2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Status of Kentucky Derby Winners

STATUS OF KENTUCKY DERBY WINNERS Year Kentucky Derby Winner Foal Date Died Age Present Status 2020 Authentic May 5, 2017 4 Stud ($75,000), Spendthrift Farm, Lexington, Ky. 2019 Country House May 8, 2016 5 Stud ($7,500), Darby Dan Farm, Lexington, Ky. 2018 Justify March 28, 2015 6 Stud ($125,000), Ashford Stud, Versailles, Ky. 2017 Always Dreaming Feb. 25, 2014 7 Stud ($17,500), WinStar Farm, Versailles, Ky. 2016 Nyquist March 10, 2013 8 Stud ($75,000), Darley, Lexington, Ky. 2015 American Pharoah Feb. 2, 2012 9 Stud ($100,000), Ashford Stud, Versailles, Ky. 2014 California Chrome Feb. 18, 2011 10 Stud ($36,500); Arrow Stud, Hokkaido, Japan 2013 Orb Feb. 24, 2010 11 Stud (Private), Claiborne Farm, Paris, Ky. 2012 I’ll Have Another April 1, 2009 12 Stud ($10,000), Ocean Breeze Ranch, Bonsall, Calif. 2011 Animal Kingdom March 20, 2008 13 Stud (Private), Jbba Shizunai Stallion Station, Hokkaido, Japan 2010 Super Saver March 18, 2007 14 Stud ($15,000), Turkish Jockey Club Izmit Stallion Complex, Izmit, Turkey 2009 Mine That Bird May 10, 2006 15 Retired, Double Eagle Ranch, Roswell, N.M. 2008 Big Brown April 10, 2005 16 Stud ($5,000), Irish Hill & Dutchess Views Stallions, Stillwater, N.Y. 2007 Street Sense Feb. 23, 2004 17 Stud ($60,000), Darley, Lexington, Ky. 2006 Barbaro April 29, 2003 Jan. 29, 2007 (4) 2005 Giacomo Feb. 16, 2002 19 Stud ($2,500), Oakhurst Equine Veterinary Services, Newberg, Ore. 2004 Smarty Jones Feb. 28, 2001 20 Stud ($3,500), Equistar Training and Breeding, Annville, Pa. 2003 Funny Cide April 20, 2000 21 Retired, Kentucky Horse Park, Lexington, Ky. -

Foreign Investment in Central Asia: Actors and Drivers 1

Foreign Investment in Central Asia: Actors and Drivers 1 Issues Paper Foreign Investment in Central Asia: Actors and Drivers by Ariel Cohen, Ph.D. James Grant December 2020 Asia-Pacific • Africa • Eurasia • Latin America • MENA International Tax and Investment Center www.ITICnet.org Foreign Investment in Central Asia: Actors and Drivers 1 Contents Authors 2 Acknowledgments 2 Forward 3 I. Introduction 4 II. Country Overview 6 1. Kazakhstan 6 2. Turkmenistan 10 3. Tajikistan 13 4. Kyrgyzstan 16 5. Uzbekistan 18 III. Conclusion 23 Endnotes 25 International Tax and Investment Center www.ITICnet.org Foreign Investment in Central Asia: Actors and Drivers 2 Authors Dr. Ariel Cohen L.L.B., Ph.D. is a recognized authority in political risk, rule of law, international energy, and security. He is a Senior Fellow with the non-profit International Tax and Investment Center (ITIC) and Director of the Energy, Growth, and Security Program (EGS). Dr. Cohen also holds a Senior Fellowship at the Eurasian Studies Center at the Atlantic Council with a regional focus on Russia/Eurasia, Eastern Europe and the Middle East. For over 20 years Dr. Cohen served as a Senior Research Fellow in Russian and Eurasian Studies and International Energy Policy at the Sarah and Douglas Allison Center at the Heritage Foundation. He directed Heritage’s energy war games and worked closely with Members of Congress and Congressional staff members as well as cabinet-level and sub-cabinet domestic and foreign decision-makers. His book, Kazakhstan: Energy Policy and the Birth of a Nation was published by SAIS Johns Hopkins (2008). -

