1214/4/8/13 Global Radio Holdings Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

EMBARGOED 00.01 2 February 2012 REGIONAL

PRESS RELEASE – EMBARGOED 00.01 2 February 2012 Year-on-Year growth for Smooth Radio UK and Real Radio brand Almost 5.6 million adults tune into a GMG Radio station each week – an extra 376,000 (YonY) Smooth Radio’s digital audience approaches 1 million adults each week GMG Radio’s Smooth Radio and Real Radio brands have recorded impressive year-on- year growth, according to the latest audience research out today (Thursday). 5.6 million adults now tune into one of the group’s stations each week - 376,000 more than a year ago. Smooth Radio UK’s weekly reach now stands at over 3.3 million adult listeners a week, up 231,000 on the same time last year. The audience also likes what they hear, with total hours listened to the station now standing at 25.75 million - almost two million (1.88m) more than a year ago – making it the UK’s second most listened to national commercial radio station. Simon Bates at Breakfast is celebrating his first year on Smooth Radio and has grown the breakfast audience by 69,000 to almost 1.4 million a week (YoY). For the group’s Real Radio brand the audience growth trend is also upwards. The stations, which broadcast on FM in Wales, Scotland, the North East and North West of England and Yorkshire and digitally across the UK, have added a total of 164,000 new adult listeners in the last year to give them a new weekly reach of just over 2.5 million adults. -

GMG Radio Response to the Ofcom Consultation on Review of Procedures for Handling Broadcasting Complaints, Investigations and Sanctions

GMG Radio response to the Ofcom consultation on review of procedures for handling broadcasting complaints, investigations and sanctions Introduction GMG Radio plc is part of The Guardian Media Group and operates fourteen analogue licences within the UK under the separate Real, Smooth and Rock Radio brands. The company was an inaugural partner and is currently a 35% shareholder in the MXR regional multiplex consortium as well as being a long-term service provider on each of its platforms. GMG Radio is also a founding partner and stakeholder in Digital Radio UK, the body charged with helping prepare the UK for digital switchover. GMG Radio considers regulatory compliance to be a hugely important and crucial element to our overall business operation and welcomes proposals which are genuinely designed to assist in improving standards and enhance understanding of regulatory procedures. We note this consultation seeks stakeholder views on proposed changes to procedures as opposed to responses to specific questions. Current understanding Ofcom has no wish to dilute the current process by which it can diligently follow when investigating breaches of broadcast licences, investigating complaints including those on fairness and privacy issues and the consideration of statutory sanctions for proven breaches. As such this consultation is specifically placed within the public arena in order to enlist stakeholder opinions on planned changes which are ultimately designed to ensure an ongoing commitment to the principles of continued fairness to those directly involved and at the same time introduce new procedures which are clearer, simpler and can be implemented as effectively and efficiently as possible. The consultation documents sets out proposals for new procedures covering the handling of broadcasting complaints, investigations and sanctions and it invites written views and comments on each of them prior to the publishing of a finalized version. -

3 Radio and Audio Content 3 3.1 Recent Developments in Scotland

3 Radio and audio content 3 3.1 Recent developments in Scotland Real Radio Scotland has been rebranded as Heart In February 2014 Capital Scotland was sold to the Irish media holding company, Communicorp. It was sold as part of eight stations divested by Global Radio to satisfy the UK regulatory authorities following the acquisition, two years ago, of GMG Radio from Guardian Media Group. Under a brand licensing agreement, Communicorp has rebranded the 'Real' stations under the 'Heart' franchise and plans to relaunch the 'Smooth' stations following the reintroduction of local programming. Therefore, Real Radio Scotland was rebranded as Heart Scotland in May 2014. XFM Scotland was re-launched by its owners, Global Radio, in March 2014. 3.2 Radio station availability Five new community radio stations are available to listeners in Scotland Scotland’s community radio industry has continued to grow. There are now 23 community stations on air, out of the 31 licences that have been awarded in Scotland. New to air in 2013/14 were East Coast FM, Irvine Beat FM, Crystal Radio, and K107 FM. Irvine Beat FM has received funding from the Lottery Awards for All fund to build a training studio. Nevis Radio, which serves Fort William and the surrounding areas, was originally licensed as a commercial radio service, but having chosen to become a community radio service it was awarded this licence instead, on application. The remaining eight of the most recent round of licence awards are preparing to launch. A licensee has two years from the date of the licence award in which to launch a service. -

