Audit Report on the Accounts of District Government Haripur

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

KPK-PDHQ) (219)Result for the Post of Male Warder (BPS - 05) Zone 5 PAKISTAN TESTING SERVICE MERIT LIST MALE (ZONE-5

KPK PRISONS DEPARTMENT (KPK-PDHQ) (219)Result for the post of Male Warder (BPS - 05) Zone 5 PAKISTAN TESTING SERVICE MERIT LIST MALE (ZONE-5) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Higher Total Obtained Marks of Matric Matric Experience Interview Grand Sr # Name Father Name Contact # District Address DOB Height Chest Runnning Higher Qualification Qualification Screening Screening Column Division Marks Marks Marks Total Marks Marks Marks 13+14+17 1 Sayyed Faisal Shah Zaffer Shah 03464404474 Mansehra Village Brat P/o Jinkiari Tehsil And Distt: Mansehra Feb 28 1991 5x9 39-40 pass 1st Division Graduation 70 8 100 52 130 4 134 2 Wajid Bashir Muhammad Bashir 03435876662 Abbottabad Moh Batta Kari Vill Nagribala Po Kala Bagh Nov 10 1990 5x7 34-35 Pass 1st Division Intermediate/HSSC 70 6 100 51 127 6 133 Dharmang Dhodial Argushai Po Dhodial D/T 3 Hassan Sufiyan Muhammad Sufiyan 03175575636 Mansehra Jan 13 1997 5x11 37-39 Pass 1st Division Intermediate/HSSC 70 6 100 53 129 4 133 Mansehra Village Chittian P/O Qalanderabad Tehsil And Distric 4 Bilal Khan Muhammad Younis 03109326326 Abbottabad Jan 15 1992 5x11 34-36 Pass 1st Division Graduation 70 8 100 47 125 5 130 Abbottabad H No 653/2 St No 5 Mohallah Farooq E Azam Kunj 5 Faisal Pervaiz Muhammad Pervaiz 03479730496 Abbottabad Jun 5 1992 5x7 34-36 Pass 1st Division Graduation 70 8 100 46 124 6 130 Qadeem 6 Sami Ullah Khan Abdul Hanan Khan 03145089747 Abbottabad Mohallah Khizer Zai Mirpur Abbottabad Oct 1 1989 5x8 39-40 Pass 2nd Division Masters and Above 53 12 100 58 123 6 129 7 Hamid -

Pakistan: Humanitarian Assistance for Internally Displaced People

Pakistan: Humanitarian Emergency appeal n° MDRPK003 Operations update n° 5 assistance for internally 23 July 2009 displaced people Period covered by this Ops Update: 9 to 23 July 2009; Appeal target (current): CHF 7,974,809 (USD 7,341,928 or EUR 5,251,486); <click here to view the attached Revised Emergency Appeal Budget> Appeal coverage: 44%. This percentage includes contributions which are currently in the pipeline. <click here to go directly to the updated donor response report, or here to link to contact details > Appeal history: • This Emergency Appeal was launched on 4 June 2009 for CHF 23.9 million for seven months to assist 140,000 people (20,000 families). • On 5 June a meeting was held in Geneva, hosted by the International Federation and the International Committee of the Red Cross (ICRC) with the Pakistan Red Crescent Society (PRCS) representatives, to present the Red Cross Red Crescent Movement response for this humanitarian crisis. The importance of a strong Movement coordination framework was agreed. A joint statement was issued at the end of June clarifying roles and responsibilities of Movement partners. • A Revised Emergency Appeal was launched on 6 July 2009 for CHF 7,974,802 to assist 91,000 displaced PRCS mobile health unit doctor examines a patient in people (13,000 families). Pandi (Hattar union council in Haripur district). This mobile health unit visits seven locations in one week. Summary: The North-West Frontier Province Photo: International Federation/Wajiha Kamran. (NWFP) government has started the repatriation process of internally displaced people (IDP). More than 39,780 families have returned to their homes (mostly from the IDP camps, west of Indus river). -