Geschäftsbericht 2003 Konzern-Kennzahlen Nach Us Gaap Definitionen Kontakt

GESCHÄFTSBERICHT 2003 KONZERN-KENNZAHLEN NACH US GAAP DEFINITIONEN KONTAKT Ergebnis vor Ertragsteuern Umsatzrentabilität = CLAAS KGaA mbH 2003 2002 Veränd. % Umsatzerlöse Postfach 1163 GuV/ERGEBNIS Jahresüberschuss + Ertragsteuern + Anteile anderer Gesellschafter -/+ Erfolgsbeiträge aus Änderungen von Münsterstraße 33 EBIT = Bilanzierungs- und Bewertungsmethoden + Zinsaufwand + auf Grund eines Teilgewinnabführungsvertrags D-33426 Harsewinkel Umsatz Mio. 1.496,3 1.265,5 18,2 abgeführte Gewinne (CMG) + Vergütung Genussrechtskapital EBIT Mio. 53,2 84,0 -36,7 www.claas.com EBITDA = EBIT + Abschreibungen auf das Anlagevermögen EBITDA Mio. 90,9 111,9 -18,8 Weitere Exemplare des Berichts Jahresüberschuss Jahresüberschuss/-fehlbetrag Mio. 17,9 32,5 -44,9 Eigenkapitalrentabilität = sowie zusätzliches Informations- Eigenkapital GESCHÄFTSBERICHT 2003 Ergebnis vor Steuern Mio. 22,6 55,8 -59,5 material über CLAAS schicken EBIT Gesamtkapitalrentabilität = Cashflow Mio. 58,1 67,4 -13,8 Bilanzsumme wir Ihnen auf Anfrage gerne kostenlos zu. F&E-Aufwendungen Mio. 67,2 63,0 6,7 Jahresüberschuss + Abschreibungen auf Anlagevermögen +/- Veränderung der Pensionsrückstellungen Cashflow nach DVFA/SG = und anderer langfristiger Rückstellungen +/- sonstige zahlungsunwirksame Aufwendungen und Erträge BILANZ Eigenkapital Eigenkapitalquote = Bilanzsumme Eigenkapital Mio. 292,5 292,2 0,1 Liquidität Sachinvestitionen Mio. 54,2 54,3 -0,2 Liquidität 1. Grades = Kurzfristiges Fremdkapital together Kunden Bilanzsumme Mio. 1.412,8 1.019,6 38,6 Eigenkapital + eigenkapitalähnliche -

Status of Kentucky Derby Winners

WEATHER 94 was the warmest Kentucky Derby Day high on May 2, 1959 (Tomy Lee) 47 was the coldest Kentucky Derby Day high on May 4, 1935 (Omaha) and May 4, 1957 (Iron Liege); the record cold in 1957 was accompanied by north winds between 20-25 mph 3.15 inches of rain was the wettest Kentucky Derby on May 5, 2018 (Justify) Sleet was recorded on Kentucky Derby Day on May 6, 1989 (Sunday Silence) between 1:01 p.m. and 1:05 p.m. (along with rain). Snow flurries fell the following morning At least a trace of precipitation has been experienced at some point during the day on 69 of the 145 Kentucky Derby Days (47.6%) The longest stretch of consecutive wet Kentucky Derby Days is six (1989-94); there had been at least a trace for seven consecutive years (2007-13) The longest stretch of consecutive dry Kentucky Derby Days is 12 (1875-86) Wettest Kentucky Derbys, 24-Hour Precipitation: 3.15” (2018 – Justify) 2.31” (1918 – Exterminator) 1.46” (2012 – I’ll Have Another) 1.32” (2010 – Super Saver) 1.19” (1929 – Clyde Van Dusen) 1.04” (1912 – Worth) 0.87” (2013 – Orb) 0.83” (1992 – Lil E. Tee) 0.82” (1897 – Typhoon II) 0.80” (1948 – Citation) Wettest Kentucky Derbys, 1-7 p.m. Precipitation: 2.85” (2018 – Justify) 1.00” (1918 – Exterminator) 0.66” (1929 – Clyde Van Dusen) 0.55” (1996 – Grindstone) 0.45” (1912 – Worth) 0.44” (2013 – Orb) 0.39” (1928 – Reigh Count) 0.35” (1898 – Plaudit) 0.35” (1992 – Lil E. -

