsall [email protected] - Cllr Nicola Richards – 28-8-19 Track Project: Very Light Rail Council) to proceed to enter into a Grant and Autonomous Agreement and/or other appropriate Stuart Everton Sandwell Council Technologies – Test Track documentation, with Dudley Council to [email protected] - Cllr Laura Rollins – 29-8-19 Project Grant Agreement deliver the Local Growth Deal funded elements ov.uk of the Very Light Rail Test Track Project. Walsall Council - Cllr Louise Harrison – 29-8-19 Notes that there is work currently ongoing with Dudley Council, the BC LEP and the City of Wolverhampton Council Accountable Body, to validate the available - Cllr Paul Sweet – 3-9-19 funds in the Black Country Enterprise Zone, to fund the next phases of the project which will include the Innovation Centre. -

LAND SECURITIES Report and Financial Statements 31 March 1999

LAND SECURITIES Report and Financial Statements 31 March 1999 Home Contents Search Next Back Home Contents Contents Corporate Statement 1 Corporate Governance 33 Financial Highlights 2 Report of the Remuneration Committee 35 Search Valuation 4 Directors’ Report 38 Chairman’s Statement 6 Directors and Advisers 40 Operating and Financial Review Senior Management 41 Next Chief Executive‘s Review 8 Directors’ Responsibilities 42 The Group’s Developments 10 Auditors’ Report 42 Offices 12 Valuers’ Report 43 Back Shops and Shopping Centres 16 Consolidated Profit and Loss Account 44 Retail Warehouses and Balance Sheets 45 Food Superstores 20 Consolidated Cash Flow Statement 46 Hotels, Leisure and Residential 23 Other Primary Statements 47 Warehouses and Industrial 24 Notes to the Financial Statements 48 Financial Review 27 Ten Year Record 62 Environment and Health & Safety 32 Major Property Holdings 63 Investor Information (Inside Back Cover) FINANCIAL CALENDAR 1999 2000 26 May Preliminary Announcement January Interim dividend payable 7 June Ex-dividend date 11 June Registration qualifying date for final dividend 14 July Annual General Meeting 26 July Final dividend payable November Announcement of interim results (unaudited) LAND SECURITIES PLC Corporate Statement Home Contents We are committed to providing our shareholders Search with sustainable and growing returns underpinned by secure and increasing income, together with Next capital appreciation. Back We deliver these returns by developing and investing for the long term to create and enhance -

Partnership News

This is an interactive News from the Black Country and West Birmingham PDF. To navigate, use the arrow buttons on Sustainability and Transformation Partnership (STP) each page or locate a specific section using the buttons below. ISSUE 03 In this issue Partnership News March 2021 Introduction Blue print for integrating health Introduction and care Three cheers for community volunteers This will be our last newsletter as a Sustainability and These new partnerships will work towards improving population NHS frontline heroes Transformation Partnership (STP) as NHS England and health outcomes and they will be decision-making forums that enable the adjustment of services and resources to better meet the needs of Don’t write off a Improvement recently confirmed our designation to an local people. cough as coronavirus Integrated Care System (ICS) from 1 April 2021. – get it checked As the 2020/21 financial year draws to a close, the biggest reflection The move to an ICS is timely with the publication of the Government is of pride in our heath and care workforce. For all those who have People with learning White Paper, ‘Integration and Innovation: Working together to gone above and beyond to care for people at their most vulnerable disabilities: Annual improve health and social care for all’ which sets the blue print for and protect many more from the impact of COVID-19. Through Health Checks (AHCs) the future of integrated health and care. This coming 12 months will the challenges of the last 12 months the strength, compassion and be a year for us to set the ground to become a statutory ICS in April Covid-19 Vaccine determination of our people has been outstanding. -

