INVESTOR PRESENTATION June 2017 DISCLAIMER

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Maxlinear Mxl261 Multi-Channel Tuner- Demodulator Single-Chip Front-End IC Powers DOCSIS(R) 3.0 Cable Modem from Hitron

February 15, 2011 MaxLinear MxL261 Multi-Channel Tuner- Demodulator Single-Chip Front-End IC Powers DOCSIS(R) 3.0 Cable Modem from Hitron Hitron's CDA-30360 Modem Achieves CableLabs(R) DOCSIS 3.0 Certification with Design Based on Low Power MxL261 Digital Cable Multi-Channel Single-Chip Front End CARLSBAD, Calif.--(BUSINESS WIRE)-- MaxLinear, Inc. (NYSE: MXL), a leading provider of integrated radio frequency (RF) and mixed-signal integrated circuits for broadband communication applications, today announced that Hitron Technologies Inc., has selected the Maxlinear MxL261 digital cable multi-channel tuner-demodulator single-chip front end IC for a new DOCSIS(R) 3.0 cable modem. Hitron's CDA-30360 modem recently achieved certification from CableLabs(R). The CDA- 30360 is a high-speed data cable modem designed using both the MxL261 and Intel(R) Puma(TM) 5 chipset. The modem features both 10/100/1000 Mbps Ethernet and USB host interfaces for future webcam, printer server or NAS file server connectivity. The modem has advanced features including voice and video support, IPv6 addressing and DES/AES data encryption to ensure complete data privacy. More information on the product can be found at www.hitrontech.com.tw. The MxL261 is based on MaxLinear's low power digital CMOS process-based RF and mixed-signal technology. It is a single-die, global standards, digital cable front end with integrated splitter, two 100MHz wideband tuners, four QAM demodulators, and a four- channel wide IF output. The MxL261 delivers ultra-low power at less than 175mW per channel in full eight-channel mode. -

BUSINESS CONTINUITY PLAN CP747 Rev D

BUSINESS CONTINUITY PLAN CP747 Rev D Business Continuity Plan Confidential Copyright ©2015 Exar Corporation. All rights reserved. CP747 Rev D BUSINESS CONTINUITY PLAN CP747 Rev D EMERGENCY CONTACT LIST EMERGENCY RESPONSE PHONE OTHER COORDINATORS John Dutra (408) 838‐7276 Renato Siljeg (925) 413‐8018 EXAR SECURITY Mobile 24/7 (510) 364‐9825 Internal 7888 Alarm Company (Cintas) (888) 710‐0886 Account Number 88217733 EMERGENCY NOTIFICATION LIST Fire 9‐911 (510) 494‐4280, Fremont Fire Department EMS/ Paramedics 9‐911 (510) 494‐4280, Fremont Fire Department Police 9‐911 (510) 790‐6800, Fremont Police Department Security Desk 7888 (510) 668‐7888 HOSPITAL / CLINICS: Washington Hospital (510) 797‐3430 2000 Mowry Avenue Fremont, CA 94538 Alliance Occupational Medicine (408) 790‐2900 315 S. Abbott Ave Travelers MPM –TCT MPN (408) 790‐2912 fax Milpitas, CA 95035 EMERGENCY CHEMICAL ASSISTANCE: Chemtrec 24 Hr. Emergency (800) 424‐9300 Chemtrec Corporate (8:30 am‐5 pm (703) 527‐3887 ET) 800‐262‐8200 x1 800‐424‐9300 DOT Hazardous Material Information (800) 467‐4922 Local D.C. phone Center (202) 366‐4488 FAX‐ON‐DEMAND (202)366‐3753 FAX (800) 467‐4922 x2 Fremont Fire Department Hazmat (510) 494‐4280 9‐911 Chemical Spill (800) 645‐8265 (408) 451‐9047 ‐ 1030 Commercial St, #107, San Clean Harbors Jose, CA Gas Supplier (408) 492‐9080 Air Products, 2880 Lakeside Dr, #331 Santa Clara, CA UTILITIES – 24 HR: Alameda County (510) 668‐6500 Operating hours emergencies Water District Emergency (510) 668‐4200 After hours emergencies PG&E (800) 743‐5000 x1 Hazard reporting PG&E On call Rep (510) 828‐4884 Union City Sanitary District (510) 477‐7500 REVISIONS LIST i Copyright ©2015 Exar Corporation. -

Maxlinear Full-Spectrum Capture™ DOCSIS® 3.1 Chipsets Power Hitron’S Full Duplex Demonstration

