Fy 2019 Local Councils' Bilateral Budget Discussions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual School Census-2020-Report

Government of Sierra Leone Ministry of Basic and Senior Secondary Education 2020 Annual School Census Report March 2021 Contents List of Tables ............................................................................................................................... 5 List of Figures ............................................................................................................................. 7 PREFACE ....................................................................................................................................... 9 ACKNOWLEDGEMENT ............................................................................................................ 11 List of Acronyms .......................................................................................................................... 12 Executive Summary ...................................................................................................................... 13 Section One: Introduction ............................................................................................................. 17 Chapter 1 Background and Methodology ..................................................................................... 17 1.1 Background Information ..................................................................................................... 17 1.2 Specific Objectives .............................................................................................................. 19 1.3 Scope of the School Census ............................................................................................... -

Download PDF File

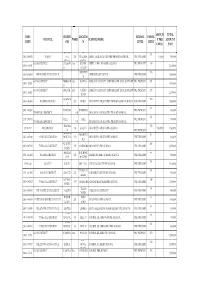

AMOUN TOTAL EMIS CHIEFD LOCATIO SCHOOL ENROL COUNCIL WARD SCHOOL NAME T PER AMOUNT CODE OM N LEVEL MENT CHILD PAID WATERL 45 85 5103-3-09029 WARDC OO 391 WILLIAM ABDUL JALIL ACADEMY PRE-PRIMARY SCHOOL PRE-PRIMARY 10,000 850,000 RURAL STREET KONO DISTRICT TANKOR East DOWN ABDULAI IBN ABASS PRE-SCHOOL PRE PRIMARY 110 1391-1-01995 1,100,000 O BALOP ABERDEE 106 5208-2-10849 FREETOWN CITY COUNCIL ABERDEEN MUNICIPAL PRE-PRIMARY 1,060,000 N KONO DISTRICT NIMIKOR East KOMAO AFRICA COMMUNITY EMPOERMENT DEVELOPMENT PRE PRIMARY 151 1309-1-02125 1,510,000 O KONO DISTRICT GBENSE East YARDU AFRICA COMMUNITY EMPOERMENT DEVELOPMENT PRE PRIMARY 127 1391-1-01802 1,270,000 ROAD MAGBEM 102 3105-1-02506 KAMBIA DISTRICT 201 ROBAT AHMADIYYA MUSLIM PRE PRIMARY SCHOOL-ROBAT PRE-PRIMARY 1,020,000 A 60 2401-1-05230 DANSOGO BUMBUNA PRE-PRIMARY 600,000 TONKOLILI DISTRICT 185 AHMADIYYA MUSLIM PRE-PRIMARY SCHOOL 54 2417-1-05764 YELE YELE PRE-PRIMARY 540,000 TONKOLILI DISTRICT 176 AHMADIYYA MUSLIM PRE-PRIMARY SCHOOL TIKONK 150 311301112 BO DISTRICT 289 KAKUA AHMADIYYA MUSLIM PRE-SCHOOL 10,000.00 1,500,000 O PRE-PRIMARY KHOLIFA MAGBURA 83 2407-1-05340 TONKOLILI DISTRICT ROWALL 170 AHMADIYYA MUSLIM PRE-SCHOOL PRE-PRIMARY 830,000 KA A KUNIKE- 105 2410-1-05521 TONKOLILI DISTRICT 179 MASINGBI AHMADIYYA PRE-SCHOOL PRE-PRIMARY 1,050,000 SANDA MAKENI ROGBOM/ 83 2191-1-04484 BOMBALI DISTRICT 123 ALHADI ISLAMIC NURSERY SCHOOL PRE-PRIMARY 830,000 CITY MAKENI 151 319101126 BO CITY KAKUA BO NO 2 ALHAJI NAZI-ALIE PRE-SCHOOL PRE-PRIMARY 1,510,000 TIMBO/M 80 2191-1-04505 BOMBALI DISTRICT -