'Rising Star' Heavies in Arkansas Derby

SUNDAY, APRIL 11, 2021 SUPER STOCK UPSETS CURLIN COLT FINISHES 'FURY'-OUSLY IN THE LEXINGTON by Alan Carasso 'RISING STAR' HEAVIES IN Fern Circle Stable & Three Chimneys Farm's King Fury (Curlin) took advantage of a fast early pace in Saturday's GIII Stonestreet ARKANSAS DERBY Lexington S. over a sloppy Keeneland main track and closed off fastest of all to cause an 18-1 upset, earning 20 points towards a potential appearance in the GI Kentucky Derby in three weeks' time. A maiden winner at first asking over a distance of ground at Churchill Sept. 3, King Fury could not overcome a wide trip when eighth of nine behind Essential Quality (Tapit) in the GI Claiborne Breeders' Futurity over this course and distance Oct. 3. The half-length winner of the Oct. 25 Street Sense S. beneath the Twin Spires, he could do no better than seventh when wheeled back on 12 days' rest in the GI Breeders' Cup Juvenile and added blinkers--to no avail--en route to a fifth in the GII Kentucky Jockey Club S. at Churchill Nov. 28. Cont. p5 Super Stock another Arkansas Derby upsetter | Coady by Alan Carasso IN TDN EUROPE TODAY The GI Arkansas Derby has been won over the last 20-plus REMEMBERING ROY ROCKET years by some short-odds favorites, like future GI Kentucky Emma Berry reflects on the Brighton specialist who became the Derby winners Smarty Jones (Elusive Quality, even-money in people's horse. Click or tap here to go straight to TDN Europe. 2004) and American Pharoah (Pioneerof the Nile, 1-10 in 2015) and future Classic winners such as Curlin (Smart Strike, 4-5 in 2007) and Afleet Alex (Northern Afleet, 12-5 in 2005). -

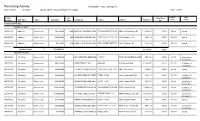

Permitting Activity 01/01/2018 Thru 10/14/2018 Date of Report: 10/15/2018 L-BUILD ONLY - Grouped by Type Then Subtype Page 1 of 295

Permitting Activity 01/01/2018 Thru 10/14/2018 Date of Report: 10/15/2018 L-BUILD ONLY - Grouped by Type then Subtype Page 1 of 295 Issued App. Permit Sq- Total Fees Date Status Number Sub Type Type Valuation Feet Contractor Owner Address Total Fees Due Commercial Permits: Addition Permits: LB1701130 Addition Commercial $92,900.00 1300 HAGGAI CONSTRUCTION &ST DEVELOPMENT PAULS BAPTIST INC CHURCH8002 Old Bainbridge Rd $1,803.31 $0.00 1/3/18 Issued LB1800208 Addition Commercial $20,000.00 400 GARRISON DESIGN AND CONSTRUCTION,GARRISON DESIGN INC. & CONTRUCTION5186 Woodlane Cir $481.13 $0.00 5/22/18 Issued LB1801519 Addition Commercial $5,500.00 240 TONY E. COLVIN INC DBA SOUTHERNNEW JOURNEY FIXIN'S BAPTIST CHURCH4527 N Monroe St $135.40 $0.00 10/4/18 Issued Addition Totals: 3 $118,400.00 $2,419.84 $0.00 Alteration Permits: LB1602042 Alteration Commercial $22,000.00 SBA NETWORK SERVICES LLCT-MOBILE 5585 CRAWFORDVILLE RD $603.86 $0.00 2/2/18 Certificate of Completion LB1700443 Alteration Commercial $56,000.00 SIMPLERBUILT, INC. SABL LLC 5205 Mcneill Blvd $1,868.57 $0.00 3/12/18 Certificate of Completion LB1701599 Alteration Commercial $20,000.00 ATLANTIC TOWER SERVICES,LANG INC MARY ALMA TRUST 6017 Roberts Rd $648.41 $0.00 4/5/18 Issued LB1701639 Alteration Commercial $20,000.00 ASCEND WIRELESS NETWORKS,TYRE JANICE INC. L 5585 Crawfordville Rd $481.73 $0.00 1/18/18 Certificate of Completion LB1701744 Alteration Commercial $20,000.00 ASCEND WIRELESS NETWORKS,MOOSE INC. LODGE 1484 Capital Cir NW $621.56 $0.00 4/3/18 Certificate of Completion LB1701795 Alteration Commercial $228,920.00 LEDFORD DESIGN & CONSTRUCTION,FLEA MARKET LLC. -