Male / Co-Education) and Male Head of Institution at Ssc Level Upto 14-07-2021

1 LIST OF AFFILIATED INSTITUTIONS WITH STATUS (MALE / CO-EDUCATION) AND MALE HEAD OF INSTITUTION AT SSC LEVEL UPTO 14-07-2021 Inst Inst Principal S.No Inst Adress Gender Principal Name Phone No Principal Mobile No level Code Gender Angelique School, St.No.81, Embassy 051-2831007-8, 1. SSC 1002 Co-Education Maj (R) Nomaan Khan MALE 0321-5007177 Road, G-6/4, Islamabad 0321-5007177 Sultana Foundation Boys High School, 2. SSC 1042 Farash Town, Lehtrar Road (F.A), MALE WASEEM IRSHAD MALE 051-2618201 (Ext 152) 0315-7299977 Islamabad Scientific Model School, 25-26, Humak 051-4491188 , 3. SSC 1051 Co-Education KHAWAJA BASHIR AHMAD MALE 0345-5366348 (F.A), Islamabad 0345-5366348 Fauji Foundation Model School, Chak Wing Cdre Muhammad Laeeq 051-2321214, 4. SSC 1067 Co-Education MALE 0320-5635441 Shahzad Campus (F.A), Islamabad. Akhtar 0321-4044282 Academy of Secondary Education, Nai 051-4611613, 5. SSC 1070 Abadi G.T Road, Rewat (F.A), Co-Education Mr. AZHAR ALI SHAH MALE 0314-5136657 0314-5136657 Islamabad National Public Secondary School, G. 051-4612166, 6. SSC 1077 Co-Education IRFAN MAHMOOD MALE 03005338499 T Road, Rewat (F.A), Islamabad 0300-5338499 National Special Education Centre for 9260858, 7. SSC 1080 Physically Handicapped Children, G- Co-Education Islam Raziq MALE 0333-0732141 9263253 8/4, Islamabad Oxford High School, 413, Street No 43, 8. SSC 1083 Co-Education Lt. Col. Zafar Iqbal Malik (Retd) MALE 051-2253646 0321-5010789 Sector G-9/1, Islamabad Rawat Residential College, college 9. SSC 1090 Co-Education Tanzeela Malik Awan MALE 051-2516381 03465296351 Road, Rawat (F.A), Islamabad Sir Syed Ideal School System, House 10. -

Compulsory Registration Northern Region

Khyber Pakhtunkhwa Revenue Authority (KPRA) Compulsory Registration Northern Region Principal Date of KPRA Comp Date of S.No Order No. Businsess Name Address STATUS KNTN Activities Effect Reg No Comp Reg Glaga, Bagnoter, Cabel 1 04/2019 UFAK CABLE NETWORK, BAGNOTER Feb 14, 19 9835000087 Feb 19, 19 UNREGD #N/A District Abbottabad. Operator Mohalla Londi Cham, Post Office Cabel 2 05/2019 WORLD TOUCH CABLEL NETWORK Feb 14, 19 9835000088 Feb 19, 19 UNREGD #N/A Dhamtore, Tehsil & Operator District Abbottabad Village Dobather, Cabel 3 06/2019 SHIMLA COMMUNICATIONS Mohallah Bagh, Feb 14, 19 9835000089 Feb 19, 19 UNREGD #N/A Operator Abbottabad. Juma Khan, Village Sherwan Kalan, Post Cabel 4 07/2019 LABI KHAN CABLE NETWORK Office Sherwan, Feb 14, 19 9835000090 Feb 19, 19 UNREGD #N/A Operator Tehsil and District Abbottabad. Naveed Ahmed, Village Bigakot, Cabel 5 08/2019 SNA COMMUNICATIONS Union Council Feb 14, 19 9835000091 Feb 19, 19 UNREGD #N/A Operator Kuthiala, Abbottabad. Principal Date of KPRA Comp Date of S.No Order No. Businsess Name Address STATUS KNTN Activities Effect Reg No Comp Reg Mir Alam Market, Opposite GBPS, Cabel 6 10/2019 SHERWAN CABLE NETWORK Feb 14, 19 9835000093 Feb 19, 19 UNREGD #N/A Sherwan Kalan, Operator District Abbottabad. Opposite PTCL Exchange, Post Cabel 7 11/2019 BAKOT CABLE NETWORK, BAKOT Office Butti, Bakot, Feb 14, 19 9835000094 Feb 19, 19 UNREGD #N/A Operator Tehsil & District Abbottabad. Main Bazar Lora Village, Tehsil Cabel 8 12/2019 LORA CABLE NETWORK, LORA, HAVELIAN Feb 14, 19 9835000095 Feb 19, 19 UNREGD #N/A Havelian District Operator Abbottabad. -