SIERRA LEONE TEACHING SERVICE COMMISSION (TSC) No

SIERRA LEONE TEACHING SERVICE COMMISSION (TSC) No. Name Position Phone No. Email Address HEAD QUARTER 1 Dr. Staneala M. Beckley Chairperson +232(0)79-686-031 [email protected] 2 Sorie I. Turay Secretary +232(0)76-608-439 [email protected] 3 Director, Registration and Licensing Department Dep. Dir. Teacher Registration & Licensing 4 Hectora Pyne Bailey +232(0)76-636-212 [email protected] Department 5 Marian Sallay Abu Director Teacher Management Department +232(0)76-605-647 [email protected] 6 Alimamy Bundu Kamara Dep. Dir. Teacher. Management Department +232(0)76-852-973 [email protected] 7 Edwin Kpana Massaquoi Director, Corporate Services Department +232(0)76-630-185 [email protected] 8 Clarence Kalawa Dep. Dir. Corporate Services Department +232(0)88-666-655 [email protected] Director, Teacher Development & Performance 9 Department Dep. Dir. Teacher Development & Performance 10 Dr. Dennis S. Luseni +232(0)76-789-520 [email protected] Department Director, Teacher-Employer Relations 11 Princess Mattia +232(0)76-400-050 [email protected] Department 12 Samuel A Sesay Deputy Director Teacher Employer Relations +232(0)78317306 [email protected] 13 Philip Goba Internal Auditor +232(0)79556161 [email protected] +232(0)78-471-106 14 Baimaro Koroma IT Manager [email protected] +232(0)77-550-089 15 Patrick Manika Bangura Facilities & Procurement Manager +232(0)76-509-742 [email protected] 16 Kelvin K. MacCormack HR Manager +232(0)79- 947-588 [email protected] 17 Gloria H. -

Preliminary Statement

European Union Election Observation Mission Sierra Leone Presidential, Parliamentary and Local Council Elections 2018 PRELIMINARY STATEMENT Election day went smoothly but the entire process was overshadowed by tensions and political attacks on the electoral commission Freetown, 3 April 2018 Summary This Preliminary Statement is delivered prior to the completion of the election process. It should be read in conjunction with the EU EOM Preliminary Statement issued on 9 March 2018. The final assessment of the elections will depend in part on the conduct of the remaining stages of the election process, in particular, the tabulation of results, and the handling of possible post-election day complaints and appeals. The EU Election Observation Mission (EOM) remains in country to observe post-election developments and will publish a Final Report, containing detailed recommendations, within two months of the conclusion of the electoral process. The run-off election took place on 31 March between the two candidates who received the most votes in the presidential election of 7 March 2018 - retired Brigadier Julius Maada Bio of the Sierra Leone People’s Party (SLPP) who gained 43.3% in the first-round, and Dr Samura Kamara of the incumbent All People’s Congress (APC) with 42.7%. Together with the vice presidential running mates, all four candidates are men. • The main institution administering the election, the National Electoral Commission (NEC) proved its genuine commitment to a transparent and inclusive election, a vital component of democratic consolidation. Contesting candidates and political parties however remained more ambiguous, publicly calling for peace but also fuelling a divisive discourse and unwarranted attacks and demands on the NEC. -

State Opening of Parliament 1

STATE OPENING OF PARLIAMENT 1 GOVERNMENT OF SIERRA LEONE PRESIDENTIAL ADDRESS DELIVERED BY HIS EXCELLENCY, BRIG (Retd) DR. JULIUS MAADA BIO, GCRSL, President of The Republic and Commander-In-Chief of the Republic of Sierra Leone Armed Forces On the Occasion of the State Opening of the Third Session of the Fifth Parliament of the Second Republic of Sierra Leone In the Chamber of Parliament Building Tower Hill, Freetown On Thursday, 28th May 2020 At 10:00am STATE OPENING OF PARLIAMENT 2 Mr. Speaker. Honourable Vice President. Honourable Chief Justice, Ministers of Government, Honourable Members of Parliament Your Worship, The Mayor of the Municipality of Freetown The First Lady, Distinguished Ladies and Gentlemen, As we assemble in this Great Hall that symbolizes our unity in diversity, I would ask that we rise and observe a moment of silence for our compatriots and all other citizens of the global community who have succumbed to the COVID-19 Pandemic. May their souls and the souls of all the faithful departed, through the Mercy of God/Allah rest in peace. Mr. Speaker, Honourable Members of Parliament, today’s event is taking place in a sombre atmosphere. It is observed amidst the ravages of COVID-19, not only in Sierra Leone but also the world over. That notwithstanding, I am confident that like the trials of our immediate past, this period provides yet another opportunity for all Sierra Leoneans, irrespective of religion, ethnicity and region of origin to come together for the sake of our common destiny and for the sake of humanity. While it is my prayer and hope that together with the global community, we shall combat and eliminate this global pandemic, it is equally my prayer and hope that the opportunity created for, and by our coming together will engender us to build a Sierra Leone that works for all of us. -