Localness on Commercial Radio Full Name Erzsebet “Erzsie” Nagy Contact Phone Number N/A Representing (Delete As Appropriate) Self Organisation Name N/A

Consultation response form Consultation title Localness on commercial radio Full name Erzsebet “Erzsie” Nagy Contact phone number N/A Representing (delete as appropriate) Self Organisation name N/A Your response Question Your response Question 1: Do you agree that Ofcom’s duty to secure ‘localness’ on local commercial radio Before I write anything, I should state that I am stations could be satisfied if stations were able a U.S. citizen and do not reside in the United to reduce the amount of locally-made Kingdom or have British citizenship, but have programming they provide? If not, please visited occasionally and know of people in the explain the reasons and/or evidence which UK. support your view. There was nothing in the Ofcom rules that stated a U.S. citizen could not participate, so I have decided to participate anyway. All content is original research. ---- Localness should never be reduced on local commercial radio stations. There is research to back this up, proven by statistical research from 2008-2014. There is substantial research that proves listeners value local content to some extent, and not just in major circumstances like floods, terrorist attacks, fire, major emergencies. Rather than reducing local-made programming, some radio stations should be, by statutory requirement, have as much local programming and content as necessary. There is substantial evidence from American researchers – 2004, 2008, 2012, 2014 that proved listeners value locality as a major selling point. Unofficial research in 2007 has proved this. No station should be local for only 3 hours a day, whatever the day of week. -

Hallett Arendt Rajar Topline Results - Wave 3 2019/Last Published Data

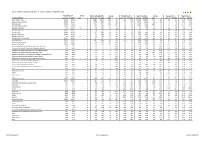

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2019/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W3 2019 000's % Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 Bauer Radio - Total 55032 55032 0 0% 18083 18371 288 2% 33% 33% 156216 158995 2779 2% 8.6 8.7 15.3% 15.9% Absolute Radio Network 55032 55032 0 0% 4743 4921 178 4% 9% 9% 35474 35522 48 0% 7.5 7.2 3.5% 3.6% Absolute Radio 55032 55032 0 0% 2151 2447 296 14% 4% 4% 16402 17626 1224 7% 7.6 7.2 1.6% 1.8% Absolute Radio (London) 12260 12260 0 0% 729 821 92 13% 6% 7% 4279 4370 91 2% 5.9 5.3 2.1% 2.2% Absolute Radio 60s n/p 55032 n/a n/a n/p 125 n/a n/a n/p *% n/p 298 n/a n/a n/p 2.4 n/p *% Absolute Radio 70s 55032 55032 0 0% 206 208 2 1% *% *% 699 712 13 2% 3.4 3.4 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1779 1824 45 3% 3% 3% 9294 9435 141 2% 5.2 5.2 0.9% 1.0% Absolute Radio 90s 55032 55032 0 0% 907 856 -51 -6% 2% 2% 4008 3661 -347 -9% 4.4 4.3 0.4% 0.4% Absolute Radio 00s n/p 55032 n/a n/a n/p 209 n/a n/a n/p *% n/p 540 n/a n/a n/p 2.6 n/p 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 741 721 -20 -3% 1% 1% 3438 3703 265 8% 4.6 5.1 0.3% 0.4% Hits Radio Brand 55032 55032 0 0% 6491 6684 193 3% 12% 12% 53184 54489 1305 2% 8.2 8.2 5.2% 5.5% Greatest Hits Network 55032 55032 0 0% 1103 1209 106 10% 2% 2% 8070 8435 365 5% 7.3 7.0 0.8% 0.8% Greatest Hits Radio 55032 55032 0 0% 715 818 103 14% 1% 1% 5281 5870 589 11% 7.4 7.2 0.5% -