October 17, 2017 MaxLinear Full-Spectrum Capture™ DOCSIS® 3.1 Chipsets Power Hitron’s Full Duplex Demonstration CARLSBAD, Calif.--(BUSINESS WIRE)-- MaxLinear, Inc. (NYSE:MXL), a leading provider of radio frequency (RF), analog and mixed-signal integrated circuits for the connected home, wired and wireless infrastructure, and industrial and multimarket applications, today announced that Hitron Technologies Inc. (TAIEX: 2419), a leading global telecommunications networking company, has picked MaxLinear front end receivers as part of a successful coexistence demonstration of its CODA family of DOCSIS® 3.1 cable modems in a Full Duplex (FDX) DOCSIS 3.1 demonstration network. The demonstration made use of MaxLinear's MxL277 and MxL278 Full-Spectrum Capture™ (FSC™) digital cable front-end receivers and the MxL236 upstream programmable gain amplifier. The demonstration also utilized the Intel® Puma™ 7 DOCSIS 3.1 SoC. The use of FDX technology provides broadband operators a path to deploy multi-gigabit upstream data speeds, enabling operators to deliver symmetric internet access speeds equivalent to fiber while extending the life of their existing hybrid coax cable plants. As part of the demonstration, Hitron is showcasing how its CODA family of cable modems are interoperable with future FDX signal environments and are ideal for cable operators who wish to deploy future-proof consumer premise equipment (CPE). Hitron’s CODA-45 models feature a 5MHz -85MHz fixed mid-split and multiple GigE ports (depending on the model), among other features. The CODA-47 models may be switched to 204MHz high-split enabling upstream speeds of 1Gbps. As utilized in Hitron’s CODA cable modem models, the MxL277 and MxL278 DOCSIS 3.1 tuners offer significant advantages in an all IP-based delivery of multimedia content and cloud services. -

Leveraging Wideband and Full Spectrum Receiver Capabilities To

ZCorum’s Ask a Broadband Expert Series: Leveraging Wideband and Full Spectrum Receiver Capabilities to Develop and Utilize Software-based Tools for Remote Spectrum Analysis and Troubleshooting A Technical Paper by Jim Koutras, Director of Product Marketing at MaxLinear and Scott Helms, VP of Technology at ZCorum 1.800.909.9441 4501 North Point Parkway, Suite 125 Alpharetta, GA 30022 ZCorum.com | TruVizion.com Facebook.ZCorum.com | Twitter.com/ZCorum Leveraging Wideband and Full Spectrum Receiver Capabilities to Develop and Utilize Software-based Tools for Remote Spectrum Analysis and Troubleshooting K. Scott Helms ZCorum Jim Koutras MaxLinear Abstract dedicated on-chip FFT hardware to transform time-sampled input signals to the frequency Spectrum analysis tools have been in use domain for subsequent user analysis and in the cable industry for troubleshooting and interpretation. design purposes for a long time. Traditionally this meant buying and maintaining large When the remote spectrum monitoring numbers of meters, spectrum analyzers, and function executes, the tuner inside the cable other specialized tools. This increased modem receives the spectrum information and expenses and training time, and limited the is commanded to fill an on-chip buffer with number of people in any organization who time-series data. Various windowing could leverage spectrum analysis. functions can be applied to time-series data on either side of the buffer to smooth Today, using new software in conjunction discontinuities at the window boundaries (thus with newer components in modems and set- reducing spectral leakage) and an FFT is top boxes, remote spectrum analysis is performed. The frequency-domain data read possible without purchasing specific test from the device are then interpolated as equipment. -

Maxlinear, Inc. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): March 30, 2021 MaxLinear, Inc. (Exact name of registrant as specified in its charter) Delaware 001-34666 14-1896129 (State or other jurisdiction (Commission (I.R.S. Employer of incorporation) File Number) Identification No.) 5966 La Place Court, Suite 100, Carlsbad, California 92008 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (760) 692-0711 N/A (Former name or former address, if changed since last report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions ( see General Instruction A.2. below): ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, $0.0001 par value MXL New York Stock Exchange Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2). -