Annual School Census Report 2019

Republic of Sierra Leone Ministry of Basic and Senior Secondary Education 2019 Annual Schools Census Report And Statistical Abstract November 2019 ii Table of Contents Preface............................................................................................................................................ iii Acknowledgement .......................................................................................................................... v List of Acronyms ........................................................................................................................... vi Executive Summary ...................................................................................................................... vii 1. Introduction .............................................................................................................................. 1 1.1 Background Information .................................................................................................. 1 1.2 Specific Objectives ........................................................................................................... 1 1.3 Scope of the School Census ............................................................................................. 1 1.4 Data Collection Tools....................................................................................................... 2 1.5 Coverage........................................................................................................................... 2 2. Field Methodology -

Emis Code Council Chiefdom Ward Location School Name

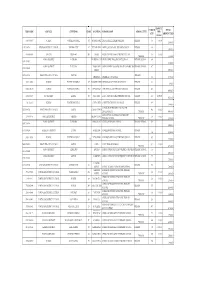

AMOUNT ENROLM TOTAL EMIS CODE COUNCIL CHIEFDOM WARD LOCATION SCHOOL NAME SCHOOL LEVEL PER ENT AMOUNT PAID CHILD 5103-2-09037 WARDC WATERLOO RURAL 391 ROGBANGBA ABDUL JALIL ACADEMY PRIMARY PRIMARY 369 10,000 3,690,000 1291-2-00714 KENEMA DISTRICT COUNCIL KENEMA CITY 67 FULAWAHUN ABDUL JALIL ISLAMIC PRIMARY SCHOOL PRIMARY 380 3,800,000 4114-2-06856 BO CITY TIKONKO 289 SAMIE ABDUL TAWAB HAIKAL PRIMARY SCHOOL 610 10,000 PRIMARY 6,100,000 KONO DISTRICT TANKORO DOWN BALLOP ABDULAI IBN ABASS PRIMARY SCHOOL PRIMARY SCHOOL 694 1391-2-02007 6,940,000 KONO DISTRICT TANKORO TAMBA ABU ABDULAI IBNU MASSOUD ANSARUL ISLAMIC MISPRIMARY SCHOOL 407 1391-2-02009 STREET 4,070,000 5208-2-10866 FREETOWN CITY COUNCIL WEST III PRIMARY ABERDEEN ABERDEEN MUNICIPAL 366 3,660,000 5103-2-09002 WARDC WATERLOO RURAL 397 KOSSOH TOWN ABIDING GRACE PRIMARY SCHOOL PRIMARY 62 620,000 5103-2-08963 WARDC WATERLOO RURAL 373 BENGUEMA ABNAWEE ISLAMIC PRIMARY SCHOOOL PRIMARY 405 4,050,000 4109-2-06695 BO DISTRICT KAKUA 303 KPETEMA ACEF / MOUNT HORED PRIMARY SCHOOL PRIMARY 411 10,000.00 4,110,000 Not found WARDC WATERLOO RURAL COLE TOWN ACHIEVERS PRIMARY TUTORAGE PRIMARY 388 3,880,000 ACTION FOR CHILDREN AND YOUTH 5205-2-09766 FREETOWN CITY COUNCIL EAST III CALABA TOWN 460 10,000 DEVELOPMENT PRIMARY 4,600,000 ADA GORVIE MEMORIAL PREPARATORY 320401214 BONTHE DISTRICT IMPERRI MORIBA TOWN 320 10,000 PRIMARY SCHOOL PRIMARY 3,200,000 KONO DISTRICT TANKORO BONGALOW ADULLAM PRIMARY SCHOOL PRIMARY SCHOOL 323 1391-2-01954 3,230,000 1109-2-00266 KAILAHUN DISTRICT LUAWA KAILAHUN ADULLAM PRIMARY -