Open UBL Branches

S.No Branch Code Branch Name Region Province Branch Address 1 0024 Ameen mirpur Azad Kashmir AJK PROPERTY # 21, SECTOR # A-5, SALEEM PLAZA, ALLAMA IQBAL ROAD, MIRPUR 2 0139 Main branch,mirpur Azad Kashmir AJK OPP. POLICE LINES, MIRPUR, AZAD KASHMIR 3 0157 Dadyal Azad Kashmir AJK Noor Alam Tower<Plot No. 412, Dadyal, District Mirpur, Azad Kashmir 4 0160 Main road chakswari Azad Kashmir AJK KHASRA # 20 BROOTIIAN P.O CHAKSWARI, TEH.& DISTT.MIRPUR, AZAD KASHMIR. 5 0224 Kotli Azad Kashmir AJK OLD BUS ADDA MAIN BAZAR KOTLI AZAD KASHMIR GROUND FLOOR, ASHRAF CENTRE, MIRPUR CHOWK BHIMBER,TEHSIL BHIMBER, DISTRICT 6 0229 Bhimber Azad Kashmir AJK MIRPUR, AZAD KASHMIR. 7 0250 Akalgarh azad kashmir Azad Kashmir AJK MAIN BAZAR AKALGARH, TEH.& DISTT. MIRPUR, AZAD KASHMIR. 8 0348 Mangoabad a k Azad Kashmir AJK MANGOABAD,PO.KANDORE TEHSIL DADYAL, DISTRICT MIRPUR, AZAD KASHMIR 9 0380 Siakh Azad Kashmir AJK VILL.& PO.SIAKH, TEHSIL DADYAL, DISTRICT MIRPUR,A.K. 10 0467 Sector f/3 branch, mirpur Azad Kashmir AJK PLOT # 515 SECTOR F-3 (PART-1) KOTLI ROAD MIRPUR AZAD KASHMIR 11 0502 Pind kalan Azad Kashmir AJK PIND KALAN, TEH. & DISTT. MIRPUR AZAD KASHMIR. 12 0503 Chattro Azad Kashmir AJK POST OFFICE CHATTRO, TEHSIL DADYAL, DISTRICT MIRPUR, AZAD KASHMIR. 13 0539 New market ratta a.k. Azad Kashmir AJK VILL.& P.O. RATTA, TEHSIL DADYAL, DISTRICT MIRPUR,A.K. 14 0540 Rakhyal Azad Kashmir AJK POST OFFICE AKALGARH TEH.& DISTT.MIRPUR, AZAD KASHMIR. 15 0567 Ghelay Azad Kashmir AJK REHMAT PLAZA MAIN ROAD JATLAN GHELAY, P.O. , TEH.& DISTT. -

Distributions and Folk Tibb Knowledge of Milk Thistle (Silybum Marianum L.) in NWFP, Pakistan

Ethnobotanical Leaflets 14: 268-73, 2010. Distributions and Folk Tibb Knowledge of Milk Thistle (Silybum marianum L.) in NWFP, Pakistan Khalid Hussain*, Syed Zia-ul-Hussnain and Aamir Shahazad *Shakarganj Sugar Research Institute, Toba Road Jhang (Punjab), Pakistan E-mail: [email protected] Issued: March 01, 2010 Abstract The purpose of our survey was to collect distribution data and folk tibb knowledge of milk thistle at NWFP Pakistan. NWFP area’s including District Haripur and Abbottabad were visited during 2007 and 2008 in the month of December. Milk thistle (Silybum marianum L.) was found growing wildly covering about 20-52% area. A total of 90 Hakims and 90 local peoples were interviewed regarding the use of Milk thistle. It was concluded that Milk thistle was used for liver disease especially for Hepatitis. About 75% from interviewed community were using it seeds while 25% preferred to use its whole plant as medicine. Key notes: Medicinal plants, folk tibb knowledge, Milk thistle. Introduction The history of discovery and use of different medicinal plants is as old as the history of discovery and use of plants for food (Ibrar, 2002). Medicinal plants play a key role in traditional health care system and a number of allopathic drugs are comprises of medicinal plants in the industrialized countries (Rashid and Arshad, 2002). Haripur and Abbottabad lie between 33° 50’ to 34° 23’ North latitudes and 72° 35’ to 73° 31’ East longitudes. The climate of Hattar is moderate. During summer season, the climate is hot average temperature ranges between 30-35oC. The winter season is very cool and extends from November to March. -