(Lux) Worldwide Fund

Semi-Annual Report 30 September 2020 Wells Fargo (Lux) Worldwide Fund ▪ Alternative Risk Premia Fund ▪ China Equity Fund ▪ Emerging Markets Equity Fund ▪ Emerging Markets Equity Income Fund ▪ EUR Investment Grade Credit Fund ▪ EUR Short Duration Credit Fund ▪ Global Equity Fund ▪ Global Equity Absolute Return Fund ▪ Global Equity Enhanced Income Fund ▪ Global Factor Enhanced Equity Fund ▪ Global Investment Grade Credit Fund ▪ Global Long/Short Equity Fund ▪ Global Low Volatility Equity Fund ▪ Global Multi-Asset Income Fund ▪ Global Opportunity Bond Fund ▪ Global Small Cap Equity Fund ▪ Small Cap Innovation Fund ▪ U.S. All Cap Growth Fund ▪ U.S. High Yield Bond Fund ▪ U.S. Large Cap Growth Fund ▪ U.S. Select Equity Fund ▪ U.S. Short-Term High Yield Bond Fund ▪ U.S. Small Cap Value Fund ▪ USD Government Money Market Fund ▪ USD Investment Grade Credit Fund Alternative Risk Premia Fund, China Equity Fund, EUR Short Duration Credit Fund, Global Equity Enhanced Income Fund, Global Factor Enhanced Equity Fund, Global Investment Grade Credit Fund, Global Small Cap Equity Fund, Small Cap Innovation Fund and USD Government Money Market Fund have not been authorised by the Hong Kong Securities and Futures Commission and are not available for investment by Hong Kong retail investors. Wells Fargo (Lux) Worldwide Fund is incorporated with limited liability in the Grand Duchy of Luxembourg as a Société d’Investissement à Capital Variable under number RCS Luxembourg B 137.479. Registered office of Wells Fargo (Lux) Worldwide Fund: 80, route d’Esch, L-1470 Luxembourg, Grand Duchy of Luxembourg. Table of Contents Portfolio of investments Alternative Risk Premia Fund ....................................... -

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 In the Matter of ) ) Promoting the Deployment of 5G Open Radio ) GN Docket No. 21-63 Access Networks ) COMMENTS OF MAVENIR SYSTEMS, INC. Mavenir Systems, Inc. Caressa D. Bennet E. Alex Espinoza Womble Bond Dickinson (US) LLP 1200 19th Street, N.W. Suite 500 Washington, D.C. 20036 (202) 467-6900 Counsel for Mavenir Systems, Inc. Table of Contents I. THE PRESENT STATE OF OPEN RAN AND ITS STANDARDS ................................ 7 A. Current Ecosystem ........................................................................................................... 7 B. Current State of Standards and Foreign-Owned Incumbent Control Over Standards- Setting Bodies ............................................................................................................................. 9 C. eCPRI is Not an Alternative to Open RAN.................................................................... 12 II. OPEN RAN IS DEPLOYMENT-READY AND IN USE NOW ..................................... 14 A. Open RAN Domestic Deployments ............................................................................... 15 B. Open RAN International Deployments .......................................................................... 17 C. Open RAN Benefits ....................................................................................................... 19 D. Costs and Deployability ................................................................................................. 20 E. Disaggregation -

GCA Semiconductor Sector Report Q1 2018

SEMICONDUCTOR SECTOR REPORT Q1 2018 DEAL DASHBOARD Semiconductor $15.6 Billion Q1 2018 M&A Volume (1) Quarterly M&A Volume ($MM) (1) Quarterly M&A Deal Count (1) Top M&A Transactions - Since 2017 $70,000 20 Acquirer Target Transaction Value ($MM) 18 $59,211 (2) $60,000 K.K. Pangea $17,867 $51,522 Flash Memory 15 $50,000 13 12 $15,004 $40,000 10 10 9 9 $10,312 8 8 $30,000 7 $19,825 $20,000 $17,021 $6,843 $15,646 5 $8,634 $10,000 $6,494 $7,430 $3,200 $3,047 $0 0 Q1' 16 Q2' 16 Q3' 16 Q4' 16 Q1' 17 Q2' 17 Q3'17 Q4'17 Q1' 18 Q1' 16 Q2' 16 Q3' 16 Q4' 16 Q1' 17 Q2' 17 Q3' 17 Q4' 17 Q1' 18 $1,833 LTM Semiconductor Performance vs. SPX (3) Median M&A EV / NTM Revenue Over Time (4) 6.0x 50% ^SOX ^SPX 40% 4.4x 4.0x 31% 30% 3.1x 2.8x 20% 2.3x 2.2x 1.9x 2.0x 12% 1.3x 10% 0% 0.0x (10%) 2012 2013 2014 2015 2016 2017 YTD 2018 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Notes: Source: Capital IQ and 451 Group. Q1 financial information as of 03/31/2018. (1) Criteria based on global semiconductor transactions announced with transaction values greater than or equal to $20MM. (2) A special purpose acquisition company formed and controlled by Bain Capital-led consortium. Members of the consortium include: Bain Capital, SK Hynix, Toshiba, Hoya Corp, Apple, Kingston Technology, Seagate Technology and Dell Technologies. -