Introduction Accessibility Across UK Local Authorities

Accessibility across UK Local Authorities Socitm and Sitemorse collaboration – supporting BetterConnected Introduction Digital accessibility regulation is challenging to manage and is negatively impacting those for whom the rules should be assisting. Public sector bodies must deal with accessibility, against a timetable. Now with a specific timeline in relation to the public sector achieving accessibility compliance for their websites, we have summarised our Q3 / 2019 results, reporting the position across the sector. For over 10 years Sitemorse have been in partnership with Socitm, working on numerous initiatives including BetterConnected. Sept. 29th 2019 | Ver. 1.9 | Release | © Sitemorse In Summary. For the Sitemorse 2019 Q3 UK Local Government INDEX we assessed over 400 authority websites for adherence to WCAG 2.1. The INDEX was compiled 37% following some 250 million tests, checks and measures across nearly 820,000 URLs. 17% Comparing the Q3 to the Q2 results; 49 improved, 44 dropped, with the balance remaining the same. Three Local Authorities achieved a score of 10 (out of 10) for accessibility. It’s important to note that the INDEX covers the main website of each authority. The law applies to all websites operated, directly or on behalf of the authority. 46% The target score is 7.7 out of 10. • Pages passing accessibility level A: 87.11% • Pages passing accessibility level AA: 12.2% • Of the 3,550 PDF’s 56.4% PDF’s passed the accessibility tests. Score 10 - 7 Score 5 - 6 Score 1 - 4 It is important to note that this score is for automated tests; there are still manual tests that need to be performed however, a score of 10 demonstrates a thorough understanding of what needs to be done and it is highly likely that the manual tests will pass too. -

Current Investment Opportunites Coming Soon

INVESTMENT INDEX CURRENT INVESTMENT COMING SOON OPPORTUNITES TO INVESTORS ONES TO WATCH 01 Birmingham Curzon 01 Birmingham International Station 01 Former Ironbridge Power Station Integrated Transport Exchange Solihull 02 Springfield Campus Wolverhampton 02 Friargate Coventry 02 City Centre South Coventry 03 Walsall Town Centre 03 i54 South Staffordshire - Western Extension 03 DY5 Dudley’s Business 04 West Bromwich Eastern Quarter 04 Interchange Commercial District and Innovation Enterprise Zone and Canalside Living Quarter Wolverhampton 04 Dudley Town Centre MIRA Technology Park Southern 05 05 Friar Park, Sandwell Manufacturing Sector Nuneaton 06 Greater Icknield and Smethwick 06 Paradise Birmingham Birmingham/Sandwell 07 Redditch Gateway 07 M6 Junction 10 Cluster Walsall 08 Solihull Town Centre 08 Perry Barr Regeneration and Commonwealth Games 2022 Birmingham 09 Telford Investment Cluster 09 The Brewers Yard Wolverhampton 10 Transforming Nuneaton 11 UK Central Hub and HS2 Interchange Solihull CURRENT INVESTMENT OPPORTUNITIES 01 Birmingham Curzon Birmingham Curzon is a 141 hectare regeneration area at the heart of the city and the UK High Speed rail network. OPPORTUNITY Centred around a new High Speed 2 (HS2) terminus station a number of major investment opportunities exist for parties interested in exploring development Birmingham partner/funder and equity investment on sites ranging up to 3.3 hectares and covering a selection of commercial and residential uses. Birmingham City Council as promoter is working with Homes England as well as private sector landowners to identify investable development projects within the Curzon regeneration area. There is a strategic opportunity to help shape projects at an early stage, as these are expected to come forward over the next 3–5 years. -

Local Authority / Combined Authority / STB Members (July 2021)

Local Authority / Combined Authority / STB members (July 2021) 1. Barnet (London Borough) 24. Durham County Council 50. E Northants Council 73. Sunderland City Council 2. Bath & NE Somerset Council 25. East Riding of Yorkshire 51. N. Northants Council 74. Surrey County Council 3. Bedford Borough Council Council 52. Northumberland County 75. Swindon Borough Council 4. Birmingham City Council 26. East Sussex County Council Council 76. Telford & Wrekin Council 5. Bolton Council 27. Essex County Council 53. Nottinghamshire County 77. Torbay Council 6. Bournemouth Christchurch & 28. Gloucestershire County Council 78. Wakefield Metropolitan Poole Council Council 54. Oxfordshire County Council District Council 7. Bracknell Forest Council 29. Hampshire County Council 55. Peterborough City Council 79. Walsall Council 8. Brighton & Hove City Council 30. Herefordshire Council 56. Plymouth City Council 80. Warrington Borough Council 9. Buckinghamshire Council 31. Hertfordshire County Council 57. Portsmouth City Council 81. Warwickshire County Council 10. Cambridgeshire County 32. Hull City Council 58. Reading Borough Council 82. West Berkshire Council Council 33. Isle of Man 59. Rochdale Borough Council 83. West Sussex County Council 11. Central Bedfordshire Council 34. Kent County Council 60. Rutland County Council 84. Wigan Council 12. Cheshire East Council 35. Kirklees Council 61. Salford City Council 85. Wiltshire Council 13. Cheshire West & Chester 36. Lancashire County Council 62. Sandwell Borough Council 86. Wokingham Borough Council Council 37. Leeds City Council 63. Sheffield City Council 14. City of Wolverhampton 38. Leicestershire County Council 64. Shropshire Council Combined Authorities Council 39. Lincolnshire County Council 65. Slough Borough Council • West of England Combined 15. City of York Council 40. -