Local Government and Paramount Chieftaincy in Sierra Leone: a Concise Introduction

Local Government and Paramount Chieftaincy in Sierra Leone: A Concise Introduction P. C. Gbawuru Mansaray III (alias Pagay) P. C. Alimamy Lahai Mansaray V Dembelia Sinkunia Chiefdom P. C. Madam Doris Lenga-Caulker P. C. Henry Fangawa of Gbabiyor II of Kagboro Chiefdom, Wandor Chiefdom, Falla Shenge (Moyamba District), (Kenema District), P. C. Theresa Vibbi III. of Kandu Leppiama, Gbadu Levuma (Kenema District) M. N. Conteh Revised Edition 2019 Local Government and Paramount Chieftaincy in Sierra Leone: A Concise Introduction A cross-section of Paramount Chiefs of Sierra Leone displaying their new staffs M. N. Conteh Revised Edition 2019 Table of Contents Page Contents i Acronyms ii Preface and acknowledgements iii About the Author v Chapter 1. 1 Local Government in Sierra Leone Chapter 2. 38 Paramount Chieftaincy in Sierra Leone: an introduction to its history and Electoral Process. Chapter 3. 80 Appendices Appendix 1: List of Chiefdoms and their Ruling Houses 82 Appendix 2: NEC Form PC 3 – statutory Declaration of Rights for 103 PC elections Appendix 3: List of symbols for PC elections (and Independent 105 candidates for Local Councils). Appendix 4: Joint Reporting Format for PC elections 107 Appendix 5 and 6: Single and multi-member wards for District 111 Councils. Appendix 7 Nomination Form for Local Council Candidate 114 References and Suggested books for further reading 1 16 i Acronyms APC – All Peoples’ Congress CC – Chiefdom Council / Chiefdom Committee DC – District Commissioner /District Council DEO – District Electoral Officer -

Ministry of Energy

Public Disclosure Authorized GOVERNMENT OF SIERRA LEONE Ministry of Energy ENHANCING SIERRA LEONE ENERGY ACCESS (P171059) Public Disclosure Authorized Environmental and Social Management Framework Public Disclosure Authorized November 2020 Public Disclosure Authorized Table of Contents ACRONYMS AND ABBREVIATIONS ...................................................................................................... VI EXECUTIVE SUMMARY ................................................................................................................................ IX SECTION ONE ................................................................................................................................................. 14 INTRODUCTION ............................................................................................................................................ 14 1.1 BACKGROUND ................................................................................................................................... 14 1.2 SECTORAL CONTEXT ......................................................................................................................... 16 1.2.1 Energy Policy Objectives .............................................................................................................. 17 1.2.2 Evolution of the energy sector in Sierra Leone ............................................................................. 17 1.2.3 Sierra Leone’s Medium-Term National Development Plan 2019-2023 ...................................... -

(Amendment) Act, 2017

ACT Supplement to the Sierra Leone Gazette Vol. CXLVIII, No. 34 dated 22nd June, 2017 SIGNED this 16th day ofJune, 2017. DR. ERNEST BAI KOROMA, President. No. 2 2017 Sierra Leone The Local Government (Amendment) Act, 2017. Short title. Being an Act to amend the Local Government Act, 2004, to provide for the addition of new Districts created under the Provinces (Administrative Division) Order, 2017 and other related mJtters. ENACTED by the President and Members of Parliament in this present Parliament assembled . • I 2 No. 2 Local Government (Amendmen~ Act 2017 Amendment t. The First Schedule to the Local Government Act 2004 is of First Schedule of Act No.I of amended- 2004. (a) in Part I - (0 in paragraph A by inserting - "Falaba District" immediately after "Kenema District''; "Karene District" immediately after J(oinadugu District- (iI) in paragraph B by inserting immediately after "Freetown City" the following new cities- Bo City; Bonthe City; Kenema City; Koidu-New SembehW1 City; Makeni City; Port Loko City. (b) in Part II by repealing and replacing that part with the following new p::i.rt - . ' No. 2 Local Government (Amendment) Act 2017 3 PARTII The number of Paramount Chiefs in each Local Council shall be as follows- COUNCIL NUMBER OF PARAMOUNT CHIEFS 1. Bo District Council Three 2. Bombali District Council Two 3. Bonthe District Council Two 4. Kailahun District Council Three 5. Kambia District CoWlcil Two 6. Kenema District Council Three 7. Falaba District Council Two 8. Koinadugu District Council Two 9. Karene District Council Two 10. Kono District Council Three 11. -