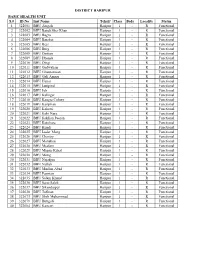

Class Beds Locality Status 1 322001 BHU Amgah Haripur 1

DISTRICT HARIPUR BASIC HEALTH UNIT S.# ID No Inst Name Tehsil/ Class Beds Locality Status 1 322001 BHU Amgah Haripur 1 - R Functional 2 322002 BHU Bandi Sher Khan Haripur 1 - R Functional 3 322003 BHU Bagra Haripur 1 - R Functional 4 322004 BHU Barakot Haripur 1 - R Functional 5 322005 BHU Beer Haripur 1 - R Functional 6 322006 BHU Burg Haripur 1 - R Functional 7 322008 BHU Dartian Haripur 1 - R Functional 8 322009 BHU Dhenda Haripur 1 - R Functional 9 322010 BHU Dingi Haripur 1 - R Functional 10 322011 BHU Gadwalian Haripur 1 - R Functional 11 322012 BHU Ghumanwan Haripur 1 - R Functional 12 322013 BHU Gali Amazi Haripur 1 - R Functional 13 322014 BHU Hattar Haripur 1 - R Functional 14 322015 BHU Jattipind Haripur 1 - R Functional 15 322016 BHU Job Haripur 1 - R Functional 16 322017 BHU Kalinger Haripur 1 - R Functional 17 322018 BHU Kangra Colony Haripur 1 - R Functional 18 322019 BHU Kariplian Haripur 1 - R Functional 19 322020 BHU Kakotri Haripur 1 - R Functional 20 322021 BHU Kohi Nara Haripur 1 - R Functional 21 322022 BHU Koklian Peeran Haripur 1 - R Functional 22 322023 BHU Kotohara Haripur 1 - R Functional 23 322024 BHU Kundi Haripur 1 - R Functional 24 322025 BHU Luder Mong Haripur 1 - R Functional 25 322026 BHU Chantry Haripur 1 - R Functional 26 322027 BHU Manakrai Haripur 1 - R Functional 27 322028 BHU Meelam Haripur 1 - R Functional 28 322029 BHU Mirpur Kahal Haripur 1 - R Functional 29 322030 BHU Mong Haripur 1 - R Functional 30 322031 BHU Najafpur Haripur 1 - R Functional 31 322032 BHU Nullah Haripur 1 - R Functional 32 322033 BHU Muslim Abad Haripur 1 - R Functional 33 322034 BHU Pannian Haripur 1 - R Functional 34 322035 BHU Salam Khund Haripur 1 - R Functional 35 322036 BHU Sarai Saleh Haripur 1 - R Functional 36 322037 BHU Sikandarpur Haripur 1 - R Functional 37 322038 BHU Tofkian Haripur 1 - R Functional 38 322073 BHU Shah Muhammad Haripur 1 - R Functional 39 322079 BHU Buttgali Haripur 1 - R Functional 40 322084 BHU Kaneeri Haripur 1 - R Functional DISPENSARY 1 322041 Civil Dispy. -

REPORT of Mos and Mts TRAINING, District Haripur (28Th December, 2016)

REPORT OF MOs AND MTs TRAINING, District Haripur (28th December, 2016) Background: This Training (MOs and MTs on PEC) was held in lecture hall DHQ Hospital Haripur. Report of MOs and MTs Training on PEC District Haripur 2016 Initially we had some problem in adjusting the date for training so that all participants make their presence sure. After the extensive efforts of Dr Junaid Faisal Wazir through meeting, telephonic discussion and Mobilizing haripur Team at last Training Date was finalized from DHO office. Training was held at lecture hall DHQ hospital Haripur on 28th December at District Haripur. List of Facilitators and Participants is as follow: Facilitator 1. Dr. Junaid Faisal Wazir (CCO/AP) PICO HMC Project Team 2. Mr Nifaz Ulllah (Optometrist), DHQ Hospital Haripur 3. Mr Abid Ali (Optometrist), DHQ Hospital Haripur 4. Mr Habib Ullah (Social Organizer), DHQ Hospital Haripur 5. Mr Fiaz Ali (Social Organizer), DHQ Hospital Haripur Below are lists of Participants MEDICAL OFFICERS S# NAME CENTRE OF DUTY 1 Dr Muhammad saeed CH Rehana 2 Dr gulab hussain Ch KOTLA 3 Dr Muhammad asad khan CH KTS 4 Dr seerat khan BHU KOTLIA PIRAN 5 Dr akhjlaq khan BHU JATII PAND 6 Dr asad mahmood BHU BEER 7 Dr usman asghar BHU DHENDA 8 Dr saima akbar BHU KOHI NARA 9 Dr bushra rafeeq BHU PANIAN 10 Dr ghazala idrees BHU TOFKIAN 11 Dr abdul qayyyum BHU SARAYE SALIH 12 Dr naushad ali BHU MANKARAI 13 Dr tariq mahmood BHU KHATTAR 14 Dr roshan zada RHC KOT NAJEEBULLAH 15 Dr Khalid mahmood BHU BARA KOT 16 Dr ijaz khan BHU BURG 17 Dr shazia zaheer BHU DARTIAN 18 -