Walsall Council Walsall Market Location Review and Evidence Base

Walsall Council Walsall Market Location review and evidence base ARP-WAL-EVB Planning | 10 February 2014 This report takes into account the particular instructions and requirements of our client. It is not intended for and should not be relied upon by any third party and no responsibility is undertaken to any third party. Job number 232986 Ove Arup & Partners Ltd The Arup Campus Blythe Gate Blythe Valley Park Solihull B90 8AE United Kingdom www.arup.com Walsall Council Walsall Market Location review and evidence base Contents Page 1 Introduction 1 1.1 Purpose of this report 1 1.2 Arup’s commission 1 2 Key considerations 2 3 Previously considered market locations 4 3.1 Overview 4 3.2 Location requirements 5 3.3 The preferred location 5 4 Review of existing market and preferred location 6 4.1 Economic context 6 4.2 Public realm 7 4.3 Accessibility 11 4.4 Recognising best practice 11 4.5 Exclusion Zone 22 4.6 Viability 23 4.7 Civil works and infrastructure 27 4.8 Planning and regeneration context 29 5 Revised market location criteria 33 6 Potential market locations 35 6.1 Identifying potential market locations 35 6.2 Updated locations 35 7 Assessment of potential market locations 38 7.1 Assessment of locations 38 7.2 Assessment summary table 41 7.3 Preferred options 45 7.4 Recommendation 45 Tables Table 1: Soft market discussions summary Table 2: Popup stall income and expenditure Table 3: Summary of relevant local planning policy Table 4: Location criteria ARP-WAL-EVB | Planning | 10 February 2014 J:\232000\232986-00\4 INTERNAL PROJECT DATA\4-05 REPORTS\PLANNING\SUPPORTING PLANNING DOCUMENTS\EVIDENCE BASE REPORT\LOCATION REVIEW AND EVIDENCE BASE FINAL.DOCX Walsall Council Walsall Market Location review and evidence base Table 5: Potential locations assessment summary Figures Figure 1: Locations considered by GVA study. -

Street Lighting As an Asset; Smart Cities and Infrastructure Developments ADEPTE ASSOCIATION of DIRECTORS of ENVIRONMENT, ECONOMY PLANNING and TRANSPORT

ADEPTE ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT DAVE JOHNSON ADEPT Street Lighting Group chair ADEPT Engineering Board member UKLB member TfL Contracts Development Manager ADEPTE ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT • Financial impact of converting to LED • Use of Central Management Systems to profile lighting levels • Street Lighting as an Asset; Smart Cities and Infrastructure Developments ADEPTE ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY, PLANNING AND TRANSPORT Representing directors from county, unitary and metropolitan authorities, & Local Enterprise Partnerships. Maximising sustainable community growth across the UK. Delivering projects to unlock economic success and create resilient communities, economies and infrastructure. http://www.adeptnet.org.uk ADEPTE SOCIETY OF CHIEF OFFICERS OF CSS Wales TRANSPORTATION IN SCOTLAND ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT ADEPTE SOCIETY OF CHIEF OFFICERS OF CSS Wales TRANSPORTATION IN SCOTLAND ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT Bedford Borough Council Gloucestershire County Council Peterborough City Council Blackburn with Darwen Council Hampshire County Council Plymouth County Council Bournemouth Borough Council Hertfordshire County Council Portsmouth City Council Bristol City Council Hull City Council Solihull MBC Buckinghamshire County Council Kent County Council Somerset County -

Thousands of Businesses Across England Facing Further Job Losses Or Bankruptcy Due to Local Authorities Failing to Pay up to £1.4Bn of Emergency COVID-19 Grants

PRESS RELEASE Thousands of businesses across England facing further job losses or bankruptcy due to local authorities failing to pay up to £1.4bn of emergency COVID-19 grants Freedom of Information Request by the Events Industry Alliance to Local Authorities across England has shown that an estimated 87 per cent of the £1.6bn Additional Restrictions Grant (ARG) funds announced by the UK Government have yet to be paid out to companies, despite the scheme being launched four months ago The ARG scheme was announced in October to help businesses forced to close due to COVID-19 restrictions, including those in the events, exhibitions and hospitality sectors Businesses closed by COVID-19 restrictions face being forced into making further job cuts or bankruptcy due to local council delays London, 10 February 2021, The Events Industry Alliance (EIA), which represents the UK’s event organisers, venues, and suppliers, can today reveal that an estimated £1.4bn of Additional Restrictions Grants (ARG) announced by the UK Government on 31 October, has not yet been paid by local authorities in England to businesses closed by the Covid-19 pandemic. The ARG, which could be worth up to £3,000 per month per company, provides funding for local authorities to support businesses that have been forced to close because of national COVID-19 restrictions. These include companies in the retail, hospitality, and leisure sectors, as well as events and exhibitions businesses. The scheme was announced by the UK Government on 31st October 2020 with an initial £1bn funding allocation, with a further £594m issued in early January 2021. -