Hallett Arendt Rajar Topline Results - Wave 1 2020/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 1 2020/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W1 2020 000's % Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 Bauer Radio - Total 55032 55032 0 0% 18160 17986 -174 -1% 33% 33% 155537 154249 -1288 -1% 8.6 8.6 15.9% 15.7% Absolute Radio Network 55032 55032 0 0% 4908 4716 -192 -4% 9% 9% 34837 33647 -1190 -3% 7.1 7.1 3.6% 3.4% Absolute Radio 55032 55032 0 0% 2309 2416 107 5% 4% 4% 16739 18365 1626 10% 7.3 7.6 1.7% 1.9% Absolute Radio (London) 12260 12260 0 0% 715 743 28 4% 6% 6% 5344 5586 242 5% 7.5 7.5 2.7% 2.8% Absolute Radio 60s 55032 55032 0 0% 136 119 -17 -13% *% *% 359 345 -14 -4% 2.6 2.9 *% *% Absolute Radio 70s 55032 55032 0 0% 212 230 18 8% *% *% 804 867 63 8% 3.8 3.8 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1420 1459 39 3% 3% 3% 7020 7088 68 1% 4.9 4.9 0.7% 0.7% Absolute Radio 90s 55032 55032 0 0% 851 837 -14 -2% 2% 2% 3518 3593 75 2% 4.1 4.3 0.4% 0.4% Absolute Radio 00s 55032 55032 0 0% 217 186 -31 -14% *% *% 584 540 -44 -8% 2.7 2.9 0.1% 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 740 813 73 10% 1% 1% 4028 4209 181 4% 5.4 5.2 0.4% 0.4% Hits Radio Brand 55032 55032 0 0% 6657 6619 -38 -1% 12% 12% 52607 52863 256 0% 7.9 8.0 5.4% 5.4% Greatest Hits Network 55032 55032 0 0% 1264 1295 31 2% 2% 2% 9347 10538 1191 13% 7.4 8.1 1.0% 1.1% Greatest Hits Radio 55032 55032 0 0% 845 892 47 6% 2% 2% 6449 7146 697 11% 7.6 8.0 0.7% -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 22Nd June 2008

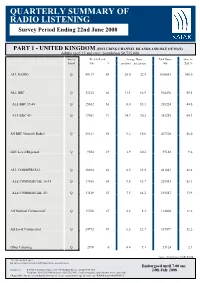

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 22nd June 2008 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 50,735,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % ALL RADIO Q 45117 89 20.0 22.5 1016681 100.0 ALL BBC Q 33323 66 11.1 16.9 564476 55.5 ALL BBC 15-44 Q 15362 61 8.0 13.1 201224 44.6 ALL BBC 45+ Q 17961 71 14.3 20.2 363252 64.3 All BBC Network Radio¹ Q 29611 58 9.2 15.8 467328 46.0 BBC Local/Regional Q 9504 19 1.9 10.2 97148 9.6 ALL COMMERCIAL Q 30984 61 8.5 13.9 431081 42.4 ALL COMMERCIAL 15-44 Q 17465 69 9.5 13.7 239533 53.1 ALL COMMERCIAL 45+ Q 13519 53 7.5 14.2 191547 33.9 All National Commercial¹ Q 13760 27 2.2 8.3 114002 11.2 All Local Commercial Q 24992 49 6.2 12.7 317079 31.2 Other Listening Q 2978 6 0.4 7.1 21124 2.1 Source: RAJAR/Ipsos MORI/RSMB ¹ See note on back cover. For survey periods and other definitions please see back cover. Embargoed until 7.00 am Enquires to: RAJAR, Paramount House, 162-170 Wardour Street, London W1F 8ZX 24th July 2008 Telephone: 020 7292 9040 Facsimile: 020 7292 9041 e mail: [email protected] Internet: www.rajar.co.uk ©Rajar 2008. -