Public Notice Auction of Gold Ornament & Valuables

PUBLIC NOTICE AUCTION OF GOLD ORNAMENT & VALUABLES Finance facilities were extended by JS Bank Limited to its customers mentioned below against the security of deposit and pledge of Gold ornaments/valuables. The customers have neglected and failed to repay the finances extended to them by JS Bank Limited along with the mark-up thereon. The current outstanding liability of such customers is mentioned below. Notice is hereby given to the under mentioned customers that if payment of the entire outstanding amount of finance along with mark-up is not made by them to JS Bank Limited within 15 days of the publication of this notice, JS Bank Limited shall auction the Gold ornaments/valuables after issuing public notice regarding the date and time of the public auction and the proceeds realized from such auction shall be applied towards the outstanding amount due and payable by the customers to JS Bank Limited. No further public notice shall be issued to call upon the customers to make payment of the outstanding amounts due and payable to JS Bank as mentioned hereunder: Customer Sr. No. Customer's Name Address Balance as on 20th August 2020 Number 1 1038553 ZAHID HUSSAIN MUHALLA MASANDPURSHI KARPUR SHIKARPUR 298,614 2 1012051 ZEESHAN ALI HYDERI MUHALLA SHIKA RPUR SHIKARPUR PK SHIKARPUR 298,107 3 1008854 NANIK RAM VILLAGE JARWAR PSOT OFFICE JARWAR GHOTKI 65110 PAK SITAN GHOTKI 553,300 4 999474 DARYA KHAN THENDA PO HABIB KOT TALUKA LAKHI DISTRICT SHIKARPU R 781000 SHIKARPUR PAKISTAN SHIKARPUR 270,709 5 1181615 FAISAL MEHMOOD GHQ SIGNAL BATTALION -

Pak Pos and RMS Offices 3Rd Ed 1962

Instructions for Sorting Clerks and Sorters ARTICLES ADDRl!SSBD TO TWO PosT-TOWNS.-If the address Dead Letter Offices receiving articles of the description re 01(an article contains the names of two post-town, the article ferred in this clause shall be guided by these instructions so far should, as a general rule, be forwarded to whichever of the two as the circumstances of each case admit of their application. towns is named last unless the last post-town- Officers employed in Dead Letter Offices are selected for their special fitness for the work and are expected to exercise intelli ( a) is obviously meant to indicate the district, in which gence and discretion in the disposal of articles received by case the article should be . forwar ~ ed ~ · :, the first them. named post-town, e. g.- A. K. Malik, Nowshera, Pes!iaivar. 3. ARTICLES ADDRESSED TO A TERRITORIAL DIVISION WITH (b) is intended merely as a guide to the locality, in which OUT THE ADDITION OF A PosT-TOWN.-If an article is addressed case the article should be forwarded to the first to one of the provinces, districts, or other territorial divisions named post-town, e. g.- mentioned in Appendix I and the address does not contain the name of any post-town, it should be forwarded to the post-town A. U. Khan, Khanpur, Bahawalpur. mentioned opposite, with the exception of articles addressed to (c) Case in which the first-named post-town forms a a military command which are to be sent to its headquarters. component part of the addressee's designation come under the general rule, e. -