Winners of the Geoplace Exemplar Awards 2014

Winners of the GeoPlace Exemplar Awards 2014 Exemplar Award 2014 Winner Joint Emergency Services Group (Wales) Runner-up Oxford City Council Highly commended Northumberland County Council Custodian of the Year 2014 Marilyn George East Riding of Yorkshire Most Improved Address Data Ribble Valley Borough Council Most Improved Street Data Milton Keynes Council Best Address Data in Region Best Address Data in East Midlands Region 2014 Mansfield District Council Best Address Data in East of England Region 2014 Huntingdonshire District Council Best Address Data in Greater London Region 2014 London Borough of Enfield Best Address Data in North East Region 2014 South Tyneside Council Best Address Data in North West Region 2014 Allerdale Borough Council 1 Best Address Data in South East Region 2014 Lewes District Council Best Address Data in South East Region 2014 Adur District Council Best Address Data in South West Region 2014 Torridge District Council Best Address Data in Wales Region 2014 Flintshire County Council Best Address Data in West Midlands Region 2014 Wyre Forest District Council Best Address Data in Yorkshire and the Humber Region 2014 Kingston upon Hull City Council and Sheffield City Council Best Street Data in Region Best Street Data in East Midlands Region 2014 Northamptonshire County Council Best Street Data in East of England Region 2014 Peterborough City Council Best Street Data in Greater London Region 2014 London Borough of Enfield Best Street Data in Greater London Region 2014 London Borough of Hillingdon Best Street Data -

National Centre for Creative Health (NCCH) Safeguarding Policy

National Centre for Creative Health (NCCH) Safeguarding Policy Registered Charity No. 1190515 Policy Adopted October 2020 (Updated March 2021) Contents 1. INTRODUCTION .................................................................................................................................... 2 2. PART 1 – SAFEGUARDING CHILDREN ................................................................................................... 4 3. PART 2 – SAFEGUARDING ADULTS ...................................................................................................... 8 4. ENABLING REPORTS .......................................................................................................................... 11 5. CONFIDENTIALITY .............................................................................................................................. 13 6. PARTNERSHIP PROJECTS AND COLLABORATION ............................................................................. 13 7. NCCH PROGRAMME STRANDS AND DELIVERY .................................................................................. 13 8. E-SAFETY ........................................................................................................................................... 14 9. INTERNATIONAL SAFEGUARDING ...................................................................................................... 15 10. FURTHER RESOURCES .................................................................................................................... 15 11. CONTACT -

St. Matthew's Quarter – Relocation of Walsall Market

St. Matthew’s Quarter – Relocation of Walsall Market Update of Evidence Base Walsall Council August 2010 www.gvagrimley.co.uk Report to Walsall Council Relocation of Walsall Market – Update of Evidence Base Contents 1. INTRODUCTION.........................................................................................................1 2. BACKGROUND AND DEVELOPMENT HISTORY ...................................................7 3. POLICY CONTEXT...................................................................................................11 4. THE ROLE AND FUTURE OF WALSALL MARKET ..............................................18 5. TOWN CENTRE HEALTH CHECK (VITALITY AND VIABILITY) ASSESSMENT .25 6. CONSULTATION FINDINGS ...................................................................................62 7. THE SCENARIOS AND APPROACH TO THEIR ASSESSMENT ..........................65 8. ASSESSMENT OF SCENARIOS.............................................................................68 9. CONCLUSIONS AND RECOMMENDATIONS........................................................82 Appendices APPENDIX A – WALSALL MBC STUDY BRIEF 2010 APPENDIX B – WALSALL UDP POLICIES APPENDIX C – WALSALL MBC SHOPPER SURVEY 2010 QUESTIONNAIRE August 2010 Report to Walsall Council Relocation of Walsall Market – Update of Evidence Base 1. INTRODUCTION 1.1 GVA Grimley has been appointed by Walsall Council to provide consultancy advice in relation to the update of the Evidence Base for the Market Relocation (as previously prepared by GVA Grimley, in September