Kentucky Derby Winners Vs. Kentucky Derby Winners

KENTUCKY DERBY WINNERS VS. KENTUCKY DERBY WINNERS Winners of the Kentucky Derby have faced each other 43 times. The races have occurred 17 times in New York, nine in California, nine in Maryland, six in Kentucky, one in Illinois and one in Canada. Derby winners have run 1-2 on 12 occasions. The older Derby winner has prevailed 24 times. Three Kentucky Derby winners have been pitted against one another twice, including a 1-2-3 finish in the 1918 Bowie Handicap at Pimlico by George Smith, Omar Khayyam and Exterminator. Exterminator raced against Derby winners 15 times and finished ahead of his rose-bearing rivals nine times. His chief competitor was Paul Jones, who he beat in seven of 10 races while carrying more weight in each affair. Date Track Race Distance Derby Winner (Age, Weight) Finish Derby Winner (Age, Weight) Finish Nov. 2, 1991 Churchill Downs Breeders’ Cup Classic 1 ¼ M Unbridled (4, 126) 3rd Strike the Gold (3, 122) 5th June 26, 1988 Hollywood Park Hollywood Gold Cup H. 1 ¼ M Alysheba (4,126) 2nd Ferdinand (5, 125) 3rd April 17, 1988 Santa Anita San Bernardino H. 1 1/8 M Alysheba (4, 127) 1st Ferdinand (5, 127) 2nd March 6, 1988 Santa Anita Santa Anita H. 1 ¼ M Alysheba (4, 126) 1st Ferdinand (5, 127) 2nd Nov. 21, 1987 Hollywood Park Breeders’ Cup Classic 1 ¼ M Ferdinand (4, 126) 1st Alysheba (3, 122) 2nd Oct. 6, 1979 Belmont Park Jockey Club Gold Cup 1 ½ M Affirmed (4, 126) 1st Spectacular Bid (3, 121) 2nd Oct. 14, 1978 Belmont Park Jockey Club Gold Cup 1 ½ M Seattle Slew (4, 126) 2nd Affirmed (3, 121) 5th Sept. -

Scale-Appropriate Farm Machinery for Rice and Wheat Harvesting: Updates from South and South East Asia

Scale-Appropriate Farm Machinery for Rice and Wheat Harvesting: Updates from South and South East Asia Cereal Systems Initiative for South Asia Scale-Appropriate Farm Machinery for Rice and Wheat Harvesting: Updates from South and South East Asia Cereal Systems Initiative for South Asia (CSISA) 2021 Edited by Scott Justice, Stephen J. Keeling, Govinda Basnet and Timothy J. Krupnik Cereal Systems Initiative for South Asia Scale-Appropriate Farm Machinery for Rice and Wheat Harvesting: Updates from South and South East Asia i The Cereal Systems Initiative for South Asia (CSISA) was established in 2009 to promote durable change at scale in South Asia’s cereal-based cropping systems. Operating in rural ‘innovation hubs’ in Bangladesh, India and Nepal, CSISA works to increase the adoption of various resourceconserving and climate-resilient technologies, and improve farmers’ access to market information and enterprise development. CSISA supports women farmers by improving their access and exposure to modern and improved technological innovations, knowledge and entrepreneurial skills. By continuing to work in synergy with regional and national efforts, collaborating with myriad public, civil society and private-sector partners, CSISA aims to benefit more than 8 million farmers by the end of 2020. The International Maize and Wheat Improvement Center (CIMMYT) is the global leader on publicly funded maize and wheat research and related farming systems. Headquartered near Mexico City, Mexico, CIMMYT works with hundreds of partners throughout the developing world to sustainably increase the productivity of maize and wheat cropping systems, thus improving global food security and reducing poverty. CIMMYT is a member of the CGIAR Consortium and leads the CGIAR Research Programs on MAIZE and WHEAT. -