2021 VNR REPORT on Sdgs in SIERRA LEONE

UNITED NATIONS SUSTAINABLE DEVELOPMENT GOALS -------- THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 2021 VNR REPORT ON SDGs IN SIERRA LEONE GOVERNMENT OF SIERRA LEONE MINISTRY OF PLANNING AND ECONOMIC DEVELOPMENT ----------- JUNE 2021 Foreword Despite the ravages of the COVID-19 pandemic, Sierra Leone has been able to prepare its third Voluntary National Review (VNR) report for presentation at the 2021 High-Level Political Forum on the SDGs. We will be among the countries presenting progress report on these UN Goals the highest number of times, which demonstrates our Government’s sustained commitment to the UN 2030 Agenda for Sustainable Development. We have continued to follow a strategic approach to implementing the SDGs, as we remain steadfast in upholding two of the 17 Goals as our accelerators that are deemed cardinal in the transformation of our economy and building long-term resilience for sustainable development. The two accelerators are: SDG 4 (inclusive education) and SDG16 (justice, peace and inclusive society) which are also key in the process of advancing the achievement of other SDGs. The report also covers nine other priority goals for 2021, namely: Goal 1 (ending poverty), 2 (zero hunger), 3 (health), 5 (gender), 8 (decent work), 10 (inequality), 12 (responsible consumption and production), 13 (climate change) and 17 (means of implementation). With the full participation of stakeholders, we successfully generated large data set from nationwide consultations on the 11 Goals, leading to a comprehensive report that was validated by all the institutions involved in the process, including government ministries, departments and agencies; parliament, local councils, civil society organisations including those for persons with disabilities; and the private sector, the media, research institutions and development partners. -

2017 Constituency Boundary Delimitation Report, Vol. 2

NATIONAL ELECTORAL COMMISSION Republic of Sierra Leone Constituency Boundary Delimitation Report Volume 2 August, 2017 Foreword The National Electoral Commission (NEC) is submitting this report on the delimitation of constituency and ward boundaries in adherence to its constitutional mandate to delimit electoral constituency and ward boundaries, to be done “not less than five years and not more than seven years”; and complying with the timeline as stipulated in the NEC Electoral Calendar (2015-2019). The report is subject to Parliamentary approval, as enshrined in the 1991 Constitution of Sierra Leone (Act No 6 of 1991); which inter alia states delimitation of electoral boundaries to be done by NEC, while Section 38 (1) empowers the Commission to divide the country into constituencies for the purpose of electing Members of Parliament (MPs) using Single Member First- Past –the Post (FPTP) system. The Local Government Act of 2004, Part 1 –preliminary, assigns the task of drawing wards to NEC; while the Public Elections Act, 2012 (Section 14, sub-sections 1 &2) forms the legal basis for the allocation of council seats and delimitation of wards in Sierra Leone. The Commission appreciates the level of technical assistance, collaboration and cooperation it received from Statistics Sierra Leone (SSL), the Boundary Delimitation Technical Committee (BDTC), the Boundary Delimitation Monitoring Committee (BDMC), donor partners, line Ministries, Departments and Agencies and other key actors in the boundary delimitation exercise. The hiring of a Consultant, Dr Lisa Handley, an internationally renowned Boundary delimitation expert, added credence and credibility to the process as she provided professional advice which assisted in maintaining international standards and best practices.