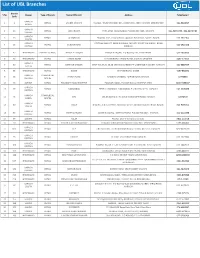

To Download UBL Branch List

List of UBL Branches Branch S No Region Type of Branch Name Of Branch Address Telephone # Code KARACHI 1 2 RETAIL LANDHI KARACHI H-G/9-D, TRUST CERAMIC IND., LANDHI IND. AREA KARACHI (EPZ) EXPORT 021-5018697 NORTH KARACHI 2 19 RETAIL JODIA BAZAR PARA LANE, JODIA BAZAR, P.O.BOX NO.4627, KARACHI. 021-32434679 , 021-32439484 CENTRAL KARACHI 3 23 RETAIL AL-HAROON Shop No. 39/1, Ground Floor, Opposite BVS School, Sadder, Karachi 021-2727106 SOUTH KARACHI CENTRAL BANK OF INDIA BUILDING, OPP CITY COURT,MA JINNAH ROAD 4 25 RETAIL BUNDER ROAD 021-2623128 CENTRAL KARACHI. 5 47 HYDERABAD AMEEN - ISLAMIC PRINCE ALLY ROAD PRINCE ALI ROAD, P.O.BOX NO.131, HYDERABAD. 022-2633606 6 46 HYDERABAD RETAIL TANDO ADAM STATION ROAD TANDO ADAM, DISTRICT SANGHAR. 0235-574313 KARACHI 7 52 RETAIL DEFENCE GARDEN SHOP NO.29,30, 35,36 DEFENCE GARDEN PH-1 DEFENCE H.SOCIETY KARACHI 021-5888434 SOUTH 8 55 HYDERABAD RETAIL BADIN STATION ROAD, BADIN. 0297-861871 KARACHI COMMERCIAL 9 65 NAPIER ROAD KASSIM CHAMBERS, NAPIER ROAD,KARACHI. 32775993 CENTRAL CENTRE 10 66 SUKKUR RETAIL FOUJDARY ROAD KHAIRPUR FOAJDARI ROAD, P.O.BOX NO.14, KHAIRPUR MIRS. 0243-9280047 KARACHI 11 69 RETAIL NAZIMABAD FIRST CHOWRANGI, NAZIMABAD, P.O.BOX NO.2135, KARACHI. 021-6608288 CENTRAL KARACHI COMMERCIAL 12 71 SITE UBL BUILDING S.I.T.E.AREA MANGHOPIR ROAD, KARACHI 32570719 NORTH CENTRE KARACHI 13 80 RETAIL VAULT Shop No. 2, Ground Floor, Nonwhite Center Abdullah Harpoon Road, Karachi. 021-9205312 SOUTH KARACHI 14 85 RETAIL MARRIOT ROAD GILANI BUILDING, MARRIOT ROAD, P.O.BOX NO.5037, KARACHI. -

Addresses of DPW Offices, RHSC-As, Msus, Fwcs & Counters in Khyber

Addresses of Service Delivery Network Including Newly Merged Districts (DPW Offices, RHSC-As, MSUs, FWCs & Counters) (Technical Section) Directorate of Population Welfare Department Government of Khyber Pakhtunkhwa (August, 2019) Plot No 18, Sector E-8, Street No 05, Phase 7, Hayatabad. Phone: 091-9219052, Fax: 091-9219066 1 Content S.No Contents Page No 1. Updated Addresses of District Population Welfare Offices in 3 Khyber Pakhtunkhwa 2. Updated Addresses of Reproductive Health Services Outlets 4 (RHSC-As) in Khyber Pakhtunkhwa 3. Updated Addresses of Mobile Service Units in Khyber 5 Pakhtunkhwa 4. Updated Addresses of Family Welfare Centers in Khyber 7 Pakhtunkhwa 5. Updated Addresses of Counters in Khyber Pakhtunkhwa 28 6. Updated Addresses of District Population Welfare Offices in 29 Merged Districts (Erstwhile FATA) 7. Updated Addresses of Reproductive Health Services Outlets 30 (RHSC-As) in Merged Districts (Erstwhile FATA) 8. Updated Addresses of Mobile Service Units in Merged Districts 31 (Erstwhile FATA) 9. Updated Addresses of Family Welfare Centers in Merged Districts 32 (Erstwhile FATA) 2 Updated Addresses of District Population Welfare Offices in Khyber Pakhtunkhwa S.No Name of DPW Office Complete Address Abbottabad Wajid Iqbal House Azam Town Thanda Chowa PMA Road 1 KakulAbbottabad Phone and fax No.0992-401897 2 Bannu Banglow No.21, Defence Officers Colony Bannu Cantt:. (Ph: No.0928-9270330) 3 Buner Mohallah Tawheed Abad Sawari Buner 4 Battagram Opposite Sub-Jail, Near Lahore Scholars Schools System, Tehsil and District Battagram 5 Chitral Village Goldor, P.O Chitral, Teh& District Lower Chitral 6 Charsadda Opposite Excise & Taxation Office Nowshera Road Charsadda 7 D.I Khan Zakori Town, Draban Road, DIKhan 8 Dir Lower Main GT Road Malik Plaza Khungi Paeen Phone.