Psychedelia, the Summer of Love, & Monterey-The Rock Culture of 1967

Trinity College Trinity College Digital Repository Senior Theses and Projects Student Scholarship Spring 2012 Psychedelia, the Summer of Love, & Monterey-The Rock Culture of 1967 James M. Maynard Trinity College, [email protected] Follow this and additional works at: https://digitalrepository.trincoll.edu/theses Part of the American Film Studies Commons, American Literature Commons, and the American Popular Culture Commons Recommended Citation Maynard, James M., "Psychedelia, the Summer of Love, & Monterey-The Rock Culture of 1967". Senior Theses, Trinity College, Hartford, CT 2012. Trinity College Digital Repository, https://digitalrepository.trincoll.edu/theses/170 Psychedelia, the Summer of Love, & Monterey-The Rock Culture of 1967 Jamie Maynard American Studies Program Senior Thesis Advisor: Louis P. Masur Spring 2012 1 Table of Contents Introduction..…………………………………………………………………………………4 Chapter One: Developing the niche for rock culture & Monterey as a “savior” of Avant- Garde ideals…………………………………………………………………………………...7 Chapter Two: Building the rock “umbrella” & the “Hippie Aesthetic”……………………24 Chapter Three: The Yin & Yang of early hippie rock & culture—developing the San Francisco rock scene…………………………………………………………………………53 Chapter Four: The British sound, acid rock “unpacked” & the countercultural Mecca of Haight-Ashbury………………………………………………………………………………71 Chapter Five: From whisperings of a revolution to a revolution of 100,000 strong— Monterey Pop………………………………………………………………………………...97 Conclusion: The legacy of rock-culture in 1967 and onward……………………………...123 Bibliography……………………………………………………………………………….128 Acknowledgements………………………………………………………………………..131 2 For Louis P. Masur and Scott Gac- The best music is essentially there to provide you something to face the world with -The Boss 3 Introduction: “Music is prophetic. It has always been in its essence a herald of times to come. Music is more than an object of study: it is a way of perceiving the world. -

While Making Strides, Claas Still Seeks NA Brand Identity Decision

Vol. 13, Issue 1 News, Information & Analysis for the Ag Equipment Marketer May 15, 2006 While Making Strides, Claas Still Seeks NA Brand Identity Claas, the Harsewinkel, Germany- as well. Gains in the U.S. market large- confused the market a bit,”says Russ based manufacturer of farm equip- ly came from sales of its Caterpillar- Green, executive vice president and ment and Europe’s largest manufac- branded Lexion combines.And this is general manager, Claas-Lexion Div.“But turer of harvesting equipment, is gain- where the Claas brand becomes hazy. we need them (Cat dealers) to have ing momentum in its attempts to In the U.S., 95% of Lexion com- stellar products at their disposal to establish a significant presence in the bines are sold through Cat Challenger meet the needs of the customer.The U.S. ag industry.With the construction dealers. But many Cat dealers also han- tractors do that, but the combine has of its $25 million assembly plant in dle Challenger combines and other caused some confusion.” Omaha, Neb. in 2001, and a distribu- farm equipment through Cat’s part- Despite this, Claas continues to tion and service facility in Columbus, nership with AGCO, diluting Claas’ improve its U.S. market position as it Ind., Claas is starting to make waves in efforts to firmly establish the Lexion experienced a 37.6% increase in ’05 North America. brand and creating a level of confu- sales revenues from its Omaha-based In 2005, Claas set a record for its sion for potential customers. company. worldwide sales of farm equipment as When Challenger rolled out its Green also says that the Claas- it neared the $2.5 billion mark for the new 680B model combine and MT900 Jaguar line of forage equipment is first time.At the same time, as report- tractor line earlier this year, it was making significant gains in the U.S. -