Celebrating 40 Years of Commercial Radio With

01 Cover_v3_.27/06/1317:08Page1 CELEBRATING 40 YEARS OF COMMERCIAL RADIOWITHRADIOCENTRE OFCOMMERCIAL 40 YEARS CELEBRATING 01 9 776669 776136 03 Contents_v12_. 27/06/13 16:23 Page 1 40 YEARS OF MUSIC AND MIRTH CONTENTS 05. TIMELINE: t would be almost impossible to imagine A HISTORY OF Ia history of modern COMMERCIAL RADIO music without commercial radio - and FROM PRE-1973 TO vice-versa, of course. The impact of TODAY’S VERY privately-funded stations on pop, jazz, classical, soul, dance MODERN BUSINESS and many more genres has been nothing short of revolutionary, ever since the genome of commercial radio - the pirate 14. INTERVIEW: stations - moved in on the BBC’s territory in the 1960s, spurring Auntie to launch RADIOCENTRE’S Radio 1 and Radio 2 in hasty response. ANDREW HARRISON From that moment to this, independent radio in the UK has consistently supported ON THE ARQIVAS and exposed recording artists to the masses, despite a changing landscape for AND THE FUTURE broadcasters’ own businesses. “I’m delighted that Music Week 16. MUSIC: can be involved in celebrating the WHY COMMERCIAL RadioCentre’s Roll Of Honour” RADIO MATTERS Some say that the days of true ‘local-ness’ on the UK’s airwaves - regional radio for regional people, pioneered by 18. CHART: the likes of Les Ross and Alan Robson - are being superseded by all-powerful 40 UK NO.1 SINGLES national brands. If that’s true, support for the record industry remains reassuringly OVER 40 YEARS robust in both corners of the sector. I’m delighted that Music Week can be involved in celebrating the RadioCentre’s 22. -

Group Accounts 2014 FINAL

Registered no. 94531 Guardian Media Group plc 2014 Annual Report and Financial Statements FINAL Consol v4 Guardian Media Group plc Page 2 Registered no. 94531 Contents List of directors and advisers 3 Strategic report 4 Report of the directors 6 Independent auditors' report 7 Consolidated income statement 8 Consolidated statement of comprehensive income 8 Consolidated balance sheet 9 Consolidated statement of changes in equity 10 Consolidated statement of cash flows 10 Notes relating to the financial statements 11 Company financial statements of Guardian Media Group plc 30 Addresses 39 Guardian Media Group plc Page 3 Registered no. 94531 List of directors and advisers The directors of the Company who were in office during the year and up to the date of signing the financial statements were: Neil Berkett Nick Backhouse Judy Gibbons Brent Hoberman Andrew Miller Nigel Morris Alan Rusbridger Darren Singer Ronan Dunne (appointed 14 May 2013) John Paton (appointed 14 May 2013) Jennifer Duvalier (appointed 21 May 2014) Amelia Fawcett DBE (resigned 24 September 2013) Secretary Philip Tranter Independent auditors PricewaterhouseCoopers LLP Chartered Accountants and Statutory Auditors 1 Embankment Place London WC2N 6RH Solicitors Freshfields Bruckhaus Deringer LLP 65 Fleet Street London EC4Y 1HS Bankers The Royal Bank of Scotland Group Division of Large Corporate Banking 280 Bishopsgate London EC2M 4RB Guardian Media Group plc Page 4 Registered no. 94531 Strategic report The directors present their strategic report, the report of the directors and the audited consolidated financial statements for the Group, comprising the Guardian Media Group plc (the “Company”) and its subsidiaries, joint ventures and associate investments (“the Group”), for the year ended 30 March 2014. -