Maxlinear Mxl277 Full-Spectrum Capture™ DOCSIS® 3.1 Cable Receiver & Amplifier Chipset Powers Hitron’S DOCSIS® 3.1 CPE Family

December 1, 2016 MaxLinear MxL277 Full-Spectrum Capture™ DOCSIS® 3.1 Cable Receiver & Amplifier Chipset Powers Hitron’s DOCSIS® 3.1 CPE Family Hitron’s CODA-45 Data Modem, Latest Addition to its CODA™ Product Line, Achieves DOCSIS 3.1 Certification Based on the MxL277 Multi-Gigabit Front-End CARLSBAD, Calif.--(BUSINESS WIRE)-- MaxLinear, Inc. (NYSE: MXL), a leading provider of radio frequency (RF) and mixed-signal integrated circuits for broadband communications, the connected home, data center, metro, long-haul fiber networks, and wireless infrastructure, today announced that Hitron Technologies Inc. (TAIEX: 2419), a leading global telecommunications networking company, has successfully achieved Cable Labs® certification of its CODA-45 DOCSIS 3.1 cable modem using the MxL277 Full-Spectrum Capture™ (FSC™) digital cable front-end receiver, the MxL236 upstream programmable gain amplifier, and the Intel® Puma™ 7 DOCSIS 3.1 SoC. First in Hitron’s new multi-gigabit cable CPE family, the certified CODA-45 is capable of up to 5Gbps downstream over multi-carrier OFDM channels bonded with 32 single-carrier QAM channels and up to 1Gbps upstream throughput via DOCSIS 3.1. The two GigE ports deliver 1.97Gbps to the customer’s home. The CODA-45 not only enables cable operators to offer services that exceed current fiber optic data rates, but also allows them to use their existing cable plant infrastructure to provide multi-gigabit data services. Capturing up to the entire 1.2 Gigahertz (GHz) of fully deployed cable spectrum bandwidth to the home, the MxL277 DOCSIS 3.1 receiver enables cable operators to meet consumer demand for multi-gigabit data rates by the flexible deployment of spectrum bandwidth between the new OFDM and legacy QAM modulation based data services. -

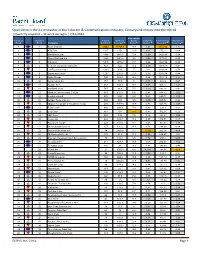

Qualcomm Is the #1 Innovator in the Telecom & Communications

Qualcomm is the #1 Innovator in the Telecom & Communications Industry, CenturyLink moves into the top 10 | Quarterly snapshot – 13 week averages | 7/11/2014 Innovation P revio us C urrent P atent Science C ycle Industry T echno lo gy R esearch R ank R ank Company Granted* Strength™ T ime™ Impact™ Strength™ Intensity™ 1 vw 1 Qualcomm Inc 2542 11755.5 9.9 1.21 4564.64 1.6 2 vw 2 AT&T Inc 1827 1151 10.9 1.02 2752.1 0.64 3 vw 3 BlackBerry Ltd 1486 1445.5 10.4 1.09 2406.49 0.98 4 vw 4 Cisco Systems Inc 1028 1561.8 9.6 1.02 1547.01 0.99 5 vw 5 Ericsson 1410 1475.8 7.7 0.64 1341.54 0.99 7 r 6 Verizon Communications Inc 741 322 11.2 1.17 1287.19 0.41 6 s 7 LG Electronics Inc* 1000 604 7 0.8 1193.28 0.79 8 vw 8 Samsung Group* 1207 255.8 7.3 0.58 1035.34 0.49 9 vw 9 Nokia Group 796 929.5 9.4 0.86 1015.18 1.14 12 r 10 CenturyLink Inc 151 17.5 8 4.18 934.8 0.67 11 vw 11 Google Inc* 567 654.5 9.7 1.08 905.11 1.21 10 s 12 SoftBank Corp 547 88.8 7.5 1.09 883.24 0.41 13 vw 13 Huaw ei Technologies Co Ltd 959 615.5 6.6 0.48 684.52 1.02 14 vw 14 Alcatel-Lucent 672 1021 8.5 0.63 629.71 1.18 16 r 15 Juniper Netw orks Inc 302 280 9.5 1.35 605.52 0.92 15 s 16 Nippon Telegraph & Telephone Corp 470 3079.5 11.9 0.76 526.95 1.47 17 vw 17 Fujitsu Ltd* 868 398.3 7.8 0.39 503.3 0.62 22 r 18 ZTE Corp 467 8.8 5.7 0.53 362.97 0.22 20 r 19 NEC Corp* 525 346 7.5 0.42 324.81 1.06 18 s 20 Avaya Inc 224 329.8 11.4 0.95 316.51 0.87 19 s 21 Panasonic Corp* 423 351.5 9.1 0.48 301.01 1.17 21 s 22 Motorola Solutions Inc 257 120.5 11.2 0.76 288.08 0.68 25 r 23 Skyhook Wireless -