Contwe're ACT

Media contacts for Linkin Park: Dvora Vener Englefield / Michael Moses / Luke Burland (310) 248-6161 / (310) 248-6171 / (615) 214-1490 [email protected] / [email protected] / [email protected] LINKIN PARK ADDS BUSTA RHYMES TO 2008 SUMMER TOUR ACCLAIMED HIP HOP INNOVATOR WILL PERFORM WITH LINKIN PARK, CHRIS CORNELL, THE BRAVERY, ASHES DIVIDE ON PROJEKT REVOLUTION MAIN STAGE REVOLUTION STAGE HEADLINED BY ATREYU AND FEATURING 10 YEARS, HAWTHORNE HEIGHTS, ARMOR FOR SLEEP & STREET DRUM CORPS TOUR BEGINS JULY 16 IN BOSTON Los Angeles, CA (June 3, 2008) – Multi-platinum two-time Grammy-winning rock band Linkin Park has announced that acclaimed hip-hop innovator Busta Rhymes will join their Projekt Revolution 2008 lineup. Rhymes and Linkin Park recently collaborated on “We Made It,” the first single and video from Rhymes’ upcoming album, Blessed. By touring together, Linkin Park & Busta are taking a cue from the chorus of their song: “…we took it on the road…”. As recently pointed out in Rolling Stone’s “Summer Tour Guide,” the tour will see nine acts joining rock superstars Linkin Park, who are also offering concertgoers a digital souvenir pack that includes a recording of the band’s entire set. As the band’s co-lead vocalist Mike Shinoda told the magazine, “That puts extra pressure on us to make sure our set is different every night.” The fifth installation of Linkin Park’s raging road show will see them headlining an all-star bill that features former Soundgarden/Audioslave frontman Chris Cornell, electro-rockers The Bravery and Ashes Divide featuring Billy Howerdel, known for his work with A Perfect Circle. -

God's Love in Christ

Let us help you strive to Let us help you strive to Grow...Preserve...Sustain Grow...Preserve...SustainYour investments Your investments Blake Hahn Financial Group LLC 1650Blake E. HahnMadison Financial Ave., Ste 107 Group LLC Mankat1650 E. Madisono, MN 56001 Ave., Ste 107 pMankathone: 507-345-3588o, MN 56001 cell:phone: 507-382-8396 507-345-3588 fcell:ax: 507-345-8705507-382-8396 blake@blakehahnfinancial.comfax: 507-345-8705 blake@blakehahnfinancial.com Securities oered through LPL Financial, Member FINRA/SIPC. Investment Advice oered through Fortis Group Advisors LLC, a registered investment advisor and separate entity from LPL Financial Securities oered through LPL Financial, Member FINRA/SIPC. Investment Advice oered through Fortis Group Advisors LLC, a registered investment advisor and separate entity from LPL Financial Blake Hahn Financial Group LLC Blake1650 Hahn E.Blake Madison Financial Hahn Ave., Group ,Ste ChFC 107 LLC 1650Mankato, E.Blake Madison Hahn MN AFinancial ve.,56001 Ste 107 Group Mankato,Registered MN Representative, 56001 LPL Financial phone: 507-345-3588 phone:cell:1650 E. 507-382-8396 Madison507-345-3588 Ave., Ste 107 Mankato, MN 56001 phone:cell:fax: 507-345-8705507-382-8396 507-345-3588 [email protected]:fax: 50 507-345-87057-382-8396 [email protected]@blakehahnfinancial.com Securities oered through LPL Financial, Member FINRA/SIPC. Investment advice oered through Fortis Group Advisors LLC, a registered Securitiesinvestment offered advisor. through Fortis LPL Group Financial, Advisors LLC Member and Blake Hahn FINRA/SIPC. Financial Group Investment are separate entities advice from offered LPL Financial. through Fortis Group Advisors LLC a registered investment advisor.