By Global Radio

Annexes to the report on the Global Radio/GMG Radio public interest test Report on public interest test on the acquisition of Guardian Media Group’s radio stations (Real and Smooth) by Global Radio ANNEXES 0 Annexes to the report on the Global Radio/GMG Radio public interest test Contents 1 Annex 1: Glossary Annex 2: Summary of stakeholder representations 2 Annex 3: Information received from OFT Annex 4: Area by area analysis 1 Annexes to the report on the Global Radio/GMG Radio public interest test Annex 1 3 Glossary BARB Broadcasters Audience Research Board. The pan-industry body that measures television viewing. Broadband A service or connection generally defined as being ‘always on’ and providing a bandwidth greater than narrowband. Communications Act Communications Act 2003, which came into force in July 2003. ‘Connected’ TV A television that is broadband-enabled to allow viewers to access internet content. DAB Digital audio broadcasting. A set of internationally-accepted standards for the technology by which terrestrial digital radio multiplex services are broadcast in the UK. DCMS Department for Culture, Media and Sport Digital switchover The process of switching over the analogue television or radio broadcasting system to digital. DTT Digital terrestrial television. The television technology that carries the Freeview service. First-run acquisitions A ready-made programme bought by a broadcaster from another rights holder and broadcast for the first time in the UK during the reference year. First-run originations Programmes commissioned by or for a licensed public service channel with a view to their first showing on television in the United Kingdom in the reference year. -

Global Radio Holdings Limited of Juice Holdco Limited

Anticipated acquisition by Global Radio Holdings Limited of Juice Holdco Limited Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. The CMA’s decision on reference under section 33(1) of the Enterprise Act 2002 given on 5 October 2015. Full text of the decision published on 22 October 2015. ME/6546/15 SUMMARY 1. Global Radio Holdings Limited (Global) has agreed to acquire Juice Holdco Limited (Juice) (the Merger). Global and Juice are together referred to as the Parties. 2. The Competition and Markets Authority (CMA) considers that the Parties will cease to be distinct as a result of the Merger, that the share of supply test is met and that accordingly arrangements are in progress or in contemplation which, if carried into effect, will result in the creation of a relevant merger situation. 3. The Parties overlap in the supply of commercial radio services, a two-sided market in which radio stations compete both for advertisers and consumers (in this case, radio listeners). In this case, the CMA has focussed on the effect of this Merger on the advertisers’ side of the market as the CMA considers that the interests of listeners are largely protected through Ofcom’s licencing requirements and the presence of the BBC. In terms of geographic scope, the CMA assessed the effect of the Merger in those areas where the Parties currently operate (ie the Total Survey Area (TSA))1 and where there is some overlap either at a regional or local level. -

Bauer Radio Ltd / TIML Golden Square

Anticipated acquisition by Bauer Radio Limited of TIML Golden Square Limited (Absolute Radio) The OFT’s decision on reference under section 33(1) given on 20 December 2013. Full text of decision published 10 January 2014. Please note that the square brackets indicate figures or text which have been deleted or replaced in ranges at the request of the parties or third parties for reasons of commercial confidentiality. PARTIES 1. Bauer Radio Limited ('Bauer') is a UK-based division of Bauer Media Group, a multi-national media group covering print, online, radio and TV. In 2012, Bauer's total UK radio turnover was approximately £[ ]million with advertising revenues accounting for approximately £[ ]million. Bauer currently holds 41 local and eight national commercial radio licences which Bauer transmits on AM, FM, digital audio broadcasting ('DAB'), Digital Terrestrial Television ('DTT'), satellite, cable and the internet across the UK. Bauer's key brands include Kiss and Magic in addition to multiple local radio stations. 2. Absolute Radio ('Absolute') is owned by TIML Golden Square Limited ('TIML'), which is in turn owned by TIML Global Limited, a subsidiary of The Times of India Group. Absolute's 2012 UK turnover is £[ ]. Absolute Radio broadcasts across its national AM licence, a London FM licence and national DAB services, all under the Absolute brand. 1 TRANSACTION 3. On 26 July 2013, Bauer signed a Share Purchase Agreement to acquire the entire issued share capital of TIML, the owner of Absolute Radio (the 'Merger'). Completion of the Merger is subject clearance by the UK competition authorities. 4. On 25 October 2013, the OFT received an informal submission from the parties concerning the Merger.