Press Release

PRESS RELEASE SES YTD AND Q3 2015 RESULTS Luxembourg, 30 October 2015 – SES S.A. (NYSE Euronext Paris and Luxembourg Stock Exchange: SESG) reports financial results for the nine months and three months ended 30 September 2015. HIGHLIGHTS SES’s global business generating revenue and profit growth YTD 2015 revenue of EUR 1,492.6 million, up 6.1% (-2.9% at constant FX1) over prior year YTD 2015 EBITDA of EUR 1,106.5 million, up 5.4% (-3.6% at constant FX) over prior year YTD 2015 EBITDA margin of 74.1% (YTD 2014: 74.6%) YTD 2015 profit after tax up 3.7% to EUR 473.5 million Solid medium-term growth drivers in Global Video, Next Generation Data and ‘fibre in the sky’ HD TV channels grew 18.6% (YOY) to 2,178; HD penetration up from 28.6% to 30.6% of all channels Six commercial Ultra HD agreements now secured YTD 2015, with five channels already broadcasting Expanded StarTimes partnership with differentiated combination of infrastructure and services solutions SES’s SAT>IP Alliance gaining momentum and support across the industry Developing SES’s Next Generation Data business through partnerships with Post Telecom and Softwire O3b Networks now has 40 customers in service after first full year of operation Karim Michel Sabbagh, President and CEO, commented: “SES has continued to be productive in the third quarter 2015. SES has been first out of the starting gate in the commercial introduction of Ultra HD, building on the milestone of Europe’s first commercial UHD channel, pearl.tv – and adding further agreements in Europe and North America with Sky Deutschland, NASA TV, Fashion One, High 4K and TERN. -

1 in the United States District Court for The

Case 1:19-cv-02109-UNA Document 1 Filed 11/07/19 Page 1 of 24 PageID #: 1 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE DIFF SCALE OPERATION RESEARCH, LLC, Civil Action No._________ Plaintiff, JURY TRIAL DEMANDED v. MAXLINEAR, INC AND EXAR CORPORATION Defendants. COMPLAINT FOR PATENT INFRINGEMENT DIFF Scale Operation Research, LLC (“Plaintiff”), by its undersigned counsel, bring this action and make the following allegations of patent infringement relating to U.S. Patent Nos.: 7,881,413 (the “’413 Patent”) and 6,664,827 (the “’827 Patent”) (collectively, the “Patents-in- Suit”). Defendants MaxLinear, Inc. and Exar Corporation (collectively, “MaxLinear” or “Defendant(s)”) infringe each of the patents-in-suit in violation of the patent laws of the United States of America, 35 U.S.C. § 1 et seq. INTRODUCTION This case arises from MaxLinear’s infringement of a portfolio of semiconductor and network infrastructure patents. This patent portfolio arose from the groundbreaking work of ADC Telecommunications, Inc. (“ADC Telecommunications”) which . In 1935, ADC Telecommunications, then known as the Audio Development Company1 was founded in Minneapolis, Minnesota by two Bell Laboratory engineers to create 1 Audio Development Company was later renamed ADC Telecommunications, Inc. U.S. Senate Executive Reports, U.S. PRINTING OFFICE at 39 (1999) (“The story of ADC Telecommunications begins in 1935, the height of the great depression . The company got its start with a new innovation called the audiometer, an electronic device designed to test hearing.”). 1 Case 1:19-cv-02109-UNA Document 1 Filed 11/07/19 Page 2 of 24 PageID #: 2 custom transformers and amplifiers for the broadcast radio industry.